Want to live comfortably during your golden years? Start planning early.

Retiring comfortably is a cherished dream for every Singaporean. We all look forward to the day we don’t have to worry about work anymore and can spend more time with family, friends and our community. Perhaps indulge in more leisurely pursuits like reading, gardening or exercise. But it’s likely that many of us have not actively thought about retirement planning. Why? Because it’s too far away to think about? Or maybe we don’t believe we can ever retire because of household bills, medical costs and fees for children’s education.

Is retirement really out of reach for the average Singaporean? What are the myths that hinder our ability to start planning and getting ready for retirement?

Myth 1: I'm still young, it’s too early to start retirement planning

Fact: You may think your retirement age is still far but time passes faster than you think. Small steps you take now can make a big difference in the long run.

The most common reason why people under the age of 40 aren’t actively planning and saving up for their retirement is this: they think it’s too early.

Psychology is partly to blame here - researchers have found we all have a ‘present bias’, which makes it difficult for us to act for the good of tomorrow. Even though we consciously agree that retirement planning and building a nest egg for our golden years is important, we put off starting a retirement savings plan today, believing time is on our side.

And therein lies the problem. All we’re really doing is reducing our chances of having a more comfortable retirement or worse, burdening others, like our children, to plan for us.

How much do I need to retire?

Planning your finances for retirement can be rather complex. We encourage you to use this detailed retirement calculator found at CPF’s website to find out how much you need to retire. There is a lot of information to fill in, but the more details you include, the clearer and more accurate your results will be.

Having said that, we’ve also included a simplified example to illustrate a typical retirement scenario in Singapore.

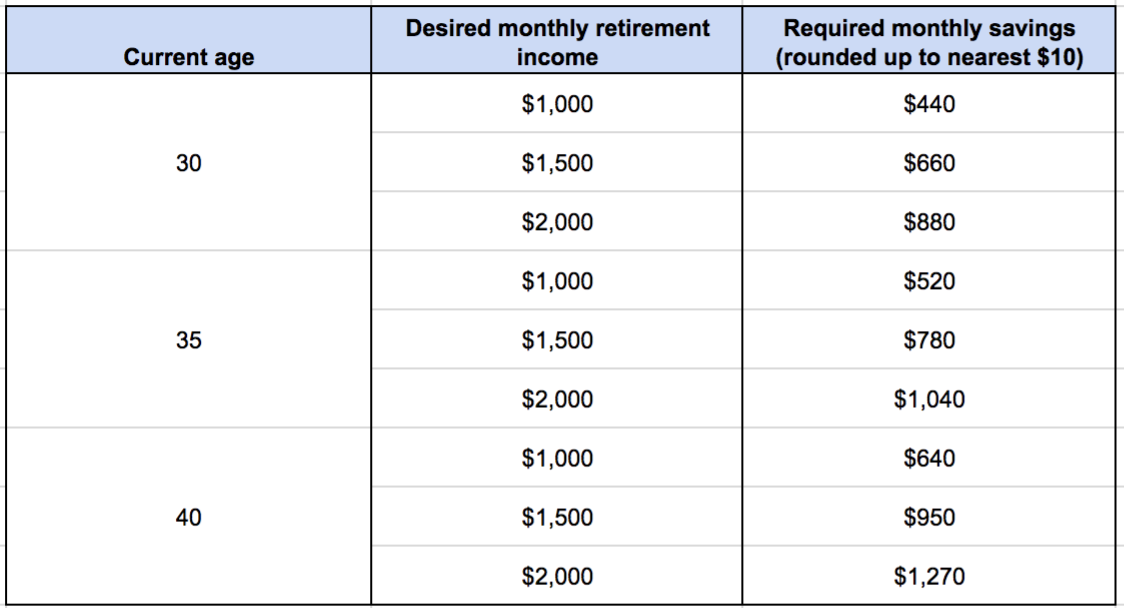

In the following table, we show you how much you need to save per month, for a monthly retirement income of $1,000 or $1,500 or $2,000, and starting at 30 or 35 or 40 years old.

Now, a couple of important caveats:

- Calculation excludes CPF savings. Your CPF savings that are set aside for retirement will be used to join CPF LIFE or Retirement Sum Scheme to provide you with monthly payouts from age 65 (for those born in or after 1954).

- We are assuming retirement at age 65 and for a period of 20 years.

- We’ve included inflation at 2% per year.

- We’ve included pre- and post-retirement investment returns at 4%.

From the above example, you can clearly see the later you start, the harder it is for you to reach your goals.

Still think 65 is a long time away? Well, did you choose Bulbasaur, Charmander or Squirtle when you first started playing Pokemon on the Gameboy?

Yeah… that was 23 years ago.

Myth 2: I can’t afford to retire; I don’t have enough to set aside as savings

Fact: Given enough time, compound interest can make a little go a long way.

