The Pros and Cons of Debt Consolidation

Updated: 11 Dec 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

If you're managing multiple debts — such as high-interest credit cards, medical expenses, or personal loans — debt consolidation can simplify your repayments by merging them into a single monthly payment.

Opting for a debt consolidation loan or a balance transfer credit card may be a smart move if it helps reduce your overall interest costs. However, while refinancing can ease financial strain, it’s important to weigh the benefits and drawbacks to determine if it's the right solution for your financial situation.

At a glance: Pros and cons of debt consolidation

Pros

You may secure a lower interest rate, reducing overall repayment costs

A structured repayment plan can help you clear debt faster

Managing a single monthly payment simplifies budgeting

Timely repayments can improve your credit score over time

Cons

Not everyone qualifies for the lowest interest rates

Additional fees, such as processing or early repayment charges, may apply

Missing payments could negatively impact your credit and financial standing

It doesn’t solve underlying spending or financial management habits

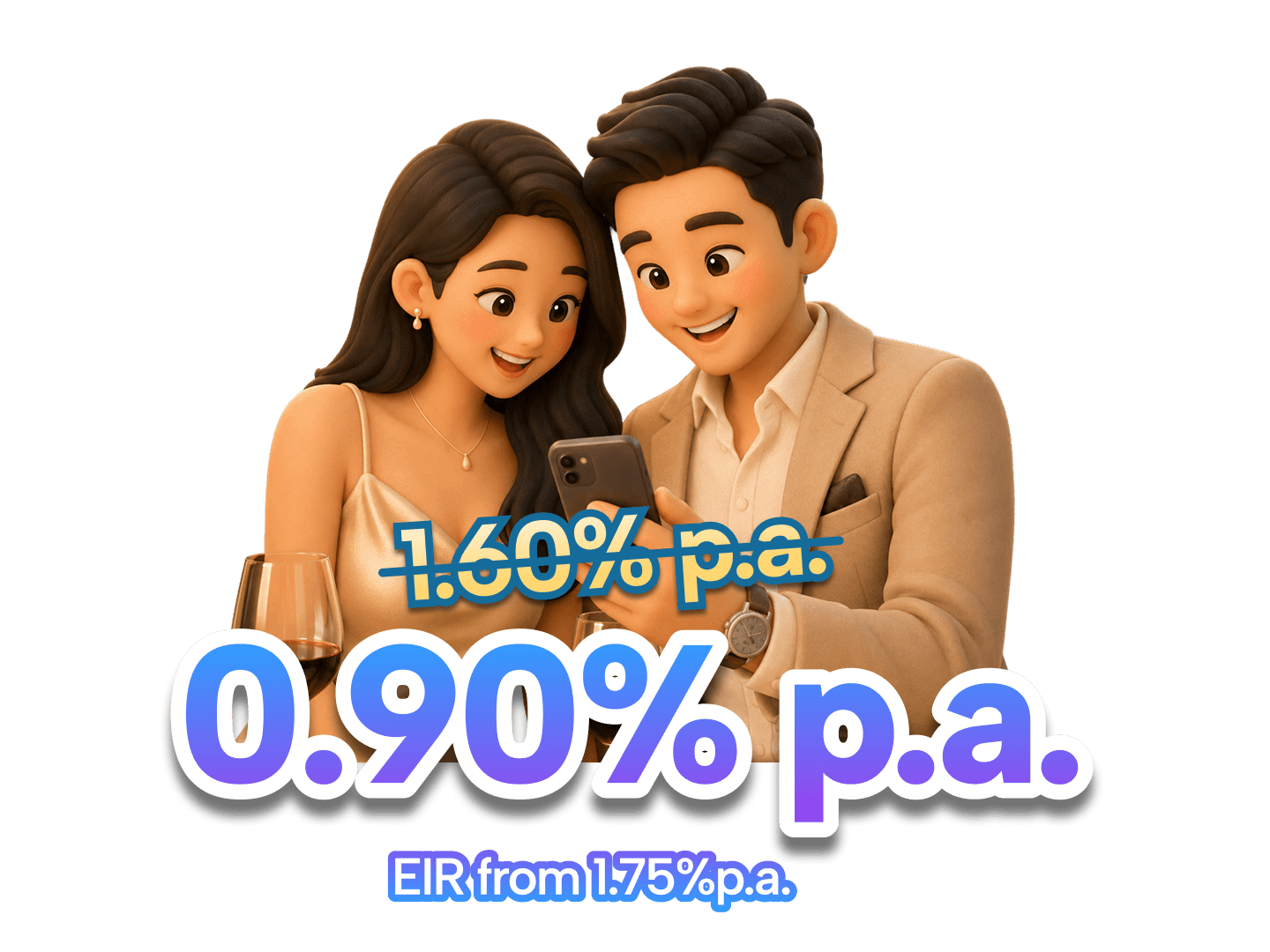

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Pros of debt consolidation

You could receive a lower interest rate

One of the main benefits of debt consolidation is reducing your overall interest costs. By consolidating multiple high-interest debts into a single loan or balance transfer credit card, you may secure a lower effective interest rate (EIR), helping you save money in the long run.

For example, if you have $9,000 in total debt with an average EIR of 25% and a combined monthly repayment of $500, you would pay approximately $2,500 in interest over two years.

However, if you take out a debt consolidation plan with a 17% EIR and a two-year repayment period, your new monthly instalment would be around $445, and you could save about $820 in interest costs.

