Best Credit Cards for Fresh Grads in Singapore 2026

Updated: 28 Jan 2026

Written byAaron Wong

The Milelion

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Card | Hot Reward Pick | SingSaver Reward | Card Benefit | Annual Fee | Minimum Annual Income | ||

|---|---|---|---|---|---|---|---|

| DBS Live Fresh Student Card | - | - | 0.3 - 10 % | S$196.20 | None | |

| Standard Chartered Simply Cash Credit Card | - | - | 1.5 % | S$196.20 | S$30,000 | |

| UOB One Card | S$1,099 | 3.33 - 20 % | S$196.20 | S$30,000 | ||

| OCBC Frank Card | - | - | 0.3 - 10 % | S$196.20 | S$30,000 |

Best for general use

CIMB AWSM Card

-

Seedly rating: 4.3 / 5

-

Rewards earned: Unlimited 1% cashback on dining, entertainment, online shopping, and telco

-

Monthly spend: None

-

Annual fee: None

-

Min. annual income: S$18,000 (Age below 35); S$30,000 (Age 35-70) (for salaried employees)

Card details

-

Cashback on dining, entertainment, groceries, and online shopping

-

Cashback cap applies monthly

-

No annual fee for life

-

Contactless and mobile wallet compatible

-

Standard interest rates apply on unpaid balances

SingSaver’s take

The CIMB AWSM Card is ideal for fresh graduates who want rewards without worrying about fees or spending thresholds. It works best as a first card for daily expenses like meals, groceries, and casual shopping, while helping you build a clean credit history from day one.

Pros

No annual fee for life

No minimum spend

Simple cashback structure

Good coverage for everyday categories such as dining and telco bills

Cons

Cashback caps can be restrictive for higher spenders

No miles or premium travel benefits

SingSaver x CIMB Exclusive Offer

Receive S$50 cash when you apply and spend a min. of S$2,000 within 60 days of card approval. Plus, get an additional Samsonite Black Label Fanthom Spinner 69/25 EXP TSA Luggage (worth S$1,150) fulfilled by CIMB. Valid until 2 August 2026. T&Cs apply.

Best for those who spend on entertainment, dining and activities

OCBC Frank Card

- Enjoy 8% cashback on foreign currency transactions.

- Enjoy 8% cashback on online/contactless mobile transactions in SGD.

- Enjoy 2% cashback at selected green merchants.

- Annual fee waiver of 2 years

- Contactless payment

- Overseas rebate

- Online shopping rebate

- Minimum spend of S$800 required to earn higher cashback rate.

- Cashback capped at S$100 per month.

- Automatic annual fee waiver requires min. annual spend of S$10,000.

- Monthly spend required

Card details

-

Earn 8% in cashback on foreign currency transactions and online/contactless mobile transactions in SGD

-

Earn an additional 2% in cashback at selected green merchants

-

Earn up to S$100 in monthly cashback when you spend at least S$800 a month

-

Cashback capped monthly by category

-

Minimum S$10,000 spend required to have enjoy annual fee waiver

SingSaver’s take

This card is best suited for fresh graduates who enjoy going out, socialising, and spending on experiences rather than just necessities. If your lifestyle includes frequent dining out, events, or weekend activities, the OCBC Frank Credit Card helps offset those costs meaningfully. However, it only makes sense if you can consistently hit the minimum spend, otherwise the rewards drop sharply. Used intentionally, it works well as a lifestyle-focused card rather than an all-purpose one.

Pros

Strong cashback on lifestyle spending

Relevant rewards for social and urban lifestyles

Easy integration with mobile wallets

Cons

Requires disciplined spending to meet minimum spend

Cashback caps limit high spenders

Annual fee applies after the first year

Best for those planning a gap year or travel

DBS Live Fresh Student Card

- Enjoy 5% Cashback on McDonald's, Starbucks, Golden Village, Netflix and Spotify.

- Enjoy additional 5% Green Cashback on selected eco-friendly Eateries, Retailers, and Transport Services.

