T-bills are short-term government bonds that allow you to park your money safely. But are they good investments?

Best Investment Platforms of 2024

Webull Singapore | Tiger Brokers | CMC Invest | Webull | moomoo

The Singapore Treasury Bill, or T-bill, is one of the most popular fixed-income financial instruments around.

Backed by the Singapore government, T-bills are practically risk-free and offer stable returns. They also have a short maturity period of either six months or a year.

But just what are T-bills? And how do they differ from other Singapore Government bonds like the Singapore Savings Bond (SSB) and the Singapore Government Securities (SGS) bond? More importantly, are T-bills good investments?

SingSaver's Exclusive Offer: Open a CMC Invest account and get a S$20 bonus cash via PayNow. Plus, fund a minimum initial amount of S$500 and make 2 trades to receive 1 free Bank of America share (worth S$46) fulfilled by CMC Invest. Valid till 1 May 2024. T&Cs apply.

Additionally, receive 1 Nike share (NYSE:NKE) and/or 1 Tesla Inc. share (NASDAQ:TSLA) when you meet the required deposit and trade with your CMC Invest account. Valid till 1 May 2024. T&Cs apply.

What is the current T-bill interest rate?

The interest rate for T-bills is determined at the auction. Here are the details of the latest T-bill:

|

Issue code |

BY24101X |

|

Tenor |

1 year |

|

Cut-off yield |

3.58% p.a. |

|

Total amount offered |

S$5.1 billion |

|

Total amount applied |

S$10.1 billion |

|

Amount allocated to non-competitive applications |

S$1.2 billion |

|

% of non-competitive applications allocated |

100% |

|

% of competitive applications at cut-off allotted |

Approximately 27% |

|

Bid-to-cover ratio |

1.97 |

|

Announcement date |

11 Apr 2024 |

|

Auction date |

18 Apr 2024 |

|

Issue date |

23 Apr 2024 |

|

Maturity date |

22 Apr 2025 |

The cut-off yield of the latest 1-year T-bill tranche (BY24101X) was 3.58% p.a., which is higher than the previous 1-year T-bill in January 2023, which had a cut-off yield of 3.45% p.a..

However, demand for the latest tranche was lower, with a total of S$10.1 billion in applications for the S$5.1 billion offered, representing a bid-to-ratio of 1.97.

In comparison, the previous 1-year T-bill in January 2023 received S$14.4 billion in applications for the S$4.5 billion on offer, with a bid-to-ratio of 3.19.

Additionally, 100% of non-competitive applications were allocated, amounting to S$1.2 billion, while only about 27% of competitive applications at the cut-off yield were allocated.

The next 1-year T-bill (BY24102W) will be announced on 18 July 2024.

Meanwhile, the next 6-month T-bill tranche (BS24108V) is now open for applications on 18 April, and auctions will start on 25 April.

|

Issue code |

BS24108V |

|

Tenor |

6 months |

|

Cut-off yield |

TBA |

|

Total amount offered |

S$6.6 billion |

|

Total amount applied |

TBA |

|

Amount allocated to non-competitive applications |

TBA |

|

% of non-competitive applications allocated |

TBA |

|

% of competitive applications at cut-off allotted |

TBA |

|

Bid-to-cover ratio |

TBA |

|

Announcement date |

18 Apr 2024 |

|

Auction date |

25 Apr 2024 |

|

Issue date |

30 Apr 2024 |

|

Maturity date |

29 Oct 2024 |

You can view the 2024 auctions and issuance calendar on MAS’ website here.

T-bills Singapore: what are T-bills?

T-bills are government bonds that are backed by the Singapore government, which holds a ‘AAA’ credit rating from credit rating agencies (the highest rating possible). In other words, this means that the risk of losing your money is relatively low (note: it’s not risk-free).

T-bills are deemed short-term bonds with a short maturity period of either six months or a year. They're also issued every fortnightly or quarterly and are sold in denominations of S$1,000.

SingSaver Exclusive Offer: Receive your choice of an Apple AirPods 3rd Gen with MagSafe charging case (worth S$274) or S$200 cash via PayNow when you open a Tiger Brokers account and fund at least USD 1,000. Valid till 2 May 2024. T&Cs apply.

Plus, enjoy prizes worth USD 3,600 when you deposit and trade with your Tiger Brokers account. Valid till 15 July 2024. T&Cs apply.

SSB Vs SGS bonds Vs T-bills: What's the difference?

