Don’t count your chickens before they hatch. Selling off your biggest and most expensive asset is an effective way to get cash-rich — but there’s many costs to bear in any resale transaction.

Raking in a small fortune from your property transaction is usually the ideal scenario for those wishing to sell their HDB flat.

It’s tempting to put that huge influx of cash to good use, such as buying a bigger home, getting an endowment plan and/or investing in stocks.

However, the reality is that most of what you’re taking in from the sale will have to be used to finance the money owed from your recently sold property.

As a result, what you’re left with could be insufficient to help you buy your next home as well as help you achieve the finance goals you initially had in mind.

It‘s important to understand where our money goes once you receive the proceeds from the sale as you’ll have a clearer picture of how much you’ll be pocketing at the end of the day.

This will also help to calculate your budget for your next property purchase as well.

- Hidden costs of selling your HDB flat

- Factor in these additional costs

- How much cash can you take home?

- Conclusion

What are the hidden costs of selling your HDB flat?

First, it’s important to plan for these necessary payments:

Remaining home loan

Letting go of your current home means having to pay off your outstanding mortgage. Depending on how long you’ve been servicing your loan, this may require quite a sizable chunk of your sale proceeds.

HDB resale levy

You may be required to pay HDB resale levy when you sell your flat. The levy applies if your current flat happens to be subsidised (eg. BTOs), and you’re intending to buy an Executive Condominium (EC) directly from a developer or buying another subsidised flat.

Resale levy fees

| Flat type | Resale levy fees |

| 2-room flat | S$15,000 |

| 3-room flat | S$30,000 |

| 4-room flat | S$40,000 |

| 5-room flat | S$45,000 |

| Executive flat | S$50,000 |

| Executive Condominium | S$55,000 |

Property agent commission fees

Your property agent has done the job of marketing and closing the deal on your behalf. Naturally, they’ll have to be paid for their services. Typically, the market rate for an agent would set you back 1% to 2% of the transaction price.

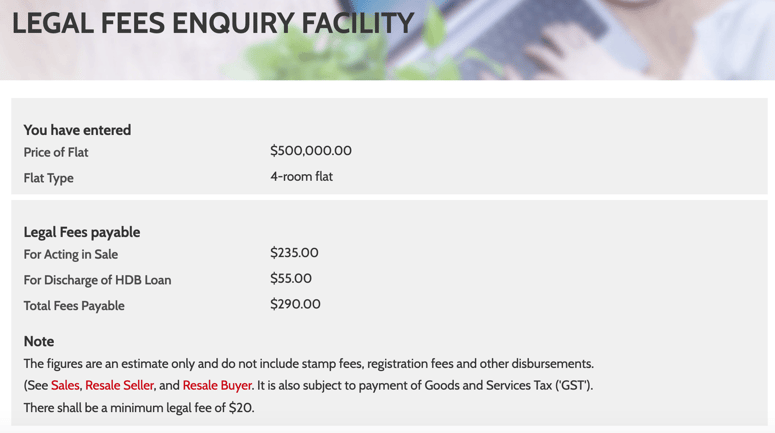

Legal fees

By appointing HDB to act for you in the legal process, this will ensure that your legal fees remain extremely affordable. For instance, if you’re looking to sell your 4-room HDB flat for S$500,000, HDB’s Legal Fees Enquiry Facility computed that your total legal fees payable will add up to S$290.

Next, don’t forget to factor in these additional ‘costs’

Amount taken from your CPF Ordinary Account (OA)

Anything taken out of your OA must go back to your OA. In fact, the total amount will be slightly higher than the initial amount borrowed as you would need to factor in the accrued interest. Accrued interest is the amount your OA would have accumulated if the money was left untouched to compound interest.

Amount to return to CPF OA = Principal amount + Accrued interest

CPF housing grants used (if any)

Proximity Housing Grant, Enhanced Housing Grant — these grants aren’t just free money, unfortunately. Remember the relief you felt when your flat got a lot more affordable when the grants came flowing in?

Well, the reality of enjoying the cushioning effect of grants is that you would have to refund it back to your CPF OA — not forgetting the accrued interest on that amount as well. If the grant amount is more than $30,000, a portion of the grant will be funnelled to your Retirement Account, Special Account and/or Medisave Account.

Amount to return to CPF = Total CPF grant used + Accrued interest

Case study: How much cash can you take home?

Let’s say that you’re putting your 5-room HDB flat on the market. The sale price is negotiated down to S$500,000. The total down payment was S$50,000 (10% of purchase price).

Here’s a breakdown of the estimated sale proceeds you’ll receive in cash:

| Selling price | $500,000 |

| Remaining home loan amount | (S$200,000) |

| HDB resale levy | (S$45,000) |

| Property agent commission fees | (S$10,000) |

| Legal fees (HDB) | (S$301) |

| CPF OA amount used | (S$25,000 + $100,000 = S$125,000) |

| CPF OA accrued interest (2.5%) | (S$21,875) |

| CPF grants used | (S$25,000) |

| CPF grants accrued interest (2.5%) | (S$4,375) |

| Balance amount | S$68,449 |

*These figures are rough estimates

In conclusion

With the exception of those with million-dollar flats, sellers may make the mistake of overestimating their cash proceeds without paying enough attention to what really goes into a resale transaction.

It’s important to exercise prudence here and not only know how much you could be left with but also how much you can afford in housing loan repayments once you’ve bought the next house.

To keep up with repayments and avoid overstretching your finances with a home that is beyond your means, always do the cost breakdown (like the one above) before hanging up that for sale sign on your door.

Shopping for the best home loan for your next property purchase shouldn’t be hard. Find the best rates all in one place right here on SingSaver.

Read these next:

How To Sell Your HDB DIY-style, And Save On Property Agent Commission

Stamp Duty: A Summary For Property Buyers & Sellers In Singapore

Guide To Property Investment In Singapore

Buying A HDB Resale Flat: How To Minimise Cash Over Valuation (COV)

Property Tax, Explained: Annual Value, Tax Rate And How To Make Payment

Similar articles

6 Misconceptions About Using Your CPF For Housing

How To Sell Your HDB DIY-style, And Save On Property Agent Commission

HDB Minimum Occupation Period Guide For Homeowners In Singapore

How To Save Money For A Flat Before Your 35th Birthday

CPF Accrued Interest On Housing: What Is It And How To Calculate

How Much Should You Save to Upgrade From an HDB to a Condo?

How To Save Money When Buying A Resale Flat

7 Lesser-Known Things You Should Be Aware Of Before Purchasing A BTO Flat

Back to Blog

Back to Blog