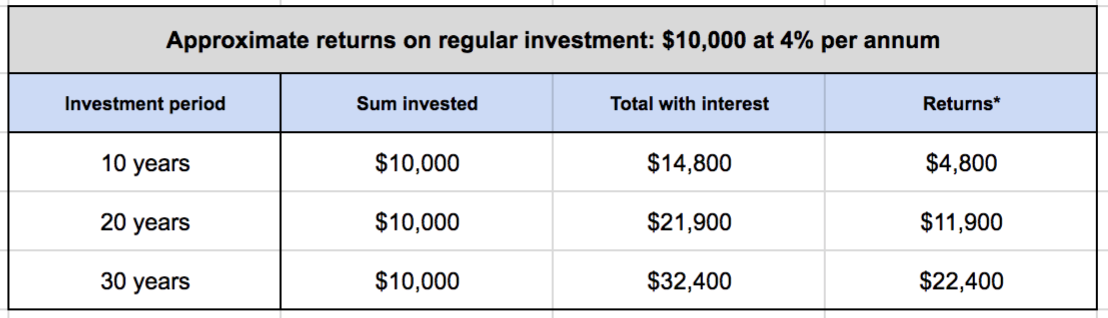

Here’s where it’s key to understand that starting a retirement savings plan early is more important than how much you actually save -- thanks to the power of compound interest.

Let’s say you squirrel away $1,000 per year in a fixed fund that gives you 4% p.a. returns. Here’s how much you will be getting back after 10, 20 and 30 years’ time.

(*Rounded down to nearest $100)

Pay attention to the right-most column, because that’s where the magic happens. Do you see how much more your money grew over 30 years? Compound interest helps to grow your savings significantly over time, and the effect is amplified the earlier you start. Starting to save for retirement 10, or even 5 years earlier makes a big, big difference.

Myth 3: I’m contributing CPF every month; that’s enough for retirement planning

Fact: We all have access to tools that can help maximise our retirement funds.

With mandatory CPF contributions, Singaporeans are building up their retirement nest egg with every pay cheque. We also have CPF LIFE, which provides us with lifelong payouts in our golden years, while MediSave savings and MediShield Life helps us with our medical needs.

A portion of our income is saved in our CPF Ordinary Account (OA), and it’s earning interest at a decent 2.5% p.a, higher than say, fixed deposit accounts. (Sure, you can get higher returns if you invest smartly, but how many of us have the time, skill and patience to play the market without getting burnt?)

Still, if you want to increase your returns and build a larger retirement nest egg, you can. Under the Retirement Sum Topping-Up Scheme, if your OA funds aren’t being used, you can transfer them to your Special Account (SA) (if you’re below 55 years old) to enjoy interest of up to 5%* per annum. Alternatively, you can top-up your SA with cash. For those age 55 and above, you can top up via CPF transfer or cash to your Retirement Account (RA).

(*This figure includes the extra 1% interest paid on the first $60,000 of a member’s combined balances, with $20,000 from the OA. An additional 1% interest is also paid on the first $30,000 of combined CPF balances for members aged 55 and above. Read more on CPF interest rates here. Also note CPF transfers and top-ups to SA/RA are irreversible, so make sure you won’t be needing those funds before transferring or topping up.)

How two Singaporeans approached retirement planning

Accountant Steven Wee, 44, said he and his wife, who works as a secretary, started planning for retirement when they hit their early 40s.

“We started doing top-ups to our CPF Special Accounts through the Retirement Sum Topping-Up Scheme. Initially, it was one-off top-ups when we received our year-end bonus,” said the father of two boys aged 16 and 10.

“Now that our kids are older, we can afford to make more regular top-ups. We’re aiming for a comfortable passive monthly income of $3,500 for both of us once we retire,” he added, estimating that they need a retirement nest egg of $840,000 if they were to retire at the age of 65. Given that they plan to work for the next 20 years, and that the monthly contributions to their Special Accounts will grow as they get older, Wee said he’s confident of reaching the magic sum of $840,000 by the time they hit 65.

On the other hand, Goh Kim Lye, an office manager in his mid-50s, wished he had started saving for retirement earlier.

“It was tough saving every month when my two children were growing up. My wife stayed at home to look after our children, so I was the only breadwinner,” he said.

“Now my elder son is about to get married and start his own family. My wife and I don’t want to burden him financially. We have some money in my CPF account and I try to save more of my salary in my personal savings account every month. I hope it will be enough during my golden years,” he added.

“On hindsight, if I had started earlier, I could have started with smaller amounts and taken advantage of compound interest to grow my nest egg,” said Goh, who hopes to bring his wife to travel around the world in retirement, as a reward to his wife, who sacrificed her career to raise their two children.

The future is closer than you think: Act today

We’ve all heard of the saying “time flies”. Nowhere is this truer than when it comes to retirement planning. Before you know it, your kids have all grown up and living their own lives.

So, act today. Have a plan today. With the power of compound interest and financial tools with attractive interest rates (like your CPF accounts), you can grow your nest egg and stand a very real chance of enjoying a comfortable retirement.

To find out how you can grow your retirement nest egg with CPF, visit cpf.gov.sg/BeReady

This article was developed in partnership with CPF Board.

By Alevin Chan

By Alevin Chan

A Certified Financial Planner with a curiosity about what makes people tick, Alevin's mission is to help readers understand the psychology of money. He's also on an ongoing quest to optimize happiness and enjoyment in his life.

Similar articles

Will I Ever Retire in Singapore?

Retirement Age: What’s The “Correct” Age to Retire in Singapore?

What Are You Doing to Plan For Your Retirement?

Retirement Planning in Singapore: Does The 4% Withdrawal Rule Still Make Sense?

FIRE: Are You Planning Your Early Retirement All Wrong?

Singapore-based Author and Financial Analyst Retired At 33… Here’s How He Did It

‘Want To Be Financially Free? Start Planning For Retirement As Soon As You Start Work’

CPF Has No Equal as Investment Vehicle: Singapore’s Mr. CPF

Back to Blog

Back to Blog -2.png?width=280&name=Insurance%20(2)-2.png)