Here’s an overview comparison between the SSB, SGS bonds, and T-bills:

|

Bond type |

SSB |

SGS bonds |

T-bills |

|

Tenor |

10 years |

2, 5, 10, 15, 20, 30, or 50 years |

Six months or a year |

|

Minimum investment |

S$500 (and in subsequent multiples of S$500) |

S$1,000 (and in subsequent multiples of S$1,000) |

S$1,000 (and in subsequent multiples of S$1,000) |

|

Maximum investment |

S$200,000 overall |

Auction: up to the allotment limit for auction

|

No limit, but up to the allotment limit for auctions |

|

Investment funds |

Cash and SRS |

Cash, SRS, CPF (auction), cash (syndication) |

Cash, SRS, CPF |

|

How often is interest paid |

Every six months, starting from the month of issue |

Every six months, starting from the month of issue |

At maturity |

|

Can redeem before maturity? |

Yes |

No early redemption. Investors can receive the face (par) value at maturity |

No early redemption. Investors can receive the face (par) value at maturity |

|

Type of interest payment |

Fixed coupon with a ‘step up’ interest |

Fixed coupon |

No coupon; issued and traded at a discount to the face (par) value |

|

Secondary market trading |

No |

At DBS, OCBC or UOB main branches; on SGX through brokers |

At DBS, OCBC or UOB main branches |

|

Tax exempted? |

Yes |

Yes |

Yes |

How do I buy T-bills in Singapore?

You can invest in T-bills with cash, funds from your Supplementary Retirement Scheme (SRS) funds, or your CPF savings.

Like SGS bonds, there’s no limit to how many T-bills you can hold, but you can bid up to a maximum of S$1M in each auction.

To buy T-bills, you’ll need the following:

- A bank account with DBS/POSB, OCBC, or UOB

- A Central Depository (CDP) account linked to the bank account that you intend to invest with

- For CPFIS applications: a CPFIS account with DBS/POSB, OCBC, or UOB

- For SRS applications: an SRS account

If you’re investing with cash, you can apply through DBS, OCBC, or UOB ATMs or internet banking (under invest>Singapore Government Securities).

For SRS applications, you can apply through the internet banking portal of your SRS operator (DBS, OCBC, or UOB).

Finally, for CPFIS applications, CPF members can apply online through DBS i-banking portal or POSB digibank online (under invest>Singapore Government Securities). Note there will be a S$2.50 fee (excluding GST) if you use your CPF OA funds.

OCBC and UOB members can also apply online under the CPFIS via their respective services. For UOB, go to investment

Or, you can do it the old-fashioned way by submitting your applications at any branch of your CPFIS bond dealers (DBS/POSB, OCBC, or UOB).

Do T-bills pay out interest?

Unlike the SSB and SGS bonds, T-bills don’t pay out interest. Instead, you buy T-bills at a discount to the par (face) value and receive the par value when the bond matures. In other words, the upfront discount is essentially the profit you earn and you'll receive your full principal amount when the T-bill matures.

For example, if you were to pay S$5,000 to buy a 6-month T-bill bond with a yield of 3% p.a., you would only need to pay S$4,925 upfront. When the bond matures, you’ll receive the full S$5,000 in return, thus earning you S$75.

T-bills interest yields

Another thing to note is the actual interest yield for T-bills is only revealed when the auction results are announced. So unlike the SSB and SGS bonds, where you'll know the exact interest rates you'll be getting before buying, T-bills are auctioned first before the yields are determined.

Back to top

Can I redeem my T-bills early?

One caveat of T-bills is you can't redeem your T-bills before they mature. That said, you can sell them to other buyers in the secondary market through the main branches of DBS, OCBC, or UOB.

|

Bank |

Contact |

Branch address |

|

DBS |

1800-111 1111 |

12 Marina Boulevard Level 3 |

|

UOB |

1800-222 2121 |

80 Raffles Place |

|

OCBC |

1800-363 3333 |

65 Chulia Street |

The drawback of selling in the secondary market is that price swings influence bond prices in the market. In other words, the price that you sell your T-bills might be lower than what you had paid.

Aside from market conditions, another downside to selling your T-bills is a lack of interested buyers. Hence, it’s generally advisable to hold your T-bills until maturity.

T-bills Singapore: what are competitive and non-competitive bids?

Like SGS bonds, T-bills are issued via auctions in competitive and non-competitive bids.

A competitive bid is where you buy T-bills at your desired yield based on the price you're willing to pay. Every competitive bid exercise asks you to state the lowest yield you're willing to accept. The lower the yield, the more competitive it is.

