Personal Loan vs Credit Card Installment: The Smart Way to Finance Your Big-Ticket Home Upgrade

Updated: 3 Jun 2026

Written byAfina Najib

Senior Content Editor - Singapore

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

With major international football tournaments and massive sports events streaming throughout the year, Singaporeans are constantly looking for ways to upgrade their viewing experience. If you want to feel like you are sitting pitchside right from your living room, a premier home cinema upgrade is almost mandatory. We are talking about an 85-inch QD-OLED TV, a Dolby Atmos 11.1.4 channel soundbar system, and deep, plush theater seating to handle those grueling extra-time matches.

A high-end cinematic setup like this can easily set you back S$6,000 to S$10,000.

When financing major home upgrades, most Singaporeans instinctively pull out a credit card for a 0% Installment Payment Plan (IPP). However, looking beneath the surface reveals that if you want to protect your cash flow and keep your credit score pristine, securing a personal loan for a big purchase is often the superior financial play.

The Hidden Trap of Credit Card 0% Installment Plans

Credit card installment plans are heavily marketed as "free." While technically true for the interest rate itself, they come with operational constraints that can quietly jeopardize your financial flexibility.

1. The Credit Limit Freeze (The "Max-Out" Effect)

When you swipe your credit card for a S$8,000 home theater system on a 12-month installment plan, the bank locks up the full S$8,000 against your credit limit immediately.

Under Monetary Authority of Singapore (MAS) regulations, the maximum aggregate credit limit for individuals earning an annual income of S$30,000 and above is capped at 4 times your monthly income per financial institution. If you earn S$5,000 a month, your credit limit is likely S$20,000. Sinking S$8,000 into a home theater means 40% of your purchasing power with that bank vanishes instantly.

This leaves you vulnerable if an actual emergency occurs, such as sudden medical bills or urgent home repairs. Your credit limit only gets restored gradually, month by month, as you pay off each installment.

2. High Processing Fees and Sneaky EIRs

Many "0% interest" plans offered directly by banks for non-participating merchants are not actually free. They charge an upfront processing fee that typically spans between 3% to 5%.

While a 5% one-time fee on a 12-month plan sounds minor, the Effective Interest Rate (EIR)—which reflects the true cost of borrowing as you pay down the principal—climbs surprisingly high, often hitting 9.5% p.a. to 10.5% p.a.

3. Credit Score Impact

Utilizing a massive chunk of your available credit card limit spikes your credit utilization ratio. Credit Bureau Singapore (CBS) tracks this closely. Consistently running a high utilization rate can signal financial stress to the bureau, temporarily dragging down your credit score and making it harder to secure crucial loans—like an HDB or bank home loan—down the road.

Predict the Champion. Share S$30,000 in Cash! ⚽

Apply for participating products, predict the next FIFA World Cup 2026 Champion, and win your share of up to S$30,000 cash. Applicable to the first 16 successful applicants at 2 PM and 8 PM daily only. Valid till 28 June 2026. T&Cs apply.

Or, apply and post creative World Cup content on Facebook or Instagram, tag SingSaver, and use #SingSaverWorldCup to win a Golden Ticket, giving you one chance to predict the winning team. Valid till 28 June 2026. T&Cs apply.

