A Full Guide To Priority Banking In Singapore (2026)

Updated: 16 Apr 2026

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Saver takeaways

-

A step above ordinary bank accounts and a step below private banking accounts reserved for Ultra High Net Worth Individuals (UHNWI), Priority Banking grants you access to a slew of VIP privileges as well as favourable interest rates on savings and deposits.

-

You’ll need anywhere between $200,000-350,000 to qualify for Priority Banking.

-

Thanks to dedicated branches and priority queues, Priority Banking customers can conduct their financial transactions in greater privacy, efficiency and comfort.

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

What is Priority Banking?

Priority Banking is a specialized tier for "High Net Worth" or "Affluent" individuals. By maintaining a certain Total Relationship Balance (TRB)—which includes cash, investments, and insurance—you gain access to a dedicated Relationship Manager (RM), better interest rates, and premium lifestyle benefits.

In 2026, many banks have integrated Accredited Investor (AI) opt-ins as a core part of their Priority experience to unlock higher-tier rewards and more complex investment products (like private equity or structured notes).

Priority Banking vs. Private Banking: What’s the difference?

The main difference is the "barrier to entry" and the level of customization:

-

Priority Banking (S$200k – S$1.5M): Focuses on "Mass Affluent" wealth management, preferential rates, and standard lifestyle perks (e.g., airport lounges).

-

Private Banking (>US$5M): Offers bespoke wealth structuring, succession planning, and access to institutional-grade investments. In 2026, the gap has widened as DBS and other majors shifted to USD-denominated benchmarks for Private Banking.

What are the benefits of Priority Banking?

1. Preferential Interest Rates

While the 4% fixed deposit rates of 2023 are long gone, Priority customers in April 2026 still enjoy a premium over the retail market.

-

Fixed Deposits: 1.35% to 1.60% p.a. (compared to retail ~1.10%).

-

Mortgages: Preferential SORA spreads (e.g., 3M SORA + 0.65%).

2. Dedicated Relationship Manager

You bypass the general branch queues and call centers. Your RM provides quarterly portfolio reviews and personalized market insights from the bank’s Chief Investment Office (CIO).

3. Lifestyle Perks & Travel

-

Airport Lounges: Access to Plaza Premium or Priority Pass lounges

-

Limo Transfers: Complimentary airport transfers (usually requires a minimum monthly spend or specific AUM).

-

Priority Queues: Dedicated "blue-carpet" or "gold-tier" counters at physical branches.

How do you decide which Priority Banking programme is best for you?

It can be difficult to decide which Priority Banking programme to sign up for. After all, there are numerous local and international banks doing business here in the Lion City. To help narrow your search, you first need to determine what the qualifying amount is.

As mentioned earlier, not every Priority Banking programme has the same minimum AUM or TRB.

Secondly, decide whether the Priority Banking programme’s financial and lifestyle benefits meet your needs. For example, complimentary golf games and airport lounge access aren’t very attractive if you’re not a fan of the sport or overseas vacations.

Neither is it worth your time and assets if the financial services and products offered don’t help in achieving your goals.

The following Priority Banking programmes listed are just several from the top banks operating in Singapore.

They might appear similar on the surface, but you’ll quickly notice how they differentiate themselves from each other.

Compare Priority Banking accounts

Product Name | Hot Reward Pick | SingSaver Reward | Min. Deposit | Min. Annual Interest Rate | Max. Annual Interest Rate | ||

|---|---|---|---|---|---|---|---|

| Citigold | S$1,599 | S$350,000 | 0.01 % | 7.51 % | ||

| DBS Treasures | - | - | - | - | 0.05 % | |

| UOB Privilege Banking | - | - | - | - | 0.05 % | |

| Standard Chartered Priority Banking | - | - | - | - | 7.05 % |

CIMB Preferred

CIMB Preferred requires a TRB of S$250,000 to qualify. Like most of the other programmes listed here, there’s no need for Accredited Investor status to enter.

