For those turning 55, here are the details on the widely-discussed CPF pre-retirement ‘hack’ that lets you earn more from the 4.08% interest from 1 Jan to 31 March 2024, risk free.

If you’re living in Singapore, the planning of your finances and your retirement cannot exclude your CPF.

From the day you start working, you’ll be contributing to your CPF Ordinary Account (OA), CPF Special Account (SA) and your MediSave Account (MA).

Due to the increase in the 12-month average yield from the Singapore Government Securities bond, the interest rates for the Special and MediSave Account (SMA) will also increase from 4.04% to 4.08% from 1 Jan to 31 March 2024.

This is the third consecutive interest rate increase.

With all that money set aside over the years, you’ll have to start making plans to capitalise on your CPF savings when retirement comes knocking.

But in this article, let’s zoom in on one plan-making in particular – a retirement ‘cheat code’, if you will – CPF SA Shielding. It is a term originally coined in this article back in 2019, highlighting how one can maximise your CPF accounts for retirement.

Here’s a guide for you pre-retirees, or for young adults helping their parents manage their finances. We’ll touch on what the CPF SA Shielding hack is, why people do it and how you can effectively execute it.

Table of contents

- How CPF Retirement Account is formed

- What is CPF SA Shielding

- How to carry out CPF SA Shielding

- Where to put CPF SA money

- Benefits of CPF SA Shielding

How your CPF Retirement Account is formed

To understand CPF SA Shielding, you first have to understand the CPF Retirement Account (RA).

As its name suggests, your CPF RA is meant for your retirement, where your retirement sum will provide you with monthly payouts during your golden years.

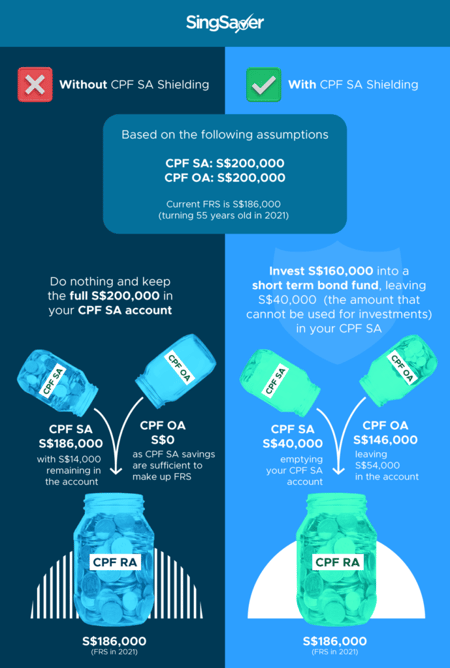

When you turn 55 years old, your CPF RA will automatically be created for you by pooling the savings in your CPF SA, followed by the money in your CPF OA, up to the Full Retirement Sum (FRS) which is currently S$205,800 in 2024. This order of funding your CPF RA cannot be changed.

What is CPF SA Shielding, and why people do it

Both your CPF RA and CPF SA earn a respectable 4.08% interest per annum, risk-free. However, the money in your CPF OA earns just 2.5% p.a.

Hence, someone financially savvy would try to maximise the interest earned in their CPF accounts, by having their CPF RA formed largely by CPF OA (which earns lower interest) rather than CPF SA. Do also keep in mind that you cannot make transfers from your CPF OA to your CPF SA after you turn 55.

The aim is to have more of your CPF money earning 4.08% p.a., rather than 2.5% p.a.

This is done by taking out the money in your CPF SA to invest, to keep the balance in your CPF SA to a minimum just before 55 years old. The less money you have in your CPF SA account, the more money is taken from your CPF OA to form your CPF RA.

However, you can’t completely empty your CPF SA if you're making investments. You will need to leave S$40,000 in your CPF SA, because the first S$40,000 from your CPF SA cannot be used for investments under the CPF Investment Scheme (CPFIS). Similarly, you are also not allowed to use the first S$20,000 in your CPF OA for investments.

As this S$40,000 rule only applies when you use your CPF SA savings for investments, this means that your CPF RA can be entirely formed by using your CPF SA savings, if it's sufficient to make up your FRS.

How much you’ll have left in your CPF OA would ultimately depend on how much money was used from your CPF SA and how much you have in the account to begin with.

SingSaver's Exclusive Offer: Open a CMC Invest account and get a S$20 Capitaland voucher. Plus, fund a minimum initial amount of S$500 and make 2 trades to receive 1 free Bank of America share (worth S$46) fulfilled by CMC Invest. Valid till 2 May 2024. T&Cs apply.

Additionally, receive 1 Nike share (NYSE:NKE) and/or 1 Tesla Inc. share (NASDAQ:TSLA) when you meet the required deposit and trade with your CMC Invest account. Valid till 2 May 2024. T&Cs apply.

How to execute CPF SA Shielding

Before you turn 55 years old:

- Step 1: Calculate how much you need to transfer out of your CPF SA, in order to keep just S$40,000 in the account

- Step 2: Transfer that amount of money out of your CPF SA by investing the money in a low risk investment product (more on this in the section below)

Note, you’ll need to be able to invest under the CPFIS before you can do this.

After you turn 55 years old:

- Step 3: Wait and check for your CPF RA to be formed

- Step 4: Cash out by selling your investments

- Step 5: Transfer the money back into your CPF SA

- Step 6 (optional): Consider topping up your CPF RA up to the Enhanced Retirement Sum (ERS) to enjoy higher monthly payouts during your retirement

![]()

SingSaver Exclusive Offer: Receive your choice of an Apple AirPods 3rd Gen with MagSafe charging case (worth S$274) or S$200 cash via PayNow when you open a Tiger Brokers account and fund at least USD 1,000. Valid till 2 May 2024. T&Cs apply.

