What Are Debt Management Plans?

Updated: 12 Dec 2025

In Singapore, debt management plans are structured programmes designed to help individuals consolidate and repay their unsecured debts, typically through a single monthly payment to a credit counselling agency, which then distributes the funds to the creditors according to an agreed-upon schedule.

If you're having difficulties repaying multiple loans and or credit card bills every month, a debt repayment plan from a non-profit credit counselling agency might offer structured assistance and guidance. A debt management plan generally has a less adverse effect on your credit score than more drastic debt payoff options, like debt settlement or bankruptcy, and can help you pay down credit card debt whilst potentially saving on interest charges.

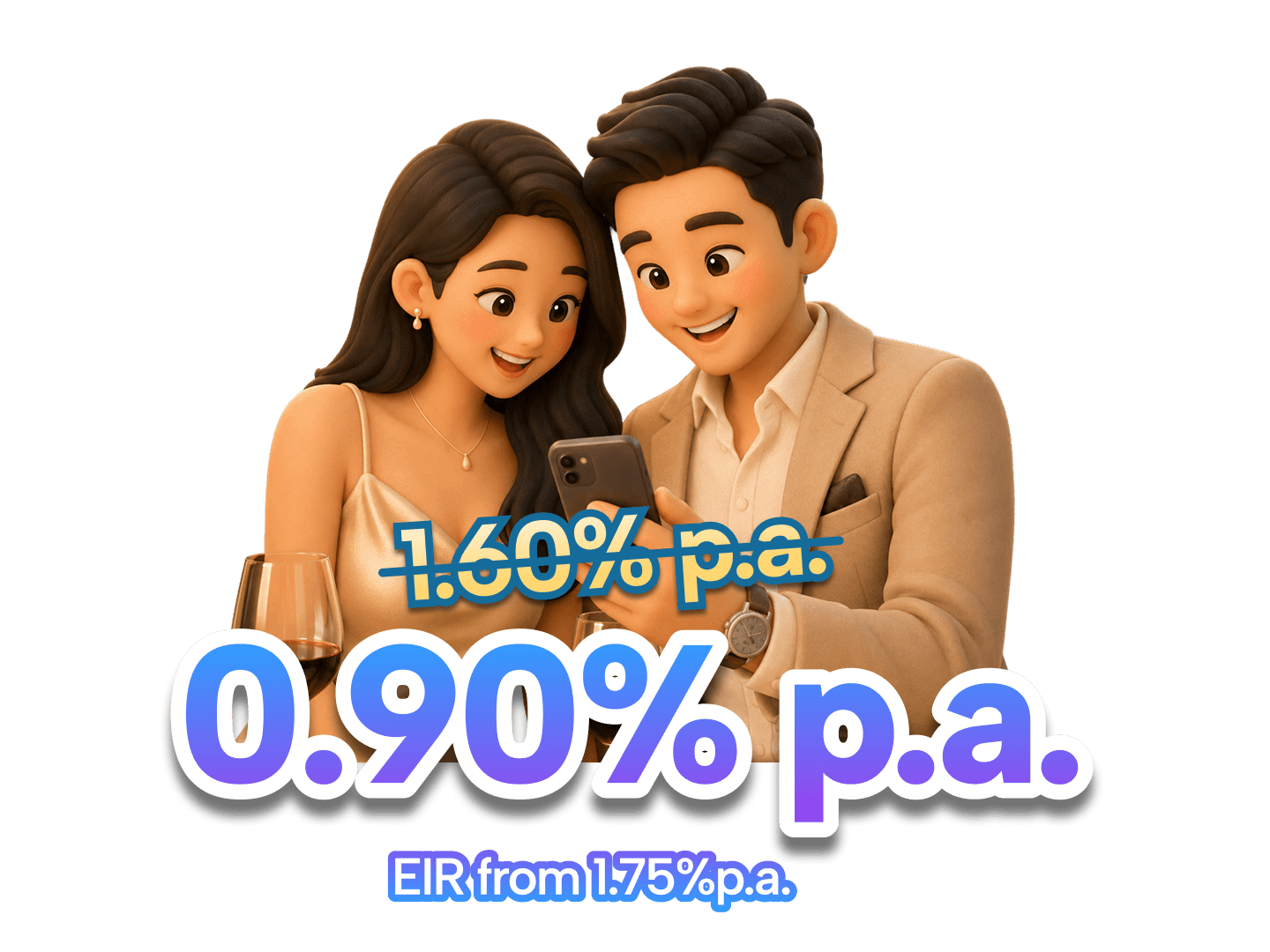

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

What is a debt management plan?

