BOC NVMO Card

S$207.10

Updated: 11 Jun 2026

As life would have it, we’ll find ourselves having to pay medical bills — big and small — at some point in time. Do medical bills payment plans and hospital payment plans exist? Find out.

Team

Facing a medical emergency or managing chronic conditions can be stressful, and dealing with the accompanying invoices shouldn't add to your anxiety. When it comes to managing medical bills singapore offers a robust ecosystem of government subsidies, national insurance, and self-payment optimization strategies.

Understanding how to pay medical bills effectively can prevent you from draining your hard-earned savings. Below is the fully updated guide on the best ways to pay medical bills in singapore while maximizing your financial options.

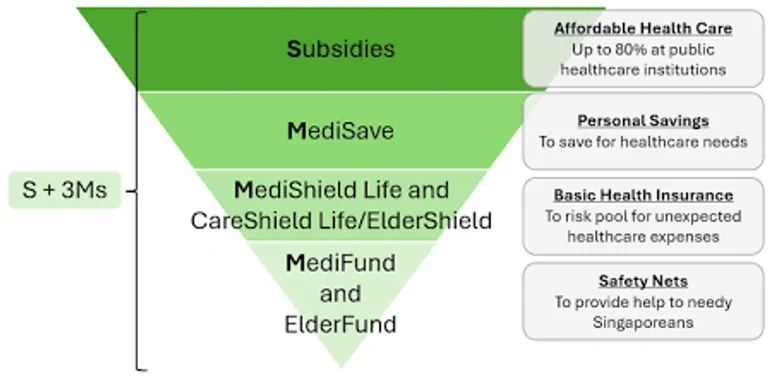

Before looking at your own wallet, Singapore’s primary line of defense against rising healthcare costs singapore is its generous framework of institutional subsidies.

Singapore's national healthcare financing framework (S + 3Ms). Source: HealthHub

Public Polyclinics and Specialists: Singaporeans receive up to 80% subsidy for inpatient treatments in subsidized wards (B2 and C class) at public restructured hospitals, and up to 70% for outpatient consultations at polyclinics and Specialist Outpatient Clinics (SOCs).

Community Health Assist Scheme (CHAS): Lower-to-middle-income households receive tiered subsidies at participating private General Practitioners (GPs) and dental clinics.

Healthier SG Chronic Tier: For those managing chronic conditions, this framework offers fully subsidized screenings and chronic medications at your designated Healthier SG GP clinic, alongside an annual subsidy allocation to lower cash outlays.

Medication Assistance Fund (MAF): For high-cost or specialized drugs not covered on the standard drug list, eligible patients can receive up to 92.5% in additional subsidies depending on their household monthly income means-test.

MediSave is a national medical savings scheme where a portion of your monthly CPF contributions is set aside. It can be used to pay for your own or your approved dependants' (spouse, children, parents, grandparents) medical expenses.

Inpatient Stays: You can use up to S$550 per day for daily hospital charges, which includes up to S$300 per day for surgical implants.

Day Surgery: A limit of up to S$300 per day applies for daily hospital charges, alongside a fixed limit for the surgical procedure based on the Ministry of Health (MOH) table of surgical codes.

Outpatient Treatments: MediSave can be deployed for costly outpatient treatments like chemotherapy (up to S$1,200 per month), renal dialysis (up to S$450 per month), and selected chronic disease management plans under the Chronic Disease Management Programme (CDMP), subject to a 15% co-payment.

When medical events escalate into large hospital bills, health insurance acts as your core shield.

MediShield Life: This is a basic, mandatory health insurance scheme administered by the CPF Board that covers all Singapore Citizens and Permanent Residents. It is structured to cover large bills in subsidized B2/C wards in public hospitals.

Integrated Shield Plans (IPs): If you prefer to stay in A/B1 class wards or private hospitals, you can upgrade your coverage via private insurers. IPs combine MediShield Life with an additional private insurance component.

Deductibles and Co-insurance: Remember that insurance policies come with a deductible (the fixed amount you must pay out-of-pocket before insurance kicks in) and co-insurance (a percentage of the remaining bill you must split with the insurer). Most modern riders cap your out-of-pocket co-payment at S$3,000 per year, provided you utilize panel doctors.

No Singaporean will be denied access to basic healthcare due to an inability to pay. If you have exhausted your MediSave, insurance, and cash options, additional safety nets exist.

MediFund: Known as the ultimate safety net, MediFund is an endowment fund set up by the government. It acts as a final line of assistance for needy Singaporean patients who face financial difficulties with their remaining subsidized bills. Medical social workers at public healthcare institutions will review individual applications to determine eligibility.

If you have to pay the remaining balance using cash, choosing the right credit card for medical bills singapore can help you recoup some costs through cashback or rewards points.

However, banks have continuously tightened their rules. Most major banks explicitly exclude transactions under Merchant Category Codes (MCC) 8062 (Hospitals), 8011 (Doctors/Physicians), and 9399 (Government Services/Public Hospitals) from earning rewards.

Here is how the top cards stack up today:

| Credit Card | Current Rewards / Cashback Rate for Medical Bills | Important Fine Print & Exclusions |

| BOC Family Card | Up to 3% Cashback on Health & Wellness | Capped at S$25 per month for this category. Requires a high minimum overall card spend of S$800 within the calendar month, otherwise the rate falls back to 0.3%. |

| UOB Absolute Cashback Card | 0.3% Cashback | Heavily nerfed. While it originally offered 1.7% unlimited cashback on all exclusions, UOB revised its terms to drop retail healthcare and public hospital transactions down to a basic 0.3%. |

| American Express True Cashback Card | 0% (Excluded) | AMEX has officially updated its terms to exclude all hospital, medical, and healthcare providers from earning the standard 1.5% cashback rebate. |

| Maybank Platinum Visa Card | Up to 3.33% Quarterly Cashback | Can still earn rewards if your medical bill matches their quarterly spending tiers. Requires consistent monthly spending of S$800 across three consecutive months to receive a S$100 quarterly rebate. |

If your bill is in the thousands and your standard cards exclude rewards, look into payment helper platforms like Citi PayAll or CardUp. While these services charge a small administrative fee (usually between 1.5% to 2.2%), they allow you to pay your hospital invoice using your favorite rewards or air miles card, helping you successfully trigger sign-up bonuses or accumulate massive blocks of miles that far outweigh the fee.

Effectively managing medical bills singapore requires a systematic approach. Always ensure you leverage public ward options to maximize baseline government subsidies, draw logically down on your MediSave limits, and keep an active Integrated Shield Plan to cushion severe medical emergencies.

When a cash payment is ultimately required at the discharge counter, look closely at your bank's latest terms or deploy payment routing tools to make sure you are optimized for every dollar spent.

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.