In a digitalised world of efficiency and efficacy, consumer habits have likewise become more demanding. But when is it acceptable to spend for convenience as opposed to saving extra for a rainy day?

We can all agree that we’ve heard the words “unprecedented times” enough already, but are we truly aware of how much the pandemic has transformed/affected market and consumer behaviour?

Having been locked up at home multiple times because of the pandemic, the focus of consumer habits has shifted to timely accessibility. In turn, this has led to excessive stress being placed on the e-commerce industry, floundering to meet demand in crisis despite supply chain disruptions worldwide.

Many businesses were forced to pivot and prioritise sales online to stay afloat. They found themselves switching business models, finetuning products and services and re-aligning their marketing objectives.

But just how much has the retail landscape in Southeast Asia — and Singapore — changed over the last few years?

- Online retail vs. physical retail

- The effectiveness of online shopping

- The secret to e-commerce longevity: comfort & convenience

- Why comfort & convenience are so significant

- The delicate boundary between price & convenience

- Balancing saving & spending

Majority of consumers prefer online shopping over physical retail

According to Lazada’s first regional survey, 73% (4,380 respondents) agreed that online shopping was essential to their day-to-day living compared to only 60% previously pre-pandemic.

Over 85% of Lazada’s Singaporean respondents expressed more interest in online shopping than in person — so much so that 96% of locals felt that physical retail was obsolete since all transactions could be made digitally.

This was bolstered by another survey done by Qualtrics that showed 73% of 300 respondents were perfectly comfortable shopping online for the next six months, with 47% of them visiting actual retailers less frequently.

Still can’t see the bigger picture? To put things to scale, one-third of Singaporeans in a Visa study made their first online purchase when COVID-19 pandemic ensued in 2020. In fact, their results shed light on how nearly three in four (74%) of Singaporeans were just shopping online more often overall.

Why has online shopping been so effective?

Back to Lazada’s survey, 67% of their participants attributed their virtually never-ending e-commerce mega campaigns every few weeks or month as the main incentive to spend — and who could blame them? With discount codes on top of flash deals, it’s hard to resist the draw of such attractive sales.

Even James Chang, the chief business officer of Lazada Group commented that “changes [in online shopping] are showing a lasting effect, especially on emerging markets”.

This means that if incumbent firms and major stakeholders with significant market share are already struggling with competition, what more for smaller and new businesses seeking to enter the field? It seems like a near-impossible feat.

Nevertheless, this didn’t stop a whole horde of home-based and local businesses to pop up throughout the height of the pandemic. In fact, a good portion of Singaporeans exhibited a positive shift in attitude and sentiments towards supporting locals than previously.

So what is the common denominator between smaller businesses and e-commerce giants?

Well, it all boils down to comfort and convenience consisting of multiple factors like ease of product/service search, competitively-matched prices, and efficient shipping all with a single click at home.

How have brands leveraged on comfort and convenience?

In a business sense, the essence of convenience hinges on “delivering the right information, at the right time, to the right person, on the right platform”.

Any and all crucial information needs to be displayed to customers from the get-go to lure them in and snag the consumer bait.

Brands have been achieving this by reducing consumer friction at points along the e-commerce journey.

Where “friction exists, frustration exists” — and “frustrated buyers will seek out the path of least resistance”.

Caitlin Burgess, for TopRank Marketing

As a result, this manifests in business behaviours like funnelling tons of targeted ads, skewing content algorithms to one’s preference and delivering desired goods and services with minimal delay.

Streamlining the commercial process from start to finish is all part and parcel of customer acquisition; and boy, is it working on us.

Why are comfort and convenience so significant?

Why? Because let’s face it, humans have an inclination to accomplish tasks at home and work in the easiest and fastest way possible.

Bill Gates himself praised lazy people (or procrastinators) as “making for the best employees” because “lazy people would find an easy way to do hard jobs”.

Now isn’t that an inspirational quote?

Jokes aside, comfort and convenience have everything to do with why fast food restaurants even exist. Or perhaps, why next-day delivery is even a thing. It’s literally the reason why transportation was invented and has advanced so rapidly over the centuries into its modern renditions today.

In a nutshell, these two concepts are so fundamental to societal’s progress because it banks on the idea of saving time. And as we all know, time is a precious and finite resource to humanity that no amount of money can buy back.

