Best Personal Loans for Foreigners & Expats in Singapore

Updated: 8 Jun 2026

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Moving to a new country comes with its fair share of settling-in costs—from rental deposits to furnishing your condo or handling unexpected emergencies. If you are an expatriate living here, securing a personal loan for foreigners singapore can provide a vital financial cushion.

However, banks assess foreign applicants differently than citizens or Permanent Residents (PRs). Lending guidelines are much stricter, and baseline requirements vary significantly depending on whether you are an Employment Pass (EP) holder, an S Pass holder, or a specific nationality like Malaysian or Indian expats.

Let's break down the best personal loan for foreigners singapore options currently available on the market, helping you navigate interest rates, processing fees, and eligibility benchmarks

Want to learn more about the financial situation in Singapore? Read our blog on the top five financial trends in Singapore.

Can foreigners in Singapore get personal loans?

Short answer is yes, if you fulfil several requirements. Securing a personal loan as a non-resident requires meeting several strict baseline benchmarks set by retail banks to mitigate capital flight risks.

1. Income Tiers By Pass Type

Your work pass type heavily influences your credit risk profile:

-

Employment Pass (EP) Holders: If you hold a standard EP, Personalised Employment Pass (PEP), or One Pass, you have access to the lowest interest rates and highest loan limits, provided you meet the S$45,000 to S$90,000 annual income thresholds.

-

S Pass Holders: Mid-level skilled technicians on an S Pass face a tougher borrowing landscape. While some banks accept a baseline income of S$40,000 to S$45,000, your loan quantum is strictly capped, and interest rates may lean slightly higher.

-

Work Permit Holders: Standard retail banks in Singapore generally do not extend unsecured personal loans to Work Permit holders due to strict regulatory frameworks.

2. Nationality Variations

-

Malaysian Expats: Because of close cross-border economic links and credit-tracking capabilities, Malaysian professionals often enjoy lower minimum income thresholds (e.g., S$40,000 at UOB) compared to other global nationalities.

-

Other Global Expats (Indian, British, Australian, etc.): Most institutions treat non-Malaysian expats under standard global foreign criteria, locking the minimum income bar uniformly between S$60,000 and S$90,000.

3. Employment & Residential Stability

Banks generally want to see that you are well-settled. Expect to meet these operational conditions:

-

Employment Tenure: You must have been employed continuously in Singapore for a minimum of 6 to 12 months, or hold a corporate contract showing validation of employment stability.

-

Work Pass Validity: Your current work pass must have at least 6 to 12 months of remaining validity at the time of your loan application.

-

Age Profile: Applicants must fall within the core working age bracket, typically between 21 and 60 or 65 years old.

