Best High Interest Savings Accounts In Singapore (2025)

Updated: 23 Sept 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Make your money work for your savings goals with a high-yield savings account. Used right, this is a valuable tool for Singaporeans looking to grow their savings, provided you understand how to utilise it effectively.

Find the right bank account for your needs

Easily compare savings accounts across banks in Singapore. Get details on minimum deposits, minimum and maximum interest rates, as well as sign-up offers at a glance.

With rising costs of living and growing financial stress among Singaporeans, saving habits have shifted. More people are prioritising long-term goals like retirement and emergency buffers over discretionary spending. According to a recent report by Fund Selector Asia, nearly 6 in 10 Singaporeans are now more focused on saving for retirement than maintaining their current lifestyle. In this new environment, finding a savings account that offers both security and meaningful returns is more important than ever.

That’s where high-yield savings accounts come in. These accounts offer higher-than-average interest rates, to help your money grow while remaining accessible. In this guide, we break down how they work, which banks are offering the best rates in 2025, and how to maximise your returns.

Which banks in Singapore have the best savings interest rates?

|

Minimum Deposit |

Annual Interest Rate |

Offers & Rewards |

||

|

Standard Chartered Bonus$aver |

S$3,000 |

Up to 8.05% |

High rates with card spend and GIRO bills |

|

|

HSBC Everyday Global Account |

S$ 2,000 |

Up to 3.55% |

Multicurrency, cashback options |

|

|

CIMB StarSaver Account |

S$100,000 |

Up to 2.70% |

Zero monthly fees or hidden charges, convenient top-up options |

|

|

UOB One Account |

S$1,000 |

Up to 5.3% p.a. |

Bonus for salary + card spend |

|

|

OCBC 360 Account |

S$1,000 |

Up to 6.30% |

Interest boosts across 6 categories |

|

|

DBS Multiplier Account |

No minimum |

Up to 4.10% |

Rewards across salary, spend, and invest |

*Rates accurate as of July 2025. Actual rates may vary depending on fulfilment of bonus conditions.

Standard Chartered Bonus$aver

- Earn up to 5.85% interest p.a. on deposit balances of up to S$100,000 with Bonu$aver.

- Unlock Invest category to enjoy 1.5% p.a. bonus interest for first 6 months

- Additional 4.35% p.a. interest when you insure, spend or credit your salary.

- T&Cs apply.

- Transact in up to 14 currencies from your account, convert at competitive FX exchange rates and enjoy S$0 fees for overseas transactions

- Invest a minimum of S$30,000 in an SC Invest portfolio and earn 2.50% p.a. bonus interest for 6 months on your Bonus$aver account

- MoneyLock: Protect your funds from scams and unauthorised transfers or withdrawals with our new anti-scam security feature.

- Read our full review of the Standard Chartered Bonus$aver

- Fall-below fee of S$5 if average daily balance falls below S$3,000

- Early closure fee of S$30 if account is closed within 6 months

- The average daily balance eligible for bonus interest is subject to a cap of S$100,000 per Bonus$aver account. Any average daily balance amount in excess of the cap is not eligible for bonus interest (but the prevailing interest rates will apply)

SingSaver’s take

The Standard Chartered Bonus$aver account is one of the most rewarding high-yield savings accounts available in Singapore for 2025, boasting a headline rate of up to 8.05% p.a. on your first S$100,000 when you fulfil multiple criteria. It's designed to reward a holistic banking relationship — salary crediting, card spending, insurance, investing, and bill payments all contribute to unlocking better interest rates. For committed users who channel most of their financial activity through Standard Chartered, this really delivers on value.

