For tax period YA 2024, you will be paying taxes for income earned in 2023. We've put together a checklist of everything you need to know when filing your income tax.

Taxes are considered contributions towards nation-building in Singapore.

Across the world, income tax rates vary. In Singapore, with a progressive tax system in place, here’s all you’d need to know when filing this Year of Assessment (YA) 2024 for the year that ended on 31 December 2023.

As announced during Budget 2024, the government has agreed to provide a Personal Income Tax Rebate of 50% for the Year of Assessment 2024, capped at S$200, in light of the rising costs of living.

Table of contents

- 5 Ways to reduce income tax

- Who needs to pay income tax

- What is taxable and what is not?

- How much tax will you need to pay?

- What is the deadline for you to file your income tax?

- How to file your income tax?

- What happens if you file your taxes late or if you do not file your tax?

- Income tax payment methods

- What happens if you pay your tax late?

Ways to reduce income tax

Here are 5 ways you can reduce your income tax in Singapore. Do keep in mind that efforts to reduce tax done in 2023 will be for the year that ends 31 December 2023, for the Year of Assessment (YA) 2024. (Yes, it's too late to reduce your taxable income for last year.)

[NEW] In light of the rising cost of living, the government has agreed to provide a Personal Income Tax Rebate of 50% for the Year of Assessment 2024, capped at S$200, as announced during Budget 2024.

#1 Contribute to your Supplementary Retirement Scheme (SRS) account: Singaporeans and PRs can contribute up to S$15,300 while foreigners can contribute up to S$35,700. SRS contributions are eligible for tax relief and can be invested to help you prepare for retirement.

#2 Top up your CPF Special Account (SA) voluntarily: CPF SA top ups enjoy dollar-for-dollar tax relief. Previously, this tax relief was capped at S$7,000 for yourself and another S$7,000 when you top up the SA of your loved one, potentially lowering your taxable income by S$14,000.

However, with changes to the tax relief top-up, you can now enjoy a tax relief of up to S$8,000 for yourself, and an additional S$8,000 if you top up for your family. This means that you can enjoy tax relief of up to S$16,000 in total. What's more, the money in your CPF SA earns an interest rate of 4.08% p.a. (1 January 2024 to 31 March 2024).

#3 Voluntarily contribute to your Medisave account: Similarly, contributions to your Medisave account are also eligible for tax relief. Your Medisave money can be used to help offset medical bills and also earn 4.08% p.a. (1 January 2024 to 31 March 2024). You can refer to IRAS' website for more details.

#4 Life Insurance relief: If you pay insurance premiums on your own life policy and your total CPF contribution under employee's CPF contribution and compulsory MediSave/voluntary CPF contribution for self employed is less than S$5,000 in the year preceding the year of assessment, you can earn tax reliefs. More details here.

#5 Sign up for an eligible course: Not only do you enjoy course fees relief of up to S$5,500 each year, you can also upgrade your skills and increase your employability at the same time. Talk about win-win!

You can also enjoy various tax reliefs which you can find later in this article.

Keep in mind that there is a personal income tax relief cap of S$80,000 for each Year of Assessment. This applies to the total amount of all tax reliefs claimed, limiting the amount of tax relief you can enjoy.

However, approved donations are exempt from this cap, so it's something you can consider should your reliefs start to approach the limit.

Who needs to pay income tax in Singapore?

You will need to pay income tax if you earn, derive or receive income in Singapore, unless specifically exempted under the Income Tax Act or by an Administrative Concession. Also, you must file an Income Tax Return if you receive a letter, form or an SMS from the Inland Authority of Singapore (IRAS) informing you to do so.

More specifically, these are the following groups of people that will need to pay tax in Singapore:

1. Individuals working in Singapore: Those who receive payments (whether in the form of cash or benefits-in-kind) for any service rendered in or any form of employment from Singapore.

2. Individuals doing business in Singapore: Self-employed individuals such as sole-proprietors, partners, freelancers, taxi drivers, hawkers, commission agents, among others, who derive their income in Singapore.

3. Individuals with investments in Singapore: Those who derive income from their investments in property, shares, unit trusts, fixed deposits, etc. in Singapore (unless their investment is specifically exempted under the Income Tax Act).

4. Individuals working outside Singapore:

- Individuals working outside Singapore whose overseas employment is incidental to their Singapore employment; or

- Individuals working outside Singapore on behalf of the Singapore Government; or

- Individuals who receive income through a partnership in Singapore

5. Individuals who are not working but receiving income: This includes income from investments, NSman income (including all awards and allowances including IPPT monetary incentives), part-time income, royalty income, pension, or Supplementary Retirement Scheme (SRS) withdrawals.

