KrisFlyer UOB Savings Account Review (2025): Earn Bonus Miles (Capped at 5%) While You Save and Spend

Updated: 10 Nov 2025

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Unlike other savings accounts, mile chasers can leverage both base and bonus miles with a KrisFlyer UOB savings account. Earn up to 6 bonus KrisFlyer miles on top of a 0.05% p.a. interest rate.

Poised to win over frequent flyers and everyday spenders alike, the KrisFlyer UOB Savings Account lets you earn up to 6 KrisFlyer miles per S$1 spent when you use eligible UOB cards and credit your salary into the account.

It’s a neat way to grow your savings and your miles at the same time — but don’t get carried away just yet. The bonus miles are capped at 5 % of your monthly average balance (MAB), which means your total bonus miles depend on how much you keep in the account. So while the 6-miles-per-dollar earn rate sounds great, your actual mileage will vary based on your savings balance.

How the KrisFlyer UOB Savings Account works

As compared to other savings accounts, the KrisFlyer UOB savings account doesn’t set too many requirements for you to get the most out of your savings and spending.

First things first, you’ll have to deposit a minimum of S$1,000 to open an account.

Once you’ve opened your KrisFlyer UOB Account, you’ll need to maintain a monthly average balance (MAB) of at least S$1,000 to start earning bonus miles. You’ll also earn a base interest rate of 0.05% p.a. on your savings, which is standard for this account.

To start accumulating miles, use your KrisFlyer UOB Debit Card for everyday spending. With at least S$1,000 in your account, you can earn 5 bonus KrisFlyer miles for every dollar spent on eligible UOB cards. If you’d like to unlock the full 6 bonus miles per dollar, credit a monthly salary of at least S$1,600 into your KrisFlyer UOB Account via GIRO using the “SALA” transaction reference.