Pros

Up to 8.05% p.a. on the first S$100,000

Uncomplicated balance tiers

Access and transact in 14 currencies with no FX fees

Even meeting just salary and card-spend criteria gets you solid returns

Cons

Multiple conditions needed for maximum yield: Salary, card-spend, invest, insure, bill-pay

Realistic yield is around 3.05% unless all criteria are met

Fall-below fee of S$5 monthly if average balance goes under S$3,000

Investment/insurance bonus valid for only six months

HSBC Everyday Global Account

HSBC Everyday Global Account

- Receive up to S$600 in cashback and bonus interest every month through the HSBC Everyday+ rewards programme

- Bonus cashback and interest granted by spending on HSBC debit/credit cards, making GIRO bill payments, and increasing account balance

- Sign up using SingPass MyInfo to enjoy a quicker application process

- Global Transfers lets you transfer funds to your other HSBC accounts instantly

- Get real-time exchange rates with HSBC's Online GetRate feature

- S$0 withdrawal fees at HSBC ATMs worldwide except for Argentina, Brazil, France, Greece, and several other nations

- Insured up to S$75,000 by SDIC. Additional T&Cs apply

- Standing instruction fee of S$10 per item

- Fall-below fee of S$5 if average daily balance falls below S$2,000

N/A

SingSaver’s take

The HSBC Everyday Global Account is a polished, multi-currency savings solution tailored for globally mobile individuals, offering both convenience and solid rewards. That blend of interest and cashback, plus support for 11 currencies and fee-free overseas cash withdrawals, makes it especially appealing to frequent travellers, expatriates, or anyone needing easy currency access while still earning a competitive return. However, the HSBC EGA is optimised for those who can consistently meet its reward conditions. Without fulfilling these criteria, the interest rate drops to a simple 0.05% base rate, which is low for a high-yield account.

Pros

Potential to earn up to 3.55% p.a. on fresh SGD deposits during promotions

1% cashback on debit card transactions and GIRO bill payments

Supports multi-currency balances in up to 11 currencies with zero FX or withdrawal fees

Fee‑free global ATM withdrawals in most countries

Digital onboarding via Singpass/MyInfo makes sign-up quick and easy

Cons

Base interest is only 0.05% p.a. without bonuses

Bonus interest and cashback require depositing fresh funds and at least five transactions monthly

Promotional bonus interest currently limited

Bonus interest caps apply (e.g., S$5 million incremental deposit limit)

CIMB StarSaver Account

CIMB StarSaver Account

- Enjoy attractive interest rates up to 3.30%* p.a. without multiple conditions

- No fall-below fee, monthly service fees or multiple conditions

- Hassle-free Online Account Opening process

- Earn 3.30%* p.a. with no cap for balances above S$250,000

- Insured up to S$100,000 by SDIC. Additional T&Cs apply.

- Minimum initial deposit of S$1,000

SingSaver’s take

CIMB StarSaver is a standout if you're after a simple, high-yield savings account that rewards your balance, not your activity. With tiered interest rates reaching up to 2.70% p.a. on the first S$5 million, it's one of the rare accounts offering competitive returns without needing salary crediting, card spend, or bill pay.

The account works best for those with larger deposits as you’ll only reach the top tiers if you consistently hold S$150,000 or more. It's also worth noting there’s a S$1,000 minimum to earn interest and an early-closure fee, which makes it less fluid than accounts with no deposit minimum.

Pros

Up to 2.70% p.a. interest on balances across S$5 million

No salary crediting, card spend, or bill payment required

Daily interest accrual, monthly crediting

No fall-below monthly fees, transparent and low-cost structure

SDIC-insured up to S$75,000

Cons

Must maintain at least S$1,000 to earn any interest

Early closure fee of S$50 if closed within six months

Returns only begin to excel at high balances (S$150,000+)

No bonus or promotional rates

No salary credit or spending incentives for modest savers

UOB One Account

UOB One Account

- Earn up to 7.8% interest p.a. on your first S$75,000 when you credit a min. salary of S$1,600 or make 3 GIRO transactions monthly and make a min. credit card spend of S$500

- Choose between salary crediting or GIRO transactions to score higher interest rates, lowered salary requirement of $1,600

- Earn up to 10% cash rebate when you spend on your UOB One Credit Card or Debit Card

- Link Mighty FX to your One Account for competitive exchange rates

- UOB Mighty mobile app allows for tracking of transactions that earn bonus interest

- Insured up to S$75,000 by SDIC. Additional T&Cs apply.