You will not need to pay income tax if you are earning gross income of S$22,000 or less in a year, or if you do not derive or receive any income in Singapore. If you receive a letter or SMS informing you that you have been selected for No Filing Service, you are not required to file a tax return.

You can also check your filing requirement if you have not been contacted by IRAS.

What is taxable and what is not?

You are taxed based on the income earned in the preceding calendar year. This means that for income earned in 2023, you will be taxed in the Year of Assessment (YA) which is 2024.

Taxable income refers to:

- Gain or profits from any trade or business

- Income from investment such as dividends, interest or rental

- Royalties, premiums and any other profits from property

- Other gains that is revenue in nature

Income that is non-taxable include:

- Capital gains, such as gains on sale of fixed assets; and gains on foreign exchange on capital transactions

- Income specifically exempted from tax under the Income Tax Act

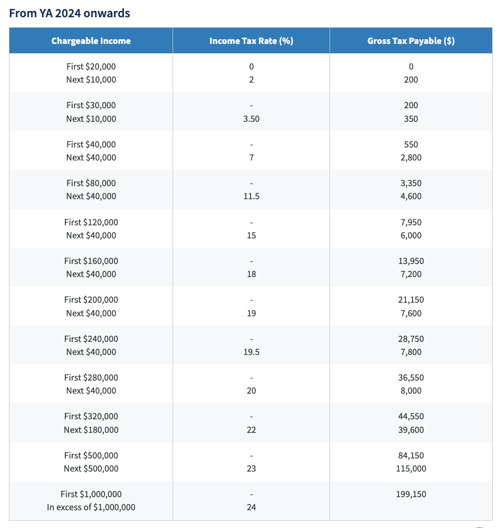

How much tax will you need to pay?

Singapore has a progressive income tax system in place for resident taxpayers. This means that higher income earners pay proportionately more tax. The current highest personal income tax rate for the higher earners is 24%.

Here’s the resident tax rates that you can refer to in order to find out how much you will need to pay in taxes.

What is the deadline for you to file your income tax?

Filing for the Year of Assessment (YA) 2023 began on 1 March 2023. You will need to file your taxes before:

- 15 April 2024 (for paper filing) or

- 18 April 2024 (for e-filing online)

After filing, you should see an Acknowledgement Page on the screen. You should also receive a copy of your tax bill (Notice of Assessment) for YA 2024 from end-April 2024 onwards.

This will show you how much tax you need to pay. You might also receive an SMS alert once your tax bill is finalised and ready for online viewing, if you have updated your mobile number with IRAS.

You have one month from the date of the Notice of Assessment (NOA) to pay your taxes.

How to file your income tax

To file your tax return, log into myTax Portal using Singpass. You can do so either on your desktop or on your mobile phone. You will need Singpass 2FA to login to myTax Portal.

There are 5 parts to filing your income tax.

1. Income

Declare your income. This includes employment income, trade, business, profession or vocation income, rental income and any other income. If your employer is participating in the Auto-Inclusion Scheme (AIS) for Employment Income, you do not need to declare your employment income information, and this information will be pre-filled in the form.

However, if your employer is not participating in the AIS, you would have received a IR8A form from your employer and you will have to input details such as your income and bonuses. You should also have records of your income on hand to help you accurately declare it in your tax return.

2. Expenses

This section refers to expenses incurred while earning your income. This could include employment expenses, business expenses and other expenses.

3. Reliefs/rebates available to all taxpayers

These tax reliefs help promote specific social and economic objectives. For example, making a donation at a registered charity is eligible for tax relief. The reliefs under this section for individuals include:

- Course fees relief

- CPF cash top up relief, CPF relief

- Earned income relief

- Handicapped brother/sister relief

- Life insurance relief

- NSman (self) relief

- Parent/handicapped parent relief

- Supplementary Retirement Scheme (SRS) relief

These tax reliefs on your income tax, assessed in YA 2024, has to be undertaken during the year in which you earned your income (2023 in this case). This is something you can keep in mind before 2025 arrives.