SingSaver x HSBC Credit Cards Exclusive Offers

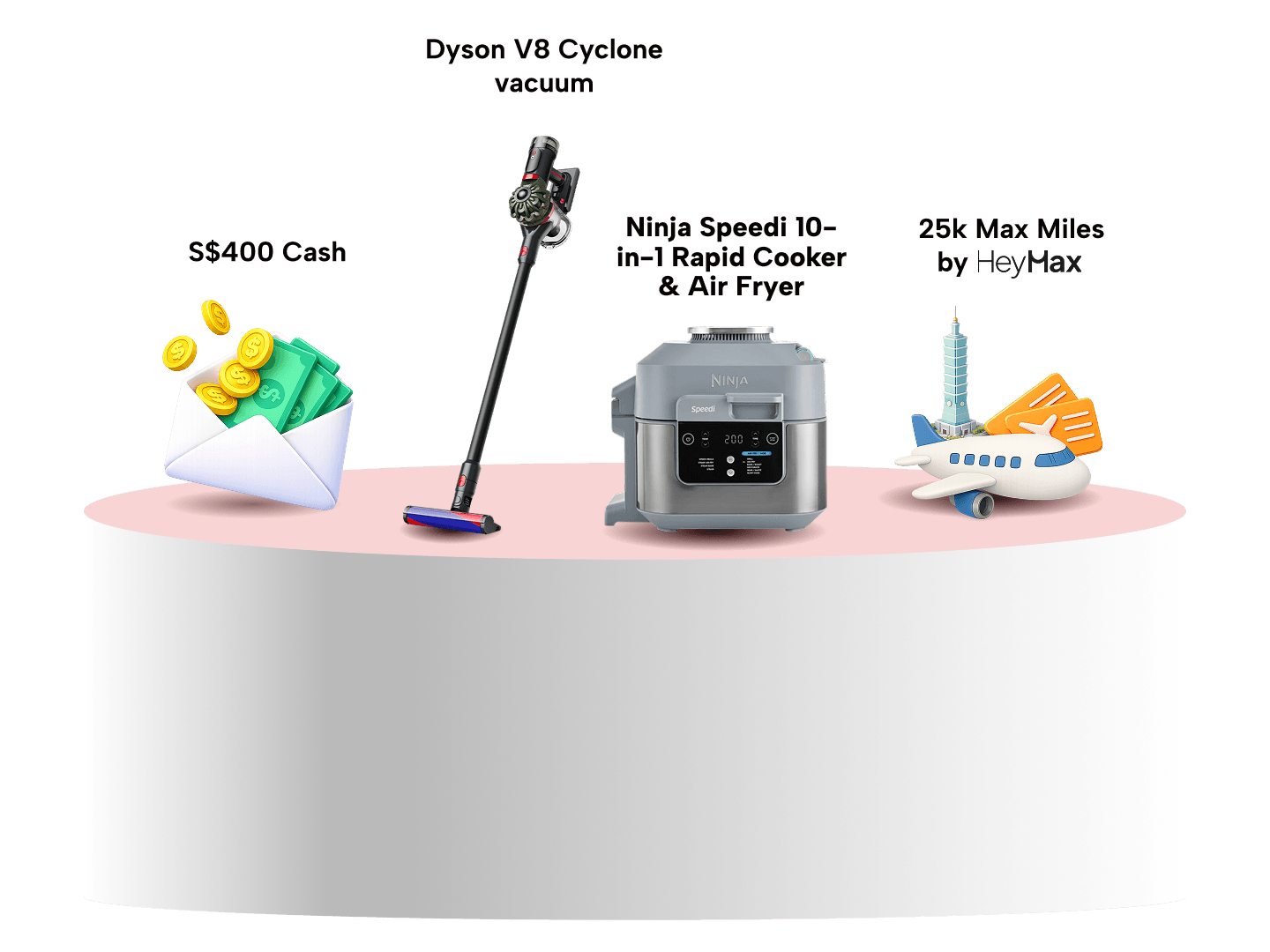

Score S$420 Upsized Cash, Dyson Airstait or V8 Cyclone cordless vacuum, 25,000 Max Miles by HeyMax (worth S$600 in travel value), or a Galaxy Buds4 Pro + S$160 eCapitaVoucher Bundle when you apply for an HSBC Credit Card via SingSaver and fulfil promo requirements. Valid until 30 June 2026. T&Cs apply.

Why a Personal Loan is the Smarter Alternative

Evaluating a personal loan vs credit card installment setup reveals that an unsecured personal loan functions entirely differently. Instead of eating into your daily purchasing power, it operates as a separate, structured credit facility.

| Financial Feature | Credit Card Installment (IPP) | Unsecured Personal Loan |

| Credit Limit Impact | Maxes out your card limit instantly | Keeps your card limits completely free |

| Repayment Flexibility | Short tenures (typically 3 to 24 months) | Flexible tenures (12 to 60 months) |

| True Cost (EIR) | Hidden upfront fees can push EIR to 10.5% p.a. | Competitive market rates |

| Credit Bureau Impact | Spikes credit utilization on CBS | Fixed installment schedule; predictable profile |

1. Keeps Your Credit Cards Liquid

A personal loan is disbursed to your bank account as a lump sum of cash. You use that cash to buy your home cinema system upfront, leaving your credit cards completely unencumbered. Your daily card remains fully functional for groceries, petrol, rewards points accumulation, and unexpected emergencies.