- 6-month fall-below fee waiver for accounts opened online

- Read our full review of the UOB One Account

- Fall-below fee of S$5 if average monthly balance falls below S$1,000

- Early closure fees of S$30 if account is closed within 6 months

SingSaver’s take

UOB One Account makes high-yield savings straightforward by only requiring two monthly actions, card spend and salary credit. It’s ideal for busy individuals seeking high returns with minimal effort, and avoids complicated bonus categories. However, balances above S$150,000 earn only the base rate of 0.05%, and the recent rate cut suggests that returns may soften over time.

Pros

Simple requirements, card spend + salary or GIRO

Daily interest accrual, monthly crediting

No need to buy insurance/investments

Backed by SDIC up to S$75,000

Cons

Base rate of 0.05%

Rate may reduce as market conditions change

Early account closure fees apply

OCBC 360 Account

OCBC 360 Account

- Earn bonus interest p.a. on the first S$75,000 of your account balance

- Score higher interest rates when you credit your salary, spend on your credit card, invest, insure, and increase your account balance every month

- Insured up to S$75,000 by SDIC. Additional T&Cs apply.

- Read our full review of the OCBC 360 Account

- Fall-below fee of S$2 if average daily balance falls below S$3,000 (first-year waived)

- Early closure fees of S$30 if account is closed within 6 months.

SingSaver’s take

OCBC 360 has traditionally rewarded customers who take a more active approach — salary crediting, spending, saving, investing, or buying insurance — to earn bonus interest. Up to 3.3% p.a. is achievable across the first S$100,000 before August 2025. It’s still a decent option, especially if you’re already engaging with OCBC products, but the declining rates make it less compelling compared to simpler alternatives.

Pros

Bonusable interest up to 3.3% on first S$100,000

Multiple bonus streams: Salary, spend, save, insure, invest

Accounts suit those who maintain active banking relationships

Cons

Requires juggling 4-5 bonus categories

Bonus rates may not justify the effort for casual savers

DBS Multiplier Account

DBS Multiplier Account

- Earn up to max. 3% p.a on your first S$100,000

- Enjoy at least 0.30% p.a. interest rate by making a PayLah! retail spend, no min. transaction amount required

- Boost interest rate by increasing your total eligible transactions per month (i.e. salary crediting, credit card spend, investments, insurance)

- Transfer foreign currency funds overseas directly with your account at zero or lower fees. Learn more.

- No initial deposit required

- No monthly account fees

- No minimum average daily balance required if this is your first DBS/POSB account

- Insured up to S$75,000 by SDIC. Additional T&Cs apply.

- Read our full review of the DBS/POSB Multiplier Account

- Popular

- Fall-below fee of S$5 if average daily balance falls below S$3,000

- Early closure fees of S$30 if account is closed within 6 months

SingSaver’s take

DBS Multiplier rewards you for consolidating your banking with DBS. By crediting salary, making card or PayLah! spending, paying home loans, or investing, you can earn up to 4.1% p.a. on the first S$100,000, a strong offer that stands out for frequent DBS users. It’s excellent for savers with diverse DBS activities, though those with minimal engagement may only earn 1.8%.

Pros

Up to 4.1% p.a. on S$100K for fulfilling three categories

Recognises a range of DBS transactions: salary, spending, loans, insurance, investments

Daily balance accrual with monthly crediting

Cons

Base rate only 0.05%

Requires active use across multiple DBS products

Bonus only applies to first S$100K

A guide to choosing the best high-interest savings accounts

With numerous savings accounts offering varying interest rates, bonus conditions, and promotional rates, finding the best one can be overwhelming. But it doesn’t have to be. The key is to match the account’s structure to your financial habits.

These are the essential factors to consider before opening a high-yield savings account in Singapore.

-

Compare rates offered by various banks – Interest rates can vary significantly from bank to bank, and even across different tiers within the same account. Always compare base rates, bonus rates, and caps on eligible balances to ensure you're getting the best deal for your money.

-

Pay attention to terms and conditions – High returns often come with strings attached — such as crediting your salary, maintaining a minimum spend on a linked credit card, or performing specific transactions each month. Ensure you understand the necessary actions to unlock the highest interest tier.

-

Look for hidden fees – Some accounts come with fall-below fees, ATM fees, or account closure charges. These can erode your returns over time, so read the fine print carefully before making a commitment.

