Is it compulsory for self-employed persons to contribute to their CPF accounts? How much do you have to contribute? Read on to find out.

Regardless of whether you are a seasoned self-employed professional or one of the many who have taken up side jobs and freelance gigs to supplement their income, it is important that you know what kind of CPF contribution is mandatory and what’s not for self-employed persons in Singapore.

It pays to understand the different CPF contribution schemes for self-employed persons and how they can potentially help you in your own personal finance journey. Therefore, this article will cover:

Table of contents

Compulsory self-employed CPF contribution

Self-employed Singapore Citizens or Permanent Residents are required to contribute to their MediSave so long as they earn an annual Net Trade Income (NTI) of more than S$6,000. The NTI is your gross trade income after subtracting all allowable business expenses, capital allowances and trade losses as determined by the IRAS.

This applies even if you are already making regular CPF contributions for income earned from your full-time job — you will have to contribute to your MediSave if your NTI from your side hustle is more than S$6,000 a year. That being said, if your total employment income for the year is more than S$72,000, you may apply to limit the MediSave payable on your self-employed income.

How much MediSave contribution must self-employed persons make annually?

Take note that you have to declare your NTI to the IRAS or the CPF Board using the Self-Employed Person Income Declaration Form.

The exact amount that you have to contribute to your MediSave varies according to your NTI and age. Want the quickest way to find out the payable amount? Simply use CPF’s Self-Employed MediSave Contribution Calculator.

If you’ve already reached the Basic Healthcare Sum, any money that would otherwise be allocated to your MediSave account will go into your CPF SA (or Retirement Account) instead.

When must self-employed persons make their MediSave contributions?

You have 30 days from the date of issuance of the (i) Notice of Computation (NOC) from IRAS or (ii) notification from CPF Board informing you of your MediSave payable to make your MediSave contribution.

Why you need to contribute to your MediSave

Like regular salaried employees, self-employed persons have to plan for their healthcare needs. As you know, medical inflation is real; medical costs will only go up as we age.

The Basic Healthcare Sum (BHS) is the government estimated savings required for basic subsidised healthcare needs in old age. The BHS is adjusted yearly for CPF members below age 65 to keep pace with MediSave usage increase. At age 65, the BHS will be fixed for the rest of their lives.

As of 1 January 2023, the BHS has been updated to the following:

1. For CPF members below 65 years old, their BHS will be raised from $66,000 to $68,500.

2. For members who turn 65 years old in 2023, their BHS will be fixed at $68,500 and will not change thereafter.

For those who are solely self-employed (and hence do not receive regular MediSave contributions from employers), it is even more crucial that they squirrel away money in their MediSave account so that the funds can accrue up to 6% interest per annum and be used to pay for things like:

- MediShield Life premiums

- Integrated Shield Plan premiums

- Approved hospitalisation and medical care expenses, etc

Your MediSave funds earn 4% interest per annum, with the first S$60,000 of your combined CPF balances earning an extra 1% interest per annum. CPF members who are 55 and above can enjoy an extra 1% interest per annum on the first S$30,000 of their combined CPF balances.

You could even receive Workfare Income Supplement (WIS) payouts of up to S$2,667 annually if you contribute to your MediSave and earn an average monthly income of not more than S$2,300.

What happens if you don’t contribute to your MediSave?

Aside from running the risk of having insufficient MediSave funds for your various healthcare needs, you could be hauled to court and wind up facing a fine of up to S$5,000, six-month imprisonment or both for first-time offenders. For subsequent offences, you could be fined up to S$10,000, slapped with a 12-month jail sentence or both.

Under the CPF Act, self-employed persons are legally required to make MediSave contributions as long as their NTI exceeds S$6,000.

While the CPF Board will not hesitate to take recalcitrant self-employed defaulters to court as the last resort, the CPF Board has made it clear it will work with those with genuine financial difficulties so they can settle the outstanding payable amounts to their MediSave over a reasonable period of time. Instalment plans are an option!

That’s not all. You may not be able to register or renew your business registration with ACRA if you don’t make your MediSave contributions.