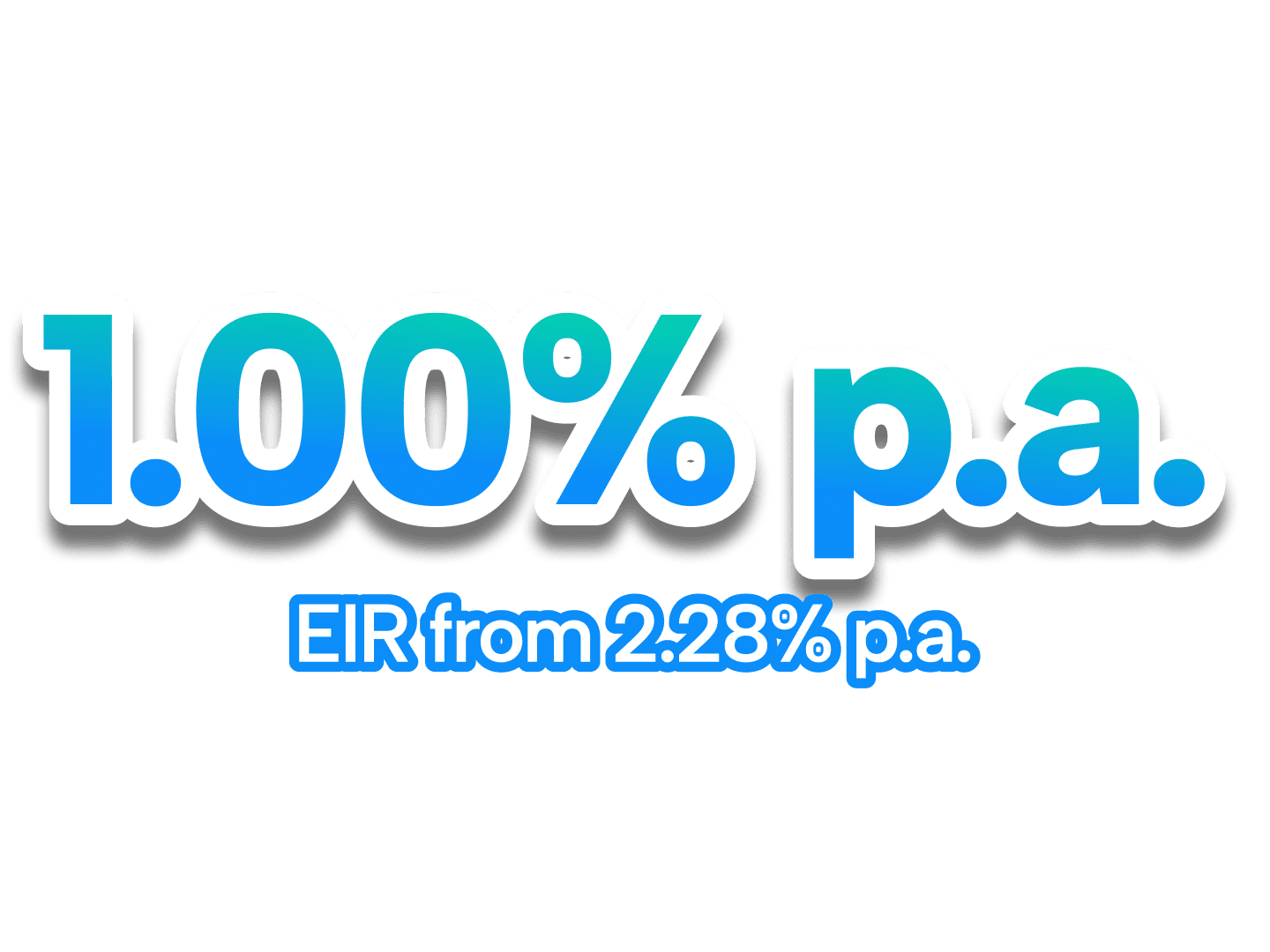

⚡SingSaver x Trust Personal Loan Flash Deal⚡

Enjoy low interest rates from 1.00% p.a. (EIR 2.28% p.a.) plus up to S$1,750 in cashback and rewards when you sign up for Trust Bank Personal Loan via SingSaver. Plus, receive a S$10 FairPrice E-Vouchers from Trust when you sign up with the referral code SINGSAVE. Valid till 2 August 2026. T&Cs apply.

SingSaver Tips

Best personal loans for foreigners in Singapore

Several banks and alternative lenders in Singapore offer personal loan products catering to the needs of foreigners and expats. Here is a breakdown of personal loan options for foreigners in Singapore.

