Master Your Finances: The Ultimate Credit Card Interest Calculator

Updated: 11 Dec 2025

Find the right credit card for you in no time. 💳✨

Compare exclusive offers on SingSaver across cashback, miles, and rewards cards—plus enjoy stackable welcome gifts.

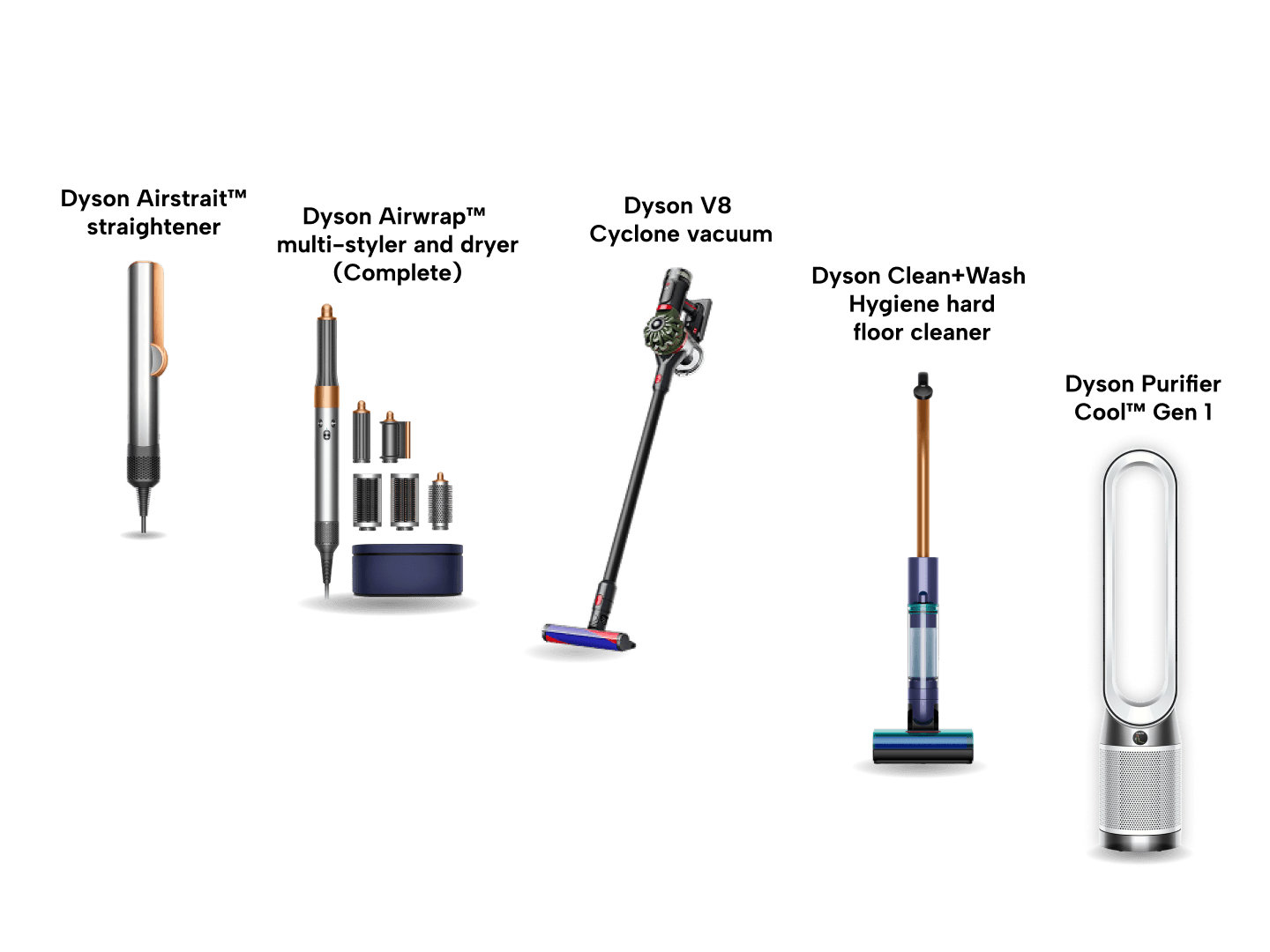

Make Dyson yours today

Apply for select Citi, HSBC, OCBC, DBS and Standard Chartered Credit Cards and a premium Dyson machine as your sign-up gift! Whether it’s a high-tech vacuum or the iconic hair stylers, it’s yours at a fraction of the cost. Exclusive deal, only via SingSaver. Claim your Dyson with a small top-up and required spend – promo ends soon. T&Cs apply.

Understanding Credit Card Interest: The Basics

Credit card interest can appear complex, but it's fundamental to effective money management. Let's delve into the basics of credit card interest and its impact on your finances.

What is Credit Card Interest?

Credit card interest is the fee charged for borrowing money if you don't clear your balance by the due date. It's expressed as an annual percentage rate (APR) and can significantly affect your debt.

How Credit Card Interest Calculator Works

Understanding how to calculate credit card interest is crucial. In Singapore, banks employ the daily balance method. They divide your APR by 365 to determine a daily rate, which is then multiplied by your daily balance and the number of days in the billing cycle.

The calculator will estimate the interest you will accrue if you only make the minimum payment, the time it will take to pay off the balance, and the interest you will end up paying over time.

Factors Affecting Your Credit Card Interest Rate

Several factors can influence your credit card interest rate:

Credit score: A higher score typically results in lower rates

Card type: Rewards cards often come with higher APRs

Market conditions: Economic factors can cause rates to fluctuate (not so relevant in Singapore because of our size).

With an improved credit score, your credit card limit calculator might indicate a higher limit, which could also affect your interest rate.

Frequently asked questions

A credit card interest calculator is a tool that helps you determine the total interest you'll pay on your credit card balance. It takes into account factors such as your current balance, interest rate, and repayment plan to provide an estimate of the total interest and time required to clear your debt.

A credit card debt calculator is a tool that shows you the total debt you'll accumulate if you continue making minimum payments or a fixed monthly payment. It encourages more aggressive repayment strategies to help you become debt-free faster.

By regularly using a credit card interest calculator, you can gain a clear understanding of your debt situation and explore different repayment strategies. This knowledge empowers you to make informed decisions about your credit card usage and repayment plans, potentially saving you thousands of dollars in interest charges over time.