How to Use a Personal Loan as a Mid-Year "Financial Reset" (Without Falling Into Debt)

Updated: 13 Jul 2026

Written byAfina Najib

Senior Content Editor - Singapore

We have officially crossed the equator of the year. For many Singaporeans, June is a season of reflection—not just for lifestyle goals, but for our wallets. If your financial resolutions from January have been derailed by high-interest credit card bills, unexpected medical emergencies, or necessary home repairs, you might feel like you are dragging a heavy anchor into the second half of the year.

When your cash flow is stuck in a bottleneck, you need an intentional financial planning for midyear reset strategy to break the cycle. This is where an unexpected tool comes into play: a low-interest personal loan.

While taking on debt to clear debt sounds counterintuitive, learning how to use a personal loan wisely can actually streamline your cash flow, slash your interest costs, and give you a clean slate. Here is how to execute a successful personal financial reset safely within Singapore’s regulatory framework.

1. The Strategy: When is a Personal Loan a "Reset" and Not a Trap?

Taking a personal loan should never be about funding an impulse holiday to Tokyo or upgrading to the newest luxury timepiece. Instead, it should act as a personal loan for financial fresh start purposes, specifically targeting high-interest liabilities.

The logic comes down to math. If you are carrying a rolling balance on multiple credit cards in Singapore, you are likely being hammered by an Average Daily Interest Rate equivalent to 25.9% to 27.9% p.a.

By executing a debt consolidation personal loan strategy, you roll those high-interest balances into a single personal loan. This instantly cuts your interest rate by more than half, as competitive bank loan rates in Singapore range from 0.90% to 1.50% p.a. (flat interest rate), which translates to an Effective Interest Rate (EIR) of roughly 1.75% to 3.50% p.a.

Instead of your payments only scraping the surface of your credit card's minimum payout, your fixed monthly personal loan installments aggressively pay down both the principal and the interest simultaneously. This structural change is exactly how to reset your budget moving forward.