Opt for a competitive bid if you want your funds to be invested only if the cut-off yield is above your specified yield, up to 2 decimal places. A competitive bid is usually for savvy investors.

Note that you will only get the full amount if your bid is lower than the cut-off yield. If your bid equals the cut-off yield, your return might be lower as the allocation is pro-rated.

That said, you're allowed to submit multiple competitive bids, so one strategy is to submit several bids with different amounts to ensure that some of your bids are allocated.

On the other hand, a non-competitive bid is where you specify the amount you want to buy and are willing to accept the discount rate at the auction. This is the best option for most retail investors.

If you want to invest in the bond regardless of the return or are unsure of what yield to bid, go for a non-competitive bid. This method also guarantees you receive the full amount of the T-bill when it matures.

Remember that non-competitive bids will be allocated first, up to 40% of the total issuance amount. However, if non-competitive bids exceed 40%, the bond will be allocated pro-rated. The remaining amount will be given to competitive bids from the lowest to highest yields.

The maximum allotment for non-competitive bids is S$1 million per T-bills auction, which means you can't apply for more than S$1 million in an auction. For instance, if you apply for S$500,000 on the first day and S$600,000 on the second day, you would need to reduce the amount to S$500,000 to apply again.

You may refer to the auction days based on the MAS’ auctions and issuance calendar.

🎉Lucky Draw🎉: Get a chance to win an Apple iPhone 15 128GB (worth S$1,311) when you sign-up for a Webull account and transfer-in a minimum value of USD 5,000. Valid till 2 May 2024. T&Cs apply.

SingSaver Exclusive Offer: Receive your choice of S$100 cash or S$110 Grab Vouchers when you sign up for a Webull account and fund at least S$700 within the promo period. Fund at least S$2,000 to receive S$130 cash or S$140 Grab Vouchers. Valid till 2 May 2024. T&C's apply.

Plus, get up to USD 3,000 worth of NVDA shares when you complete actions with your Webull account. Valid till 2 May 2024. T&Cs apply.

Also, get up to USD 10,450 transfer-in rewards when you transfer in at least USD 500,000 worth of shares and fulfill additional requirements. Valid till 2 May 2024. T&Cs apply.

T-bills Singapore: how to check T-bills auction results?

You’ll be issued T-bills three business days after the results are revealed.

If you applied with cash, you can check your CDP statement.

If you applied with your SRS funds, you can check the statements from your SRS operator (DBS/POSB, OCBC, and UOB).

If you applied with your CPFIS-OA, you can check your CPFIS statement from your agent bank (DBS/POSB, OCBC, and UOB).

For CPFIS-SA, you can check your CPF statement.

T-bills maturity: where will the funds be credited?

When your T-bills mature, the proceeds will be credited to your Direct Crediting Service (DCS) bank account. This may not be the same bank account that you used to apply for the T-bill, but you can check your CDP account to see which bank account is registered as your DCS account.

If you applied with your CPF money, the funds will be credited to your CPFIA or CPF-SA.

Should you invest in T-bills using your CPF savings?

With the latest interest yields of T-bills surpassing the CPF OA's basic 2.5% interest rate per year and around the CPF SA's and RA's 4% interest rate, you may be wondering whether it's a good idea to use your CPF monies to invest in T-bills.

Before deciding to invest with your CPF savings, here are some factors to consider beforehand:

Liquidity

If you foresee yourself using your CPF monies in the near future — be it for buying a property or if you need to withdraw your CPF RA savings (if you’re 55 and above) — within the next six to 12 months, then it’s better to leave your savings in your CPF account than to invest it.

Remember that you can't redeem your T-bills before maturity and would need to sell them in the secondary market if you want to redeem them before maturity.

However, as mentioned, bond prices fluctuate based on the interest rate environment and market conditions, so you might not be able to get back your principal amount.

Additionally, there must also be an interested buyer who's willing to match your price. As such, consider your time horizon before investing in T-bills.

Opportunity cost and fees

When using your CPF monies to invest in T-bills, there are also opportunity costs to consider, particularly the risk of losing out on the CPF interest.

