The definition of "critical illness" in life insurance policies is set to change from August 26, 2020. In short, the definitions have been tightened to provide greater clarity.

In August 2019, the Life Insurance Association (LIA) of Singapore announced that changes will be made to the definition of critical illness in life insurance policies. This is to take into account the advances in medical treatment and technology which may impact how certain critical illnesses can be treated, managed or mitigated.

All member companies of LIA Singapore and the General Insurance Association of Singapore will adopt the new standardised set of revised definitions.

Policyholders with existing critical illness policies will not impacted by the new definitions. However, all critical illness products based on definitions used from 2014, when the last update was done, may no longer be sold in Singapore from 26 August 2020.

"Especially with the rapidly ageing population and rising incidences of chronic illnesses here, regular reviews of the critical illnesses definitions will ensure that critical illnesses products stay relevant with changing times, and that the intended scope of coverage is clear to consumers," said Mr Khor Hock Seng, president of LIA Singapore.

What is critical illness insurance?

Critical illness insurance pays a lump sum if you're diagnosed with a critical illness (see list of 37 critical illnesses covered below) or after having undergone a type of surgery covered by the policy.

Key features include:

- Payment of lump sum if you are diagnosed with an illness covered by the policy. Or after first having a type of surgery covered by the policy.

- Benefits are paid only if the illness or surgery meets the definition stated in the policy.

- There is usually a waiting period for specific illnesses or types of surgery. If any illness is diagnosed or a type of surgery is carried out during the waiting period, no benefits will be paid.

- Some critical illness policies pay a smaller amount for earlier stages of cancer, or make several payments upon diagnosis of different insured critical illnesses, subject to the sum insured or policy limits.

Five most common critical illnesses in Singapore

This is not the first time the LIA of Singapore has reviewed the definition of critical illnesses. In the last update in 2014, many of the 37 severe stage critical illness definitions were revised. Then, it also removed the maximum limit of 30 medical conditions per critical illnesses plan to allow for more medical conditions to be covered.

Over 90 per cent of all severe stage claims received by life insurers in Singapore are for the following five critical illnesses:

- major cancer

- heart attack of specified severity

- stroke with permanent neurological deficit

- coronary artery bypass surgery

- end-stage kidney failure

List of 37 critical illness conditions

The following is the updated industry list of 37 critical illness conditions:

- Major Cancer

- Heart Attack of Specified Severity

- Stroke with Permanent Neurological Deficit

- Coronary Artery By-pass Surgery

- End Stage Kidney Failure

- Irreversible Aplastic Anaemia

- End Stage Lung Disease

- End Stage Liver Failure

- Coma

- Deafness (Irreversible Loss of Hearing)

- Open Chest Heart Valve Surgery

- Irreversible Loss of Speech

- Major Burns

- Major Organ / Bone Marrow Transplantation

- Multiple Sclerosis

- Muscular Dystrophy

- Idiopathic Parkinson’s Disease

- Open Chest Surgery to Aorta

- Alzheimer’s Disease / Severe Dementia

- Fulminant Hepatitis

- Motor Neurone Disease

- Primary Pulmonary Hypertension

- HIV Due to Blood Transfusion and Occupationally Acquired HIV

- Benign Brain Tumour

- Severe Encephalitis

- Severe Bacterial Meningitis

- Angioplasty & Other Invasive Treatment for Coronary Artery

- Blindness (Irreversible Loss of Sight)

- Major Head Trauma

- Paralysis (Irreversible Loss of Use of Limbs)

- Terminal Illness

- Progressive Scleroderma

- Persistent Vegetative State (Apallic Syndrome)

- Systemic Lupus Erythematosus with Lupus Nephritis

- Other Serious Coronary Artery Disease

- Poliomyelitis

- Loss of Independent Existence

What are the notable changes to the critical illness definitions?