The qualifying requirements might be steep, but CIMB ensures that membership perks are worth the price of entry. Not only are you assigned a Relationship Manager, but there’s also a dedicated CIMB Preferred Call Centre. While physical presence remains limited (the main office at Raffles Place is the primary hub), CIMB’s digital integration is highly rated in 2026.

Lifestyle benefits include complimentary airport lounge access, exclusive event invitations, and regional medical benefits across ASEAN.

-

Interest Rate: You can enjoy up to 1.98% p.a. on your incremental balance when you top up fresh funds to your CIMB StarSaver Account (valid through April 30, 2026).

-

Welcome Gift: New-to-bank customers can receive S$800 eCapitaVouchers with S$250,000 funding.

Citigold

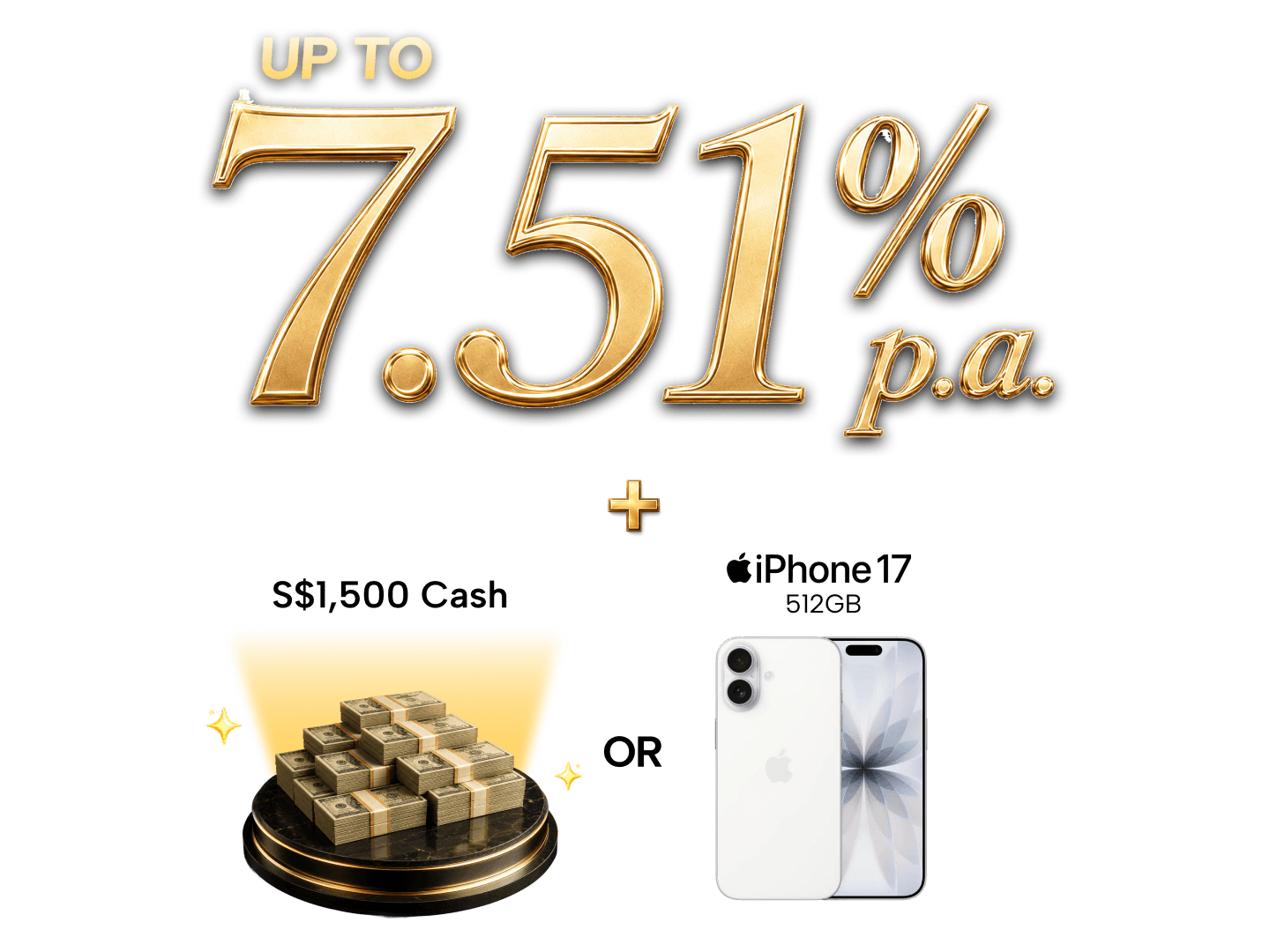

A wealth-focused priority banking programme, Citigold offers a comprehensive suite of financial advisory services. Applicants are required to make a minimum deposit and/or investment of S$350,000 (updated from S$250,000 in previous years) to unlock the full suite of rewards.

Apart from preferential interest rates, you'll have access to a dedicated Relationship Manager and a team of experts including mortgage specialists. The Citigold privileges are extended worldwide, making it the top choice for frequent travelers.

-

Interest Rate: Grow your savings with up to 7.51% p.a. interest when you open a Citi Wealth First account (achieved through salary credit, spending, investing, and insuring).

-

Welcome Deal (April 2026): Get an Apple iPhone 17 (256GB or 512GB) or up to S$1,500 cash via PayNow when you apply, become an Accredited Investor, and maintain S$350,000 in fresh funds.

What is an Accredited Investor?

An Accredited Investor (AI) is someone who meets the requirements set out by the Monetary Authority of Singapore (MAS) and has opted in to be treated as an AI by the bank. In 2026, many banks make this a prerequisite for high-tier welcome gifts.

Advantages of an Accredited Investor

-

Expand investment opportunities: Access to private equity, hedge funds, and structured notes not available to retail clients.

-

Higher Rewards: Priority banks in 2026 heavily weight their "Flash Deals" toward those who opt-in as AIs.

Eligibility for Accredited Investor (2026)

-

Net personal assets: Exceeding S$2 million (residence value capped at S$1M); or