- 0.3% Cashback on All Other Spend

- 5 Years Annual Fee Waiver

- No minimum spend required

- No minimum income required

- Mobile contactless rebate

- Local spending rebate

- No income required

- Monthly credit limit of S$500

- Monthly cashback cap of S$50

- Rebate cap applied

Card details

-

Up to 5% cashback on certain brands including McDonald’s, McDelivery, Starbucks, and streaming services

-

Additional 5% green cashback on selected eco-eateries, retailers and transport services

-

0.3% cashback on all other spend

-

24/7 Visa concierge with a curated range of services, amenities and exclusive privileges.

-

S$100 late fee for an outstanding balance above S$200

-

Designed for students and those without full-time income

-

Sustainable and made from 85.5% recycled plastic

SingSaver’s take

If you are taking time off to travel, volunteer, or explore opportunities before full-time work, this card keeps costs predictable while still rewarding digital-first spending. It is particularly useful for booking flights, accommodation, and transport online. While the cashback caps are modest, the lack of fees and income requirements make it a low-risk entry point into credit cards during transitional life stages.

Pros

No income requirement

No annual fee

Rewards align well with common spend categories for students such as popular eateries and streaming services

Cons

Lower cashback limits

Not suitable once spending increases significantly

Limited long-term rewards growth

SingSaver x DBS CC Exclusive Offer

Enjoy S$300 Cash, S$340 eCapitaVoucher, 22k HeyMax Miles (worth S$396), Sony WF-1000XM6 (Earbuds), or Dyson TP10 when you apply and spend a minimum of S$500 within 30 days of card approval. Use promo code SINGSAVER. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$120 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

Best for those who just got their first job

- 1.5% unlimited cashback rate with no min. spend.

- Enjoy offers and privileges for online, dining, retail and more with The Good Life®.

- First year annual fee waiver.

- 1.5% unlimited cashback

- No rebate cap

- No monthly spend required

- First year annual Fee waiver

- Cannot be used for EZ-Reload.

Card details

-

Unlimited cashback on all spending categories — no need to track categories

-

No minimum spend to earn cashback

-

Cash rebate automatically credited to your card statement

-

Contactless and mobile wallet enabled

-

Works well for everyday expenses like transport, groceries, meals, and bills

SingSaver’s take

The Standard Chartered Simply Cash Credit Card is a great starter card for fresh graduates as they focus on building their credit score, because it combines simplicity with ongoing usefulness. There’s no annual fee to worry about, and you earn cashback on everyday spending without needing to hit tiers or track categories. Most importantly, regular on-time payments and responsible usage of this card will be reported to the Credit Bureau Singapore, helping you establish a solid credit profile, a key factor that lenders consider when you apply for bigger financial products like loans or higher-limit cards in the future.

