Priority Banking vs. Private Banking: How to Qualify?

Updated: 21 Jul 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Once you have a 6-7 figure sum you need to stash in the bank, you'll be well on your way to becoming either a Priority or Private Banking client. Read on to find out which one suits your needs better.

Priority Banking and Private Banking are like twins; while they may look similar, they are completely separate and different individuals. In this article, we'll go over the differences between the two, the perks they offer and which banking service is best equipped to meet your needs.

The best Priority Banking options in Singapore

Citigold

SingSaver’s take

Citigold's minimum AUM requirement is among the lowest out there, which makes it significantly easier to qualify for Citigold. If you are a frequent traveller with S$250,000 to spare, you'll love Citigold's travel benefits and Global Wallet. Plus, you'll have access to all the expert advice you need to grow your wealth.

Pros

Aside from the slew of VIP privileges you'll get with a Citigold account, Citi also gives you many ways to earn bonus interest—up to a maximum of 7.51%.

Cons

While qualifying transactions and saving some extra cash each month are easy enough, the other criteria can be more challenging to meet. This means that it's reasonable to expect that interest rates of 7.51% is the exception, rather than the norm for most months.

HSBC Premier Bank Account

SingSaver’s take

HSBC Premier rewards its clients with family-centric benefits, such as legacy planning, healthcare protection for the whole family and international education for children under 18. HSBC Premier is also a multi-currency account, making it a great choice for well-heeled, global families.

Pros

S$200,000 is as low as you can get when it comes to qualifying AUMs for Priority Banking accounts. It's hard to beat HSBC Premier when it comes to family-centric benefits, since you can gift your Premier status to your spouse and children for free.

Cons

Singapore dollar deposits are covered by the Singapore Deposit Insurance Corporation (SDIC) for up to S$100,000, to protect against the unlikely scenario of a bank failure. This will not be enough to cover all of your funds, if you're a HSBC Premier client.

Standard Chartered Priority Banking

SingSaver’s take

Standard Chartered Priority Banking's AUM of S$200,000 is one of the easiest to reach. In return for parking your money with the bank, you get a good blend of investments, wealth management solutions and VIP lifestyle benefits.

Pros

Fast-track APEC clearance at airports and complimentary lounge access are 2 big perks for anybody who has to fly frequently for work. It also helps that you can bring your Priority perks with you to over 25 markets worldwide.

Cons

Unlike with HSBC Premier, you cannot transfer your Priority benefits to your spouse or children.

This is your sign to consider Priority Banking

5 signs to determine if you're ready to make the leap from Personal to Priority Banking.

CIMB Preferred

SingSaver’s take

Perhaps the Priority Banking account of choice for those who shuttle frequently between Malaysia and Singapore, CIMB Preferred also has a strong presence in ASEAN. It's an excellent choice for those with families with ties to neighbouring countries in the region.

Pros

The CIMB Preferred Account's borderless banking features and robust regional presence will benefit those who spend significant chunks of their time in Malaysia and around the region.

Cons

Those with ties outside the region, or who often travel to cities outside of ASEAN will not be able to benefit as much.

What is Priority Banking?

Priority Banking sits one tier above Personal Banking, which is what you and I probably use. Priority Banking, however, is for the mass affluent. According to The Straits Times, the Mass Affluent are defined as those with investible assets between US$500,000 to under US$5 million.

To qualify for Priority Banking, banks require customers to have Assets Under Management (AUM) between S$200,000 to S$350,000. The exact figure varies from bank to bank.

AUM doesn't just refer to cold, hard cash. Some banks, like Standard Chartered Bank, let customers sign up for Priority Banking if they have at least S$1.5 million in housing loans with them. Other products offered by the bank, such as investment and insurance products, also contribute to one's total AUM.

Once you're a Priority Bank client, you’ll enjoy VIP privileges reserved for people like you. This includes exclusive lifestyle perks, preferential rates for loans and credit cards, priority queuing at the bank, and your own Relationship Manager.

Note that Priority Banking perks may differ greatly from bank to bank, with some of them offering more value for money than others.

>> FIND OUT: Standard Chartered vs. UOB Priority Banking: Who's Better?

The best Private Banking options in Singapore

Citigold Private Client

SingSaver’s take

From fee-free cash withdrawals from any Citi ATM in the world, to complimentary airport limousine transfers, Citigold Private Client has developed an impressive assortment of ways to make life as smooth-sailing as possible for their esteemed customers.

Pros

Thanks to Citibank's strong global presence, Citigold Private Client members can delight in their exclusive privileges anywhere they are in the world. Features like Citibank Global Wallet, Citibank Global Transfer and Global ATM Access make traveling for work and pleasure a breeze.