4. Additional reliefs/rebates available to married/divorced/widowed taxpayers

These include:

- NSman (parent) Relief

- Parenthood Tax Rebate

- Qualifying/Handicapped Child Relief

- Spouse/Handicapped Spouse Relief

5. Additional reliefs/rebates available to married/divorced/widowed female taxpayers

These include:

- Foreign Maid Levy Relief

- Grandparent Caregiver Relief

- NSman (wife) Relief

- Working Mother’s Child Relief

There is a personal income tax relief cap of S$80,000 for each Year of Assessment. You can find the full list and information on deductions for individuals (reliefs, expenses, donations) here.

What happens if you file your taxes late or if you do not file your tax at all?

Firstly, IRAS could do the following if you fail to file your taxes by the deadline.

- Impose a late filing fee not exceeding S$1,000;

- Issue an estimated Notice of Assessment (NOA); and/or

- Summon you to Court

If IRAS issues an estimated NOA based on the your past years’ income or information available to IRAS, you must:

- Pay the estimated tax within one month from the date of the NOA.

- File your Tax Return. You should file your tax return immediately. Upon revision of the estimated assessment, any excess tax paid will be refunded.

Income tax payment methods

When you receive a copy of your tax bill (Notice of Assessment) for YA 2023 sometime after the end of April 2024, you will have to pay the amount indicated in the tax bill.

There are a few ways you can pay your income tax:

- GIRO

- Electronic payment modes (such as iBanking, ATM, AXS, SAM, NETS etc.)

- Credit card

- Telegraphic transfer

Here are all the details on the tax payment modes available for individuals. You get one month from the date of the Notice of Assessment (NOA) to pay your taxes (even if you have filed an objection and are awaiting the outcome).

If you are planning to use a credit card to pay for your taxes, do note that for most credit cards exclude tax payments from earning credit card rewards.

However, there are still ways to work around that limitation, by paying an administrative fee (as a percentage of your tax deduction amount) or applying for a payment facility to use your credit card for tax payments. This fee ranges from 0.5% to 3% of the payment amount.

Here are the options available:

- Bank of China: If you plan to use your BOC credit card, you will have to mail this form to the bank.

- CardUp: CardUp enables users to pay for big expenses using credit card, in places where credit cards are usually not accepted. Not exclusive to any particular bank, you can continue to earn your credit card rewards by paying your taxes with CardUp, while incurring a small CardUp fee.

- Citi PayAll: Use your Citibank credit card to earn miles or reward points for a small fee.

- DBS: DBS has an Income Tax Payment Plan that allows you to pay your taxes with a DBS credit card for a one-time processing fee of 3%.

- HSBC: The administrative fee charged differs based on the HSBC credit card you use.

- Standard Chartered Tax Payment Facility: An income tax payment facility specifically for existing Visa Infinite Credit Cardholders.

- Standard Chartered EasyBill: For a small processing fee, get awarded cashback and/or 360° Rewards Points on eligible taxes paid to IRAS with your Standard Chartered credit card.

- UOB PRVI Miles Payment Facility: For individuals who hold a UOB PRVI Miles credit card.

What happens if you pay your income tax late?

Similar to a credit card bill or monthly repayment for loans, you will incur late charges. If you miss the payment due date, you will incur a late payment penalty of 5% and an additional 1% for every month (up to a maximum of 12% of the tax outstanding). A letter will be sent to you regarding this 5% late payment penalty.

Thereafter, you will have to make the payment before the due date stated on the letter to avoid further penalties.

If the income tax continues to remain unpaid, further enforcement actions could be performed for IRAS to recover the taxes, such as:

- Appointing agents like your bank, employer, tenant, or lawyer to pay the money to IRAS

- Issuing a Travel Restriction Order (TRO) to stop you from leaving Singapore; and/or taking legal action

With tax season soon approaching, it’s a good time to visit the myTax Portal to get started and get yourself familiarised. You could also use this handy guide by IRAS for step-by-step instructions on e-Filing via MyTaxPortal.

Similar articles

Financial Topics That Are Safe for This Year’s Christmas/New Year Table

Optimise Your Income Tax, Score Better Investment Returns. Here’s How

Paying Income Tax: Are CardUp, ipaymy, and Citi PayAll Worth the Admin Fee?

Property Tax, Explained: Annual Value, Tax Rate And How To Make Payment

What To Know About Income Tax Relief Season

How To Earn Rewards and Miles for Paying Your Income Tax

Goods and Services Tax (GST) Singapore – What Is It, Current Rates, Output Tax

In the Millionaires’ Club? Here's how to Optimise Your Tax Efficiency

Back to Blog

Back to Blog