Pros

Unlimited cashback with no category tracking

Easy to manage for first-time cardholders

Good for all-around everyday spending

Cons

Cashback rate is modest compared with targeted lifestyle cards

Fewer perks for specific categories like dining or travel

SingSaver x SCB Simply Cash Card Exclusive Offer

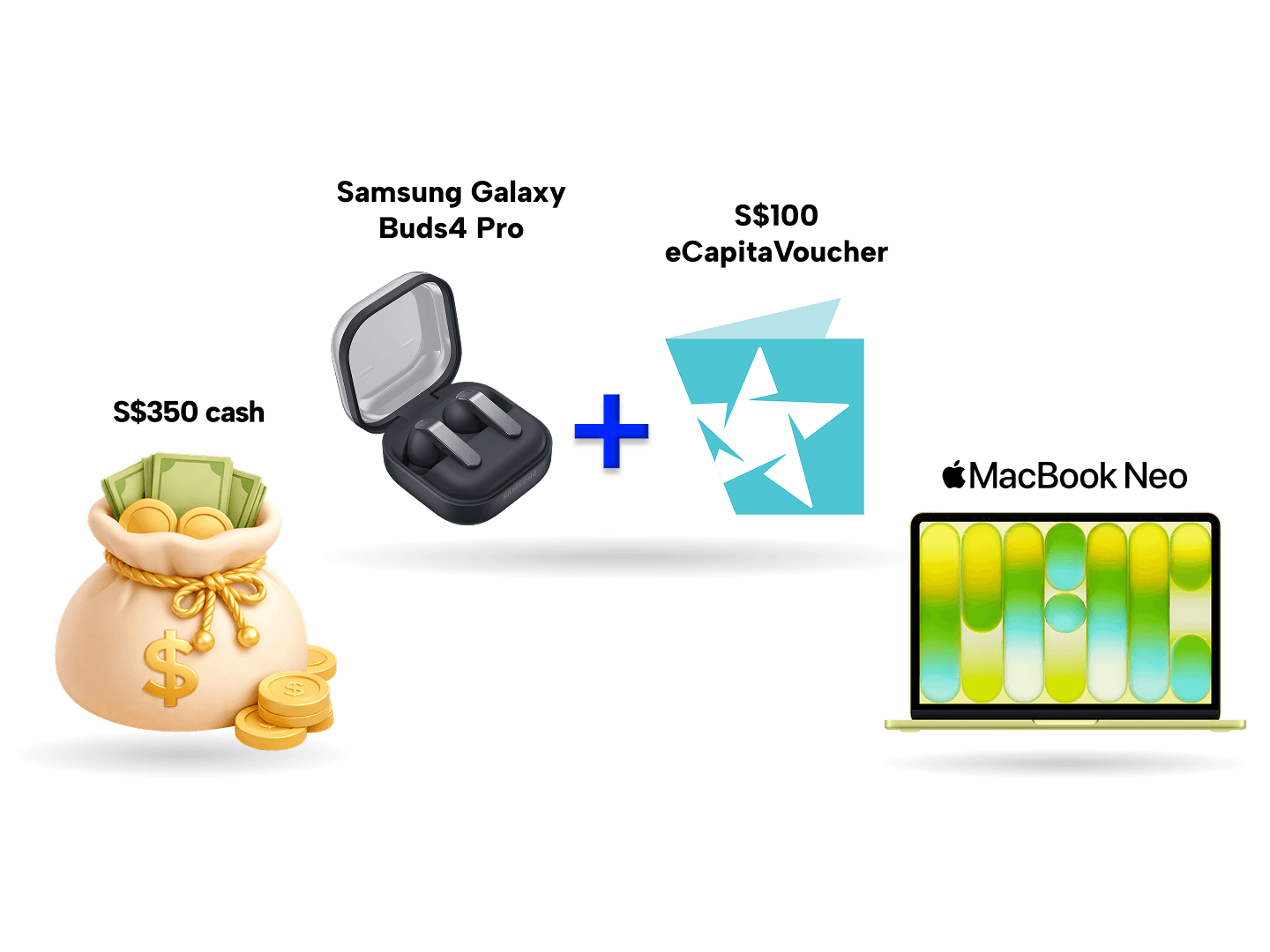

Get a Samsung Galaxy Buds4 Pro + 100 eCap bundle (worth S$449) or up to S$370 when you apply for a Standard Chartered Simply Cash Credit Card via SingSaver, spend a minimum of S$800 within 30 days of card approval, and apply for one of these products: EasyPay, Bonus$aver Account, CashOne, or CCFT. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

Best for those planning further study

- Up to 20% cashback on daily spend at McDonald's, Grab, SimplyGo (bus/train rides) and Shopee.

- Up to 18% cashback on all grocery spend.

- Up to 4.33% on SP utilities bill.

- Up to 3.33% cashback on all retail spend.

- Petrol savings of up to 22.66% at Shell and SPC.

- Greater savings with up to 3.4% p.a. interest with UOB One Account+.

- Supermarket rebate

- Grab/taxi rebate

- Spend at least $600 monthly based on your qualifying quarter to enjoy up to 10% cashback.

- Awarding of cash rebate only comes every quarter.

- Qualifying monthly spend for cash rebate has to be spread out across min. 10 different purchases.

- Terms and conditions apply for all above-mentioned privileges. Visit here for more details. Insured up to S$100,000 by SDIC.

- Monthly spend required

- Rebate cap applied

Card details

-

Cashback of up to 10% on daily spend and up to 8% on all groceries

-

Additional cashback cap at S$120 monthly

-

Mobile wallet and contactless payment supported

-

Flexible redemption options including statement rebates or UOB rewards points

-

Useful banking ecosystem with UOB app budgeting tools

SingSaver’s take

The UOB One Card is a strong choice for fresh graduates who are transitioning into a period of intensive study — whether that’s a master’s degree, professional certification, or overseas programme. The card’s tiered rewards structure means you can earn meaningful rebates on everyday spending while also keeping your costs manageable. Because the rewards are tied to meeting straightforward criteria like a spend threshold and transaction count, it encourages good card use without being overly complex. This makes it a sensible long-term card that stays useful even as your lifestyle and spending evolve from student-era habits into professional and study-focused ones.

