What is a Home Equity Loan? A Beginner's Guide

Updated: 9 Dec 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Home equity loans explained

Think of your home equity loan as a way to access the financial value you've already invested in your property. It's essentially a loan secured by the difference between what your home is currently worth and the outstanding balance on your existing mortgage. This means that if your home's value has increased, or if you've been paying down your mortgage, you've been building equity.

This type of loan can be useful for homeowners who need a substantial amount of money for significant expenses. Because it's secured by your property, lenders often offer more favourable interest rates compared to unsecured loans. However, it's important to understand that your home serves as collateral, so responsible repayment is crucial.

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Personal Loan Rates: Compare Top Lenders in Singapore

Loan | Monthly Repayment | SingSaver Reward | Annual Interest Rate | Total Cost of Loan | EIR | ||

|---|---|---|---|---|---|---|---|

| UOB Personal Loan | S$429 | S$430 | From 1.00 % p.a. | S$450 | From 1.93 % p.a. | |

| Trust Bank Instant Loan | S$429 | S$10,420 | From 1.00 % p.a. | S$450 | From 2.28 % p.a. | |

| DBS Personal Loan | S$435 | S$750 | From 1.48 % p.a. | S$666 | From 3.22 % p.a. | |

| GXS FlexiLoan | S$430 | - | From 1.08 % p.a. | S$486 | From 2.02 % p.a. | |

| Standard Chartered CashOne Personal Loan | S$428 | S$410 | From 0.90 % p.a. | S$405 | From 1.75 % p.a. | |

| MariBank Instant Loan | S$433 | - | From 1.28 % | S$576 | From 2.46 % p.a. | |

| EZ Loan | S$540 | - | 9.88 % | S$4,446 | 9.88 % p.a. | |

| Cash Direct | S$542 | - | 10.00 % | S$4,500 | 10.00 % p.a. |

Home equity loan providers in Singapore

| UOB |

|

| DBS |

|

| HSBC |

|

| Bank of China |

|

| Maybank |

|

Key takeaways

Here's a quick overview of what you need to know about home equity loans:

-

Benefits: Access to a lump sum of cash, typically at decent interest rates.

-

Drawbacks: Your home is used as collateral, and you're committed to a fixed repayment schedule.

-

Requirements: Lenders typically require a minimum amount of equity, proof of income, a good credit score, and sufficient home value.

>> MORE: See other personal loan types

Today’s home equity loan rates

When considering a home equity loan in Singapore, understanding the prevailing interest rates is crucial. As of March 2025, homeowners with private properties can generally expect fixed home equity loan interest rates to hover around 2.4% for a 30-year term. For those opting for floating rates, the lowest available is approximately 3%, though this typically requires a minimum loan amount of $500,000. These rates are comparable to those offered for refinancing or new home loans, reflecting the secured nature of home equity loans.

Several factors influence the interest rate you'll be offered:

-

Your credit score: A higher credit score generally qualifies you for better interest rates.

-

Loan amount: The amount you wish to borrow can influence the interest rate offered.

-

Loan-to-Value ratio (LTV): This is the ratio of your total loan amount (including your existing mortgage) to your home's value. A lower LTV typically results in better rates.

-

Market interest rates: Overall economic conditions and prevailing interest rates play a role in determining home equity loan rates.

Getting the best home equity loan rate

Here are some tips to help you secure the most favourable home equity loan rate:

-

Shop around: Compare rates from multiple lenders, including banks and credit unions.

-

Improve your credit score: Before applying, take steps to improve your credit score, such as paying down debt and correcting any errors on your credit report.

-

Lower Your LTV: If possible, pay down your existing mortgage to increase your equity and lower your LTV.

-

Negotiate: Don't hesitate to negotiate with lenders to see if they can offer a better rate.

>> MORE: How to improve your credit score

⚡SingSaver x UOB Personal Loan Flash Deal⚡

Get one of the lowest interest rates from 1.00% p.a. (EIR from 1.93% p.a.) plus up to S$1,900 in cashback and rewards when you apply for a UOB Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

How does a home equity loan work?

