What is a Fixed Deposit (FD) Ladder?

Updated: 16 Jul 2025

FD ladders allow you to benefit from both the liquidity of shorter-term FDs and the advantageous interest rates of longer-term FDs.

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

The financial information provided here is solely for educational purposes. SingSaver does not offer financial advisory or brokerage services, and does not provide recommendations for specific investments.

What is an FD ladder?

A Fixed Deposit (FD) ladder is an investment strategy designed to strike a balance between maximising returns and maintaining liquidity. It involves dividing a lump sum of money into multiple FDs with different maturity dates.

Instead of locking all your funds into a single FD, you create a "ladder" of FDs that mature at staggered intervals. This approach offers a way to earn higher interest rates compared to regular savings accounts while also ensuring that you have access to some of your funds at regular intervals.

>> Looking to invest? Find out the best FD rates for this month

Key takeaways

|

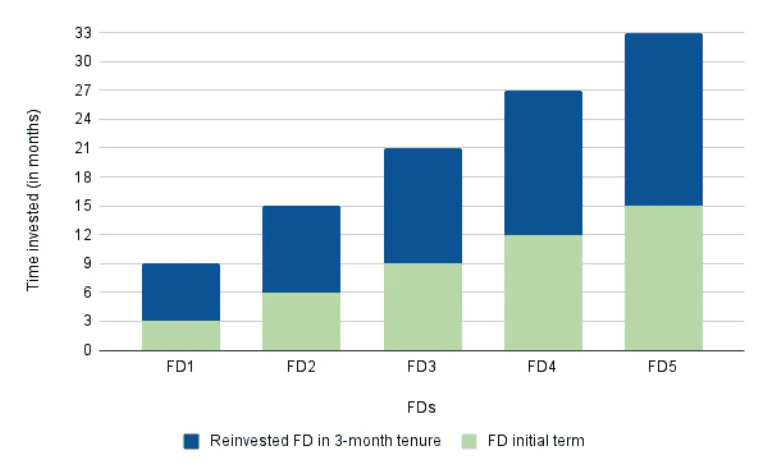

How FD laddering works

An FD ladder lets you choose FD terms by months and years and reinvest the money in long-term FDs

Saver-savvy tip

Remember, FD rates in Singapore are subject to change, and the most appealing deals are frequently promotional. To stay ahead, regularly check bank websites for the latest rates. Some banks offer exclusive promotions, often accessible only via mobile banking, so pay close attention to announcements and act quickly to secure those limited-time interest rates.

Steps on how to build an FD ladder

Building an FD ladder is a straightforward process, and here's how you can make your own.

Step 1: Open multiple FD accounts

To begin your FD ladder, you'll need to strategically open several FDs with varying maturity lengths. There are banks that offer multiple options, with some starting from 1 month and others offering yearly tenures lasting 12-, 18-, 24-months, and some even longer.

-

When choosing these tenures and amounts, it's important to align them with your specific financial goals and keep a close eye on current interest rate trends in Singapore. For example, if rates are predicted to rise, you might opt for shorter tenures to reinvest at higher rates later.

-

Consider diversifying your FDs across different banks. This allows you to capitalise on the most competitive interest rates offered by each institution, thus enhancing the overall effectiveness of your FD laddering strategy.

To illustrate how an FD ladder works, let's consider using an investment amount of S$30,000 as an example. You could divide this lump sum into three equal parts: S$10,000 each.

-

Invest the first S$10,000 in a 6-month FD.

-

Invest the second S$10,000 in a 9-month FD.

-

Invest the final S$10,000 in a 12-month FD.

Step 2: Reinvest FD funds upon maturity

As each FD in your ladder reaches its maturity date, the next step is to reinvest the funds into a new FD, typically with a longer term, to maintain the ladder's structure. As you consistently reinvest, you ensure the ladder remains intact, providing a continuous stream of maturing FDs at staggered intervals.

This strategy allows you to have a steady flow of available funds, providing you with the peace of mind that comes from knowing you have accessible capital. Moreover, the decision to reinvest into longer-term FDs, when suitable, allows you to capture the more attractive interest rates offered, leading to a substantial increase in your investment's earning potential over time.

Here’s how it would look based on the S$30,000 investment example above:

-

After six months, the first FD matures, providing you with S$10,000 plus interest.

-

Take the money from the first investment and reinvest the same amount into a new nine-month FD.

-

Three months after your first investment, the second one matures, which you can also use to invest in a new 12-month FD.

-

Six months later, the third FD matures, which you can reinvest to continue the ladder.

» Want more access? Check out SingSaver’s list of the best online savings accounts

Saver-savvy tip

What's the first step someone interested in building an FD ladder should take?

If opening a single FD is a straightforward financial task, building an FD ladder requires a more strategic approach. You'll be establishing multiple FDs simultaneously, so it's wise to begin by selecting a bank in Singapore that offers a diverse range of FD tenures. This means looking for a financial institution with terms spanning from three or six months to several years and with consistently competitive interest rates across all durations.

When constructing an FD ladder, it is generally best to focus on standard, non-promotional interest rates, ensuring that each FD matures at regular intervals, such as every 12 months. While promotional FDs can offer attractive interest rates, their often irregular maturity periods, such as three or six months, can complicate the process of building a well-structured and easily manageable ladder, especially for beginners. However, once you understand the ups and downs of FD laddering, you can now take advantage of more diverse durations and promotional rates.

FD laddering benefits

FD ladders offer several advantages, particularly for Singaporean investors seeking a balance between growth and liquidity. Here's a breakdown of the key benefits:

-

Regular access to funds upon maturity: Unlike a single, long-term FD that locks up your capital, an FD ladder provides periodic access to your money. As each FD in the ladder matures, you receive the principal plus earned interest. You can rely on a portion of your funds becoming available at regular intervals, enhancing your financial flexibility.