-

Financial assets: (Net of liabilities) exceeding S$1 million; or

-

Annual Income: Not less than S$300,000.

-

Note: As of 2026, your Digital Payment Token (crypto) holdings can contribute up to S$200,000 toward the AI asset requirement after a 50% haircut.

-

What is an Accredited Investor?

-

An Accredited Investor is someone who meets the requirements set out by the Monetary Authority of Singapore (MAS) and has opted in to be treated as an Accredited Investor by the bank. Accredited Investors generally have access to a wider range of investment products than non-Accredited Investors, and at the same time require less regulatory protection.

-

-

How to be an Accredited Investor

-

Start your wealth journey with Citigold and speak to your relationship manager.

-

-

Advantages of an Accredited Investor

-

Expand investment opportunities

-

Enjoy access to a wider range of financial products and services, including more sophisticated products to meet your bespoke wealth needs.

-

-

Access to a team of dedicated wealth experts

-

You can count on a dedicated Senior Relationship Manager and a team of experts to help you grow your portfolio and partner you to achieve your wealth goals.

-

-

Eligibility for Accredited Investor

-

Net personal assets exceeding S$2 million in value (or its equivalent in a foreign currency); or

-

Financial assets (net of any related liabilities) exceeding S$1 million in value (or its equivalent in a foreign currency); or

-

An income in the preceding 12 months of not less than S$300,000 (or its equivalent in a foreign currency)

-

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

DBS Treasures

DBS Treasures remains the most rigorous local programme. While the base AUM is S$350,000 in investable assets, many premium wealth products now require you to be an Accredited Investor.

Perks include access to four DBS Treasures centres across Singapore and better service at all DBS/POSB branches. You gain access to the DBS Lifestyle Privileges Programme, which includes curated travel and medical concierge services. For those with AUM exceeding US$5 million, the transition to DBS Private Bank offers even deeper institutional access.

HSBC Premier

HSBC Premier remains highly flexible with three entry options:

-

TRB: S$200,000 in fresh funds.