Pros

Reward rates can be strong when conditions are met

Covers a broad range of spending categories

Flexible redemption options

Helps build credit history over a longer horizon

Cons

Rewards require meeting monthly conditions

Not ideal if spending is irregular or very low

SingSaver x UOB One Credit Card Exclusive Offer

Get S$60 Cash via PayNow when you apply for a UOB One Credit Card and make a min. spend of S$500 within the first 30 days of card approval. Promotion is valid for new-to-UOB credit cardmembers only. Valid till 31 July 2026. T&Cs apply.

UOB Welcome Offer

Get S$100 Samsung e-vouchers or 10% discount on Samsung Singapore transactions via online store on top of SingSaver exclusive rewards when you apply for a UOB credit card and spend a min. of S$1,000 in the first month from the card’s approval. Valid till 31 July 2026. T&Cs apply.

What fresh grads should look for in a credit card

Your first credit card should make your financial life easier, not more stressful. As a fresh graduate, the goal is to build good credit habits, keep costs low, and earn rewards that actually match how you spend. Here are the key things to look out for before applying.

-

Prioritise low or no annual fees. Many entry-level credit cards in Singapore offer annual fee waivers for the first year or even for life. This matters because you may not spend enough early on to justify paying S$190+ a year just to keep a card. A low-cost card gives you room to learn without feeling pressured to “use it more” just to make it worthwhile.

-

Check the minimum income requirement carefully. Most standard credit cards require a minimum annual income of S$30,000, while student cards have no income requirement but stricter credit limits. If you have just started work and are still on probation, choose a card known for being more approval-friendly rather than applying for multiple cards at once, which can hurt your credit profile.

-

Look for simple rewards structures. Cards with complicated tiers, rotating categories, or tight monthly caps can be overwhelming for first-time users. A flat cashback card or a straightforward lifestyle cashback card is often easier to manage and helps you understand how credit card rewards actually work.

-

Avoid high minimum spend requirements unless they match your real spending. Some cards only unlock meaningful rewards if you spend S$600 to S$1,000 a month. If your current expenses are lower, you may end up overspending just to qualify for rewards, which defeats the purpose of having a credit card in the first place.

-

Consider how the card helps you build credit. Paying your balance in full and on time every month is far more important than earning rewards. Cards from major banks with strong digital tools, spending alerts, and repayment reminders can help you stay organised and avoid late fees.

-

Check interest rates and fees even if you plan to pay in full. Credit card interest in Singapore can exceed 25% annually, and late payment fees add up quickly. Knowing the costs upfront reinforces why credit cards should be used as a payment tool, not a borrowing one.

Finally, think about how long the card will stay relevant. A good first credit card should still make sense after your first salary bump or lifestyle change. Cards that can grow with you reduce the need to cancel and reapply too often, helping you maintain a stable credit history.

In short, the best credit card for fresh graduates is one that fits your current income, rewards your everyday spending, and encourages responsible habits from the start.

Find the right credit card for you in no time. 💳✨

Compare exclusive offers on SingSaver across cashback, miles, and rewards cards—plus enjoy stackable welcome gifts.