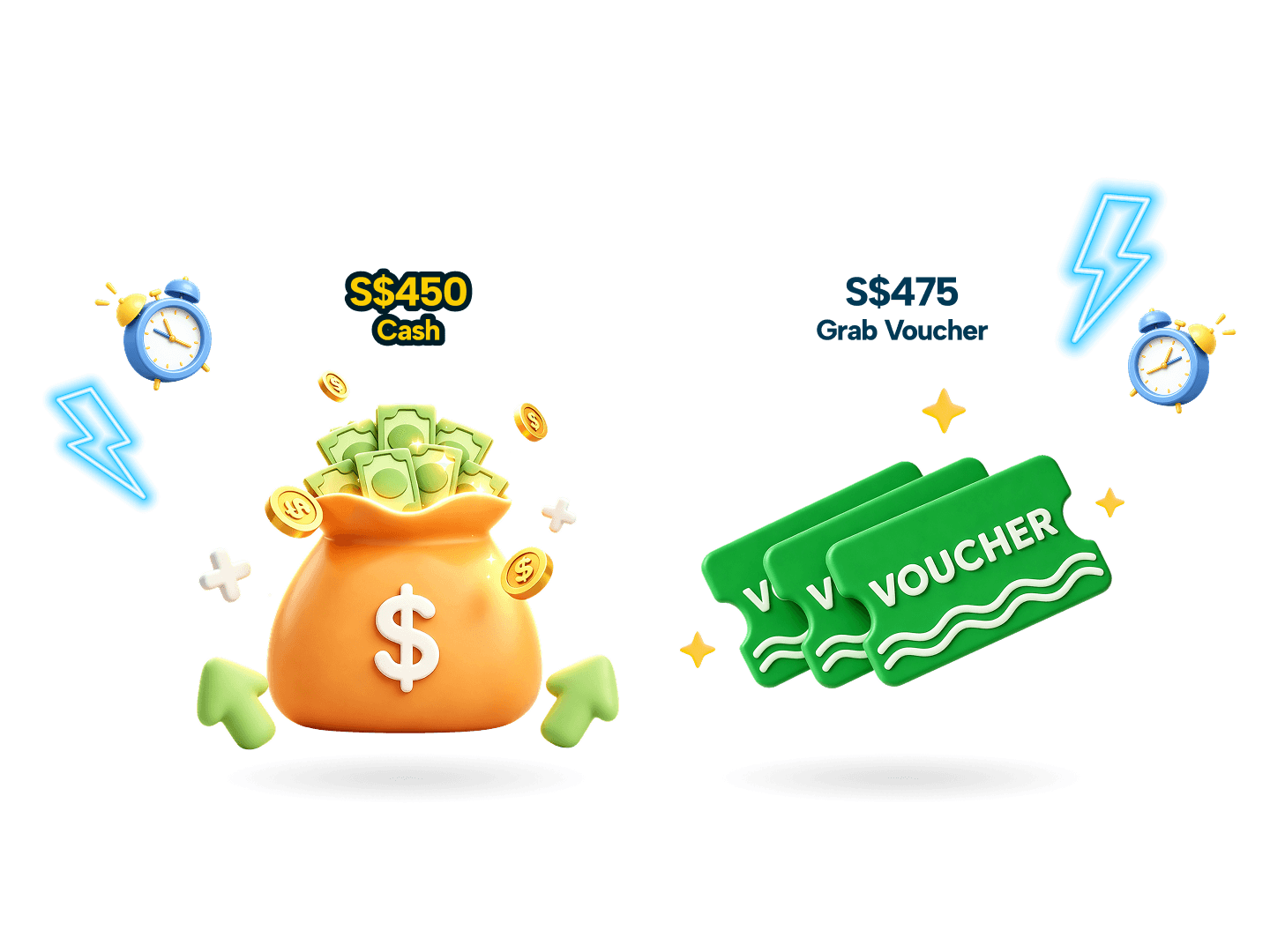

SingSaver x HSBC Revolution Credit Card Exclusive Offer

Enjoy 20X Rewards Points or 8 mpd for your travel spending with the HSBC Revolution Credit Card!

Plus, score S$450 Upsized Cash, S$500 Grab Voucher, Dyson Airstrait (worth S$799), Dyson V8 Cyclone cordless vacuum (worth S$559), or 25,000 Max Miles by HeyMax (worth S$600 in travel value) when you apply via SingSaver and fulfil promo requirements. Valid until 28 July 2026. T&Cs apply.

