How Many Personal Loans Can You Have at Once? Can You Get More?

Updated: 26 Aug 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

The number of loans and the amount you can borrow depends on the lender’s criteria and approval process. Lenders will evaluate factors such as your income, existing debt, and creditworthiness before approving an additional loan. Taking on several loans could impact your financial health, so it's wise to explore other options and ensure you can manage the repayment of multiple loans without overextending yourself.

Loan | Monthly Repayment | SingSaver Reward | Annual Interest Rate | Total Cost of Loan | EIR | ||

|---|---|---|---|---|---|---|---|

| Standard Chartered CashOne Personal Loan | S$428 | S$410 | From 0.90 % | S$405 | From 1.75 % p.a. | |

| UOB Personal Loan | S$429 | S$430 | From 1.00 % | S$450 | From 1.93 % p.a. | |

| Citi Quick Cash | S$460 | - | 3.45 % | S$1,553 | 6.50 % p.a. | |

| Credible.sg Personal Loan | S$549 | - | 10.56 % | S$4,752 | 10.56 % p.a. | |

| DBS Personal Loan | S$435 | S$750 | From 1.48 % | S$666 | From 3.22 % p.a. | |

| GXS FlexiLoan | S$430 | - | From 1.08 % | S$486 | From 2.02 % p.a. | |

| OCBC Personal Loan - Existing OCBC loan customers | S$464 | - | 3.80 % | S$1,710 | 7.49 % p.a. | |

| POSB Personal Loan | S$435 | S$750 | From 1.48 % | S$666 | From 3.22 % p.a. |

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

How many personal loans can I have at once?

There is no set legal limit on how many personal loans you can have at once, but approval depends on factors such as income, existing debt, and creditworthiness. Some lenders allow multiple personal loans, while others may impose restrictions on the number of loans or the total amount you can borrow.

In Singapore, the Monetary Authority of Singapore (MAS) sets an unsecured credit borrowing limit of up to 12 times your monthly income. This includes personal loans, credit card balances, student loans, and personal lines of credit. If your total unsecured debt exceeds this limit for three consecutive months, you will not be able to access additional unsecured credit.

Can you get two loans from the same bank? Yes. Many banks and financial institutions (FIs) will allow you to get several loans, but they typically have limits. Banks typically allow you to borrow up to six times your monthly income for personal loans. For example, if you earn S$5,000 per month and have a good credit score with no other unsecured debt, you may qualify for up to S$30,000 in personal loans. This could be structured as multiple smaller loans — such as six loans of S$5,000 each — or fewer larger loans, as long as the total amount remains within the approved limit.

Lenders also assess your debt-to-income ratio (DTI), credit score, and existing financial commitments when reviewing loan applications. While some may approve a personal loan without proof of income, they will generally require alternative financial assurances to mitigate risk.

Before applying for another loan, it is important to watch for warning signs that your debt may be getting out of control.

Can I get multiple loans from the same lender?

Yes, you can take multiple loans from the same lender in Singapore, but approval depends on factors like your income, credit score, and existing financial commitments. Banks typically assess your total loan eligibility rather than restricting the number of loans you can have. Some lenders may require you to make a minimum number of repayments on an existing loan — often around six months — before considering a new loan application.

The table below outlines the borrowing limits offered by some of Singapore’s leading lenders.

|

Lender |

Maximum loan amount |

|

Trust Bank Instant Loan |

SGD $50,000 |

|

CIMB Personal Loan |

SGD $50,000 |

|

Standard Chartered CashOne Personal Loan |

SGD $50,000 |

|

UOB Personal Loan |

SGD $50,000 |

|

Credible Personal Loan |

SGD $50,000 |

It’s essential to understand how to manage your personal loan effectively to maintain a good repayment history. Timely payments not only help in getting approval for future loans but also protect your credit score and financial health. For added convenience, you can even apply for loans online, which streamlines the process and allows you to keep track of your finances without leaving home.

>> Learn how to manage your personal loan

Thinking of another loan?

Navigate multiple loans with ease. Find the best options and manage your debt smartly.