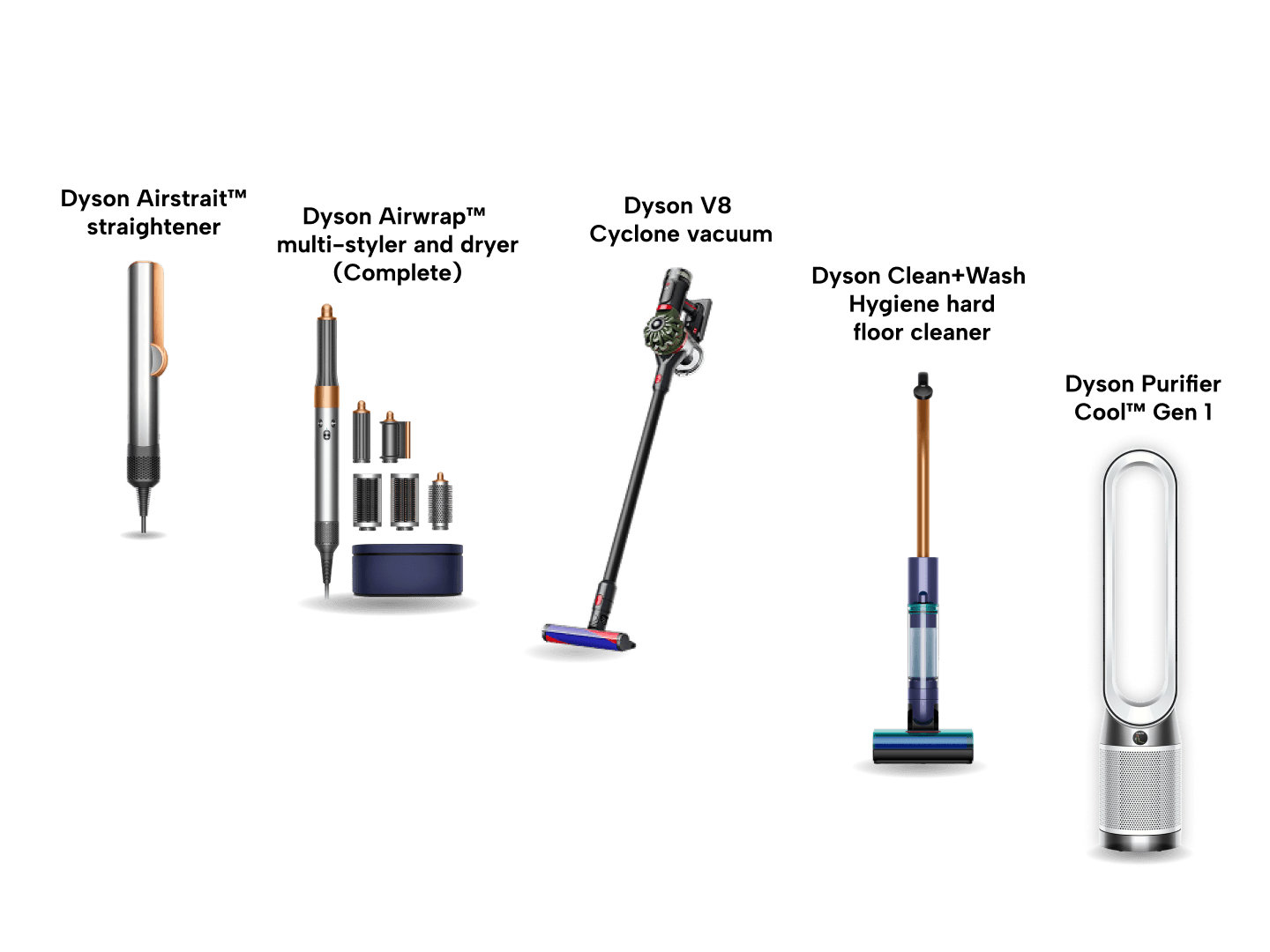

Make Dyson yours today

Apply for select Citi, HSBC, OCBC, DBS and Standard Chartered Credit Cards and a premium Dyson machine as your sign-up gift! Whether it’s a high-tech vacuum or the iconic hair stylers, it’s yours at a fraction of the cost. Exclusive deal, only via SingSaver. Claim your Dyson with a small top-up and required spend – promo ends soon. T&Cs apply.

How to best use your credit card as a fresh grad

Your first credit card can either be a helpful financial tool or an expensive mistake. The difference comes down to how you use it. Here are practical ways to make sure your credit card works in your favour from the start.

-

Use it as a payment tool, not a borrowing tool. A credit card should replace cash or a debit card for everyday spending, not fund purchases you cannot afford. Only charge amounts you already have the cash to repay.

-

Pay your balance in full every month. This is the single most important rule. Paying the full statement balance by the due date helps you avoid interest charges, which can exceed 25% annually in Singapore, and builds a positive credit history at the same time.

