Opinions expressed reflect the view of the writer (this is his story).

Playing the miles game doesn't necessarily have to hurt your credit score. I have more than a dozen cards & keep an AA rating, because I pay off my bills on time.

The miles and points game is unlike any other, and there’s really no feeling like flying First or Business Class for free. However, one common objection I get to joining the hobby goes something like this:

“To play the miles game right, I’ll need to sign up for multiple cards. This will negatively affect my credit score, and I’ll lose out when I apply for a housing/car/education loan”

That’s certainly a legitimate concern. Your credit score can affect the size of a loan a bank is willing to make, or whether they agree to lend to you in the first place. But does playing the miles and points game necessarily mean taking a hit to your credit score? Does owning multiple cards cause banks to see you in a negative light? And what is your credit score based on, anyway?

What is a credit score?

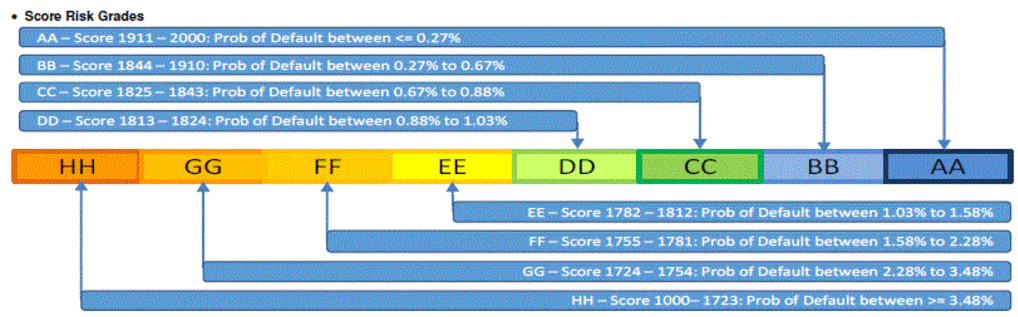

In the Singapore context, a credit score is a 4 digit number ranging from 1000 to 2000. Score ranges correspond to a two letter grade between AA to HH. The higher the score, the lower the risk of default. For example, someone with an AA score (1911-2000) has less than a 0.27% chance of default. Someone with an HH score (1000 to 1723) has a 3.48% or higher chance of default.

How is a credit score derived?

The Credit Bureau of Singapore (CBS) is responsible for the computation of credit scores. They have access to data from all retail banks and major financial institutions, and operate under the regulatory guidance and support of the MAS.

Unfortunately, the way your credit score is calculated is based on a proprietary algorithm which the CBS does not disclose. What we do know is that CBS looks at six components in deriving your credit score (the exact weightage of each component is confidential)

1. Credit Utilisation Pattern

This refers to the amount of credit you actually use. For example, your credit card may extend a line of $10,000 credit, but you only regularly use $1,000 of it.

2. Recent Credit Applications

This refers to the number of newly-opened credit facilities you have. All things equal, opening too many new credit facilities in a short period of time is a red flag for banks, as it suggests you may be taking on more than you can chew. This is definitely a concern for those planning on getting into the miles game by applying for a handful of cards, but the extent to which it actually affects your score is debatable (see below)

3. Account Delinquency

This refers to whether you’ve currently behind any payments on your credit facilities. Think: missed loan payment, late credit card payment.

4. Credit Account History

This refers to your history of making full and complete payments on your credit facilities.

5. Available Credit

This refers to the total amount of credit extended to you.

6. Enquiry Activity

This refers to the number of new application enquiries found in your account. Every time you apply for a new loan or credit card, the bank or financial institution will pull your credit score as part of its diligence. Too many enquiries in a short period of time suggests you are taking on too much credit. Requesting a credit report from the CBS does not negatively impact your score – it’s only when banks and financial institutions do it as part of a new credit request.

The CBS provides a short guide to reading a credit score here. It’s good to remember that your credit score, important as it is, is just one of many factors used in a loan application process. Banks also look at your annual salary, length of employment, ownership of other assets like a house and the presence of any pending litigation when coming to a decision.

How can I get a credit report?

A credit report normally costs $6.42. The good news, however, is that there are two ways of getting one for free:

- If you’ve applied for a new loan, overdraft or credit facility, you should receive a free credit report from CBS within 30 days of approval/rejection. Go to the CBS website to get a free download.

- HSBC is sponsoring free credit reports until 31 March 2019 in exchange for providing the bank with your personal details (such as name, NRIC, monthly income, contact details), and your consent to be contacted by HSBC for marketing purposes for a period of three months. HSBC does not see your credit report

And now, the crux of the matter...

Does playing the miles game hurt your credit score?

My stance is this: playing the miles game irresponsibly can, of course, wreck your credit history. However, when done with discipline, it can actually improve your overall credit score.

Here’s why: applying for a lot of cards in a short period of time may reduce your credit score in the short run, but as you build up a track record of paying your bills in full and on time, your score will start to improve beyond someone who doesn’t use cards at all. That’s because you’re demonstrating that you’re capable of using credit responsibly.

I know some people who have philosophical objections to using credit, perhaps because a family member of friend has run into problems in the past. That’s unfortunate, but it’s not the right solution either. If you never use credit at all, your credit score will be CX – meaning that CBS has insufficient information to assign you a score. That’s not a good thing, because the banks have no way of assessing your creditworthiness, and that will create problems when you ultimately do need to take a loan.

The proper way to build your credit score is therefore not to avoid credit cards, but to use them responsibly. Set up GIRO arrangements so you don’t miss payments. Treat credit cards as debit cards with rewards, not a way of spending more than you have (if you’re short on funds, there are cheaper options to borrow money than on a credit card).

Never let the promise of miles or points entice you to spend more than you otherwise would – remember, the miles game is about not leaving money on the table, not about putting extra money down.

Conclusion

Playing the miles game does not necessarily have to hurt your credit score. I have more than a dozen cards and keep an AA rating, simply because I pay off my bills on time and never go over my limit. If you’re looking to apply for a housing loan in the near future, it may not make sense to go on a card application spree right this minute, but otherwise, you have nothing to be worried about.

Compare and apply for the best air miles credit cards on SingSaver

Now that you know how to responsibly manage your credit cards so that they don't have a negative effect on your credit score, it's time to start playing the miles game right – by getting the best air miles card that suits your lifestyle and your needs.

Compare and apply for the best air miles credit cards on SingSaver, and get exclusive sign-up bonuses (on top of the bank's own welcome gifts)!

Related stories:

5 Ways to Get the Highest Credit Score in Singapore

7 Mistakes That Ruin Your Credit Score in Singapore

Air Miles Cards: 8 Questions to Help You Choose the Right Card

The Best Miles Cards… May Be Rewards Cards

6 Credit Cards That Give You Free Access to Airport Lounges

By Aaron Wong

Aaron started The MileLion to help people travel better for less and impress “chiobu”. He was 50% successful. This is his story.

Similar articles

How to Get a Credit Card in Singapore When You Have No Credit Score

Will A Debt Consolidation Loan Affect My Credit Score?

Money Confessions: I Have 16 Credit Cards But I’m Not In Debt

7 Mistakes That Ruin Your Credit Score in Singapore

5 Ways to Get the Highest Credit Score in Singapore

Can Cancelling A Credit Card Have Detrimental Effects?

What is a Credit Rating, and Why Should Singaporeans Care?

How Debt Consolidation Can Improve Your Credit Score Over Time

Back to Blog

Back to Blog