The Consequences of Defaulting on a Personal Loan: What You Need to Know

Updated: 11 Dec 2025

Avoiding loan repayments in Singapore has serious consequences that can hinder your life goals.

Navigating personal finances in Singapore can be complex, and loan repayments can become challenging during difficult times. However, understanding the consequences of defaulting on a loan is crucial due to its potentially severe and lasting financial impact.

Regardless of whether your lender is a bank or a licensed moneylender, defaulting on a personal loan will have consequences, including a negative impact on your credit score and potential legal issues down the line. Being aware of this is key to protecting your financial well-being.

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

What makes a personal loan default?

In Singapore, loan delinquency precedes default. A loan typically becomes delinquent when payment is more than 30 days past due. It then progresses to default status if payments remain overdue for a longer duration (generally 90 days or more, depending on the lender's specific policies).

Initially, missing payments on a personal loan results in late payment fees of up to $100, as well as continued interest on the outstanding balance. At this point, both banks and licensed moneylenders will usually contact the borrower to discuss repayment arrangements.

» Learn more: Dos and don’ts when getting a personal loan

The consequences of defaulting on your personal loan

Failing to keep up with your personal loan repayments can trigger several serious consequences:

Damage to your credit score

Missed payments and defaults are reported to the Credit Bureau Singapore (CBS), a key factor in determining your credit score. Consequently, defaulting on your loan will severely impair your creditworthiness.

This makes it significantly more challenging to secure future loans, credit cards, or even rent a property in Singapore. Unfortunately, these negative records can persist on your credit report for up to three years, even after the debt is fully repaid.

» Learn more: What factors affect your credit score in Singapore?

Debt collection

When a loan goes into default, lenders may engage debt collection agencies to pursue the outstanding sum. These agencies may employ various communication methods, such as phone calls, letters, and sometimes even personal visits, to contact the borrower and negotiate repayment.

It's crucial to understand that licensed moneylenders in Singapore must adhere to the Credit Collection Association of Singapore (CCAS) Code of Ethics during their debt recovery process. This means harassment by debt collectors is illegal, so if you encounter any abusive or threatening behaviour, you have the right to report it to the Registry of Moneylenders.

Legal action

To recover the defaulted loan amount, lenders have the option to initiate legal proceedings, beginning with a writ of summons being served on you. Should the court rule in their favour, this could lead to actions such as wage garnishment, where a portion of your salary is deducted for repayment, or the seizure and sale of your assets to satisfy the outstanding debt.

Furthermore, for defaults involving amounts greater than S$15,000, lenders might even pursue bankruptcy proceedings against you.

Interest and compounding penalties

Singaporean laws permit licensed moneylenders to charge interest on the outstanding loan balance, up to a maximum of 4% per month. Furthermore, they can also levy late interest charges and late fees, which are capped at a total of $60 per month.

These charges can accumulate rapidly, causing the total amount owed to escalate significantly if not addressed promptly. Therefore, proactively managing your loan obligations is essential to prevent this snowballing effect.

» Learn more: What can a debt collector in Singapore actually do?

Impact on future financial freedom

Beyond the immediate financial penalties, the consequences of defaulting on a personal loan in Singapore can severely limit your future financial freedom. This can impede housing and car loan applications, and negatively affect employment prospects, especially in the financial industry where a strong credit record is crucial.

Consequently, addressing the defaulted debt is vital for your long-term financial health and stability.