Standard Chartered CashOne Personal Loan

1. Go to Standard Chartered's website and click "Apply Now” button under Personal Loans

2. Fill out an application and submit all required documents

3. Wait for approval of personal loan from Standard Chartered

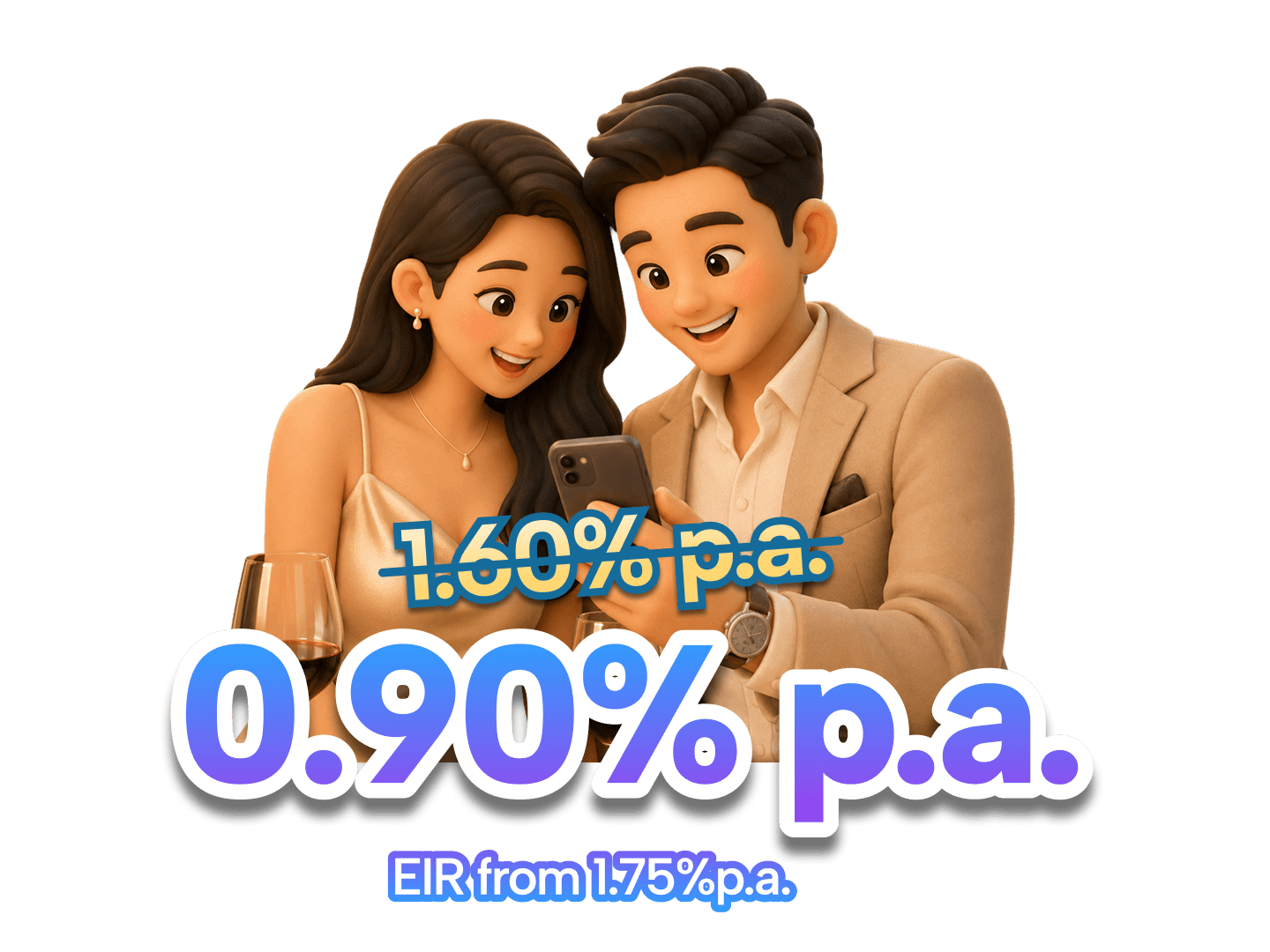

- Enjoy low interest rates from 0.90% p.a. (EIR ~1.75% p.a.) for longer tenures. Get instant loan approval and cash disbursement in as quick as 15 minutes to your designated bank account.

- Enjoy a 5-year annual fee waiver on your Standard Chartered Platinum Visa credit card

- Min. loan amount of S$1,000

- Max. loan amount of up to S$250,000

- Allow for change of loan tenure.

- Allow for flexible repayment without late fees.

- Waiver of S$50 annual fee (from 2nd year till expiry of loan) if all instalments for the year are paid on or before the due dateMax. loan amount of up to 4X monthly salary, capped at S$250,000

- Read our full review of the Standard Chartered CashOne Personal Loan

- EIR calculated is not yet inclusive of the first-year annual fee of S$199. Interest rate in your application will be based on your credit profile as determined by Standard Chartered.

- First year annual fee: S$199

- Early repayment fee: S$150 or 3% of the outstanding principal, whichever is higher

- Change of tenure: S$50 per change

- Late payment fee: S$100

- Copy of Passport (with at least 6 months' validity), including the page with address displayed (where applicable)

- Copy of your Employment Pass

- Any ONE of the following documents:

- Latest utility bill, rates or tax bill

- Latest bank / credit card statement (e-Statements are accepted)

- Rental agreement showing your address

- Latest mobile phone statement or pay-TV statement

- Letter from employer stating current address

- Government-issued document stating current address (e.g. IRAS, CPF, ICA)

No documents required for Singaporeans / PRs applying via SingPass.

For foreigners applying via SingPass, please prepare the following:

The information displayed above is for reference only. The actual rates offered to you will be based on your credit score and is subject to the provider’s approval.