-

Keep your credit utilisation low. Try not to use more than 30% of your available credit limit at any time. Lower utilisation signals responsible behaviour to lenders and supports a healthier credit profile.

-

Start with small, regular expenses. Everyday spending such as transport, groceries, meals, or subscriptions is ideal. These predictable charges make it easier to budget and repay consistently.

-

Set up alerts and reminders. Enable spending notifications and payment reminders through your bank’s app. Automation reduces the risk of missed payments, which can hurt your credit score early on.

-

Avoid instalment plans unless necessary. While interest-free instalments can be useful, having too many ongoing instalments can complicate cash flow and reduce financial flexibility.

-

Resist the temptation to chase rewards. Cashback and points are a bonus, not the goal. Do not spend more than usual just to earn rewards, especially in your first year of credit card use.

-

Review your statements monthly. Take a few minutes to check your statement for errors, fraud, or spending patterns that need adjusting. This habit builds long-term financial awareness.

Used thoughtfully, your credit card can help you build confidence, discipline, and a strong credit foundation as you move through your early career.

Benefits of owning a credit card as a fresh grad

Getting your first credit card can feel intimidating, but when used responsibly, it can be a powerful financial tool. For fresh graduates who are just starting their careers, a credit card offers more than just convenience. Here are the key benefits to understand.

-

Builds your credit history early: Using a credit card and paying your bills on time helps establish a credit record in Singapore. A good credit history makes it easier to qualify for future credit products like personal loans, car loans, or home loans, often at better rates.

-

Improves cash flow management: A credit card allows you to manage short-term expenses without needing immediate cash, as long as you repay the full balance by the due date. This can be helpful during months when expenses are uneven, such as when work-related costs or one-off purchases come up.

-

Earns rewards on everyday spending: Even basic credit cards offer cashback or points on daily expenses like transport, groceries, and meals. Over time, these small rewards add up and effectively reduce your overall spending.

-

Provides added security over debit cards: Credit cards generally offer better fraud protection and dispute processes than debit cards. If there is unauthorised spending, your personal bank balance is not immediately affected while the issue is investigated.

-

Helps track and organise spending: Monthly statements and mobile banking apps make it easier to see where your money goes. This visibility helps fresh grads build budgeting habits and spot areas where they may be overspending.

-

Unlocks access to promotions and instalment plans: Many credit cards offer exclusive discounts, dining deals, and interest-free instalment options. These can make larger purchases more manageable without paying interest, as long as instalment payments are made on time.

Used carefully, a credit card can be a stepping stone to better financial confidence and long-term financial health.

Frequently asked questions about credit cards for fresh grads

Yes, as long as you use it responsibly. Paying your credit card bills on time, keeping your balances low, and avoiding missed payments all contribute positively to your credit history with the Credit Bureau Singapore.

There is no fixed amount, but a good rule of thumb is to keep your spending below 30% of your credit limit and only charge expenses you can repay in full every month. This helps maintain healthy credit utilisation.

Yes, most Singapore-issued credit cards can be used internationally, especially those on Visa or Mastercard networks. Before travelling, check whether overseas usage is enabled in your banking app and be aware of foreign currency transaction fees, which typically range from about 2.8% to 3.5%.

Both have their place, but a credit card is generally better for fresh graduates who can manage it responsibly. Debit cards help with strict spending control since you are using your own money, but they do not help build your credit history. Credit cards, when paid in full and on time, help establish a credit record, offer better purchase protection, and provide rewards on everyday spending.

Cancelling a credit card is not necessarily bad, but keeping your first card open for a longer period can help your credit profile by maintaining a longer credit history. If the card has no annual fee, it may be worth keeping even if you stop using it regularly.

It is better to start with one card. Applying for several cards in a short period can lower your approval chances and may negatively affect your credit profile early on. Start simple and add more cards only when your income and needs grow.

Relevant articles

Stay ahead in everything finance

Subscribe to our newsletter and receive insightful articles, exclusive tips, and the latest financial news, delivered straight to your inbox.

About the author

Aaron Wong

Aaron founded The Milelion to teach people how to travel better for less, with credit cards, airline and hotel loyalty programmes. With 500,000 miles flown and counting, he’s keen to debunk the myth that you can’t travel in style without breaking the bank.