-

Check out the conditions for earning the highest rate – It’s not enough to look at the headline rate, as you’ll need to fulfil all the right conditions to get it. These can include salary crediting, bill payments via GIRO, or investing through the bank. If you can’t meet all the requirements, you may earn far less than advertised.

-

Look out for temporary promotions – Some high rates may only apply for a limited time as part of a promotional campaign. While these can be attractive in the short term, make sure you’re also happy with the long-term rate once the promo ends.

Compare the best bank accounts in Singapore 2025

From high-yield savings to multi-currency accounts, find the right bank account that fits your goals.

How to make the most of your high-interest savings account

To maximise your returns, start by automating any required actions — such as salary crediting or monthly card spend — to ensure you consistently qualify for bonus interest. Spread your funds strategically across different accounts if you're hitting interest caps (e.g. only the first S$50,000 may earn high rates).

Also, review your account regularly to ensure it still meets your needs. Banks may change their terms, and better options may appear over time.

How to open a high-interest savings account in Singapore

Opening a high-yield savings account in Singapore is typically a smooth and straightforward process, especially with digital banking making most applications fully online. Whether you're opening your first account or switching to one with better returns, here’s how to get started:

Step 1: Compare your options

Start by reviewing the available high-yield savings accounts on the market. Consider your monthly income, spending habits, and how much effort you're willing to put in to meet bonus interest requirements. Use comparison tools (like the one on SingSaver) to shortlist accounts that match your lifestyle.

Step 2: Check eligibility

Make sure you meet the account’s eligibility criteria. In most cases, you’ll need to:

-

Be at least 18 years old

-

Be a Singapore citizen, permanent resident, or foreigner with a valid pass

-

Have a valid NRIC or FIN

-

Have a local mobile number and address

Some banks may also require income proof, especially if salary crediting is part of the bonus interest conditions.

Step 3: Prepare your documents

If you're applying online via Singpass MyInfo, most of your documents will be pulled automatically. If not, you may need:

-

A copy of your NRIC or passport

-

Proof of address (e.g. utility bill or bank statement)

-

Proof of employment or income (e.g. payslips or CPF contribution history)

Step 4: Apply online or at a branch

For most banks, the fastest way to apply is via their website or mobile app using Singpass MyInfo. This pre-fills your personal information, speeding up the verification process. Alternatively, you can apply in person at a branch if you prefer face-to-face service or need help with complex requirements.

Step 5: Fund your account

Once your account is approved and activated, transfer your initial deposit (if required). Some banks have no minimum deposit, while others may require S$1,000 to S$3,000 to start earning interest.

Step 6: Set up bonus fulfilment (if applicable)

To unlock the highest interest rates, complete any required actions such as:

-

Crediting your salary to the account

-

Spending a set amount on a linked credit card

-

Paying bills via GIRO

-

Investing or purchasing insurance through the bank

Automate these tasks where possible to avoid missing out on bonus interest.

Step 7: Monitor your progress

Log in to your banking app regularly to check if you've met the bonus criteria. Some banks provide interest calculators or progress bars to help you visualise how much interest you're earning each month.

By following these steps, you can quickly get your high-yield savings account up and running — and start earning more from your everyday cash.

Expand Beyond SGD with a Multi-Currency Account

Hold and grow your savings in multiple currencies. Earn interest, avoid frequent conversion fees, and be ready for travel or overseas spending.