⚡SingSaver x SCB CashOne Personal Loan Flash Deal⚡

Enjoy one of the market's lowest interest rates starting from 0.90% p.a. (EIR from 1.75%) plus up to S$1,800 in Cashback when you apply for Standard Chartered CashOne Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

HSBC Personal Loan

1. Go to HSBC's website and click “Apply Now” under Personal Loans

2. Fill out an application and submit the required documents

3. Wait for approval from HSBC

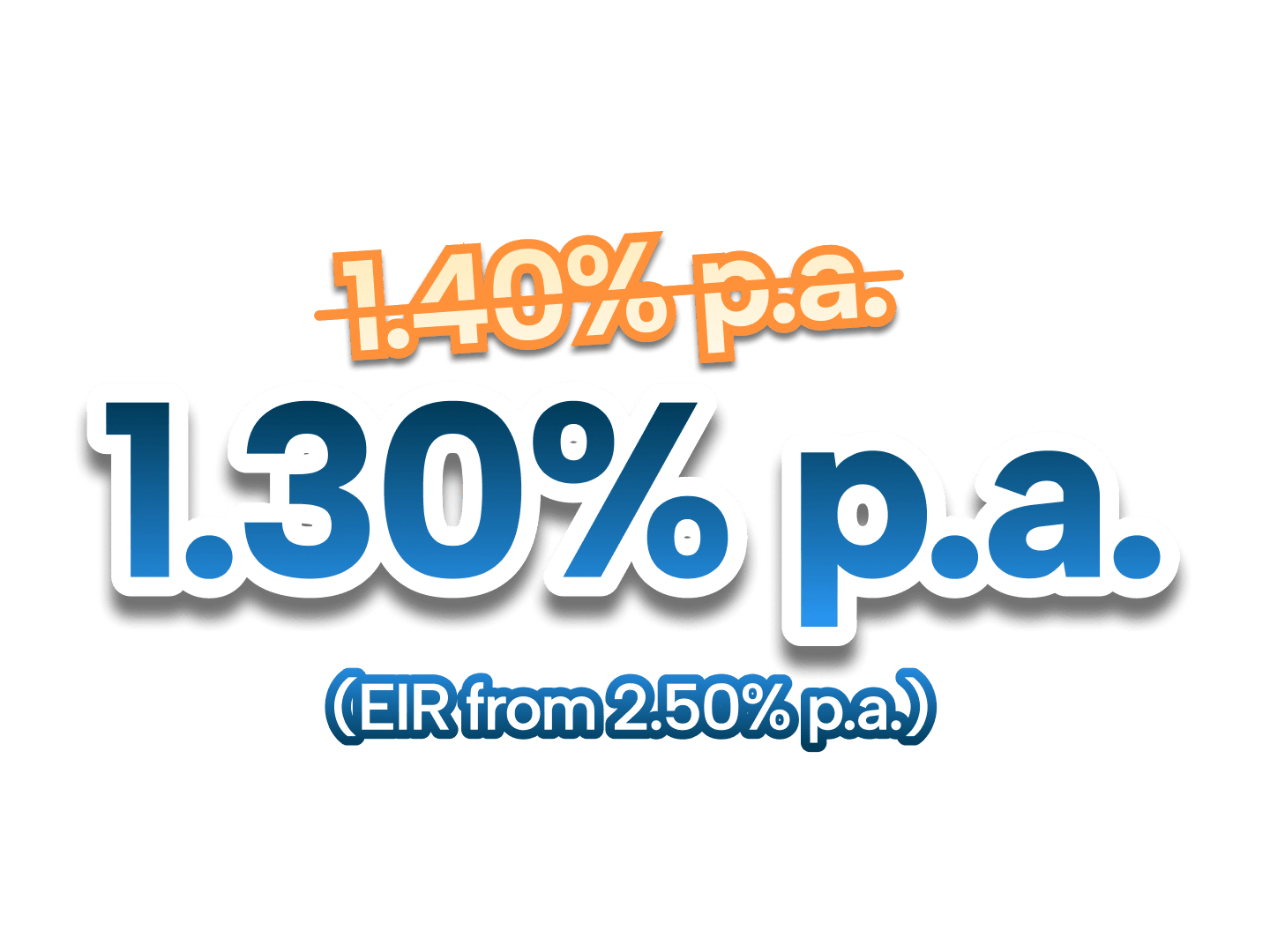

- One of the lowest interest rates from 1.30% p.a (EIR 2.50% p.a) for those earning min. S$30,000 annually.

- No processing fees

- Instant disbursement upon approval to an HSBC bank account

- Get a 1-minute in-principle approval on your HSBC Personal Loan

- Max. loan amount equal to 90/95% of approved credit limit at time of application

- Min. loan amount of S$1,000

- Option to borrow at a slightly longer loan tenure of 7 years

- Early repayment fee: 2.5% of the repayment amount

- Overdue interest: 2.5% + prevailing interest on overdue amount

- Late payment fee: S$75 for each monthly repayment that is not received in full by the monthly due date

- High base minimum annual income requirement of S$65,000 (w.e.f. 1 October 2025) Learn more.