A debt management plan is an arrangement facilitated by a credit counselling agency, where they work with you to create a budget and then negotiate with your creditors to potentially lower interest rates, waive certain fees, and establish a more manageable repayment schedule for your unsecured debts. The goal is to make it easier for individuals to learn how to clear debt and how to be debt-free.

How do debt management plans work?

For those wondering how to get rid of debt or how to clear a large amount of debt, it's essential to know how debt management plans work, as understanding the process is crucial for making informed decisions about your financial recovery and learning how to achieve debt freedom.

The process begins with enrolment. A person can apply for a debt management plan in Singapore through agencies like Credit Counselling Singapore or other accredited financial institutions offering such programmes. The individual will need to provide comprehensive details of their financial situation, including income, expenses, and a complete and accurate list of their outstanding debts.

After enrolment, the next crucial step involves debt negotiation. The credit counselling agency will then negotiate with creditors to potentially lower interest rates on your debts, reduce or waive certain fees, and extend the repayment terms, aiming to make monthly payments more affordable and manageable for the individual and help them learn how to better manage and pay off their debt.

Lastly, the individual sends one consolidated monthly payment to the credit counselling agency, and the agency then distributes these payments to the creditors according to the negotiated repayment schedule, ensuring that each creditor receives the agreed-upon amount.

It is important to note that there are usually small fees for enrolling and managing a plan, which typically range from S$25-$40 per month, and these fees vary depending on the agency or institution providing the service.

Is a debt management plan suitable for you?

A debt management plan would primarily benefit those with overwhelming credit card debt or personal loans, especially when their debt-to-income ratio is significantly over 40%, indicating a high debt burden and making it challenging to learn how to clear debt.

However, there are other important factors to consider before enrolling. Here is an overview of the potential advantages and disadvantages of a debt repayment plan:

Benefits of using a debt management plan

-

Lower interest rates: Credit counselling agencies often negotiate with creditors to secure lower interest rates on your existing debts, reducing the overall amount you pay in interest charges.

-

Simplified monthly payments: You make a single, consolidated monthly payment to the agency, streamlining the often-complex bill-paying process and making it easier to track your debt repayment progress.

-

Structured, clear path to being debt-free: A debt management plan provides a structured and clear repayment schedule, typically aiming to achieve debt freedom and help you learn how to clear your debt within a defined timeframe, usually within 3-5 years.

Drawbacks of using a debt management plan

-

Requires a multi-year commitment: Adhering to a debt management plan involves a significant multi-year commitment, demanding discipline, consistent financial stability, and adherence to the agreed-upon repayment schedule.

-

No access to new credit whilst enrolled: You generally cannot open new credit accounts whilst participating in a debt management plan, which can limit your financial flexibility for new purchases or emergencies.

-

May feel restrictive: Due to the closed nature of credit accounts during the plan, it can feel restrictive, limiting your access to credit and requiring you to rely on cash or debit for expenses.

