Avoid making these retirement planning mistakes in Singapore if you want to live your golden years in comfort.

Should Singaporeans be anxious about their retirement plans? Recent surveys seem to indicate so. We live in an ageing society with a higher life expectancy and a slowing economy with a higher cost of living.

For the first 30 years in our lives, we worry about meeting life’s important milestones, and when we turn 60 we start worrying about how much longer we may live. That’s the irony of life.

Planning for retirement is as important as other life goals such as purchasing a house, starting a family, or raising a child. HSBC’s Future of Retirement report reveals that 68% of pre-retirees aged 45+ would like to retire in the next 5 years, but 48% of them are unable to for financial reasons.

A similar report from The Straits Times reveals that 46% of survey respondents think they will have to work beyond retirement to fund their golden years.

I came across this new video from the Central Provident Fund (CPF) that reminds us why early preparations are essential to a happy retirement.

1. You Plan and Save For Retirement Too Late

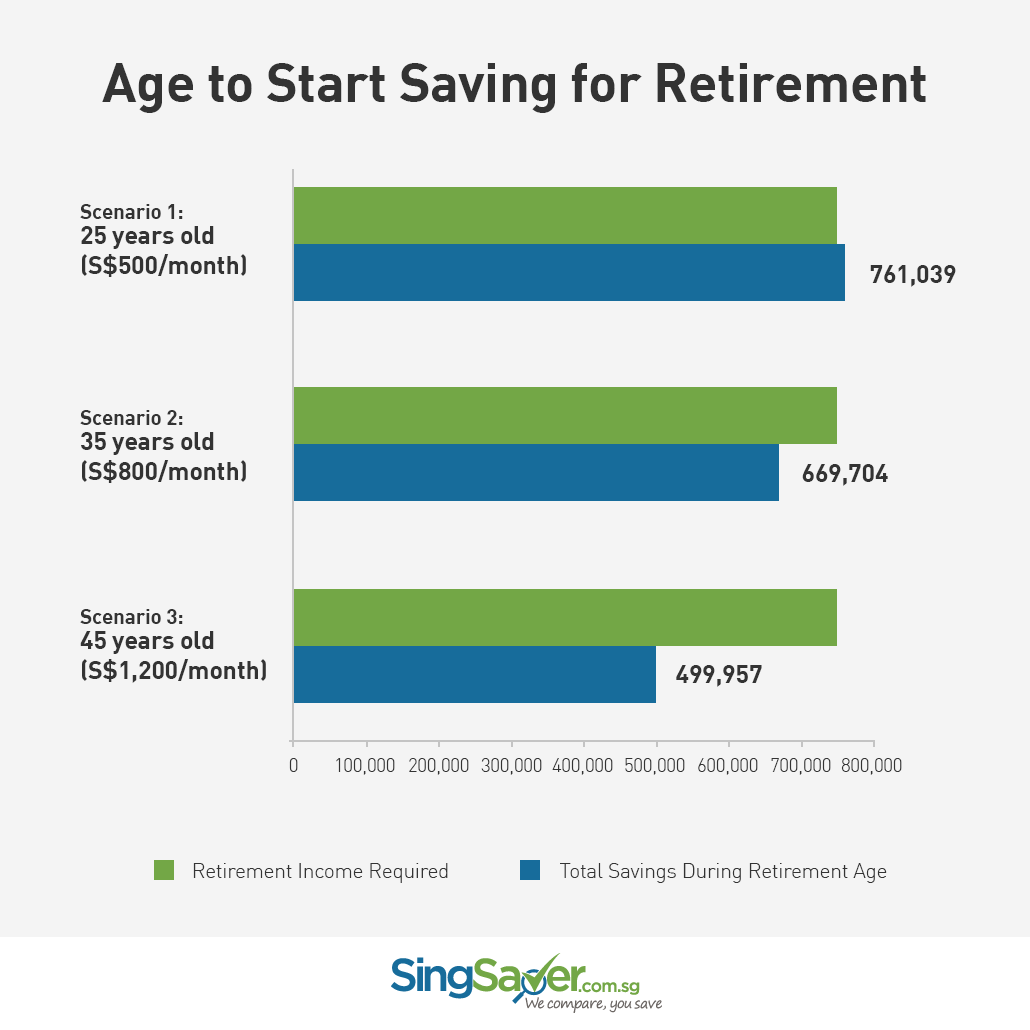

In your 20s, retirement seems like a distant thought. But the earlier you start saving for it, the more you’ll have stashed away for your golden years.

Let’s assume you need an annual income of $30,000 when you retire at the age of 65, and you expect to live until 90 (the average life expectancy in Singapore is 82 years).

The charts below illustrate three different scenarios:

Scenario 1: You start saving $500 every month from age 25, with returns of 5% compounded annually until age 65.

Scenario 2: You start saving more at about $800 every month from age 35 with same returns of 5% compounded annually until age 65.

Scenario 3: You start saving even more at $1,200 every month from age 45 with returns of 5% compounded annually until age 65.

Which scenario ends up saving the most for retirement?

As you can see, you would have the largest nest egg if you started saving at age 25, despite setting aside the smallest amount each month.

