Are you part of the endowment target audience? Find out if you are in need of an endowment plan and how they could help you achieve your financial goal.

Endowment plans — like a lot of investment products out there — appeal to certain types of people due to their predictable nature in the form of fixed premiums and guaranteed returns.

If you can relate to any of the following archetypes, it’s safe to say that you’re the target audience and your next course of action is to check out the best endowment plans in the market, pronto.

#1: The one who needs to foot their child’s university fees

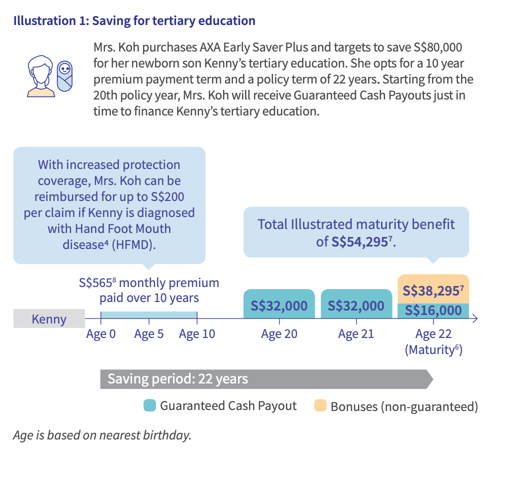

This may come as no surprise to you if you’re looking up endowment. One of the most popular reasons why Singaporeans buy endowment plans is to one day finance their child’s tertiary education. Given that a degree course at Nanyang Technological University (NTU) costs anywhere from $28,000 to $32,000, the appeal of receiving a guaranteed cash payout is undeniable.

Let’s take for example the AXA Early Saver Plus which provides one of the highest guaranteed returns for endowment plans. If you buy it early enough, your plan will mature in time for when your child enters university.

Based on the illustrated investment rate of return of 3.25% p.a. above, if you were to buy the plan right when your child is born, and opt for a 20-year policy term with a monthly premium of $256.36 for a 10-year premium term, you’re projected to cash out a total of $41,685 when the policy matures should you decide for the accumulation option. Seeing as local tertiary education fees could cost upwards of $30,000, the payout amount will go a long way towards defraying other related expenses.

#2: The impulsive spender who needs to grow savings

If you find it hard to set aside money every month to reach a long-term financial goal, endowment plans are certainly the motivation you’re looking for to grow your savings.

They require fixed premium payments scheduled monthly, quarterly or annually for the entirety of your premium term and withdrawals are limited to only once a year (depending on your plan). Unlike merely setting aside a portion of your income in a very accessible savings account, you’ll always have the total maturity payout as an incentive to have a portion of your money locked away (and safe from itchy fingers). There’s also the fixed premium payments to stick to, as you may not lower them or surrender the plan lest you’re comfortable with incurring losses.

#3: The investor looking to diversify

For a healthy financial portfolio, endowment plans are a great addition as they are relatively low-risk and comes with some life insurance coverage over the duration of the plan. It’s a good ‘back-up’ to have in your arsenal as you’d never have to worry about suffering huge losses like say, when faced with a devastating stock market crash.

Opt for a participating endowment plan where you can gain potential non-guaranteed returns to make up for the shortfall in the guaranteed sum portion. The worst that could happen would be if the returns at maturity ended up being lower than the sum of the premiums paid. Also, there’s the possibility of the non-guaranteed portion’s abysmal performance on the market. However, this loss would likely be minimal and you can still get back your savings in the guaranteed portion even if things go awry.

#4: The one who wants to plan ahead for retirement

We often hear that we ought to prepare for retirement early, and that means building up enough savings to last us from the moment we retire up to when we kick the bucket. How many times have we read that if we were to make the right financial decisions during our working years, we’ll be able to live out our days comfortably without worrying about money? Plenty, and with good reason.

Endowment plans certainly help you achieve that goal — particularly if you can hold off the yearly cash withdrawals and park your savings long enough to generate decent returns. With AXA’s SavvySaver, policyholders are able to receive a total projected maturity payout of $100,278 after 21 years, a substantial growth if you consider the $75,600 in premiums paid.

The catch? Leaving it to mature for over two decades with zero withdrawals. Yes, even the yearly cash payouts are to be left alone to reap the maximum potential returns at the 21-year mark.

#5: The one who’s saving up for a new home

Sitting on a pile of cash? Good news: buying an endowment plan is how you can make it work harder to prepare for an upcoming big-ticket purchase, like for your next property. You may want to opt for a non-participating, single-premium endowment plan with high guaranteed returns at maturity.

Consider the DBS SavvyEndowment 4, a participating endowment plan which offers attractive returns of up to 1.39% p.a. With a lump-sum premium payment of $10,000, you’ll be able to cash out from $10,283 (guaranteed) to $10,423 when the policy matures in three years. Alternatively, if you were to store the money in a savings account like the DBS Multiplier Account, you will only be generating an interest rate of 0.9% p.a. (until 31 December 2020).

Read these next:

4 Most Popular Reasons Why People Get Endowment Plans

Best Short & Long Term Endowment Plans in Singapore (2020)

Endowment vs Insurance Savings vs Bank Savings: What’s The Difference?

Best Savings Accounts in Singapore to Park Your Money (2020)

Fixed Deposit vs Singapore Savings Bond (SSB) vs Savings Account: Where To Put Your Money?

Similar articles

Buying Insurance: Pros & Cons Of Limited Premium Payment Term

How to Find the Best Education Endowment Plan in Singapore

4 Most Popular Reasons Why People Get Endowment Plans

7 Things To Consider When Buying Endowment Plans For Your Kids

Endowment vs Insurance Savings vs Bank Savings: What’s The Difference?

Endowment Comparison: Singlife MySavingsPlan vs GE Flexi Cashback vs PRUFlexicash

Fixed Deposits vs. Endowment Plans vs. Cash Management Accounts: Which Should You Choose?

Should You Surrender or Sell Your Endowment Plan?

Back to Blog

Back to Blog