Cons

Citigold Private Client's AUM requirement of S$1.5 million and above is not something that most people can meet. But then, that's what exclusivity is for, isn't it?

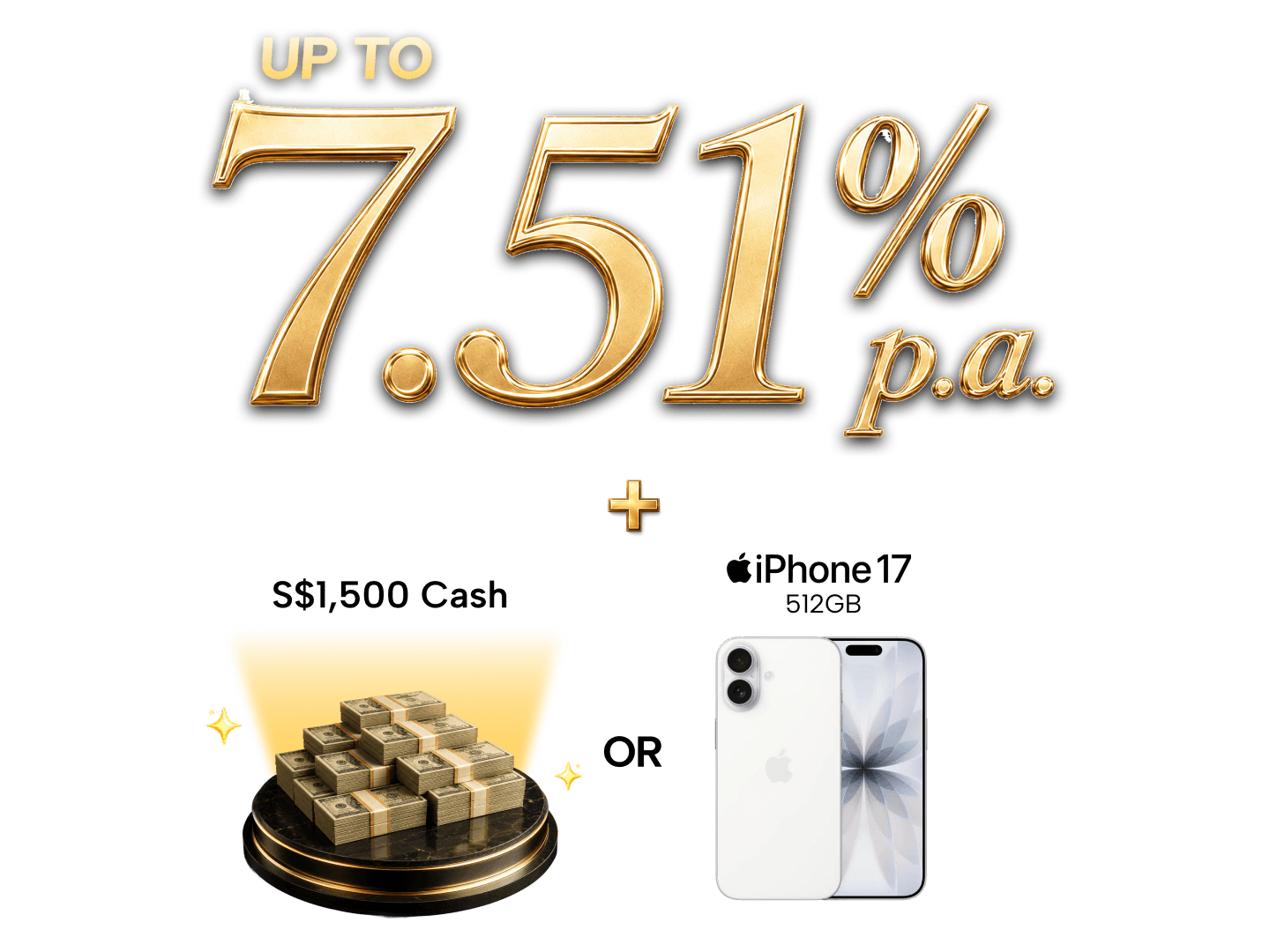

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

DBS Treasures Private Client

SingSaver’s take

DBS Treasures Private Client is only 1 out of 2 Private Banking solutions DBS offers, with the other being DBS Private Bank. While the former requires an AUM of S$1.5 million, the latter requires at least S$5 million. It's no surprise that there is little information out there on both groups, since exclusivity is the name of the game.