-

Mitigation of interest rate risks: In Singapore's dynamic financial market, interest rates can fluctuate. By diversifying your FDs across different tenures, you mitigate the risk of locking in a low rate for an extended period. If interest rates rise, you can reinvest the matured FDs at the new, higher rates. Conversely, if rates fall, you'll still benefit from the higher rates secured in your longer-term FDs. This strategy smooths out the impact of interest rate volatility, providing a more stable return on your investment.

-

Potential for higher returns: Compared to regular savings accounts, FDs typically offer higher interest rates, especially for longer tenures. And if you structure your investments into a ladder, you can capitalise on these higher rates while maintaining liquidity. This is a key reason why many Singaporeans consider FD laddering benefits.

>> MORE: Best alternatives to Fixed Deposit accounts in Singapore

Potential drawbacks of FD laddering

While FD ladders offer numerous benefits, it's important to consider the potential downsides:

-

Inflation risk: Like any fixed-income investment, FD ladders are susceptible to inflation risk. If the inflation rate in Singapore exceeds the interest rates earned on your FDs, your real return (after accounting for inflation) will be negative. To counter this, consider exploring various saving strategies to lessen inflation’s impact, such as diversifying your investments beyond FDs or regularly adjusting your FD ladder to take advantage of any potential interest rate increases.

-

Lower returns in declining interest rate environments: While FD ladders mitigate interest rate risk to some extent, they can result in lower returns when interest rates are consistently declining. As shorter-term FDs mature, you'll be forced to reinvest at the new, lower rates. This can lead to a gradual reduction in your overall returns, especially if the decline is prolonged.

-

Early withdrawal penalties: Although FD ladders provide periodic access to funds, accessing the funds before maturity will likely incur early withdrawal penalties. How much the penalties cost can vary between banks, FD types and when you withdraw the FD during the tenure. If you anticipate needing frequent access to your funds, an FD ladder may not be the most suitable option.

FD ladder structures alternatives

While the standard FD ladder provides a solid foundation for balancing returns and liquidity, there are variations that can be tailored to meet specific financial needs.

Short-term with fewer FDs

For those with limited capital or shorter-term financial goals, going for fewer FDs and shorter maturity periods can be an effective strategy. Instead of a complex, multi-year ladder, you might opt for a simpler structure with, say, three FDs maturing every one or three months.

For example, if you have a lump sum of S$6,000, you could divide it into three FDs of S$2,000 each, with maturities staggered at three-month intervals. This allows you to access a portion of your funds every three months while still benefiting from the slightly higher interest rates offered by FDs compared to standard savings accounts.

Doing uneven FD amounts

Instead of dividing your investment into equal portions across all FD tenures, you can allocate a larger portion of your funds to longer-term FDs while keeping smaller amounts in shorter-term ones. This strategy introduces greater flexibility, allowing you to fine-tune the balance between liquidity and the potential for higher returns.

For instance, you might choose to invest 60% of your funds in longer-term FDs, such as a 12-month or 24-month tenure, to capture higher interest rates and the remaining 40% in shorter-term FDs that span for 3 or 6 months for increased liquidity. This way, you benefit from the higher returns associated with longer-term investments while still having access to a portion of your capital at more frequent intervals.

» Interested in maximising returns instead of stable gains? Find out more about brokerage accounts

Alternatives to FD ladders for higher risks, higher rewards

While FD laddering offers a stable, low-risk approach to investing, those willing to accept greater risk for potentially higher returns might consider these alternatives, such as stocks, mutual funds, and bonds.

Another strategy to consider, especially when investing in these riskier assets, is dollar-cost-averaging (DCA). This involves investing a fixed amount of money at regular intervals, regardless of the asset's price. For instance, instead of making a single S$12,000 investment at the year's end, you could opt for DCA by investing S$1,000 consistently each month.

The core idea of dollar-cost averaging is simple: buy more when prices are low and less when they're high. This helps you build potential future returns. By accumulating a greater number of shares when prices are lower, you effectively reduce the average cost per share over time. Consequently, if the asset's value appreciates, you stand to profit when you sell your accumulated shares at a higher price.

Your perfect FD ladder

Creating the perfect FD ladder is all about aligning your investment strategy with your financial situation and goals. This can be saving for retirement, a down payment on a home, or children's education. Each of these objectives requires a different balance between liquidity and term savings, and your FD ladder should reflect this.

Consider your cash flow needs, risk tolerance, and the time horizon for your goals. Start by determining the total amount you wish to invest and then divide it into appropriate tenures. Also, regularly review your ladder and adjust it as your circumstances change.

Let’s say you're saving for a home purchase within the next few years, and you'll need a higher degree of liquidity. In this case, a ladder with shorter-term FDs maturing more frequently would be ideal. Conversely, if you're saving for retirement, a longer-term ladder with a higher proportion of funds in longer-tenure FDs would be more appropriate to maximise returns over time.

See FD rates by term and type

Review and compare the best rates for different FD timeframes and types:

How do FDs work?

To get the most out of FDs, it's worth understanding the ins and outs, such as understanding the current FD rates.

Stay ahead in everything finance

Subscribe to our newsletter and receive insightful articles, exclusive tips, and the latest financial news, delivered straight to your inbox.

Earn competitive yields on Singapore Treasury Bills (T-Bills) - explore our comprehensive guide.

Learn how T-Bills can potentially offer returns exceeding typical savings accounts. Explore "A Complete Guide To Treasury Bills (T-Bills) In Singapore" to understand how to maximise your investment potential.