How to qualify for another personal loan

Even if a lender allows multiple loans, qualifying for a second or third loan isn't guaranteed. Lenders carefully assess several factors to determine your creditworthiness and ability to repay multiple debts. Here are some key eligibility factors:

-

Debt-to-income ratio (DTI): Your debt to income ratio is a ratio that compares your monthly debt obligations against your gross monthly income to determine if you can handle additional debt. In Singapore, the Total Debt Servicing Ratio (TDSR) cap is 55% of your gross monthly income, meaning your total loan repayments — including any new loans — must not exceed this threshold. If your DTI is too high, securing another loan may be challenging.

-

Credit score: A good credit score is essential for loan approval. Lenders use your credit history to gauge your creditworthiness. A higher credit score generally translates to lower interest rates and better loan terms. Multiple loan applications can sometimes have a temporary impact on your credit score, so it's important to be mindful of this.

-

Income requirements: Lenders have minimum income thresholds for personal loans, which become even more crucial when applying for multiple loans. They will assess whether your current income is sufficient to support additional repayments without financial strain. Borrowers with higher incomes and stable employment generally have a better chance of approval.

Before applying for another personal loan, use a personal loan calculator to estimate your monthly repayments and assess whether your debt remains manageable. Meeting your lender’s eligibility criteria reduces the risk of rejection or unfavourable loan terms.