The fine line between price and convenience

It’s by no means an easy conundrum with a straightforward answer. Everyone has different thresholds and perceptions of what’s deemed as ‘worth it’ or ‘overpriced’.

As Antonio Perini, CEO of Milkman, wisely summarises, “Each customer has their optimal point between convenience and price.” In other words, everyone has their sweet spot for what costs are acceptable in saving time or considered overboard and not value for money.

Establishing this boundary of price versus convenience is a personal journey and requires some introspection to discern carefully.

For some, queueing up for half an hour for a plate of popular chicken rice is worthwhile whereas others might find it unnecessary and rather buy chicken rice from a random, generic stall.

Both opinions are valid. One person just values the quality and taste of the chicken rice more than the price point and time spent queueing for it.

Conversely, the other person just doesn’t really care about ‘superior’ food quality and would prefer to save on time to buy a standard plate of chicken rice and call it a day.

When should we save instead of splurge?

Life is short, but money shouldn’t be spent meaninglessly and lavishly 24/7. Despite all the grey areas overlapping saving time and justifying prices, there are certain circumstances where saving is more sensible than splurging.

1. Storing money in saving accounts

As long as you have a dollar to your name, you’ll probably have opened a savings account in any of the banks here. Although current interest rates are suboptimal, this doesn’t mean they’re entirely futile.

Interest rates are interest rates, and you’ll earn returns no matter how little it is — which is better than nothing.

However, in lieu of this, we can suggest alternatives to traditional savings accounts to accrue you higher interest, better rates of return and a more effective yet sustainable method of accumulating wealth.

They include fixed deposits, endowment plans and/or cash management accounts. Each of them bears its own perks and benefits, best catering to specific needs depending on your financial situation and goals.

Confused about the alternative savings tools available? We’ve provided a detailed explanation breaking down fixed deposits vs. endowment plans vs. cash management accounts to help you decipher which best suits your needs.

2. Investing and re-investing your savings

Once you’ve accumulated substantial savings, the next recommended step to do is to invest and reinvest your savings. There are a variety of investment strategies available, so don’t be afraid to explore your options. After all, experience is the best teacher.

For instance, some tools double up as a savings-investment hybrid account like a participating endowment plan. Examples include AXA EarlySaver Plus or Great Eastern Flexi Cashback, both with a potential policy tenure of up to 25 years.

Alternatively, cash management accounts are great solutions for storing idle cash into investment portfolios afforded by robo advisors. Because of these pre-set portfolios, accounts under robo advisors like Syfe Cash+ and Stashaway Simple make it easier for newbies to enter the stock market.

Of course, for the truly adventurous lot, you could definitely take a gander at investing in individual stocks themselves if you’re seeking to reap some sweet, direct dividend payouts or capital gain.

Otherwise, also consider investing in a basket of securities like ETFs or index funds for greater dividend stability and assurance than solely investing in a single, wildly-volatile stock or bond.

Apart from the stock market, check out these four other ways to be savvy with your investment practices.

We’ve also collated a bunch of ongoing investment sign-up promotions under various licensed brokerages and roboadvisors (e.g. Tiger Broker, Moomoo, Stashaway, etc.) that you don’t want to miss!

3. Setting up an emergency fund

Growing up, we’ve always learnt to save and be prepared for times of misfortune. Economic instability, accidents and terminal illnesses, familial loss, property loss, natural hazards, and most recently, war crimes against humanity are all rife within our current lifetime.

As much as life is unpredictable and negative nowadays (as dictated by Murphy’s Law), that doesn’t mean that we should abandon our backup plans.

Setting up and building a robust emergency fund could be precisely your safety net in times of uncertainty. Generally, emergency funds are recommended to comprise three to six months of untouched income stored in a place with high liquidity.

Unfortunately, ETFs and long-term fixed deposits will not be appropriate for your emergency fund. Their rigidity in fund withdrawal on short notice makes them unviable.