2. Highly Competitive Market Rates

The personal loan market in Singapore is highly aggressive. Major financial institutions offer highly competitive promotional flat interest rates. Using a personal loan for electronics allows you to leverage these low interest rates to fund your purchase cleanly.

3. Comfortable, Extended Breathing Room

Credit card IPPs generally restrict your repayment period to 6, 12, or occasionally 24 months. Splitting an S$8,000 purchase over 12 months demands a hefty S$666/month commitment.

With a personal loan, you can stretch your tenure up to 60 months (5 years) under standard MAS guidelines. While extending your loan increases the total interest paid slightly, it drops your monthly obligation significantly. This flexibility makes it a strong contender for the best way to buy a TV on installment, ensuring your wallet handles the upgrade without breaking a sweat.

SingSaver x DBS/POSB Personal Loan Exclusive Offer

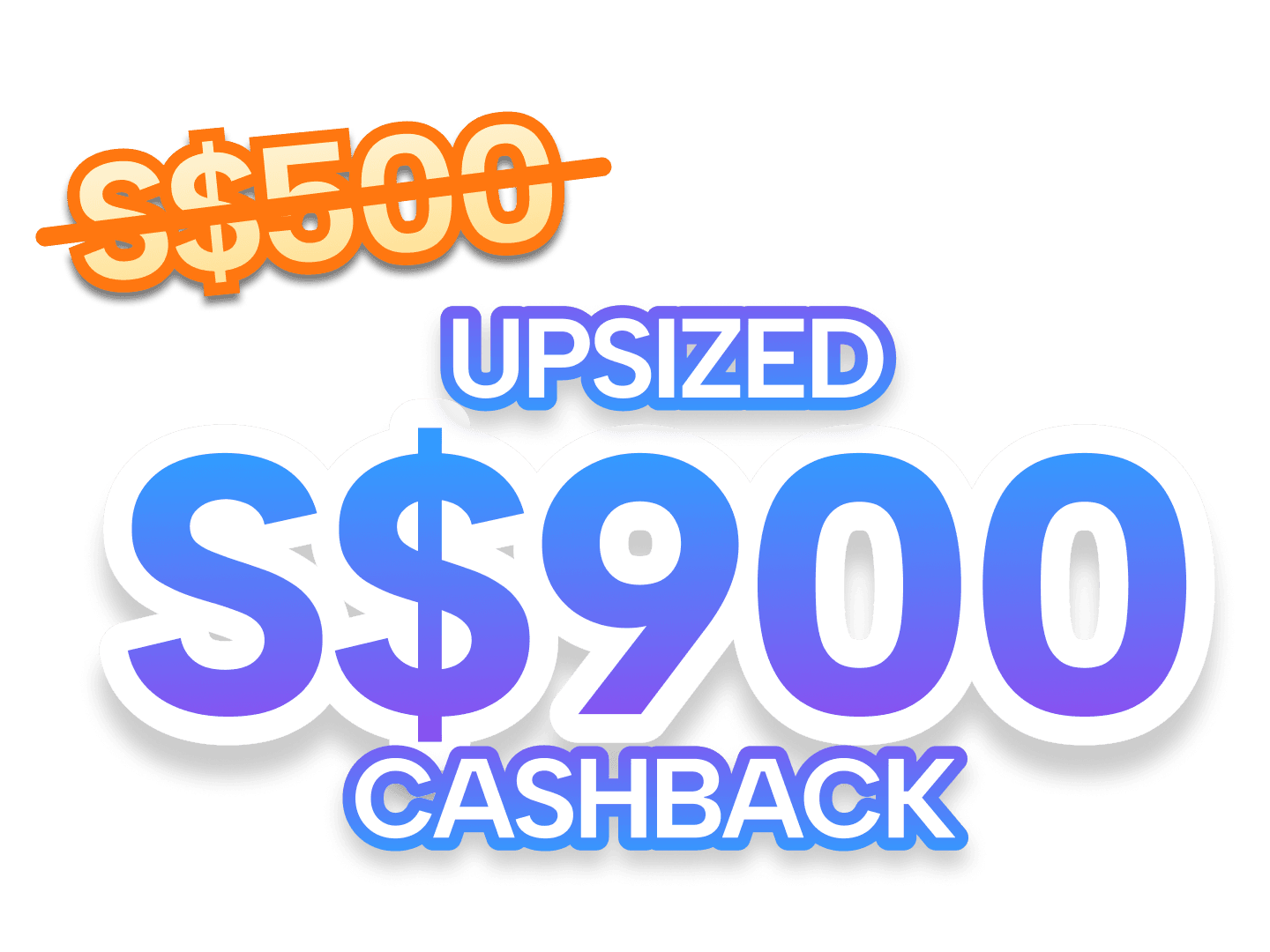

Enjoy interest rates from 1.48% p.a. (EIR from 3.22% p.a*) when you apply for a DBS/POSB Personal Loan. Plus, get S$900 bonus cash on top of up to 3% cashback when you apply for a loan min. S$10,000 with a min. tenure of 3 years. Use the promo code (SINGSAVER) upon application. Valid till 15 July 2026. T&Cs apply.

Top Personal Loan Recommendations for Big Purchases

If you are planning to utilize a personal loan for a big purchase, here are some of the most competitive options available from local and digital banks right now:

1. UOB Personal Loan

-

Best For: Fast approvals and transparent costs.

-

Interest Rate: From 1.00% p.a. (EIR from 1.93% p.a.).

-

Processing Fee: S$0 across all tenures.

-

Eligibility: Singapore Citizens/PRs with a minimum annual income of S$30,000.

-

Why we like it: Existing UOB Credit Card or CashPlus customers can skip the paperwork and get almost instant disbursement directly into their bank account.

2. Standard Chartered CashOne Personal Loan

-

Best For: Flexible instant approvals via SingPass MyInfo.

-

Interest Rate: From 1.00% p.a. (EIR from 1.94% p.a.).

-

Processing Fee: S$0 upfront processing fee (first-year annual fee is waived).

-

Eligibility: Singapore Citizens/PRs with an annual income requirement of S$30,000.

-