Here are some of the changes to the critical illness definitions that you should take note of:

- Deafness (Irreversible Loss of Hearing): Addition of the term 'irreversible' to the header. The term 'irreversible' defined to recognise the possibility of future medical treatments that can restore hearing to some level as medical advances are made

- Heart Attack of Specified Severity: The reference to Death of heart muscle due to obstruction of blood flow will be revised to Death of heart muscle due to ischaemia to make it clear that both Type 1 Myocardial Infarction and Type 2 Myocardial Infarction are covered

- Major Cancer: Major Cancers will be changed to Major Cancer and amendments have also been made to the exclusions

- Stroke with Permanent Neurological Deficit: Stroke will be amended to Stroke with Permanent Neurological Deficit for clarity rather than restricting claims as this definition was already included under the description in the previous definition

- Irreversible Aplastic Anaemia: Addition of the term 'irreversible' to the header. Irreversible was added to confirm permanency, which could be disadvantageous for customers as some forms of aplastic anaemia is treatable

- Coma: Medically induced coma has been excluded

- Benign Brain Tumour: Addition of exclusions - Abscess, Angioma, Tumours of the skull base

- Other Serious Coronary Artery Disease: The branches of the above coronary arteries have been excluded. This could be an issue as these branches being clogged could also lead to coronary problems.

- Poliomyelitis: Inclusion of 'The diagnosis must be confirmed by a consultant neurologist or specialist in the relevant medical field.' to provide clarity that diagnosis does not need to be diagnosed only by a neurologist, but from other specialists in relevant fields

Here's where you can find the full comparison between Version 2014 and Version 2019 of LIA Definitions of Critical Illnesses.

Singaporeans lack critical illness cover: study

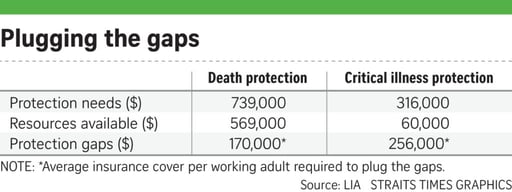

In a study published last year, the LIA said adult Singaporeans are worryingly short of critical illness cover.

A working adult in Singapore has critical illness cover of just $60,000, well under the LIA recommendation of about $316,000 which translates to about 3.9 times the average annual pay of $81,663.

This gap could be a cause of concern, as that means life insurance policies with critical illness coverage would meet just 20 per cent or so of their needs if such illnesses occur.

LIA advised that people need coverage to provide for family needs during the assumed recovery period of five years for a critical illness or until the insured person can return to work or adjust his lifestyle needs.

Should you get a critical illness plan now?

While the changes to the definition is set to be implemented come 26 August 2020, this does not mean that you should rush to get yourself critical illness insurance. Indeed, the current definition could be a point of consideration. However, the onset of critical illnesses and the type of critical illness you could suffer from is unpredictable. Similar to all other insurance plans, you should first assess your needs before deciding to purchase an insurance plan.

If you already have plans to get critical illness insurance, now's a good time as any to get yourself protected.

Read This Next:

Here’s Why You Should Seriously Consider Getting Cancer Insurance

Personal Accident Insurance: What Does It Cover and Should You Buy One?

Infectious Diseases Insurance: Best Plans To Protect Yourself

4 Must-Have Insurance In Your 20s

What Women Need to Know About Insurance

Similar articles

FWD Flex Insurance Review (2024): Low-cost Coverage for Top 3 Critical Illnesses for Singaporeans

Best HSBC Credit Cards: HSBC Revolution vs HSBC Advance vs HSBC Visa Platinum vs HSBC TravelOne Comparison Review

Critical Illness vs Cancer Insurance Plans: A Critical Comparison

Starr’s Critical Illness Advantage Global Connect Review (2022): Access to Worldwide Treatment

Why Critical Illness Insurance Is Crucial To Your Financial Planning

Critical Illness Plans vs Early Critical Illness Plans: Which Should You Get

3 Must-have Insurance Types For The YOLO & FOMO Generation

What Kind Of Critical Illness Insurance Do I Really Need?

Back to Blog

Back to Blog

%20Access%20to%20Worldwide%20Treatment.png?width=280&name=Starr%E2%80%99s%20Critical%20Illness%20Advantage%20Global%20Connect%20Review%20(2022)%20Access%20to%20Worldwide%20Treatment.png)