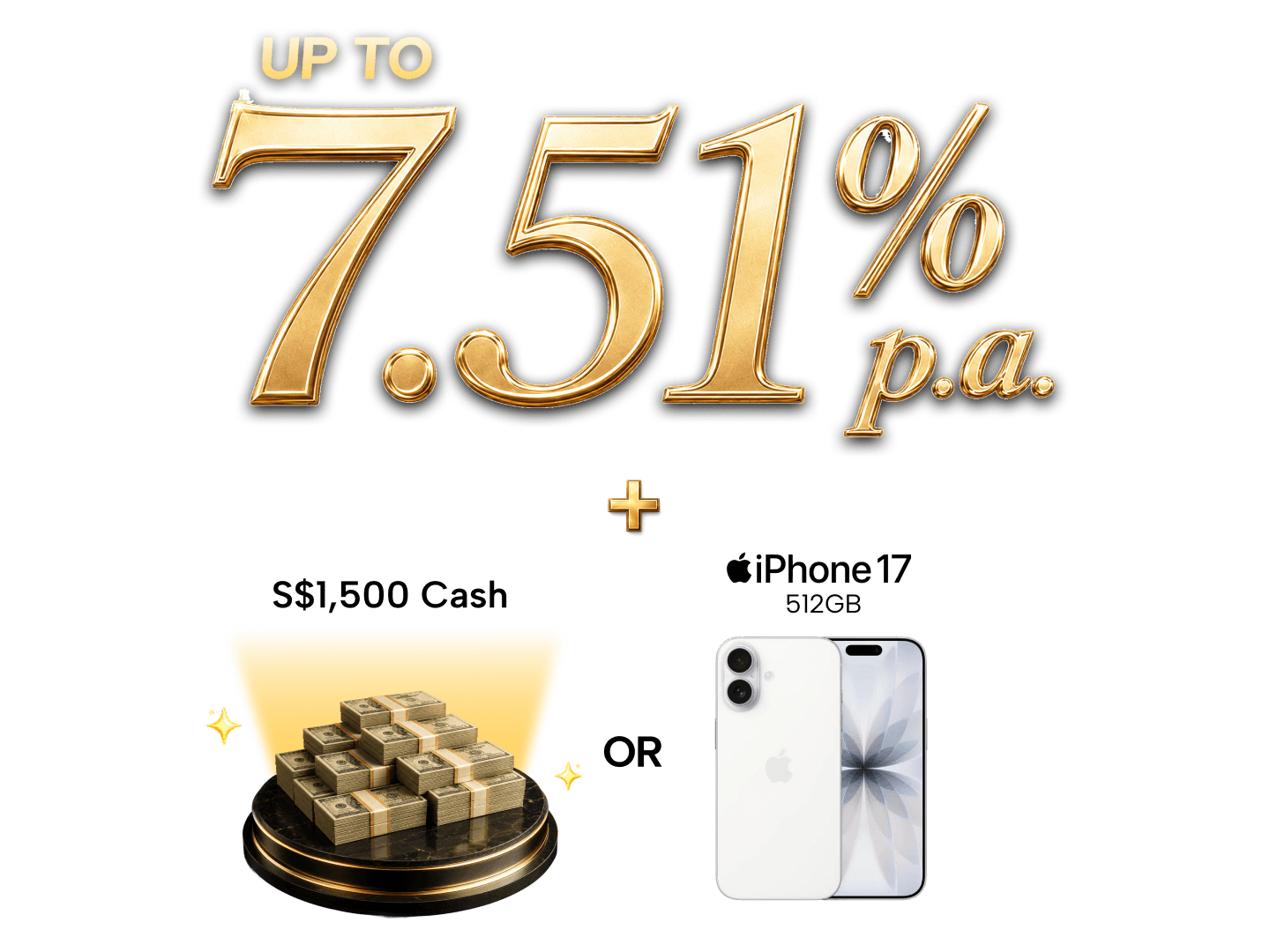

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

Frequently asked questions about high-yield savings accounts in Singapore

Many high-yield savings accounts cap the maximum balance that earns bonus interest — often between S$50,000 and S$100,000. Any amount beyond that usually earns a much lower base rate, so it may be worth spreading excess funds across multiple accounts.

As of July 2025, Standard Chartered’s Bonus$aver offers one of the highest potential rates at up to 7.88% p.a., but requires significant monthly card spend and bill payments. For more accessible rates, OCBC 360 and DBS Multiplier are strong contenders.

An application for a high-yield savings account may be declined due to incomplete documentation, poor credit history, or failure to meet eligibility criteria, as banks conduct thorough checks for compliance and risk assessment. If rejected, contact the bank to understand the specific reasons and address them, such as correcting errors or improving your financial standing. In the interim, consider other savings options.

High-yield savings accounts in Singapore are generally very safe. Most are held with MAS-regulated financial institutions and are protected under the SDIC scheme, which insures deposits of up to S$75,000 per bank per person.

Unlike stocks or unit trusts, your principal is not at risk from market volatility. However, the interest rate can be revised by the bank at any time, especially if market conditions change.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.