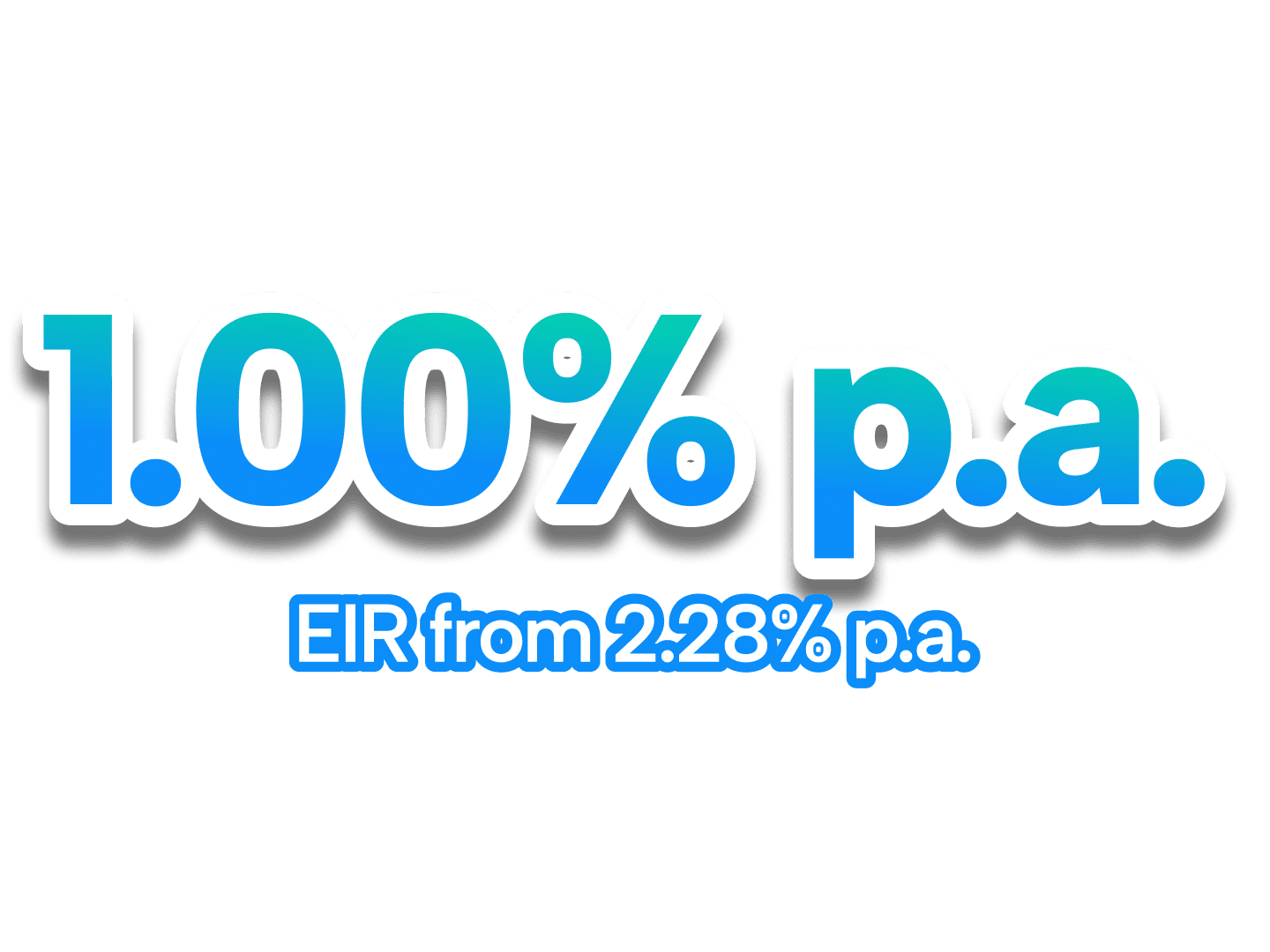

⚡SingSaver x Trust Personal Loan Flash Deal⚡

Enjoy low interest rates from 1.00% p.a. (EIR 2.28% p.a.) plus up to S$1,750 in cashback and rewards when you sign up for Trust Bank Personal Loan via SingSaver. Plus, receive a S$10 FairPrice E-Vouchers from Trust when you sign up with the referral code SINGSAVE. Valid till 2 August 2026. T&Cs apply.

Will having multiple personal loans affect credit scores?

Applying for and managing multiple personal loans can impact your credit score in several ways in Singapore. Each loan application typically triggers a hard credit inquiry, which can temporarily lower your score. Furthermore, having multiple outstanding loans increases your overall debt burden, which can also negatively affect your credit score. It's vital to assess your financial situation and ensure you can comfortably manage the repayments before taking on additional debt.

Other alternatives to personal loans

If you're hesitant about taking out another personal loan, consider these alternative financing options available in Singapore:

-

Credit cards with 0% instalment plans: Many credit cards offer 0% interest instalment plans for specific purchases. This can be a good option for managing large expenses without incurring interest charges, provided you repay the balance within the promotional period.

-

Personal lines of credit: A personal line of credit offers more flexibility than a traditional loan. You can borrow and repay funds as needed, up to a pre-approved credit limit. This can be useful for managing fluctuating expenses.

-

Buy now, pay later (BNPL) services: Buy now, pay later services are increasingly popular for smaller purchases. They allow you to split payments into instalments, often without interest. However, it's crucial to manage BNPL obligations carefully, as missed payments can impact your credit score.

-

Salary advance loans: Some financial institutions and fintech companies offer salary advance loans, which allow you to access a portion of your upcoming salary. These loans are typically for smaller amounts and come with fees or interest charges.