This happened because of compounding interest - the following year’s interest is added to the principal and the previous year’s interest. The sooner you start saving for retirement, the more time there is for your savings to compound.

If you delay saving for retirement until your 30s or 40s, it becomes more difficult to accumulate the amount you need. Not only do your investments have less time to compound; saving itself becomes tougher as your mortgage or your children’s needs take priority.

See Also: What Are You Doing to Plan For Your Retirement?

2. You Underestimate Your Retirement Age

Anticipate to live until 90 so that you can build a bigger nest egg. Meanwhile, beef up your savings in case you end up retiring early.

In Singapore, employers offer you re-employment at the age of 62 through to 65. You may also be able to find employment after that, but you must also prepare in case circumstances force you to retire earlier than expected.

If you have a physical occupation, such as construction or cleaning, you cannot assume you will be able to do the same job at 65 or 70. Even office jobs can take a toll, as stress and long hours will compound any health issues.

In other words, you must save enough to handle the prospect of unemployment - whether or not you intend to keep working.

3. You Don’t Have a Debt Repayment Plan

If you are in the position to pay off your existing debt (including mortgages) while funding your retirement, do it. Even if you’re struggling financially, you must have a debt repayment plan for all your good and bad debts.

Not only does being out of debt give you more control over your finances; it eliminates the cost of interest and gives you more cash to funnel into your retirement savings and long-term investments.

Having a debt repayment plan also keeps you from turning bad debt into a lifestyle. Typically, adults who rack up a credit card debt in middle age also had debt as young adults. When bad debt becomes a habit, it becomes difficult to get out of it without drastic action.

So if you’re under 35, deal with your bad debts now. Having a robust retirement fund will not help you if it’s offset by an equally large amount of debt. Speak to Credit Counselling Singapore or a financial advisor to see what your options are.

4. You Don’t Take Care of Your Health

The same survey by HSBC shows post retirees maintain a healthier lifestyle than pre-retirees. But you shouldn’t wait until retirement age to start taking care of your health.

Healthcare costs will rise significantly as we grow older. If you don’t take care of your health now, you can develop conditions like diabetes, which can be expensive to manage.

The cost of treating these conditions does not go away. It can be for life, and it can be devastating if you don’t have savings.

The monthly cost of kidney dialysis, for example, can be around $2,500 a month* for life. Even without these chronic conditions, we have to consider that illnesses and injuries can become more common as we get weaker.

You will notice that the MA in your CPF has a much higher interest rate of four to five per cent. This is intended to cope with rising medical costs that you will face. However, you can take further steps.

Remember that retirement planning is not just about money: by living an active lifestyle, and avoiding smoking and drinking, you can be proactive in minimising the risks.

* Not including senior citizen subsidies. MediShield can pay out $1,000 a month in the case of dialysis.

5. You Make High-Risk Financial Investments

The CPF has three different accounts at interest rates that help grow your nest egg.

The Ordinary Account (OA) interest rate grows your money at 3.5 per cent per annum*. Two other accounts, the Medisave Account (MA) and Special Account (SA) grow your money at 5 per cent per annum.

You can supplement the process by making investments on your own; however, don’t venture into high-risk investments like equities and stocks by yourself.

Speak to a financial advisor about options such as the Singapore Savings Bonds (SSBs). These are conservative investments that are likely to do better than fixed and structured deposits.

You can also use the Supplementary Retirement Scheme to go above and beyond your CPF savings and get tax relief. And with the Retirement Sum Topping Up Scheme, you get interest rates of up to 6% for Special or Retirement** Account savings.

* CPF interest rates are 2.5 per cent for the OA, and four per cent for the MA and SA, until you have a combined amount of $60,000. At this point, you earn an extra one per cent interest on each account. CPF interest rates are revised quarterly.

** Starting 1 January 2016, an additional extra interest of 1% per year will be given on the first $30,000 of your combined CPF balances (for members aged 55 and above) to help enhance your retirement savings. This is on top of the existing 1% extra interest on the first $60,000 of combined CPF balances.

Remember, it is never too late to start. As shown in the beautiful video from CPF, it only gets easier the moment you start building your savings. Visit The Big 'R' Chat for more information on how CPF enhancements can help you with your retirement planning.

Read This Next:

8 Ways for Singaporeans to Afford Having a Baby

4 Best Places to Keep Your Retirement Savings in Singapore

By Rohith Murthy

Rohith leads Singapore’s SingSaver.com.sg, a financial comparison site aimed at helping consumers in Singapore save money and time by finding the right financial products.

Similar articles

The True Cost of Selling Jewellery and Watches in Singapore

How to Use DBS Cashline for Different Financial Needs

5 Misconceptions Singaporeans Have About Disability Insurance

Credit Card Combo: Why Pair DBS Woman’s World Card & DBS Altitude

CIMB StarSaver Account Review: Great For Large Balances

HDB Ownership After Divorce: What Happens Next?

What is Cash Out Refinancing, and How Can Singaporeans Use It?

How Much Insurance Protection Do I Need In 2024?

Back to Blog

Back to Blog -2.png?width=280&name=Insurance%20(2)-2.png)