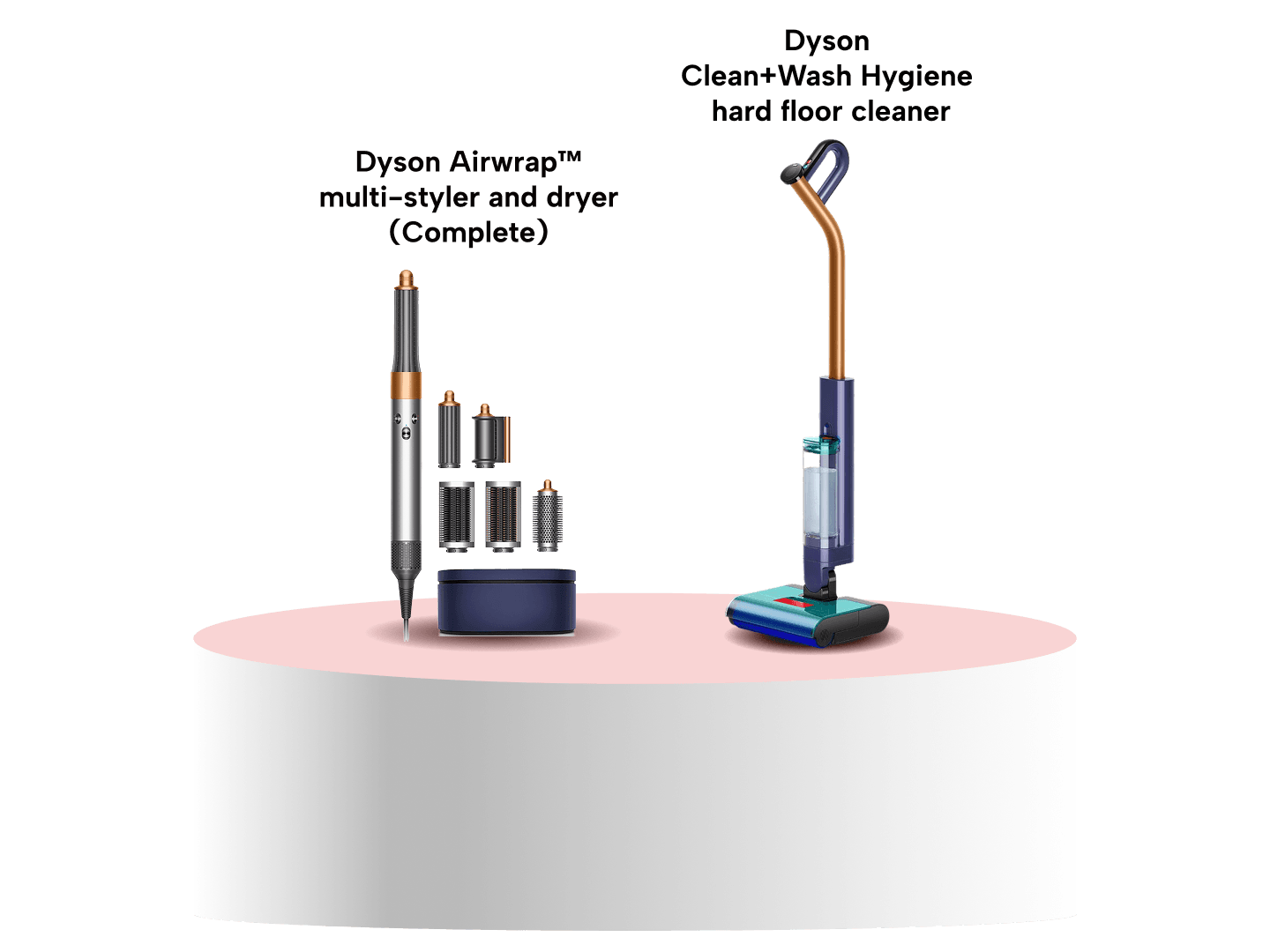

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

2. Safe and Credible Personal Loans in Singapore to Consider

To help you shop around, here are some of the safest and most competitive personal loans from major financial institutions regulated by the Monetary Authority of Singapore (MAS).

| Bank / Product | Dynamic Promotional Rates | Key Selling Point | Minimum Income (Locals/PR) |

| Standard Chartered CashOne | From 0.90% p.a. (EIR from 1.75% p.a.) | Lowest starting rate in the market; S$199 annual fee applies. | S$30,000 |

| GXS FlexiLoan (Digibank) | From 1.00% p.a. (EIR from 1.84% p.a.) | No annual or early repayment fees. Ideal for flexible extra repayments. | S$20,000 |

| UOB Personal Loan | From 1.00% p.a. (EIR from 1.93% p.a.) | $0 processing fees across all tenures; instant cash for UOB account holders. | S$30,000 |

| MariBank Instant Loan | From 1.28% p.a. (EIR from 1.92% p.a.) | Instant 10-second approval and disbursement via the Shopee-backed digital bank. | S$30,000 |

| DBS/POSB Personal Loan | From 1.48% p.a. (EIR from 3.22% p.a.) | Lower income floor for young working adults; instant digital application via MyInfo. | S$20,000 |

3. The Step-by-Step Blueprint for a Clean Mid-Year Reset

If you have decided to use a debt consolidation personal loan to achieve your personal financial reset, order is everything. Misordering these steps can hurt your credit score or result in higher borrowing costs.

4. Navigating Singapore's Borrowing Limits

Before you apply, keep in mind the strict regulatory guardrails set by the MAS to prevent consumers from over-extending themselves:

-

The Unsecured Credit Limit: Banks can generally only lend you up to 4 times your monthly salary if your annual income is below S$120,000.

-

The Industry-Wide Debt Cap: Your total outstanding balance across all unsecured credit facilities in Singapore cannot exceed 12 times your monthly income.

SingSaver Pro-Tip: If your total high-interest unsecured debt already exceeds 12 times your monthly income, a standard personal loan will not work. Instead, look into a specialized Debt Consolidation Plan (DCP)—a commercial product regulated under MAS where a single participating bank absorbs all your debts into an extended repayment plan of up to 8 years.

5. The Golden Rules: Maintaining Your Fresh Start

A personal loan provides the structural fix, but your behavioral habits dictate the long-term success of your mid-year reset. If you do not change your financial habits, you risk ending up with a personal loan installment plus newly maxed-out credit cards.

-

Freeze the Cards You Just Paid Off: The moment your personal loan funds are disbursed and used to clear your credit card balances, remove those credit cards from your Apple Pay, Google Wallet, and online shopping apps. Keep them open to maintain your credit utilization ratio, but physically lock them away.

-

Automate Your Loan Repayments: Set up a GIRO arrangement from your primary salary-crediting account directly to your personal loan account. Treat this installment as a non-negotiable expense, like your HDB mortgage or your monthly utility bill.

-

Beware of Early Repayment Penalties: If you receive a year-end bonus in December and want to clear your personal loan early, check the terms. While some digital banks like GXS do not charge penalties, traditional banks often charge an early redemption fee (often S$150 to S$250, or 3% of the outstanding principal).

The Bottom Line

A personal loan is neither inherently good nor bad—it is simply a financial tool. When used recklessly, it fuels inflation of lifestyle costs. But when deployed as a deliberate tool for a financial planning for midyear reset, it is one of the fastest ways to lower your cost of debt, consolidate your mental load, and build a reliable bridge toward your long-term financial freedom.

About the author

Afina Najib

Spending most of her young writer's phase working as a freelancer, Afina's written for various industries ranging from e-commerce, travel to health and finance. Her expertise lies in her ability to make complex subjects like finance easy to consume for everyday readers.