Pros

Turn a dreary work trip into a relaxing, even pleasant one with DBS Treasures Private Client's slew of travel privileges. Managed to score the uber exclusive DBS Insignia Visa Infinite Card? You'll earn 2 miles per dollar on overseas spend and 1.6 miles per dollar on local spend.

Cons

DBS Treasures Private Client's aura of exclusivity may be appealing to some, but to others, the lack of available information could prove to be annoying. Details like base and maximum annual interest rates will only be known to members of this prestigious club.

OCBC Premier Private Client

SingSaver’s take

OCBC Premier Private Client's eligibility criteria seems straightforward at first glance, but you also need to qualify as an Accredited Investor on top of having an AUM of S$1.5 million. That means you'll need to satisfy one additional criterion; net personal assets exceeding S$2 million, an income of at least S$300,000 in the last 12 months, or financial assets that exceed S$1 million.

Pros

Savvy investors who bounce around Asian countries like Indonesia, Malaysia and Hong Kong will love the exclusive perks OCBC has to offer. They will also benefit from being able to exchange miles earned on their credit card for flights on any airline.

Cons

The additional requirement of Accredited Investor qualification makes it significantly harder to meet the eligibility requirements for the OCBC Premier Private Client account.

Standard Chartered Priority Private Banking

SingSaver’s take

A step up from Standard Chartered Bank's Priority Banking status, Priority Private Banking offers investment solutions, legacy planning and more global experiences in comparison. A good upgrade for those who lead truly global lifestyles and who require more than just international banking privileges.

Pros

One of the biggest advantages of the Priority Private Banking account is the ability to link to Standard Chartered's other products, for added perks. Signing up for the Bonus$aver account, for example, will net you an interest rate of up to 6.05% on your account balance.

Cons

Lack of ability to transfer privileges to family members or spouses.

Priority Banking vs Private Banking: Which one should you choose?

If you would like lifestyle and financial benefits in exchange for parking a decent chunk of investible assets at a bank of your choice, Priority Banking and Private Banking are both great options.

Private Banking sometimes provides a broader range of wealth management services that aren’t available to Priority Banking members, as well as expanded global services. For example, Standard Chartered only grants legacy planning and international wealth solutions to its Priority Private Banking members.

Finally, AUM requirements are also significantly lower for Priority Banking members. If you’re in a position to consider both options, do ensure that the additional value offered by Private Banking services is aligned with your needs and goals.

HSBC Premier vs. Citigold: Which should you pick?

Discover the similarities and differences between these 2 Priority Banking accounts.

Frequently asked questions about Priority Banking and Private Banking

Banks use various terms to differentiate their products from their competitors. When it comes to Priority Banking, you’ll hear terms like “Premier”, “Preferred” and “Privilege” being thrown around. But these are just names tagged onto different Priority Banking products. Don’t confuse Priority Banking with Private Banking, however, as these two types of products are on a completely different level. While one is suited for the mass affluent, the other is tailored to ultra-high-net-worth individuals (UHNWI). In Singapore, Priority Banking tends to have an AUM requirement ranging from S$200,000 and up, whereas the AUM requirement for Private Banking typically starts at S$1.5 million.

UOB’s Priority Banking’s eligibility requirements are among the most challenging to meet. You’ll need a minimum of S$350,000 (or its equivalent in a foreign currency) in qualifying Assets Under Management (AUM). That’s S$150,000 above Standard Chartered Priority Banking’s AUM requirement of S$200,000!

To qualify for Standard Chartered Bank’s Priority Banking services, you’ll need to maintain a minimum of S$200,000 in deposits and/or investments. Alternatively, you’ll need to have a minimum of S$1.5 million in housing loans with Standard Chartered Bank. Standard Chartered Bank members who want to upgrade to Priority Private Banking will have to make sure they have an AUM of at least S$1.5 million.

While Priority Banking caters to those with 6 figures in their bank account, Private Banking is for those with 7 figures and above in their bank account. That means that instead of an AUM requirement of up to S$350,000, you'll need an AUM of at least S$1.5 million. For example, DBS Treasures Private Client and Citigold Private Client accounts have a minimum qualifying AUM of S$1.5 million, whereas you'll need an AUM of S$5 million to sign up for DBS Private Banking!

When it comes to Private Banking at DBS bank, there are 2 tiers you can choose from. Clients with investible assets of S$1.5 million and above will be eligible for DBS Treasures Private Client. Meanwhile, clients with an AUM of at least S$5 million can opt for DBS's top tier Private Bank account instead.

Latest reads on premium bank accounts

Learn how Priority Banking can help you accumulate more wealth

From preferential rates that give you higher interest rates, to investment opportunities for Accredited Investors, discover how Priority Banking can benefit your bank account balance.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.