Why we like it: Standard Chartered offers incredibly swift turnaround times and highly robust borrowing limits (up to 4 to 8 times your monthly income depending on profile).

3. DBS/POSB Personal Loan

-

Best For: Low-income earners or those looking for extra promotional incentives.

-

Interest Rate: From 1.48% p.a. (EIR from 3.22% p.a.).

-

Processing Fee: 1% of the approved loan amount.

-

Eligibility: Lowest income barrier starting at S$20,000 annual income for Singapore Citizens/PRs.

-

Why we like it: DBS frequently runs attractive promotions, such as 3% unlimited cashback on approved loan amounts for tenures of 36 months and above.

4. Trust Bank Instant Loan

-

Best For: Digitally savvy users wanting an ultra-fast digital experience via an app.

-

Interest Rate: From 1.00% p.a. (EIR from 2.28% p.a., inclusive of a 0.88% first-year annual fee).

-

Processing Fee: S$0 processing fee, with a flat 0.88% first-year fee charged on the loan amount instead.

-

Eligibility: Singapore Citizens/PRs with an annual income of S$30,000; requires a Trust Credit Card.

-

Why we like it: You get absolute transparency through the Trust app, 60-second disbursement, and you can save on interest by repaying the loan early at any time (subject to early repayment terms).

SingSaver's Smart Verdict

If you can secure a true, zero-fee, 0% installment plan directly at retail checkout (such as through major electronics chains like Harvey Norman or Courts) and you have ample credit limit to spare, using a credit card is perfectly fine.

However, if you are custom-building your setup across multiple boutique audio-visual vendors, or if you refuse to lock up your credit card liquidity for the next year, taking out a personal loan is the cleaner financial strategy. It gives you immediate cash leverage, protects your credit utilization ratio, and offers highly competitive interest rates that respect your monthly cash flow.

Upgrade responsibly, enjoy the big games, and keep your financial health in top form.

About the author

Afina Najib

Spending most of her young writer's phase working as a freelancer, Afina's written for various industries ranging from e-commerce, travel to health and finance. Her expertise lies in her ability to make complex subjects like finance easy to consume for everyday readers.