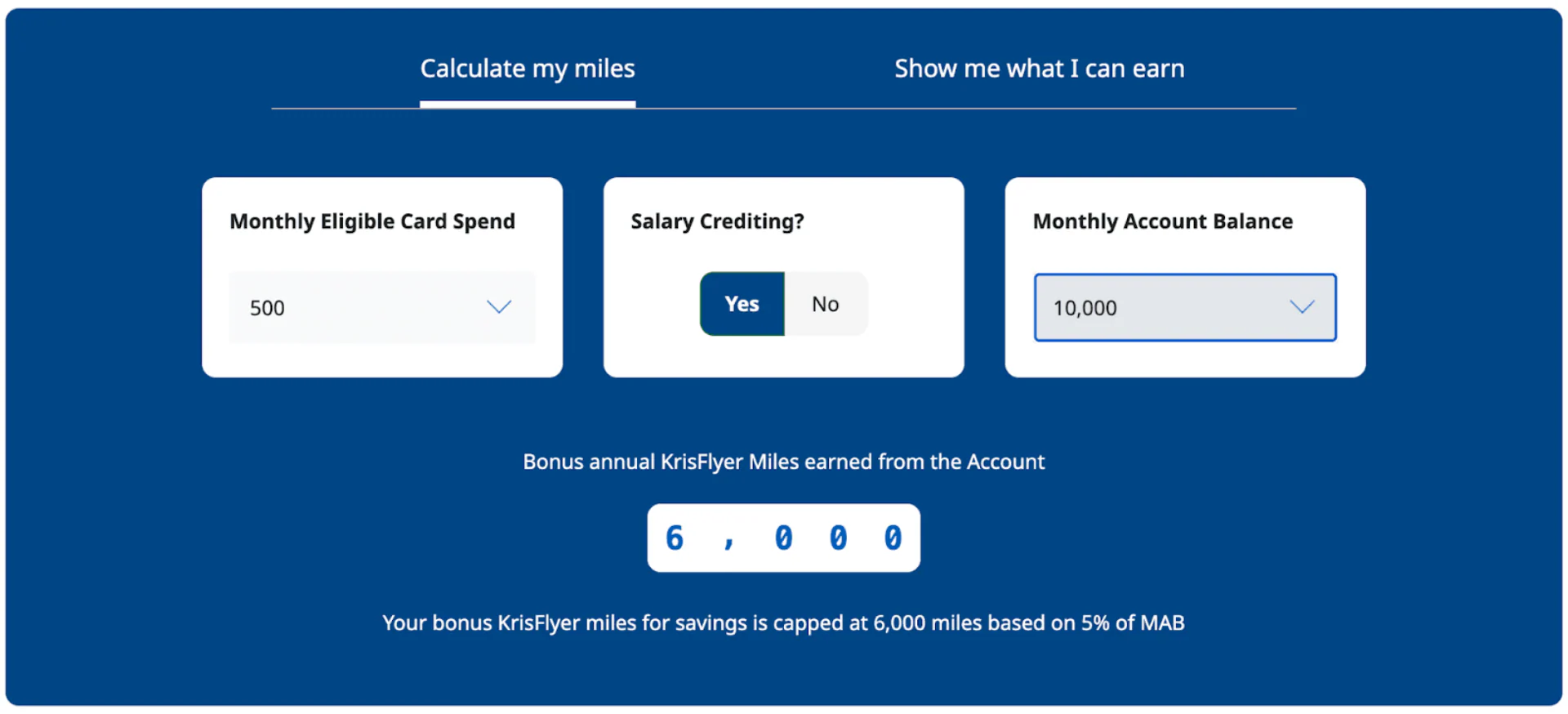

The concept is simple enough: save, spend, and earn miles at a higher rate when your salary is credited. Bonus miles, however, are capped at 5% of your monthly average balance, which means your total miles depend on how much you keep in your account. For instance, if your MAB is S$10,000, your bonus miles that month would be capped at around 500 miles.

Source: UOB

The aforementioned eligible UOB credit cards you can use to earn bonus KrisFlyer miles are:

-

KrisFlyer UOB credit card

-

UOB PRVI Miles card

-

UOB Visa Infinite Metal card

-

UOB Privilege Banking card

-

UOB Reserve card

Pros and cons of the KrisFlyer UOB Savings Account

KrisFlyer UOB savings account product summary:

-

Base interest rate: 0.05% p.a.

-

Maximum interest rate: 0.05% p.a.

-

Minimum average daily balance for auto-waiver of monthly fall-below fee: S$1,000

-

Minimum initial deposit: S$1,000

KrisFlyer UOB Credit Card

- Earn 3 KrisFlyer miles per S$1 spend on Singapore Airlines, Scoot, KrisShop, Kris+ and Pelago purchases.

- Earn 2.4 KrisFlyer miles per S$1 spend on dining, food delivery, online shopping, online travel and transport spend, with min. S$1,000 annual spend on Singapore Airlines, Scoot and KrisShop

- Earn 1.2 KrisFlyer miles per S$1 on all other spend.

- 5,000 Welcome miles with first eligible spend (min. S$5).

- 10,000 KrisFlyer miles with annual renewal fee payment.

- Exclusive privileges on Scoot (via flyscoot.com/krisflyeruob), Kris+ and more.

- Terms and conditions apply for all abovementioned privileges. Visit here for more details.

- Insured up to S$100k by SDIC.

- KrisFlyer miles

- Unlimited miles

- 1st year annual fee waiver

Pros

Start earning KrisFlyer miles easily with just S$1,000 in your account

Earn a bonus of up to 6 KrisFlyer miles per S$1 when you spend on eligible UOB cards

No minimum income requirement

No minimum card spend

Cons

Low interest rate of 0.05% p.a.

Bonus KrisFlyer miles earned is limited to 5% of the account’s monthly average balance (MAB)

Main benefits of the KrisFlyer UOB Savings Account

#1: Offers an easy way to earn miles while you save and spend

We all want to earn miles without having to bend over backwards. The KrisFlyer UOB Account allows you to accumulate miles while fitting seamlessly with your spending and saving habits. Since parking your money in a savings account and shopping are things we already do daily, it makes sense to let those actions earn you a little extra along the way.

#2: Bonus miles are easily achievable

Earning bonus miles with this account is surprisingly straightforward. You only need to maintain a minimum monthly average balance (MAB) of S$1,000 and spend on eligible UOB debit or credit cards to earn 5 miles per dollar. That’s already a generous base rate compared to typical debit card miles earn rates.

If you also credit a salary of at least S$1,600 into your KrisFlyer UOB Account via GIRO (with the “SALA” transaction reference), you’ll unlock the higher earn rate of 6 miles per dollar. It’s a simple, achievable setup — no complex hoops to jump through or high spending targets to hit.

#3: Interest rate not the highest compared to other savings accounts

In terms of interest rate, there’s not much to get excited about. The account’s base interest rate of 0.05% p.a. is the standard rate across most UOB savings accounts and remains unchanged even as your balance grows.