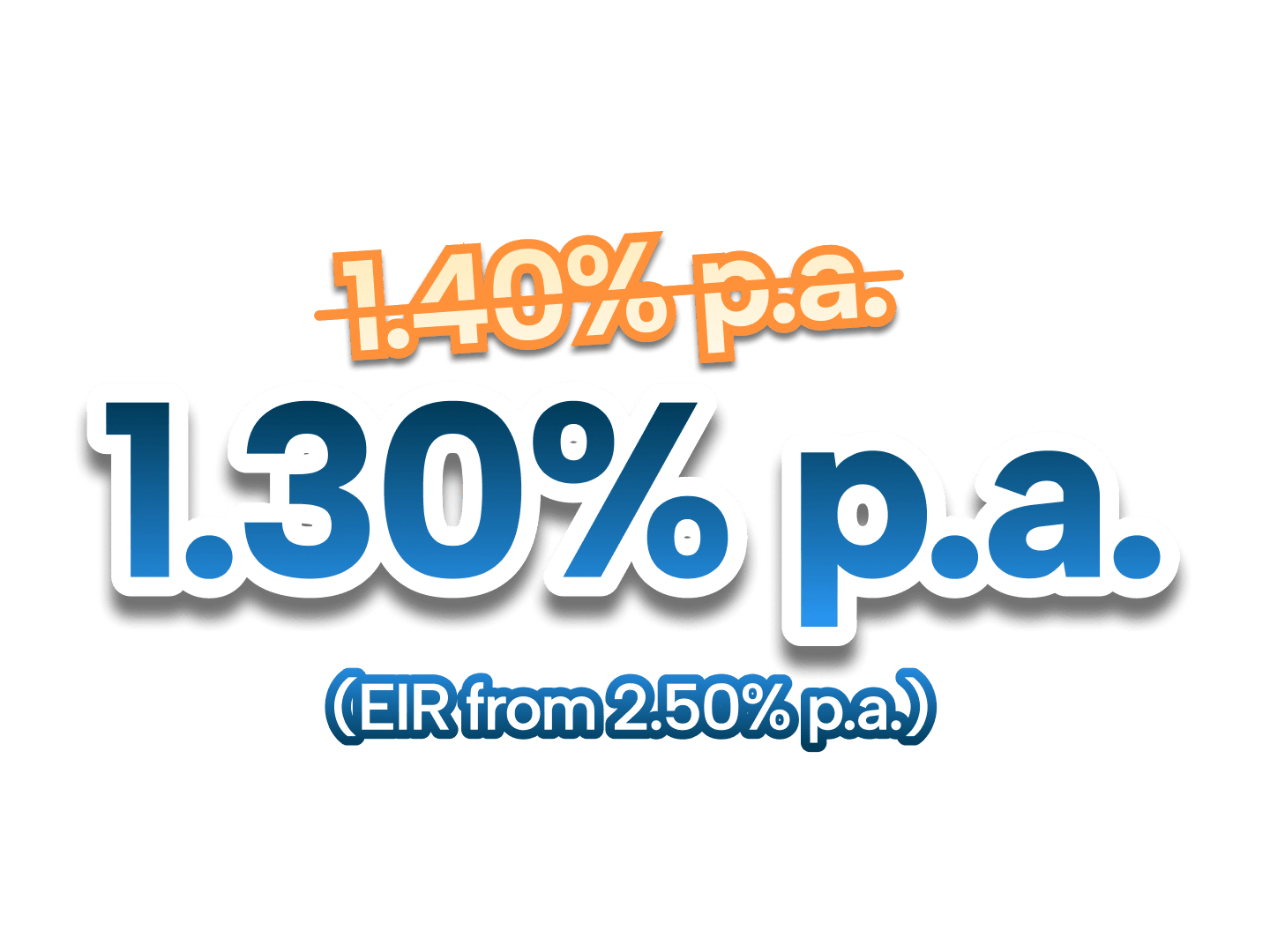

SingSaver x HSBC Personal Loan Exclusive Offer

Enjoy attractive interest rates from 1.30% p.a. (EIR from 2.50% p.a.) when you apply for HSBC Personal Loan via SingSaver. Available to new and existing customers! Valid till 2 August 2026. T&Cs apply.

How to resolve a loan default

If you find yourself struggling to repay your personal loan in Singapore, here are some steps you should take immediately:

Contact your lender immediately

If you foresee or are facing challenges with loan repayments, your immediate and most important action should be to contact your bank or licensed moneylender. Honesty about your situation is key, as they might be able to provide options such as loan restructuring or temporary payment deferment.

It's also worth inquiring about any debt consolidation plans backed by the Monetary Authority of Singapore (MAS) that may be available for unsecured loans.

Explore loan restructuring options

As mentioned earlier, loan restructuring is a potential avenue to consider. In Singapore, banks provide a Debt Consolidation Plan (DCP) that aims to help eligible borrowers manage their unsecured debts — such as personal loans and credit card balances — by consolidating them into one loan, potentially resulting in more manageable repayment terms.

Seek credit counselling

Don't hesitate to seek professional help from Credit Counselling Singapore (CCS), a non-profit organisation that offers free and confidential debt advice and assistance. CCS provides workshops on debt management, individual financial counselling, and can even help you prepare a Debt Management Programme (DMP) proposal to assist in negotiating repayment plans with your creditors.

Avoid further debt traps

It's crucial to resist the temptation of taking out new high-interest loans, such as payday loans or loans from unlicensed money lenders, to cover existing defaults. These options often come with exorbitant interest rates and fees, which can quickly worsen your financial situation.

Instead, focus on creating a strict budget, exploring ways to increase your income, or seeking temporary financial assistance from family if possible.

Take control of your debt

Simplify your repayments and reduce financial stress. Explore debt consolidation loan options in Singapore.