-

Medical payment plan: If you have medical expenses, consider medical credit cards or specialised payment plans that allow you to manage bills in instalments.

-

Consider taking a secured loan: Unlike unsecured personal loans, secured loans require you to offer something valuable, like your car or house, as a guarantee. Because this lowers the risk for the lender, your chances of being approved are higher. Just remember, if you fail to make payments, the lender can take your collateral.

-

Go to a pawn shop: If you need quick cash, a pawnshop could just be the solution. Basically, you bring in something valuable, and they give you a loan based on its worth. Pay it back with interest, and you get your stuff back. Don't pay it back, and they can sell it. It's fast, for sure, but remember that pawn shops tend to have high interest rates.

-

Apply for government financial assistance: If your loan application is rejected and you're really in a tough spot, you can consider government support. In Singapore, programmes like ComCare provide short and long-term financial aid to low-income individuals and families. They offer cash grants, help with bills, and employment support. Simply visit the Ministry of Social and Family Development's website to check if you're eligible.

-

Home equity loan: A home equity loan enables homeowners to borrow against the equity in their property, using it as collateral. Functioning as a second mortgage, it provides a lump sum that can be used for various purposes, such as home renovations, debt consolidation, or investment opportunities.

>> Discover more about home equity loans

-

Explore other income sources: Consider finding ways to earn extra side income to help pay down your existing loan and improve your debt-to-income (DTI) ratio. Generating additional income can ease financial stress and make managing your debt more manageable.

What is a personal loan and why would you need one?

