The Best Promotional FD Rates in Singapore for 2025 and How They Work

Updated: 16 Dec 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Promotional fixed deposit (FD) rates are time-limited offers from banks that provide higher interest returns than standard fixed deposits. These rates are crucial for Singaporean savers looking to maximise their returns in a secure, low-risk environment. By understanding how these promotional rates work, individuals can make informed decisions to grow their savings effectively.

What exactly is a promotional FD rate?

A promotional FD rate is a special, time-limited interest rate offered by banks on their fixed deposit accounts. Unlike standard fixed deposit rates, these promotional rates are typically higher and designed to attract new deposits or reward existing customers.

Banks may offer promotional FD rates to meet specific funding goals, such as increasing their deposit base or funding particular projects. Additionally, these rates can be used as a marketing tool to attract new customers or to encourage existing customers to deposit larger amounts.

Here's how they work: A bank might offer a standard 12-month fixed deposit rate of 2.5% per annum. During a promotional period, they could introduce a "special rate" campaign, offering 3.0% per annum for the same tenure.

For example, Maybank offers promotional FD deposit rates for 6-month (2.90%), 9-month (2.70%), and 12-month (2.70%) tenures on a minimum placement of S$20,000 in their time deposit account. This is a significant increase in their standard fixed deposit rates of 2.50% for the same durations.

Promotional FD rates in Singapore

Here are the current SGD promotional CD rates* offered by banks and institutions across Singapore.

|

Bank |

FD rate |

Duration |

Minimum amount |

|

Bank of China |

2.60% p.a. (Mobile banking) 2.50% p.a. (Over the counter) |

6 months |

S$500 (Mobile banking) S$10,000 (Over the counter) |

|

CIMB |

2.45% p.a. (Online promo) |

3 months |

S$10,000 |

|

Citibank |

2.40% p.a. (For new-to-bank and existing clients with Citi Priority, Citibanking or Citi Plus relationship) |