If you qualify for a balance transfer credit card, you may enjoy 0% interest during the promotional period, which can last up to 12 months or more, further reducing your repayment burden.

Find out more about what debt consolidation is and the way it works in our comprehensive guide.

Repay your debt faster

Consolidating your debt at a lower interest rate can help you clear your outstanding balance sooner.

Using the earlier example, your monthly repayment drops from $500 to $445. If you continue paying $500 instead of the minimum required, you can shorten your loan tenure and reduce the total interest paid.

This approach is even more effective with a balance transfer credit card. Since these cards offer 0% interest during the promotional period, applying your savings to your balance can significantly cut down your debt before interest charges apply.

Simplify your repayments with a single monthly payment

Managing multiple debts can be overwhelming, especially with different due dates and interest rates. By consolidating your debts, you streamline them into a single monthly payment with a fixed interest rate. If you opt for a balance transfer card, you'll also enjoy a 0% interest period, making it easier to stay on top of repayments.

Beyond convenience, consolidating your debt provides a clear repayment timeline, helping you stay motivated to become debt-free.

Boost your credit score with responsible repayment

Applying for a debt consolidation loan or balance transfer card may cause a temporary dip in your credit score due to the credit check. However, making consistent, on-time repayments can improve your score in the long run.

If you're paying off credit card debt, lowering your credit utilisation ratio — the percentage of your credit limit used — can positively impact your score. A lower utilisation rate signals to lenders that you're managing credit responsibly.