A personal loan is a type of unsecured loan that enables you to borrow money without having to put any of your assets (such as your home or car) as collateral. This means that if you fail to repay your personal loan, the lender can’t take your assets. However, failing to repay your personal loan will do some serious damage to your credit score.

Aside from financial emergencies like paying for medical bills and home repair work, people take out personal loans for a variety of reasons, including:

So, how do personal loans work? It’s pretty simple.

Let’s say you want to borrow S$10,000 from a bank at a 5.79% annual interest rate with a repayment period of five years. Your personal loan is amortised, meaning your repayments would include the principal loan amount plus interest. You may also need to pay a processing fee of about 2% of the principal loan amount.

Here’s a breakdown of this example:

| Description | Amount |

| Personal Loan | S$10,000 |

| Annual Interest Rate | 5.79% |

| Loan Tenor | 5 years (60 months) |

| Processing Fee | S$200 |

| Monthly Repayments | S$215.00 |

| Total Cost of the Personal Loan | S$12,900.00 |

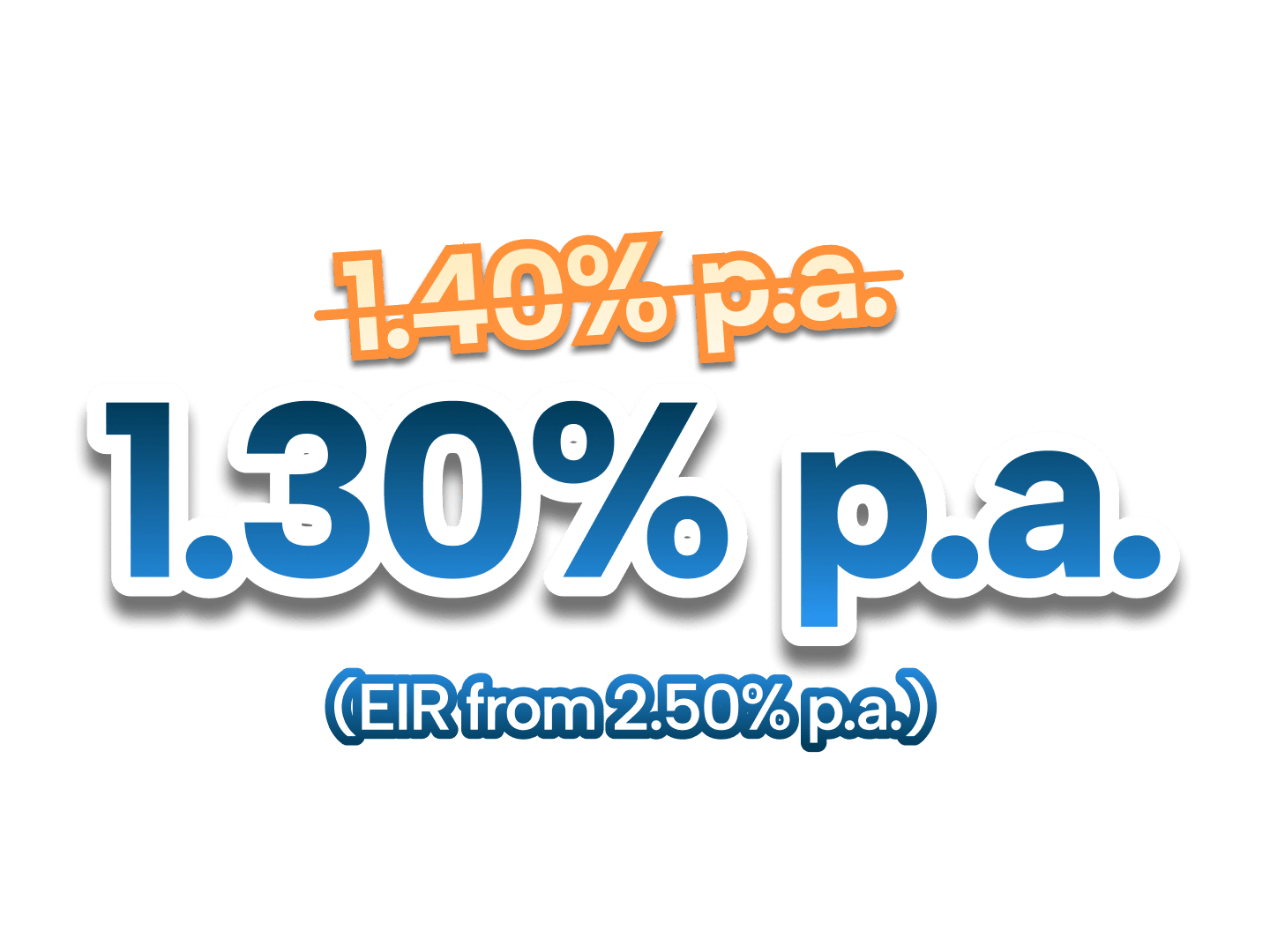

SingSaver x HSBC Personal Loan Exclusive Offer

Enjoy attractive interest rates from 1.30% p.a. (EIR from 2.50% p.a.) when you apply for HSBC Personal Loan via SingSaver. Available to new and existing customers! Valid till 2 August 2026. T&Cs apply.

Managing multiple personal loans

Managing one or more personal loans can be a challenge. If your monthly financial obligations are very manageable and your debt-to-asset ratio is low, you are probably in a better capacity to manage multiple personal loans.

If you have multiple monthly financial obligations and your debt-to-asset ratio is 50% or greater, you will need to re-evaluate your finances to reduce that number.

Here are some ways you can manage multiple personal loans better:

-

Evaluate your debt-to-asset ratio to understand your financial situation better

-

Prepare a budget to maximise the efficiency of your financial resources

-

Consolidate high-interest unsecured debt to help manage credit card bills and other unsecured credit debt

-

Work with the bank or FI to restructure or consolidate personal loans to make repayment easier on your budget

Managing multiple loans is doable if you understand your finances, create a budget, and stick with a repayment plan.

If you need to get one or more personal loans, make sure you select a loan package that provides a low annual interest rate and minimal processing fees. Remember, you may adjust your loan tenor to reduce the financial impact of your monthly repayments.

What to consider before getting multiple personal loans

Although you can get two or more loans from the same bank or other online lenders, it's best to think it through first. Here are a few key aspects you should consider before proceeding:

-

Repayment plan: Before taking on multiple loans, create a detailed budget that accounts for all loan payments. Make absolutely sure you have sufficient income to cover these new obligations, along with your existing expenses, to avoid falling behind. If your income is a concern, there are personal loans for low-income earners you can explore, which might offer more manageable terms.

-

Interest rates: Compare interest rates from different lenders. Higher rates significantly increase the overall cost of borrowing, so securing the lowest rate possible is crucial for each loan.

-

Adherence to good financial habits: Taking on more debt requires disciplined budgeting and spending. Avoid unnecessary expenses and prioritise timely loan payments to maintain a healthy financial standing.

-

Find other alternatives: Before committing to multiple loans, explore other options. Could you adjust your budget, seek a temporary side hustle, or negotiate with your current lenders to avoid taking on more debt?