Must self-employed persons make CPF OA and CPF SA contributions?

It is not compulsory. However, you are free to make voluntary contributions to your CPF Ordinary Account (OA) and Special Account (SA).

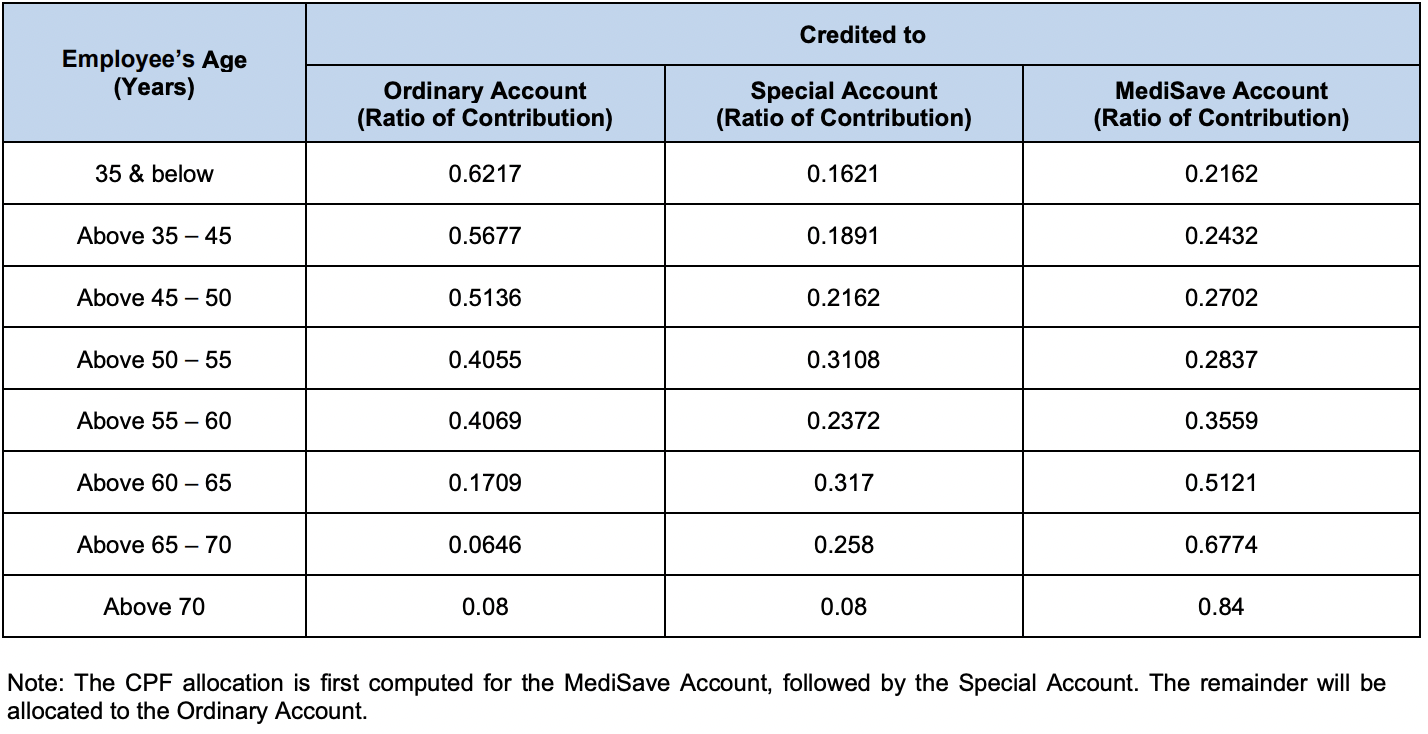

Bear in mind that all voluntary contributions will be allocated across your MediSave, CPF OA and CPF SA according to the same allocation ratios for regular employed CPF members. You may view the allocation ratios here.