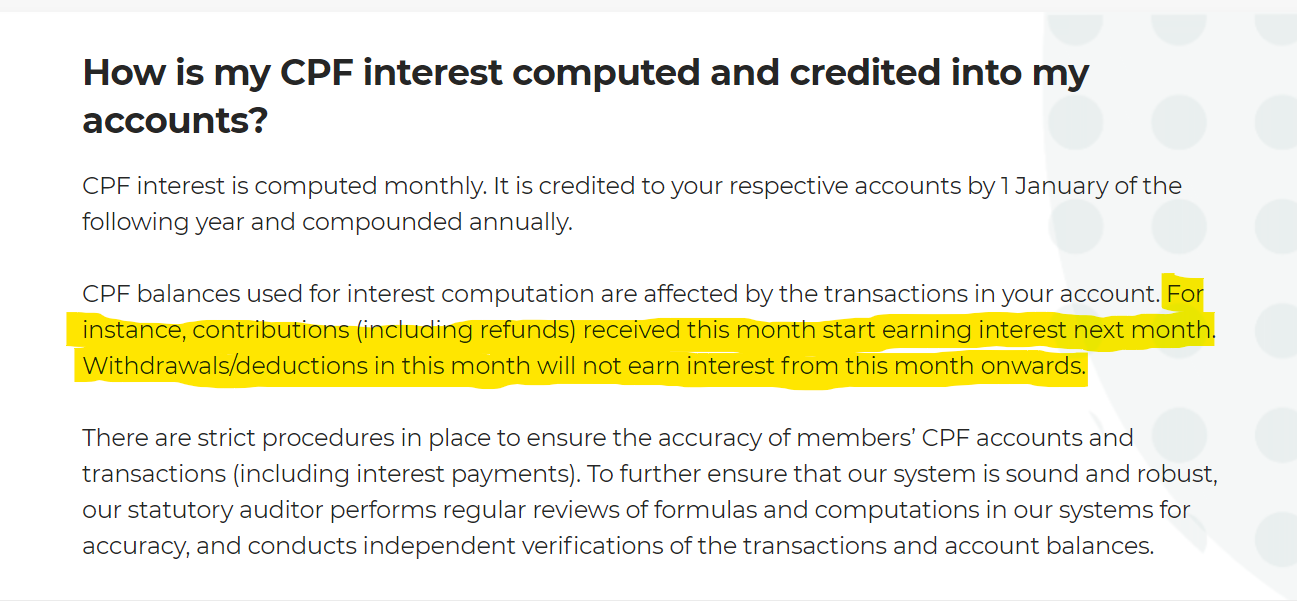

If you didn't already know, CPF interest is computed monthly and compounded annually based on the lowest balance of that month.

For example, CPF contributions received this month will only start earning interest next month. You also won't earn any interest from this month onwards if you withdraw this month.

In other words, this means that you won't earn interest in the months that you use your CPF-OA funds to apply for T-bills until the month after you receive the money back from T-bills into your account.

For example, say that you invested S$10,000 of your CPF OA savings in a 6-month T-bill with a cut-off yield of 4%.

The amount of interest you'll be forgoing in your CPF OA for seven months is: S$10,000*2.5%/12*7 = S$145.80

On the other hand, the yield that you'll receive from the T-bill is S$10,000*4% = S$200.

While the investment returns you get from T-bills are slightly higher, remember that you will be charged a fee for purchasing T-bills, so you need to factor that in too.

When investing with your CPF, you'll incur a one-time transaction fee of S$2.50 + GST and a quarterly charge of S$2 per issue. Hence, investing in a 6-month T-bill will incur a total fee of S$6.50.

So, if you include the fees, the net yield you'll receive is S$200 - S$6.50 = S$193.50.

Therefore, the excess interest earned from T-bills is S$193.50 - S$145.80 = S$47.70.

While money is money, it's debatable whether gaining S$47.70 is worth using your CPF savings for.

Don't forget that you must apply in person at a bank if you invest via CPFIS. Therefore, you'll also need to spend time queuing up, visiting the bank, finding a parking spot, etc.