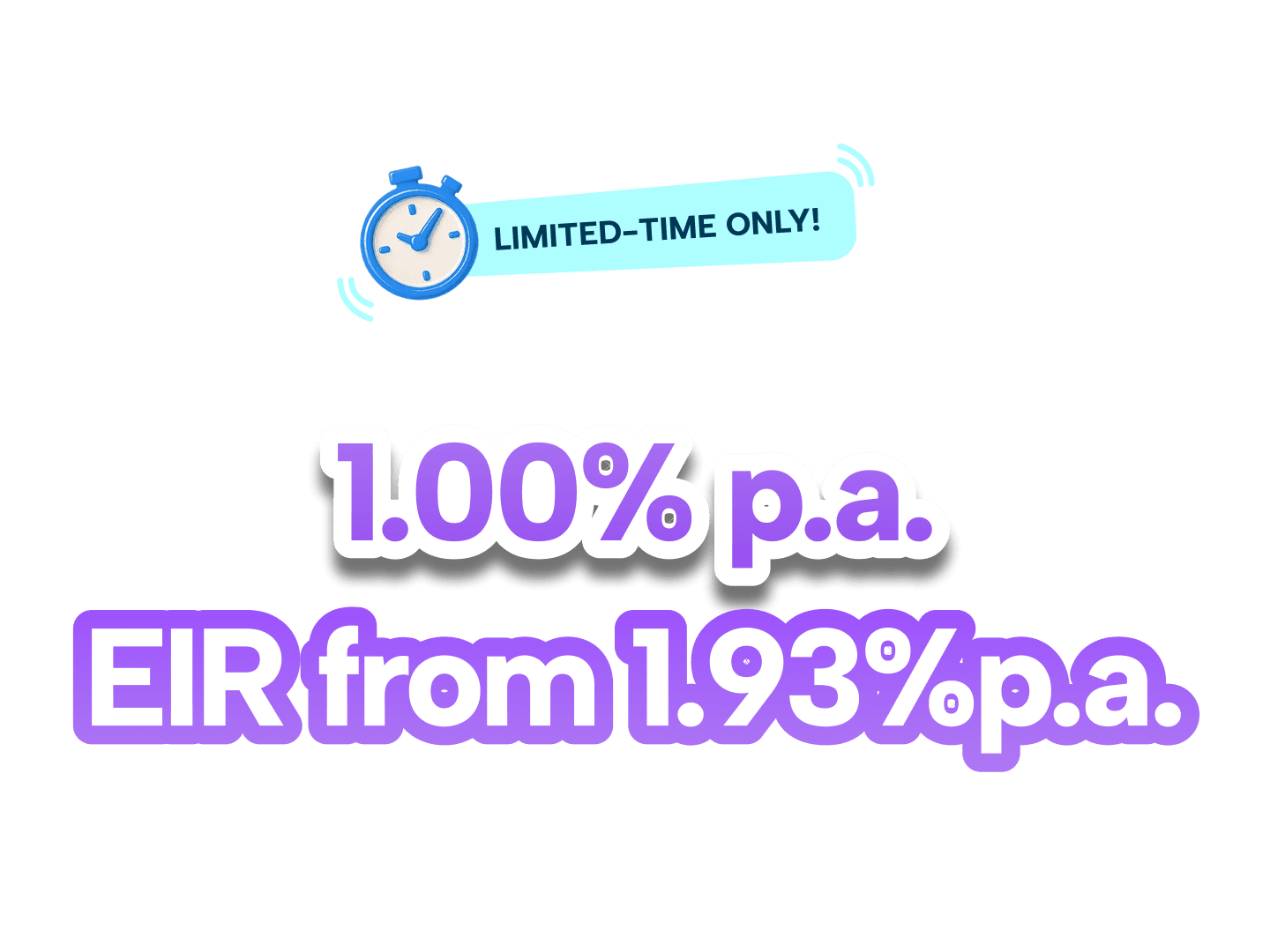

⚡SingSaver x UOB Personal Loan Flash Deal⚡

Get one of the lowest interest rates from 1.00% p.a. (EIR from 1.93% p.a.) plus up to S$1,900 in cashback and rewards when you apply for a UOB Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Frequently asked questions about getting multiple personal loans

There's no set time frame, but it's wise to wait until you've made consistent, on-time payments on your existing loan for at least a few months. This demonstrates responsible borrowing. Lenders also prefer to see a reduced debt-to-income ratio before approving a new loan. Rushing into another loan too soon can negatively impact your credit score and financial health.

While technically possible, paying off a personal loan with another one is generally not advisable. This can create a dangerous cycle of debt, as you're simply shifting the debt around rather than actually paying it off. Plus, you'll likely incur more fees and interest.

Before resorting to this tactic, consider exploring other options, like debt consolidation. However, if your debts have become unmanageable, applying for a debt repayment scheme could provide a structured way to address your obligations without accumulating further debt.

Yes, you can generally pay off a personal loan early or all at once. This can save you a significant amount of money on interest. However, some lenders impose a prepayment penalty for early payoff.

These penalties are put in place to compensate the lender for the lost interest revenue when a loan is repaid before the end of its agreed term. Always review your loan agreement to ensure that early payment, which might incur prepayment penalties, is cost-effective.

Planning your dream wedding? Know your financing options

From venue bookings to bridal packages, weddings can be costly. Find out whether a personal loan or credit makes more sense for your big day.

Estimate your loan repayments

Input your desired loan amount and repayment period to see potential monthly repayment estimates from various lenders. Discover loan options tailored to your financial needs and make informed decisions. Get started now and find the right loan for you.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.