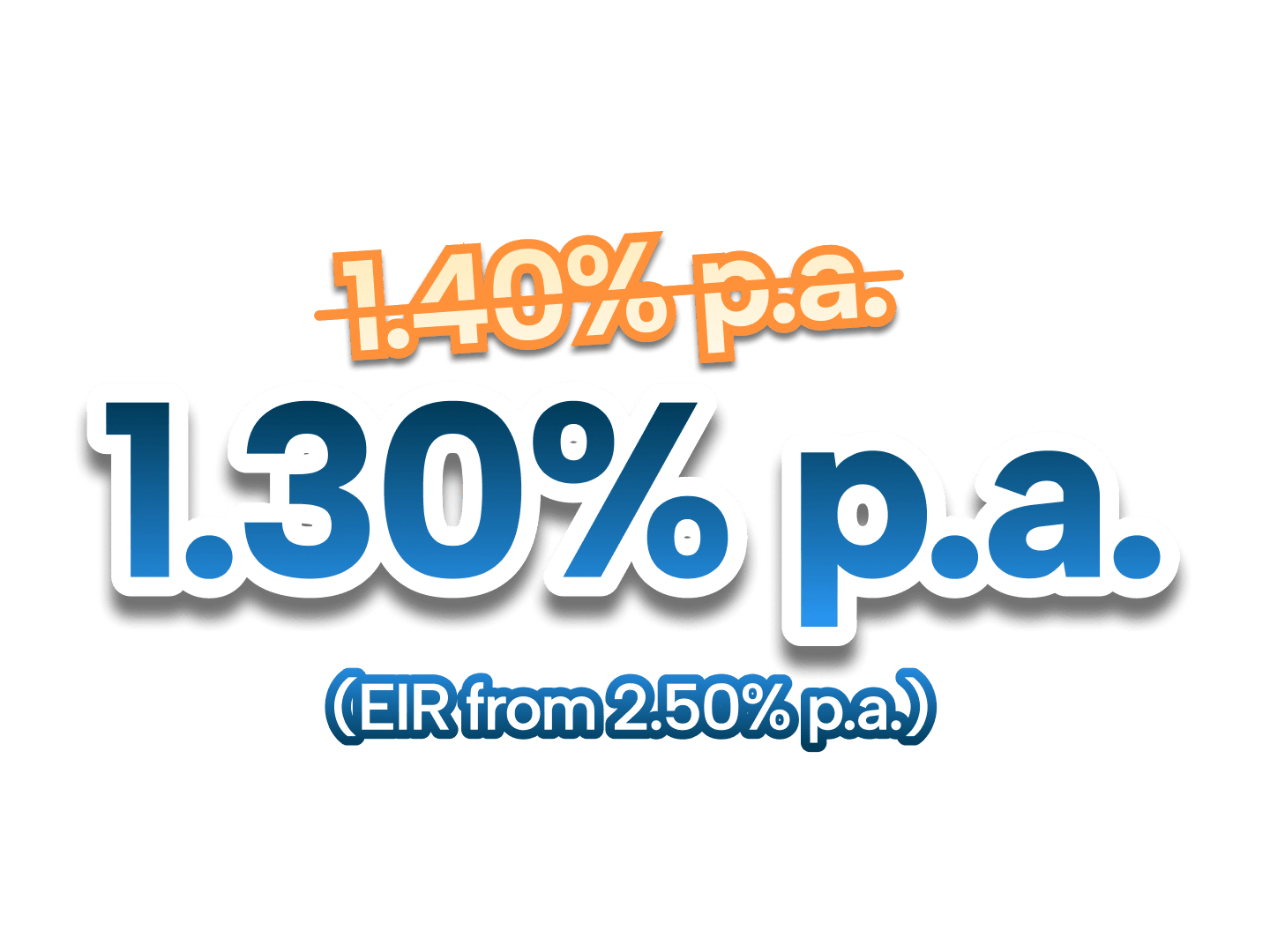

SingSaver x HSBC Personal Loan Exclusive Offer

Enjoy attractive interest rates from 1.30% p.a. (EIR from 2.50% p.a.) when you apply for HSBC Personal Loan via SingSaver. Available to new and existing customers! Valid till 2 August 2026. T&Cs apply.

Cons of debt consolidation

You may not qualify for a lower interest rate

Balance transfer credit cards typically require a good to excellent credit score, making them harder to qualify for. If your credit history isn’t strong, you may not be eligible for the most attractive 0% interest promotions.

Debt consolidation loans, on the other hand, are more accessible, with some options available for those with lower credit scores. However, the best interest rates are usually reserved for borrowers with strong credit profiles.

>> COMPARE: Top debt management plan companies of 2025

Before proceeding with debt consolidation, compare the rates offered to ensure they are lower than your existing debts. If you can’t secure a competitive rate, alternative repayment strategies like the debt avalanche or debt snowball methods may be more effective.