Source: UOB

With that in mind, the KrisFlyer UOB Savings Account is best viewed as a tool for earning miles, not maximising savings interest. If you’re holding larger sums of money, other accounts, such as the Standard Chartered Bonus$aver, which offers 0.15% p.a. for salary crediting, could give you a better return on your idle cash.

#4: The 5% MAB cap limits how far your miles can go

Here’s the catch: your bonus miles are capped at 5% of your monthly average balance (MAB). That means the total number of miles you can earn each month depends on how much you keep in your account.

For example, if you maintain an MAB of S$10,000 and spend S$500 monthly, your maximum bonus miles are capped at 500 miles, even if your spending could otherwise earn you more.

Without this cap, that same spending would generate about 3,000 miles per month, or 36,000 miles a year.

It’s not a dealbreaker, but it’s worth noting if you’re planning to rely heavily on this account for miles accumulation. The more you save, the higher your cap, but for smaller balances, you might hit that ceiling quickly.

What charges or fees should you look out for?

-

Minimum initial deposit: S$1,000

-

Fall-below fee: S$2 per month if below minimum of S$1,000 balance

-

Early account closure fee: S$30 (within 6 months of opening)

-

Cheque book fee: S$10

-

Debit card annual fee: S$54.50 (inclusive of GST, waived with S$6,000 annual spend)

-

Credit card annual fee: S$196.20

How to apply?

Thanks to SingPass, opening a KrisFlyer UOB Account is quick and fuss-free, and everything can be done online. As long as you meet the basic requirements, you’ll be up and running in no time. Students or first-time earners can also sign up easily since there’s currently no minimum income requirement.

Eligibility requirements are as follows:

-

At least 18 years old

-

Singapore citizen / Permanent Resident / Foreigner

-

Initial deposit of S$1,000

If you already bank with UOB, the process is even simpler. Just log in to your UOB Internet Banking account, fill in your details, and submit the application — no branch visit needed.

Explore more savings options

Looking for savings accounts beyond miles? Check out our full list of top-rated offers and compare to find the best fit for you.

KrisFlyer UOB Debit Card: What you get (and what to know)

Every KrisFlyer UOB Account comes with its own KrisFlyer UOB Debit Card, automatically issued when you open the account. You’ll get a one-time welcome bonus of 3,000 KrisFlyer miles after making your first transaction of at least S$5, a nice little head start for new users.

Beyond that first perk, the debit card’s earn rates aren’t the most exciting. You’ll earn 1 mile per dollar on Singapore Airlines, Scoot, KrisShop and Kris+ purchases, and 0.4 miles per dollar on everything else. Compared to UOB’s credit cards, which can offer up to 4 miles per dollar on selected categories, the debit card’s rates feel modest. Still, it can come in handy in a few scenarios.

If you don’t qualify for a credit card, whether you’re a student, retiree, or between jobs, this debit card lets you earn some miles while managing your spending directly from your account balance. Alternatively, frequent travellers might appreciate the card’s multi-currency feature through UOB FX+, which lets you hold and spend in up to 11 major currencies such as USD, EUR, and JPY. It’s similar to how YouTrip or Revolut work, giving you better foreign exchange control when you travel.

For most users, though, the KrisFlyer UOB Debit Card isn’t the most rewarding option for everyday spending. You’ll still earn just 0.4 miles per dollar on overseas transactions, and the extra perks, like 200 bonus miles for every S$1,000 converted via UOB FX+ (up to four times a year), don’t do much to offset the lower earn rate. If your goal is to rack up miles quickly, pairing the KrisFlyer UOB Account with a UOB credit card would make more sense.

Other KrisFlyer UOB Account benefits

KrisFlyer UOB Account holders also enjoy small travel-related perks with partner brands:

-

Scoot: Get free priority check-in and boarding, free standard seat selection, and an extra 5 kg baggage allowance when you book at least 20 kg of luggage.

-

Changi WiFi: Enjoy S$10 off portable Wi-Fi rentals by sending an SMS in the format KFUOB<space>[16-digit card number] to 77862.

While these are handy travel perks, the same or better benefits are available on the KrisFlyer UOB Credit Card, which typically offers higher earn rates and more flexible rewards. The debit card remains a decent starter option if you’re new to miles or prefer keeping things simple, but it’s not the fastest way to fly further.

Earn faster, travel sooner

Looking for stronger miles-earning firepower? Check out our list of the best UOB miles credit cards for 2025.