1. NRIC (Front & Back)

2. For salaried employees: Last 3 months’ computerised payslip, or latest Income Tax Notice of Assessment with latest 1 month’s computerised payslip, or latest 6 months’ CPF statement (for Singaporeans or PRs)

3. For self-employed persons: Last 2 years’ Income Tax Notice of Assessment

The information displayed above is for reference only. The actual rates offered to you will be based on your credit score and is subject to the provider’s approval.

SingSaver x HSBC Personal Loan Exclusive Offer

Enjoy attractive interest rates from 1.30% p.a. (EIR from 2.50% p.a.) when you apply for HSBC Personal Loan via SingSaver. Available to new and existing customers! Valid till 2 August 2026. T&Cs apply.

Applying for a personal loan as a foreigner

Here's how non-Singaporeans can increase their chances of approval when applying for a personal loan in Singapore.

Documents Required For Application

To prevent lengthy processing delays, ensure you have your legal documentation completely organized before executing an application.

The Fast-Track Route: Singpass MyInfo

The absolute most efficient way to apply for an expat personal loan singapore is by authorizing the bank to read your data via Singpass MyInfo. This links directly to official government registries and automatically extracts your verified identity details, employment tenure, and tax history.

When you use Singpass, your local residential address is verified automatically, often completely eliminating the need to upload physical bills.

The Manual Route: Document Checklist

If you cannot use Singpass or if a bank requests manual document verification, you must upload clear copies of the following items:

-

Primary Identity: A valid passport along with your physical Employment Pass (EP) or S Pass front and back.

-

Proof of Income: Your official Income Tax Notice of Assessment (NOA) issued by IRAS for the latest tax year, alongside your corporate payslips from the past 3 consecutive months.

-

Proof of Local Residence: A copy of your current residential tenancy agreement, a local bank statement, or a utility/telecommunications bill issued within the last 3 months clearly displaying your full legal name and Singapore address.

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Adding a co-borrower to your loan application

While you might think adding a local friend as a guarantor could help you secure an expat personal loan singapore, Singapore’s retail banking market operates differently. Major retail banks generally do not accept co-signers or third-party guarantors simply to bypass the high minimum annual income thresholds required for a personal loan for foreigners singapore.

Instead, some financial institutions allow a joint application or co-borrower arrangement, but this is typically restricted to core family members or legal spouses who are Singapore Citizens or Permanent Residents (PRs). Entering a joint credit structure can drastically improve approval odds for high-intent applicants—such as Indian expats or Malaysian expats establishing long-term roots—because the bank evaluates the combined, stable household income. However, both parties bear equal, legal responsibility for the debt; any missed payments will permanently damage the Credit Bureau Singapore (CBS) scores of both individuals

Using collateral to secure a loan

Loans in Singapore are strictly classified as either secured or unsecured. Standard retail bank platforms offer bank loan for foreigners singapore options almost exclusively as unsecured term products, meaning they do not require physical collateral but rely heavily on your employment pass verification.

If you are an S Pass holder or an expat with a limited local credit footprint who falls below the standard unsecured income floor, you cannot pledge a car or movable property to secure a standard personal loan. Instead, you can look into alternative asset-backed structured options like a secured credit card or wealth lending line. By placing a minimum cash deposit (typically starting at S$10,000) into a locked fixed deposit account with the bank, you can unlock a corresponding credit line of up to 100% of that value. This is an excellent, low-risk way to access liquid capital while establishing your initial financial history, though the bank maintains the legal right to seize the underlying deposit if you default.

What To Consider Before Taking A Loan

Taking out unsecured credit in a foreign country requires careful budgeting. Keep these three core principles top of mind before signing a credit contract:

-

Be Mindful of the EIR: Do not rely solely on the advertised "flat" interest rate. Always check the Effective Interest Rate (EIR), which represents the true economic cost of borrowing because it factors in processing fees, compounding interest periods, and reducing balances.

-

Calculate Total Debt Servicing: Ensure your monthly loan repayment installments do not consume too much of your monthly take-home income. Remember to factor in your high fixed expat costs, like local rental commitments and international health coverage.

-

Avoid Multi-Bank Applications: Applying for multiple personal loans simultaneously across three or four different banks can hurt your credit score. Every single application triggers a hard inquiry on your CBS (Credit Bureau Singapore) report, making you look credit-hungry and potentially triggering automated rejections.

More SingSaver resources for foreigners

Stay ahead in everything finance

Subscribe to our newsletter and receive insightful articles, exclusive tips, and the latest financial news, delivered straight to your inbox.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.