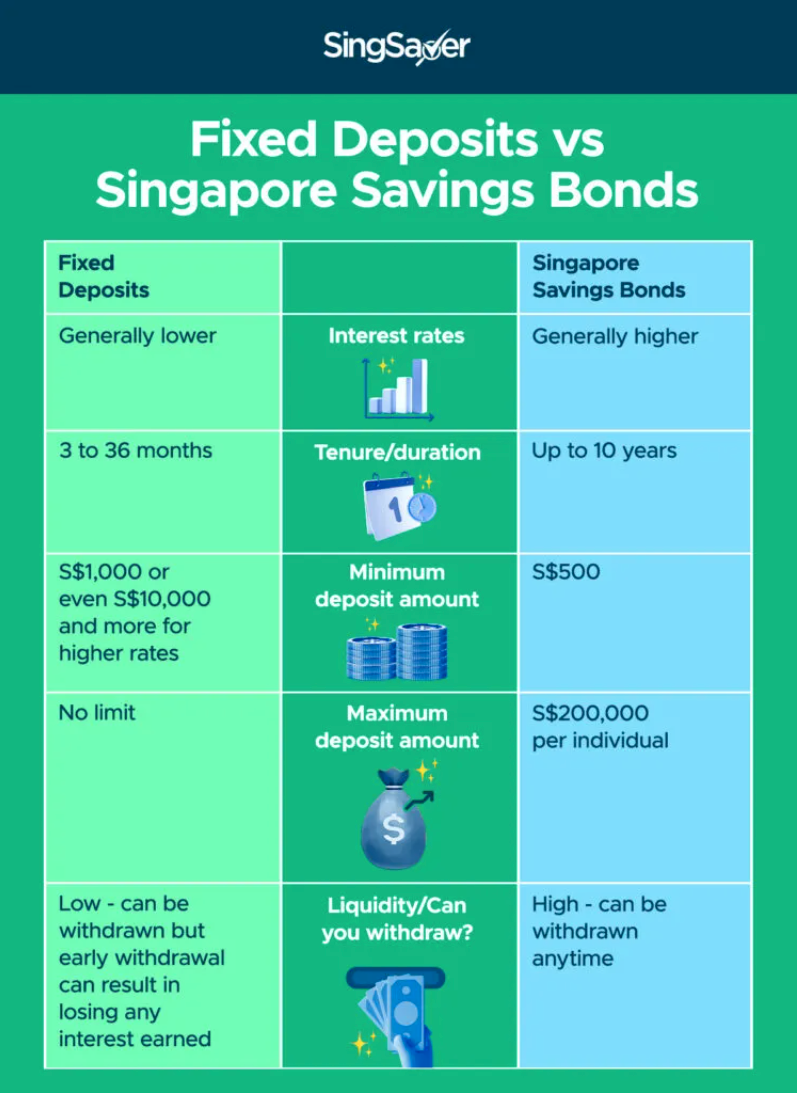

Comparison between short-term fixed deposits and SSBs

Hence, we actually advise going back to the basics and using a decent-yield savings account, short-term fixed deposit, cash management account or Singapore Savings Bonds (SSBs) instead.

Don’t forget to automate your savings process through a GIRO system to redirect at least 20% of your income into your chosen emergency fund account. Relying on willpower and discipline alone will be a struggle.

Bottom line is: Spend within your means and save wherever you can. A little goes a long way.

Read these next:

5 Ways To Invest Money That Are Better Than Buying Toto

Emergency Fund: How To Build It The Less Painful Way And Where To Keep It

12 Best Fixed Deposit From Top Banks In Singapore To Lock In Your Savings (April 2022)

Best Cash Management Accounts in Singapore to Soup Up Your Savings (2022)

Best Short & Long Term Endowment Plans in Singapore (2022)

The Complete Guide To Singapore Savings Bond (SSB) — Return Rates And How It Works

Similar articles

5 Tips To Better Plan Your Budget in a Post-COVID World

Grab Expands Financial Offerings With New Micro-Investments And Consumer Loans

International Women’s Day: 9 Female-Owned Businesses in Singapore You Should Be Supporting

Fixed Deposits vs. Endowment Plans vs. Cash Management Accounts: Which Should You Choose?

11 Things You Shouldn’t Do Before or During a Recession

4 Reasons Saving Won’t Make You Rich

SingSaver Exclusive: Have You Gotten Your Free Copy Of The Ultimate Savings Guide?

Alternative Careers During the Pandemic – How Much Can You Earn?

Back to Blog

Back to Blog

.png?width=280&name=Investments%20(6).png)