Pros and cons of topping up your CPF OA and CPF SA

| Pros | Cons |

| Tax relief | It’s irreversible |

| Higher interest rates than what regular bank accounts offer | You may miss out on opportunities to grow your business |

| CPF monies can be used for housing, retirement, medical or investment purposes | |

| Transfer funds from CPF OA to CPF SA to earn higher interest | |

| Your CPF monies are safe from creditors |

Pro #1: Tax relief

You can save on taxes as you’ll enjoy tax relief based on the MediSave and voluntary CPF contributions that you’ve made, capped at the lower of:

- 37% of your NTI assessed; or

- CPF annual limit of S$37,740; or

- Actual amount you’ve contributed

Pro #2: Higher interest rates than what regular bank accounts offer

Compared to the paltry 0.05% interest per annum that regular bank accounts offer, you might want to consider putting any extra funds you have in your CPF accounts instead.

For CPF members 55 and below, the interest rates for the various CPF accounts hold (if the Government doesn’t revise them downwards):

- OA: 2.5% p.a.

- SA: 4% p.a.

- MA: 4% p.a.

The first S$60,000 of combined balances (capped at S$20,000 for the OA) will earn an additional 1% interest, which will be funnelled into the CPF SA.

Pro #3: Can use CPF monies for housing, retirement, medical or investment purposes

It’s safe to say self-employed persons have the same housing, medical and retirement needs as their employed peers. As such, it makes sense that you voluntarily contribute to your CPF accounts so the funds can grow and accrue risk-free, relatively attractive interest — your CPF monies can be used for your housing, retirement, medical or investment purposes anyway.

Apart from having full control over how much you contribute voluntarily, you also get to enjoy some tax relief in the process!

Start managing and saving money like a pro with SingSaver’s weekly financial roundups! We dole out easy-to-follow money-saving tips, the latest financial trends and the hottest promotions every week, right into your inbox. This is one mailer you don’t want to miss.

Sign up today to receive our exclusive free investing guide for beginners!

Pro #4: Transfer funds from CPF OA to CPF SA to earn higher interest

Did you know you can transfer savings from your CPF OA to your CPF SA to build up your retirement savings quicker? For one, the CPF SA offers higher interest than the CPF OA. Note that the transfer is not reversible.

You can make the transfer if you are:

- Below 55; and

- Have less than the current Full Retirement Sum in your CPF SA, which includes net savings withdrawn under the CPFIS-SA for investments that have not been completely disposed of

Pro #5: Your CPF monies are safe from creditors

If you’re a business owner, you’ll be glad that your CPF savings are protected from creditors and/or the Official Assignee, regardless of how much you may have been sued for Liquidated Damages or if you’ve been declared bankrupt.

If you think about it, setting aside money in your CPF accounts is a smart way to protect your retirement funds from the risk of running your own business.

Con #1: It’s irreversible

The number one con you have to know is that it’s irreversible — you cannot withdraw any money from your CPF OA and CPF SA accounts in cash until you reach 55, assuming you meet whatever criteria CPF Board has set. Your MediSave funds can only be used for approved medical purposes.

Con #2: You may miss out on opportunities to grow your business

If you own a business, having a tidy sum of money on hand could translate into viable business opportunities at the right time and place if you have the means to expand your business and invest in equipment, etc. Remember, all funds in your CPF accounts are illiquid.

Read these next:

Are You Self-Employed? This Is How You Can Save Your Way To Success

A Complete Guide To CPF In Singapore (2021)

4 Reasons Why You Should Voluntarily Contribute To Your Children’s CPF

6 Best Crowdfunding Platforms To Kickstart Your Business

Starting A Side Hustle? These 6 Business Ideas Need Little To S$0 Capital

Similar articles

What Are The Consequences of Dodging CPF Contributions?

6 Things To Take Note Of About The New Changes To CPF Policies

10 Surprising Figures From CPF Board’s 2020 Annual Report To Know About Now

A Complete Guide To CPF In Singapore (2024)

4 Things to Note When Applying for a Loan as a Self-employed Person

Can You Afford to Throw a Punch in Singapore?

4 Reasons Why You Should Voluntarily Contribute To Your Children’s CPF

For Self-Employed Singaporeans, Personal Loans are Tougher to Get

Back to Blog

Back to Blog