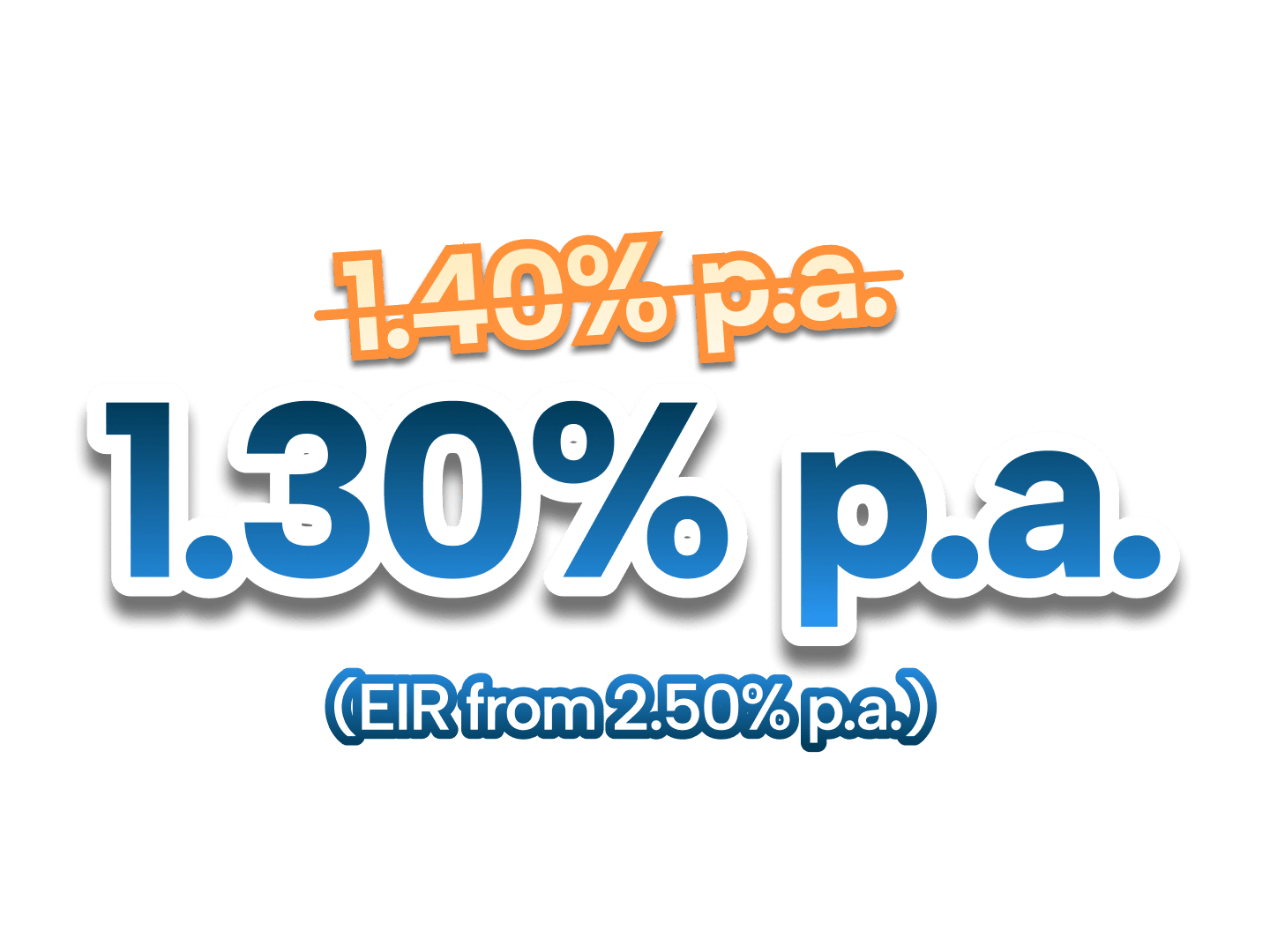

SingSaver x HSBC Personal Loan Exclusive Offer

Enjoy attractive interest rates from 1.30% p.a. (EIR from 2.50% p.a.) when you apply for HSBC Personal Loan via SingSaver. Available to new and existing customers! Valid till 2 August 2026. T&Cs apply.

Where to get a debt management plan in Singapore

In Singapore, the Debt Management Programme (DMP) is facilitated by Credit Counselling Singapore (CCS), a non-profit organisation that works with major consumer banks and credit card issuers to arrange debt repayment.

CCS aims to assist individuals in repaying unsecured debts, such as credit cards and personal loans. If a credit counsellor assesses you as having sufficient repayment capacity, CCS will prepare a DMP proposal, outlining affordable monthly instalments at reduced interest and a repayment schedule. Crucially, creditor approval is required before the commencement of payments. The general criteria to be on a DMP with CCS are:

-

Unsecured debts of $10,000 or more.

-

Unsecured debts owed to two or more creditors.

-

Assessed to have sufficient payment capacity to repay all unsecured debts fully within a reasonable time.

How debt management plans affect your credit report and CBS score

Being on a debt management plan will be reported to Credit Bureau Singapore (CBS), which maintains credit information on individuals in Singapore. Your credit report will reflect that you have been placed on a Debt Management Programme, which can have both short-term and long-term consequences for your credit score:

-

Short-term: Enrolling in a debt management plan may slightly lower your CBS score in the short term due to the closure of existing credit accounts and a temporary reduction in your overall available credit, which can affect your credit utilisation ratio and your immediate ability to learn how to clear debt.

-

Long-term: As you diligently work through the debt repayment plan, consistently making timely payments and reducing your overall debt burden, your CBS score may gradually improve over time, demonstrating responsible financial management and indicating progress in learning how to clear debt.

⚡SingSaver x SCB CashOne Personal Loan Flash Deal⚡

Enjoy one of the market's lowest interest rates starting from 0.90% p.a. (EIR from 1.75%) plus up to S$1,800 in Cashback when you apply for Standard Chartered CashOne Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Debt management plan alternatives in Singapore

If you think a debt management plan is not the right fit for your situation but are still wondering how to get out of debt, here are some options for debt relief you can consider, though each comes with its own set of risks and benefits and varying success rates in helping you learn how to clear your debt.

Debt consolidation loans

A debt consolidation loan is a type of loan where Singaporeans can combine multiple existing debts, such as credit card debt, personal loans, and other unsecured obligations, into a single new loan, often with a lower interest rate, simplifying repayment and potentially making it easier to learn how to clear your debt. Debt consolidation loans for those with poor credit may also be available, but these typically come with significantly higher interest rates and less favourable terms.