3 months |

S$50,000 to S$3 million |

|

DBS/POSB |

No current promotion |

No current promotion |

No current promotion |

|

Hong Leong Finance |

2.55% p.a. (Online via HLF Digital) |

9 months and 10 months |

S$20,000 |

|

HSBC |

Up to 2.35% p.a. |

3 months, 6 months and 12 months |

S$30,000 |

|

ICBC |

Up to 2.75% (E-banking) Up to 2.65% (Over the counter) |

1 month, 3 months, 6 months, 9 months and 12 months |

S$500 (E-banking) S$20,000 (Over the counter) |

|

Maybank |

Up to 2.45% (Online placement) Up to 2.90% (Placement in branch) |

6 months, 9 months and 12 months |

S$20,000 (Online placement) S$20,000 (Placement in branch) |

|

OCBC |

Up to 2.05% (In branch) Up to 2.15% (Online) |

9 months and 12 months |

S$30,000 (In branch) S$30,000 (Online) |

|

Standard Chartered |

2.20% p.a. |

6 months |

S$25,000 |

|

UOB |

Up to 2.30% p.a. |

6 months and 10 months |

S$10,000 |

*Information in this table updated on 14 March 2025

>>MORE: Compare the best credit card deals across different issuers in Singapore

SingSaver x Citigold Exclusive Offer

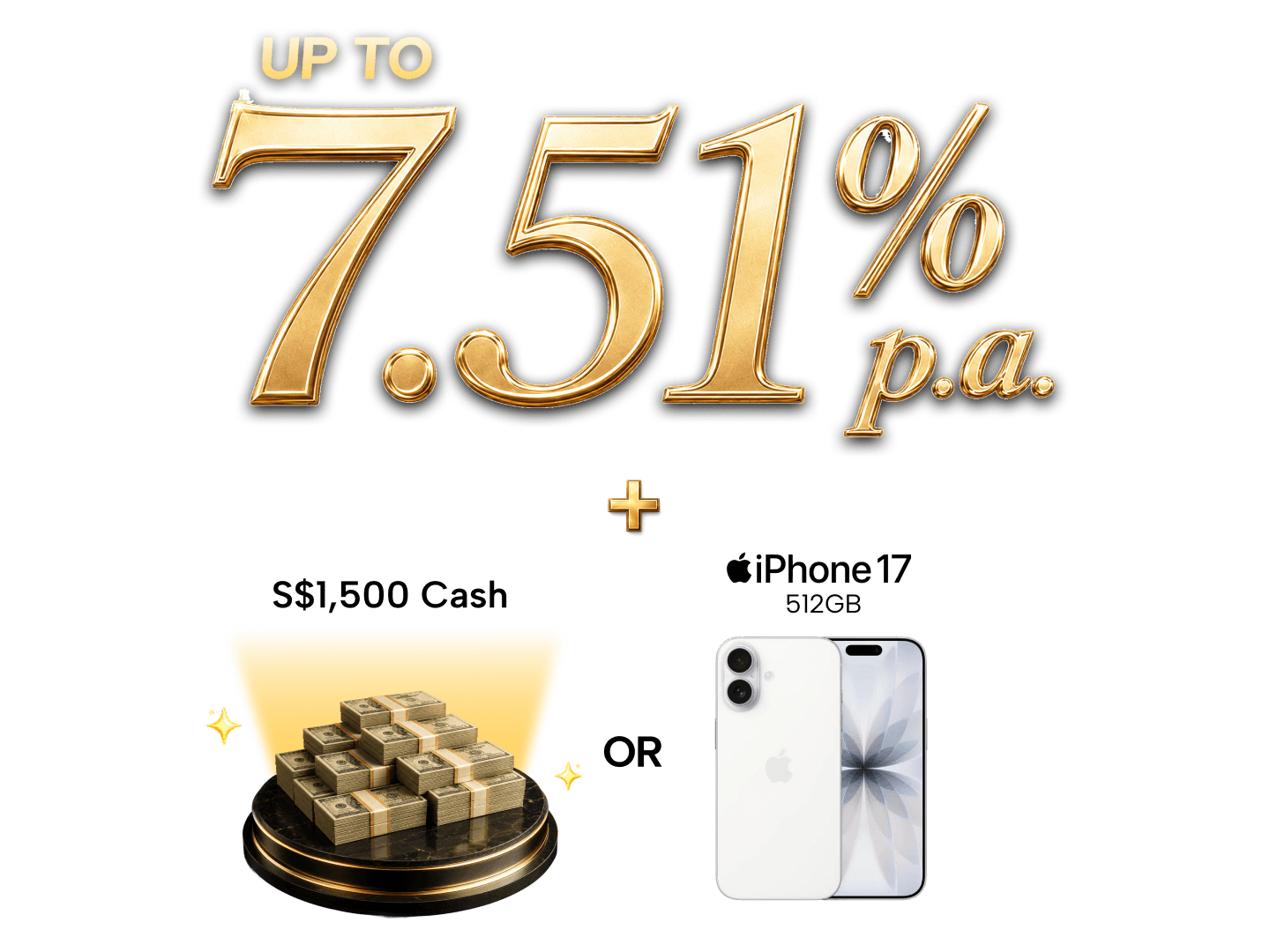

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

Is it worth going for promotional FD rates?

Promotional FD rates in Singapore can be a valuable tool for growing your savings, but it's essential to weigh the pros and cons.

Benefits of promotional FD rates:

-

Guaranteed returns: Fixed deposit rates offer a fixed interest rate for a specified period, ensuring predictable returns regardless of market fluctuations.

-

Safe investment: Fixed deposits are considered a low-risk investment, primarily because they are offered by banks regulated by the Monetary Authority of Singapore (MAS), which maintains stringent oversight of financial institutions.

-

Higher returns: Promotional FD rates generally offer higher interest rates than standard savings accounts or regular fixed deposits, maximising your earnings.

Potential downsides of fixed deposits:

-

Early withdrawal penalties: Withdrawing your funds before the maturity date may cause you incur penalties, reducing your overall returns. In some cases, you may not even have the option to withdraw.

-

Limited liquidity: Your funds are locked in for the FD's tenure, limiting your access to them in case of emergencies.

-

Opportunity cost: If interest rates rise during your FD's term, you may miss out on higher potential returns elsewhere.

Who can benefit from putting money into a fixed deposit?

-

If you have a sum of money you won't need for a specific period and want to earn a guaranteed return without the risks of the stock market, a fixed deposit is a suitable option.

-

For individuals planning for a major expense in the near to medium term, such as a child's education or a home renovation, fixed deposits provide a secure way to grow those funds with predictable interest.

-

If you are a conservative investor in Singapore who prioritises capital preservation, fixed deposits can be a reliable and low-risk investment to beat inflation.

Tips for comparing FD rates and terms:

-

Compare interest rates: Use an aggregator to look for the highest available promotional FD rates from reputable banks in Singapore.

-

Consider the tenure: Choose a tenure that aligns with your financial goals and liquidity needs.

-

Check minimum deposit requirements: Ensure you meet the minimum deposit requirements for the promotional rate.

-

Review early withdrawal penalties: Understand the penalties for withdrawing your funds before maturity.

-

Check for additional fees: Inquire about any other fees associated with the FD account.

Can banks and institutions offer higher rates without promotions?

While promotional FD rates are time-limited offers, banks and financial institutions in Singapore may also provide higher interest rates through other mechanisms.

High rates may be offered in exchange for meeting specific criteria, such as maintaining a minimum balance in a linked savings account or making regular deposits. This allows savers to earn more without necessarily relying on short-term promotional campaigns.

Additionally, some banks offer tiered interest rates, where longer-term fixed deposits yield higher returns, rewarding customers for committing their funds for extended periods.

Some banks may offer rate boosts to loyal customers as part of their relationship banking programs. This can involve offering preferential FD rates to customers who have multiple accounts or services with the bank, effectively bundling products.

For example, a customer with a mortgage, savings account, and credit card with the same bank might qualify for a higher fixed deposit rate compared to a new customer. These strategies provide avenues for savers to earn competitive returns without solely depending on promotional FD rates.

Where to find the best bank promotions

To find the best bank promotions for FD rates in Singapore, regularly check the official websites of major banks like DBS, OCBC, UOB, Standard Chartered and more. You can also utilise online comparison platforms such as SingSaver to easily compare FD rates and terms across different banks to make informed decisions and maximise your savings.

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

Make smarter financial decisions

Effortlessly compare all kinds of financial products with SingSaver. From saving accounts to credit cards, loans and more.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.