A home equity loan essentially transforms the equity you've built in your home into a readily accessible source of funds. Unlike a line of credit that allows you to draw funds as needed, a home equity loan provides you with a single, substantial lump sum at the outset. This immediate access to capital makes it particularly suitable for financing large, one-time expenses, such as major home renovations, significant medical bills, or consolidating existing high-interest debts.

The loan is secured by your home, meaning your property serves as collateral. This security allows lenders to offer fixed interest rates, which remain constant throughout the loan's term. This predictability in interest rates translates to consistent monthly payments, simplifying your budgeting and financial planning. Knowing exactly how much you'll be paying each month provides a sense of stability and allows you to manage your finances with greater confidence.

How do I access a home equity loan?

Accessing a home equity loan involves a series of steps, beginning with the initial application and culminating in the disbursement of funds.

To start, you'll need to approach a financial institution that offers home equity loans, such as a bank or credit union. Lenders will then assess your eligibility based on factors like your credit score, income, and the amount of equity you have in your home.

Once approved, the full loan amount is typically disbursed as a lump sum, providing you with immediate access to the capital. This lump-sum disbursement is what distinguishes a home equity loan from a home equity line of credit (HELOC), which allows you to draw funds as needed (like a low-interest credit card), and is what makes home equity loans suitable for financing large, one-time expenses (such as a second mortgage).

How much does a home equity loan cost?

When considering a home equity loan, it's essential to factor in the various costs associated with obtaining and maintaining the loan. In addition to the interest payments, which are a primary cost, you should also be aware of the following:

-

Closing costs: These are fees charged by the lender to process the loan and can include valuation fees to appraise your property, legal fees for documentation, and other administrative charges. These costs can vary, so it's important to ask your lender for a detailed breakdown.

-

Prepayment penalties: Some lenders may impose a penalty if you decide to pay off your loan before the agreed-upon term. This is to compensate the lender for the interest they would have earned. Always clarify with your lender whether any prepayment penalties apply and under what circumstances.

Home equity loan requirements

Lender requirements vary from lender to lender and case to case, but the below are common requirements among most lenders in Singapore:

-

Minimum equity in the home: Lenders typically require a significant equity stake, often ranging from 15% to 20% of the home's appraised value. This requirement protects the lender's investment and ensures that borrowers have a vested interest in maintaining their property. In Singapore, where property values can fluctuate, lenders are particularly cautious about this requirement.

-

Proof of income and employment: Lenders meticulously verify income stability and employment history to assess a borrower's ability to repay the loan. This often involves providing documentation such as income tax statements, payslips, and employment verification letters. In Singapore, where many individuals have diverse income streams, lenders may require detailed financial documentation.

-

Sufficient home value: The appraised value of the home must be sufficient to support the requested loan amount. Lenders conduct thorough appraisals to determine the property's current market value, ensuring that it aligns with their lending criteria. This is particularly important in Singapore's dynamic property market.

How to get a home equity loan

Here's a step-by-step guide to applying for a home equity loan:

-

Calculate your home equity: Determine the current market value of your home and subtract the outstanding balance on your mortgage.

-

Assess your needs: Decide how much you need to borrow and what you intend to use the funds for.

-

Gather documentation: Collect necessary documents, such as proof of income, employment verification, and property details.

-

Shop around: Compare loan offers from multiple lenders, including banks and financial institutions.

-

Apply for the loan: Submit your loan application to the chosen lender.

-

Undergo appraisal: The lender may order an appraisal to verify the value of your home.

-

Review loan terms: Carefully review the loan terms, including interest rates, fees, and repayment schedule.

-

Close the loan: If approved, sign the loan documents and receive the funds.