Debt Repayment Scheme (DRS)

The Debt Repayment Scheme (DRS) is a court-supervised debt repayment plan that eligible Singaporeans who are unable to manage their debts may use to restructure their liabilities, allowing them to repay their debts over a longer period under the supervision of the court and providing a structured way to learn how to clear debt.

Bankruptcy

Bankruptcy is a legal process considered the last resort for individuals with debts exceeding 40% of their income and who cannot reasonably repay them within 5 years, indicating a severe and unsustainable debt burden and making it extremely difficult to learn how to clear debt through conventional means. This is generally not the best way to manage your debt, as it carries significant long-term negative consequences for your financial future.

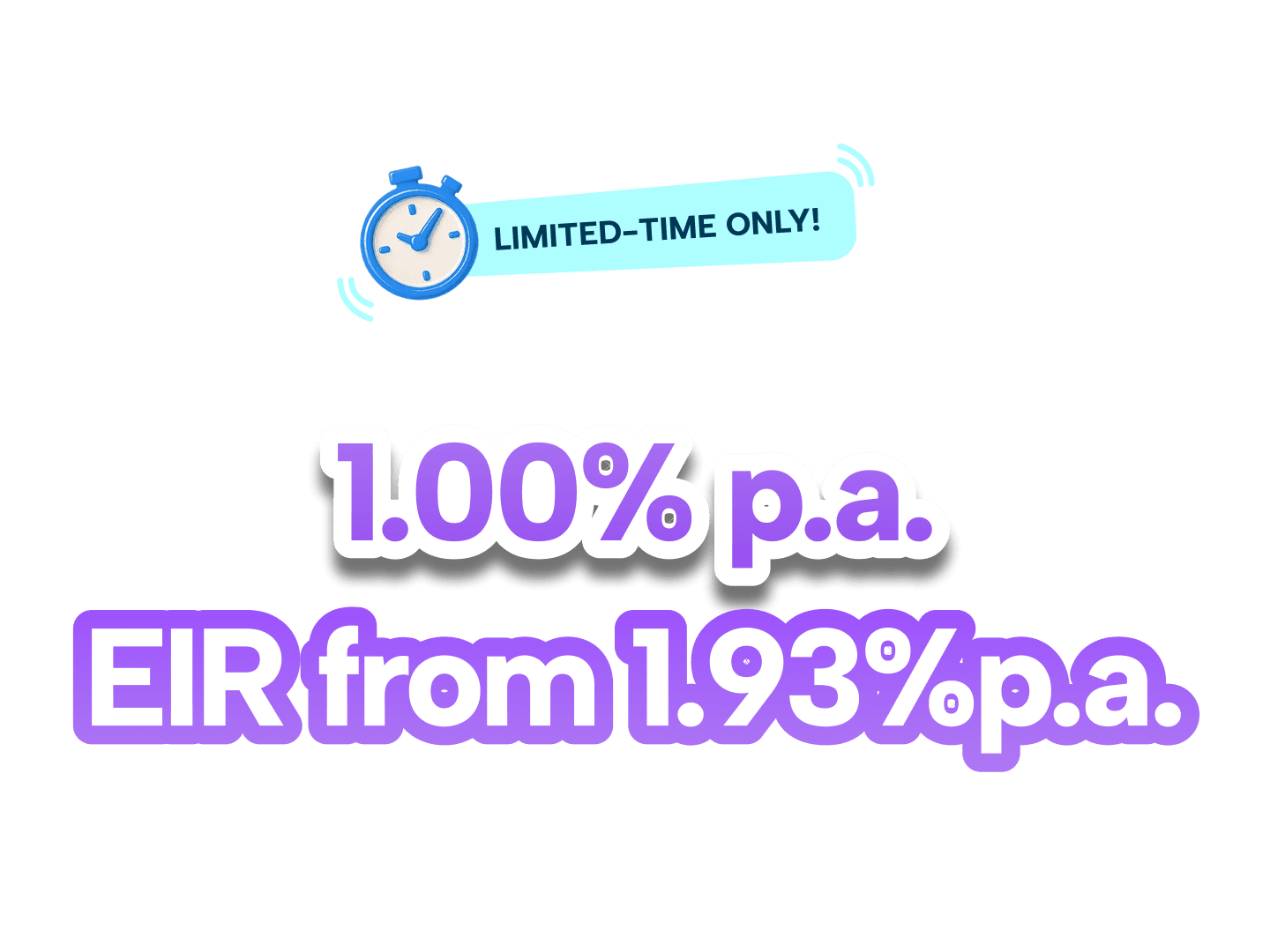

⚡SingSaver x UOB Personal Loan Flash Deal⚡

Get one of the lowest interest rates from 1.00% p.a. (EIR from 1.93% p.a.) plus up to S$1,900 in cashback and rewards when you apply for a UOB Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.