Plus, enjoy prizes worth USD 3,600 when you deposit and trade with your Tiger Brokers account. Valid till 15 July 2024. T&Cs apply.

SingSaver Exclusive Offer: Receive your choice of an Apple AirPods 3rd Gen with MagSafe charging case (worth S$274) or S$200 cash via PayNow when you open a Tiger Brokers account and fund at least USD 1,000. Valid till 2 May 2024. T&Cs apply.

Plus, enjoy prizes worth USD 3,600 when you deposit and trade with your Tiger Brokers account. Valid till 15 July 2024. T&Cs apply.

Where should you put your CPF SA money in the interim?

Let’s zoom in on Step 2, where you have to transfer your CPF SA money out of the account by making investments.

Under the CPFIS, you can use your CPF SA to invest in these products:

- Unit Trusts (less high risk products)

- Investment-linked Insurance Products (ILPs) (less high risk products)

- Annuities

- Endowment policies

- Singapore Government Bonds

- Treasury Bills

As this money is meant for your retirement, and also because you’re only going to keep it in the investment vehicle for a short period of time, your investment of choice should incur low risk and low cost while offering high liquidity and stability.

With that in mind, annuities, endowment policies, ILPs and Singapore Government Bonds are taken out of the equation, because they are less liquid and require time in order for your investments to see returns.

That leaves you with unit trusts and Treasury bills (T-bills).

If you’re considering T-bills, go for the ones with a six month maturity date. You should also ensure that these bills mature after you turn 55, in order for your investments to reward you with a return before you transfer them back into your CPF SA.

If you’re considering unit trusts, here’s the full list provided by CPF. To help you narrow down your search, look out for unit trusts with low to medium risk. Unsurprisingly, you’ll find that the options provided are the bond (fixed income) funds, such as:

- Eastspring Investments Unit Trusts – Singapore Select Bond Fund Class A (Expense ratio: 0.61%)

- LionGlobal Short Duration Bond Fund Class A (SGD) (Dist) (Expense ratio: 0.56%)

- Nikko AM Shenton Short Term Bond Funds (Expense ratio: 0.40%)

- Schroder Singapore Fixed Income Fund Class A (Expense ratio: 0.69%)

- United SGD Fund - Class A (ACC) SGD (Expense ratio: 0.67%)

You’ll find that Nikko AM Shenton Short Term Bond Fund has the lowest expense ratio. It was also the bond fund referred to in this article.

FSMOne, a platform that offers investment products and services, also recommends the Nikko AM Shenton Short Term Bond Fund as a Parking Facility Fund for CPF investment, investing in a diversified portfolio of quality, short-term bonds and money market instruments. There’s also no sales charge incurred, although it is subject to the 0.05% quarterly platform fee.

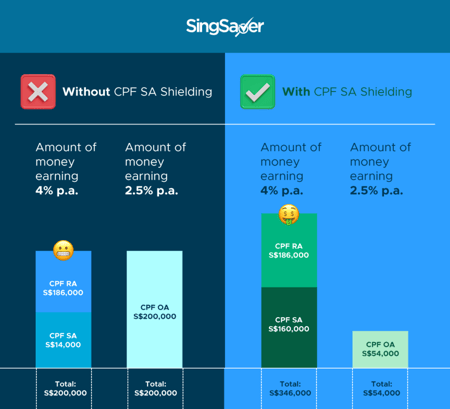

How much more do you stand to gain with CPF SA Shielding?

This all sounds great, but how much do you really stand to ‘gain’ with all this effort to shield your CPF SA?

Here’s an example of what your CPF accounts would look like, both with and without executing the CPF SA shielding.

From the following calculations, you’ll see that although you have S$400,000 in your CPF for both scenarios, an extra S$146,000 is earning 4% instead of 2.5% p.a. when you execute the CPF SA shielding.

In a single year, the difference in interest would be an extra S$2,190. With the money compounded over the years, this would grow to become a sizeable amount.

Strive for a better retirement

The aim of securing a comfortable retirement for ourselves lies at the heart of this ‘cheat code’.

Regardless whether you choose to shield your CPF SA or not, you can still top up your CPF RA up to the ERS of S$308,700, to enjoy higher monthly payouts during your retirement. And in case you didn’t already know, topping up your CPF SA or RA (or that of your grandparents, parents, spouse or siblings) can also contribute to reducing your income tax!

If you’re not yet near the retirement age, there’s still time for you to grow your pot of gold. Get started by putting your investments on autopilot with a robo-advisor, or create your own portfolio using a brokerage account.

Read these next:

How Much Do You Really Need For Your Dream Retirement Lifestyle?

A Complete Guide To CPF In Singapore

CPF Investment Scheme (CPFIS): Guide To Investing With Your CPF

Complete Guide To CPF LIFE: Facts, Myths And How To Make It Work Harder

Pros And Cons Of Keeping Your Savings In Your CPF Special Account

Similar articles

4 CEO-Proven Tips For a Healthier Bank Account

Pros And Cons Of Keeping Your Savings In Your CPF Special Account

A Complete Guide to Treasury Bills (T-Bills) in Singapore

Beginner’s Guide To CPF Retirement Sums And How To Get There (2023)

Should You Invest Your CPF Ordinary Account (OA) Money?

A Complete Guide To CPF In Singapore (2024)

The SSB vs CPF: Which One Has Better Returns?

The Most Popular Retirement Planning Methods in Singapore

Back to Blog

Back to Blog