SingSaver x HSBC Personal Loan Exclusive Offer

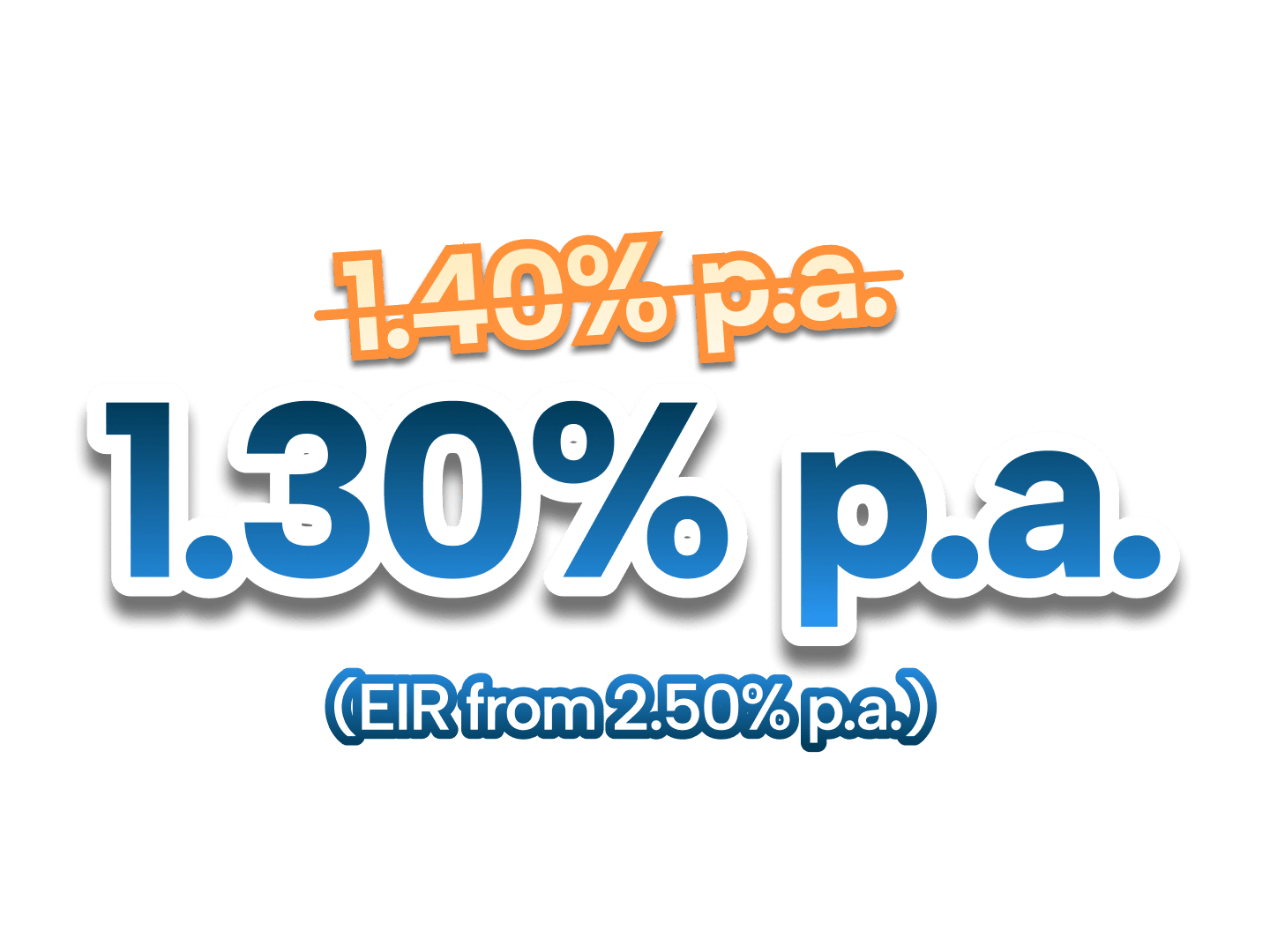

Enjoy attractive interest rates from 1.30% p.a. (EIR from 2.50% p.a.) when you apply for HSBC Personal Loan via SingSaver. Available to new and existing customers! Valid till 2 August 2026. T&Cs apply.

SingSaver Tips

How much can you borrow with a home equity loan?