-

Salary: Credit a monthly salary of S$15,000.

-

Property Loan: A loan of at least S$800,000 in Singapore.

The standout feature is the Family Premier benefit, which extends your status and perks to your spouse and up to three children (ages 12–30) at no extra cost.

-

Interest Rate: As of April 2026, Premier Elite customers enjoy a 1.30% p.a. 3-month SGD Time Deposit rate.

Maybank Premier

With a requirement of S$300,000 in deposits or investments to unlock the best perks, Maybank Premier is a solid choice for those seeking personalized attention without the "Accredited Investor" mandate.

You can earn up to 1.55% p.a. (inclusive of bonus rates) on your Prestige Savings Account for balances above S$200,000. Lifestyle privileges include golfing deals and access to six Premier Wealth Centres in Singapore.

You'll enjoy an array of lifestyle privileges from dining, golfing, and travel, invitations to exclusive events, and priority services for your transactions. You'll be privy to preferential rates and faster processing for credit facilities.

Across the Singapore network of 18 Maybank branches, there are six Premier Wealth Centres that cater exclusively to Premier customers.

Overall, Maybank Premier's holistic perks from the Maybank Premier World Mastercard Card and the programme make it a worthy investment.

OCBC Premier Banking

OCBC Premier Banking requires a fresh funds deposit or investment of S$350,000 (aligned with local competitors in 2026). Accredited Investor status is not required for entry.

Members receive the OCBC Premier Visa Infinite Credit Card, which offers high miles-earning potential and lounge access. The OCBC 360 Account remains a core benefit, offering up to 4.45% p.a. on the first S$100,000 for those who fulfill multiple categories (Salary, Save, Spend, Insure, Invest).

Ranked by our financial experts

Review the best priority banking accounts with all the stats at your fingertips.

UOB Wealth Banking

UOB Wealth Banking is the entry-tier "Priority" experience, requiring an AUM of S$100,000. This makes it the most accessible programme for young professionals.

While it doesn't require AI status, it offers a dedicated Relationship Manager and priority queues. For those reaching S$350,000, you graduate to UOB Privilege Banking, which unlocks luxury concierge services and the UOB Privilege Card.

Standard Chartered Priority Banking

Standard Chartered requires S$200,000 in AUM or a S$1.5 million housing loan. No AI status is needed for basic entry, but it is required for the "Accredited Investor" cash bonus.

-

The Perks: Business travelers benefit from the APEC Business Travel Card fee reimbursement. You also earn 360° Rewards Points across your entire banking relationship, not just credit card spend.

-

Interest Rate: The Wealth $aver Account offers up to 2.80% p.a. on balances up to S$1.5 million, making it one of the most competitive accounts for high-cash-holding individuals in 2026.

-

Welcome Gift: Funding S$200,000 can net you up to **S$1,050 cash** (with AI opt-in), while funding S$1.5M can reach **S$9,000+** in rewards.

Frequently asked questions about Priority Banking

A minimum of $200,000 in deposits or investments with Standard Chartered Bank is required to qualify for Priority Banking with the bank. An alternative way to qualify is to maintain a minimum of $1.5M in housing loans with Standard Chartered Bank.

While accounts like Citigold and Standard Chartered Priority Banking may present a lower barrier to entry in terms of the funds needed, your lifestyle matters too. Are you a frequent flyer? If so, being able to transact in 150 currencies with Citigold Debit Mastercard® might be perfect for you, since you’ll incur zero currency conversion or foreign transaction fees. Or you might appreciate earning OCBC$ with everyday spend and being able to easily exchange your points for KrisFlyer miles. In terms of regional presence, customers who spend a lot of time in Indonesia or Malaysia may want to consider the Maybank Premier Wealth programme.

Total Relationship Balance (TRB) and Assets Under Management (AUM) are used interchangeably by banks to refer to the total sum of assets an individual has parked in their bank. This can be a combination of cash, insurance and investment products.

Is it time to sign up for priority banking?

VIP privileges, access to better interest rates and free coffee? What’s not to love?

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.