Losing out on additional interest from CPF

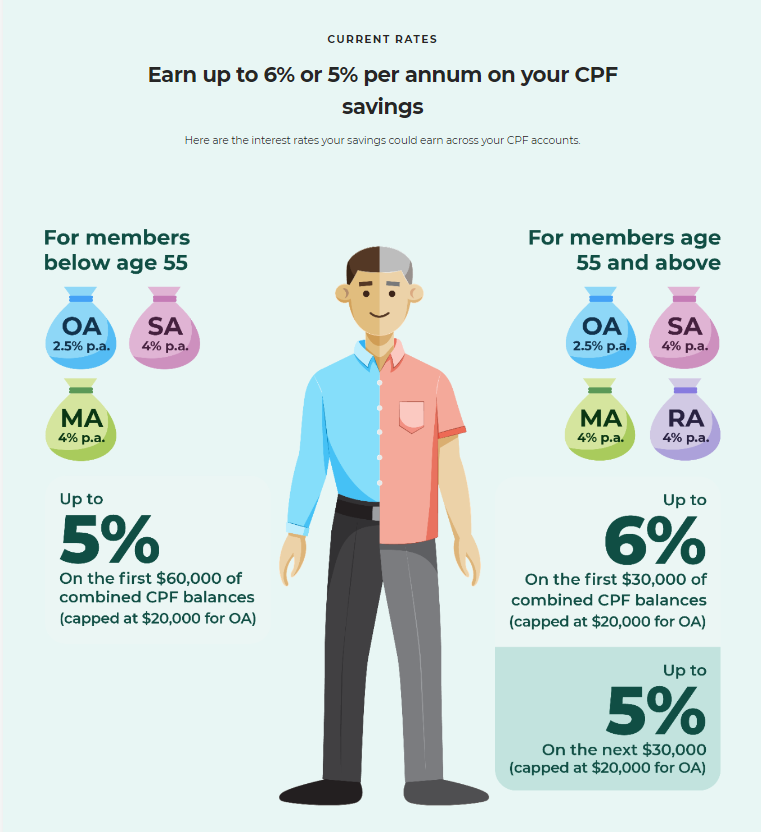

Remember that the government will pay you a bonus interest of 1-2% based on your CPF savings and age.

Those below 55 years old can earn an additional 1% p.a. on the first S$60,000 of their combined CPF balances (capped at S$20,000 of CPF OA). This means that you can earn up to 3.5% p.a. on your CPF OA savings and up to 5% p.a. on your CPF SA and MediSave.

Meanwhile, those 55 years old and above can earn an additional 2% on the first S$30,000 of their combined balances. Again, this is capped at S$20,000 for CPF OA. You'll also earn an extra 1% on the next S$30,000, meaning that you can earn up to 6% p.a. on your CPF retirement funds.

As such, the additional interest given by CPF is still quite attractive, so before using your CPF-OA funds to invest, consider your risk appetite and time horizon.

Are T-bills good investments?

T-bills can be good investments if you want to invest in the short term and park your money in a safe place as their backed by the Singapore government. You’ll also be guaranteed a fixed interest payment when the bond matures and you can start investing with a small capital of S$1,000. Furthermore, there's also no capital gains tax.

That said, while the yield for T-bills is attractive, it's only slightly above the core inflation rate in Singapore, which is currently 5% as of October 2023. T-bills also offer around the same interest rates as fixed deposits and savings accounts, though it's not near their maximum rates.

Another drawback of T-bills is that they aren’t as liquid as the SSB, as you’ll need to sell your bonds in the secondary market if you want to redeem them early. This could also result in losses as bond prices fluctuate according to market conditions.

If you're willing to lock up your money in something for longer, consider investing in the SSB or SGS bonds. But, if you want a short-term investment that offers competitive returns, T-bills might just be the right investment for you.

SingSaver Exclusive Promotion: Receive S$60 cash via PayNow when you open a moomoo universal account and fund a min. of S$100. Fund a min. of S$2,000 to receive an additional S$100 cash (S$160 total) via PayNow. Valid till 1 May 2024. T&Cs apply.

Plus, receive up to S$970 worth of welcome rewards and up to 6.8% p.a. returns when you complete additional actions with your moomoo account. Valid till 1 Jul 2024. T&Cs apply.

Read these next:

The SSB vs CPF: Which One Has Better Returns?

The Best Places To Store Your Emergency Fund

What Are SINGA Bonds (SGS Bonds) And Should You Invest In Them?

The Complete Guide To Singapore Savings Bond (SSB) — Return Rates And How It Works

13 Best Fixed Deposit From Top Banks In Singapore To Lock In Your Savings

Similar articles

Money Mysteries: Why do Bond Values Fluctuate if They are Supposed to be “Fixed Income”?

The SSB vs CPF: Which One Has Better Returns?

Astrea VI Private Equity Bonds: 8 Facts Investors Need To Know About This Hot Bond

The Complete Guide To Singapore Savings Bond (SSB) — Return Rates And How It Works

What Are SGS Bonds And Should You Invest In Them?

5 Things to Consider Before You Invest Your CPF

7 Popular Types Of Investment In Singapore (And Tips To Use Them For Optimal Gains)

When Are Fixed Deposits Better Than Singapore Savings Bonds?

Back to Blog

Back to Blog