The amount you can borrow with a home equity loan depends on your borrowing capacity, which is often determined by the LTV ratio. The LTV ratio compares the total amount of your loans (including your existing mortgage and the home equity loan) to the appraised value of your home. Lenders typically have a maximum LTV ratio that they allow.

For example, if your home is valued at $1,000,000 and you have an outstanding mortgage of $400,000, and the lender allows an LTV of 80%, you can calculate the maximum loan amount as follows:

80% of $1,000,000 = $800,000

$800,000 - $400,000 = $400,000

In this scenario, you could potentially borrow up to $400,000 with a home equity loan.

Is getting a home equity loan a good idea?

Deciding whether a home equity loan is the right financial move requires a thorough assessment of your specific circumstances. It's not a one-size-fits-all solution, and its suitability hinges on your financial stability, long-term goals, and risk tolerance. For instance, if you're a homeowner with a stable income and a clear plan for how you'll use the funds, a home equity loan can be a powerful tool. However, if your income is unpredictable or you're prone to impulsive spending, the risks might outweigh the benefits.

SingSaver x DBS/POSB Personal Loan Exclusive Offer

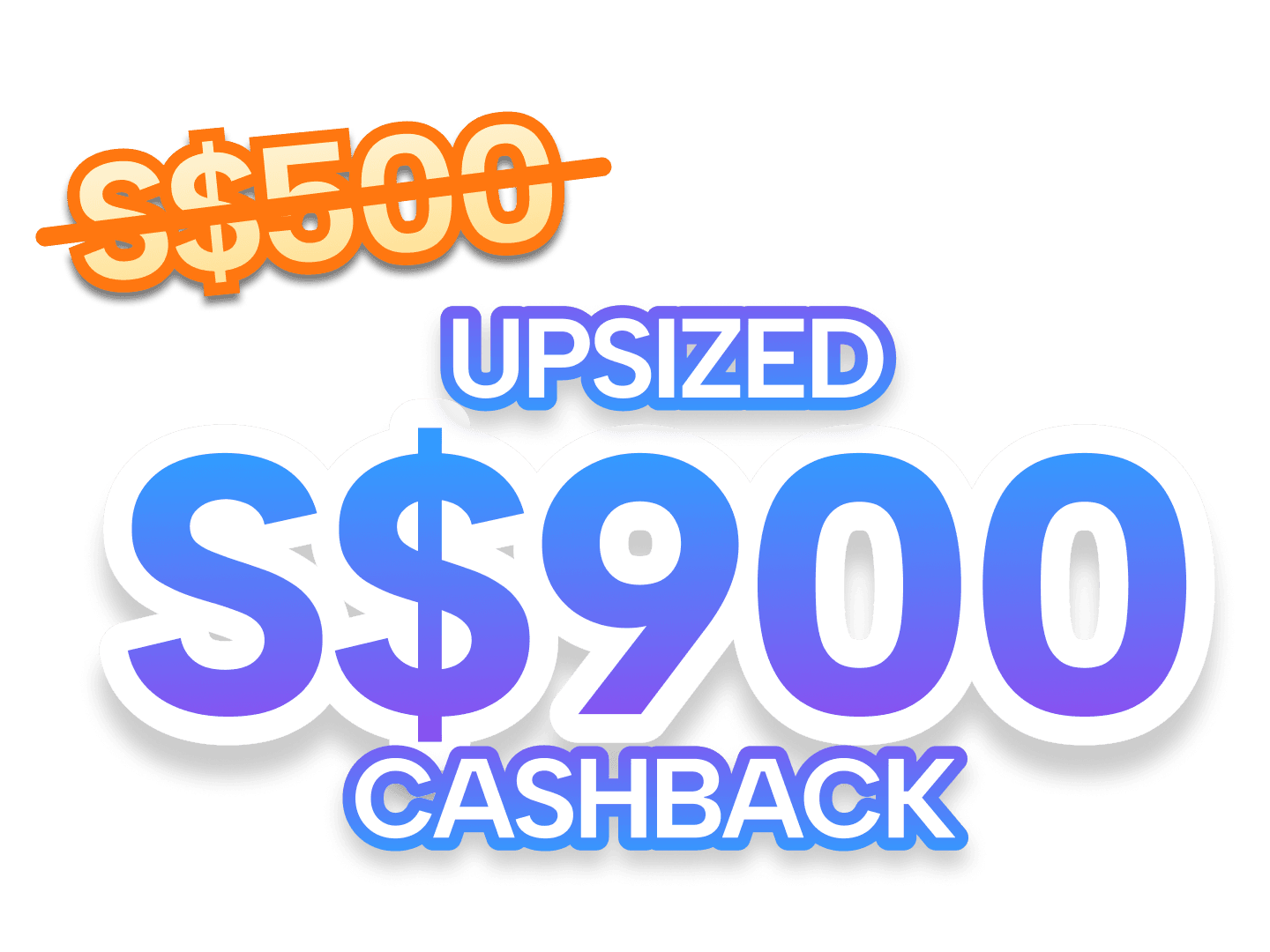

Enjoy interest rates from 1.48% p.a. (EIR from 3.22% p.a*) when you apply for a DBS/POSB Personal Loan. Plus, get S$900 bonus cash on top of up to 3% cashback when you apply for a loan min. S$10,000 with a min. tenure of 3 years. Use the promo code (SINGSAVER) upon application. Valid till 15 July 2026. T&Cs apply.

Pros

Access to a substantial, upfront capital injection

This is particularly advantageous for funding large, planned expenditures, such as major home renovations that could increase your property's value, or consolidating high-interest debts into a single, more manageable loan.

Potential for fixed interest rates, providing predictable monthly payments

Some home equity loans (such as those offered by DBS) offer fixed interest rates, which allow for accurate budgeting and financial planning, reducing the anxiety associated with fluctuating interest rates that are common with other loan types. However, variable rate loans are also available.

Versatile use of funds

Unlike some loans that are earmarked for specific purposes, home equity loans offer flexibility. You can use the funds for a wide range of expenses, from education and medical bills to starting a business.

Cons

Significant risk of losing your home