Debt consolidation may come with additional fees

While consolidating debt can help simplify repayments and potentially lower interest costs, it’s important to factor in additional fees that may apply. For balance transfer credit cards, a balance transfer fee — typically between 1% to 5% of the transferred amount — is usually charged upfront. Although this cost is lower than standard credit card interest rates, it can still reduce overall savings. For debt consolidation loans, lenders may charge an origination fee, which could range from 1% to 10% of the total loan amount. This fee is often included in the loan’s effective interest rate (EIR), impacting the overall cost of borrowing.

Before committing to a debt consolidation plan, compare the total savings against these fees to determine if consolidation is the right strategy for you. If the costs outweigh the benefits, alternative debt repayment methods may be a better fit.

>> MORE: Better alternatives to payday loans

Missed payments could put you in a worse financial position

Consolidating your debt can simplify repayments, but staying disciplined is crucial. Missing payments on your balance transfer credit card means that once the 0% interest period ends, any remaining balance will be subject to a higher interest rate, potentially exceeding what you were paying before.

For debt consolidation loans, late payments can result in additional charges and damage your credit score, as lenders report missed payments to credit bureaus.

Before opting for debt consolidation, ensure that your new monthly repayment is manageable within your budget for the full duration of the plan. Staying consistent with payments is key to avoiding additional financial strain.

It doesn’t solve the root cause of debt

While debt consolidation can make repayments more manageable, it doesn’t eliminate the underlying habits or circumstances that led to debt in the first place.

If overspending is an issue, consolidating your debt may free up available credit on your cards — tempting you to use them again before fully repaying your loan, which could lead to an even deeper debt cycle.

For those relying on credit cards for daily essentials like groceries or bills, it may be worth exploring alternative financial assistance options, such as government relief schemes or community support programs. Speaking to a licensed credit counsellor can also help you create a sustainable budget and explore long-term debt management strategies.

How to apply for a debt consolidation loan

Getting a Debt Consolidation Plan (DCP) in Singapore starts with comparing options from banks and licensed money lenders to find the best offer — typically the one with the lowest Effective Interest Rate (EIR) and repayment terms that fit your budget. Some lenders allow you to pre-qualify online, meaning you can check your potential interest rates and loan terms without affecting your credit score.

Here are two places you can apply:

-

Banks: Major banks in Singapore offer DCPs with competitive interest rates and longer repayment terms. However, eligibility criteria are strict — you must be a Singapore Citizen or Permanent Resident with an annual income between S$20,000 and S$120,000, and your total unsecured debt must exceed 12 times your monthly income.

-

Licensed money lenders: If you don’t qualify for a bank’s DCP, some licensed money lenders offer debt consolidation loans. These may have higher interest rates and shorter tenures, so it’s essential to compare terms before committing.

Once you’ve chosen the right loan and are ready to apply, you’ll need to gather the necessary documents to complete your application. These include a copy of your NRIC (front and back) for identity verification, your latest Credit Bureau Report to assess your credit history, and income documents as specified by the lender. You’ll also need your most recent credit card and unsecured loan statements, along with a confirmation letter for any unbilled principal balances on instalment plans if applicable. If you’re refinancing an existing DCP, a settlement notice from your original bank will also be required.

Most applications can be submitted online and take only a few minutes to complete.

⚡SingSaver x SCB CashOne Personal Loan Flash Deal⚡

Enjoy one of the market's lowest interest rates starting from 0.90% p.a. (EIR from 1.75%) plus up to S$1,800 in Cashback when you apply for Standard Chartered CashOne Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Need cash quick? Explore Singapore's best fast cash loan options.

Discover a range of fast cash loan solutions tailored to your needs. Compare interest rates, loan terms, and more from Singapore's leading lenders.

Relevant articles

Thinking of Taking on Additional Debt? 6 Things to Ask Yourself First

Stay ahead in everything finance

Subscribe to our newsletter and receive insightful articles, exclusive tips, and the latest financial news, delivered straight to your inbox.

Best personal loans in Singapore

Compare personal loan rates

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.