Since your home serves as collateral, defaulting on the loan could lead to foreclosure. This is a serious consideration, especially in Singapore's competitive property market.

Commitment to a rigid repayment schedule

The fixed repayment terms can be challenging for those with irregular income or those anticipating significant changes in their financial situation.

Additional upfront costs

Closing costs, including valuation and legal fees, can add a substantial sum to the overall cost of the loan, effectively reducing the net amount you receive.

A home equity loan is a significant financial undertaking. It's not just about accessing funds; it's about making a strategic decision that aligns with your long-term financial health. If you're considering a home equity loan, take the time to thoroughly evaluate your financial situation, explore alternative financing options, and seek professional advice. When used wisely, a home equity loan can be a valuable tool for achieving your financial goals.

What to do if you can’t keep up with your home equity loan payments

If you anticipate or experience difficulty making your home equity loan payments, it's crucial to take prompt action. Prioritise your loan payments and explore options for financial assistance. Contact your lender to discuss potential solutions, such as refinancing or adjusting your payment plan. Seeking financial advice from a qualified professional can also provide valuable guidance and support.

Frequently asked questions about home equity loans

A home equity loan is a type of loan that allows homeowners to borrow a lump sum of money against the equity they have built up in their property.

Home equity loans are typically paid back in monthly instalments over a set loan term, with both principal and interest payments.

A home equity loan provides a lump sum of money upfront, using your home as collateral, and you repay it with fixed monthly payments over a set period.

Interest paid on home equity loans in Singapore is generally not tax-deductible.

Responsible repayment can positively affect your score, while missed payments or default can negatively affect it. Your credit utilisation ratio, which is the amount of credit you're using compared to your available credit, can also be affected.

Stay ahead in everything finance

Subscribe to our newsletter and receive insightful articles, exclusive tips, and the latest financial news, delivered straight to your inbox.

Weigh your options

Take a look at all loans available to you before making a decision so you can get what's best suited for your needs.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.