OCBC 360 Account: Grow Your Money with High Bonus Interest Rates

Updated: 21 Jul 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Hate jumping through hoops for greater returns on your savings? With the OCBC 360 Account, you can earn an EIR of 6.3% p.a. on your first S$100,000 with a few simple steps.

Using low-risk investment vehicles to earn some extra income has become more common than ever with the rising cost of living. With a vast array of options out there like Singapore Savings Bonds, T-Bills and Fixed Deposits, it’s easy to forget that high-yield savings accounts are another tool we can use for reliable returns.

A common misconception about savings accounts is that they invariably come with low interest rates, but high-yield savings accounts do exist. The OCBC 360 Account is just one among the handful of them out there, and you can use it to earn an EIR of up to 6.3% without breaking a sweat.

Keep reading to find out how.

>> FIND OUT: The best savings accounts in 2025

SingSaver's Best Deal Guarantee

Our Best Deal Guarantee promises you the best deal only with SingSaver. If you find a better offer elsewhere, submit a claim, and we'll reward you with double the difference. Valid till 30 September 2025. T&Cs apply.

No Personal Loans Match Your Criteria

Try adjusting your loan amount or tenure to see more options.At first glance, the sea of interest rates might look complicated, but they're actually fairly straightforward.

Unlike other savings accounts where you have to jump through multiple hoops for higher returns, the OCBC 360 Account's bonus interest rewards process is simple. Let's review how interest is earned via these high-yield savings accounts.

First, we have the DBS Multiplier Account, which requires you to credit your salary and satisfy at least one other criterion for accelerated interest on your balance. For instance, you'll need to credit your salary and spend at least S$500 to start earning 1.80% p.a. interest on your first S$50,000 balance. As for the UOB One Account, the only hard requirement is the S$500 monthly minimum spend you'll need for greater returns on your interest. This will net you an interest rate of 0.65% on your first S$75,000.

Maximise your savings with these mighty duos

Boost your savings while you spend with the right credit card and savings account combo.

The Standard Chartered Bonus$aver Account is more similar in structure to the OCBC 360 Account, since it allows you the flexibility of choosing where you'd like to earn your interest from. Both accounts award you with bonus interest even if you only carry out one action, whether it's salary credit, spending, insuring or investment. The big difference between the Bonus$aver Account and 360 Account is that the former does not reward you for saving.

So, what does earning interest with the OCBC 360 Account look like in practice? By simply crediting your salary, you’re entitled to up to an EIR 1.6% p.a. on your first S$75,000 balance. Alternatively, if you only managed to qualify for the Spend bonus, you'll still earn an extra EIR of 0.60% p.a.

How does the OCBC 360 Account work?

How the OCBC 360 Account calculates interest

|

Category |

Requirement |

% interest earned |

|

Base interest |

Open an account and transfer initial deposit of S$1,000 |

0.05% p.a. |

|

Salary bonus interest |

Credit salary of at least S$1,800 per month to account via GIRO/FAST/PayNow |

First S$75,000: 1.6% p.a. Next S$25,000: 3.2% p.a. EIR: Up to 2% p.a. |

|

Save bonus interest |

Save and increase average daily balance by min. S$500 per month |

First S$75,000: 0.6% p.a. Next S$25,000: 1.2% p.a. EIR: Up to 0.75% p.a. |

|

Spend bonus interest |

Spend min. S$500 per month using eligible OCBC credit cards |

First S$75,000: 0.5% p.a. Next S$25,000: 0.5% p.a. EIR: 0.5% p.a. |

|

Insure bonus interest |

Purchase an eligible insurance product from OCBC |

First S$75,000: 1.20% p.a. Next S$25,000: 2.40% p.a. EIR: Up to 1.50% p.a. |

|

Invest bonus interest |

Purchase an eligible investment product from OCBC |

|

|

Grow bonus interest |

Maintain an average daily balance of min. S$250,000 |

2.2% p.a. EIR: 2.40% p.a. |

Now that you have a better understanding of how you can earn bonus interest with the OCBC 360 Account, let's talk about how to maximise your returns.

How to earn more interest with the OCBC 360 Account?

The OCBC 360 Account’s tiered interest rates

|

Actions |

Maximum EIR |

|

Salary + save |

2% + 0.75% + 0.05% (base interest) = 2.8% |

|

Salary + save + spend |

2% + 0.75% + 0.5% + 0.05% (base interest) = 3.3% |

|

Salary + save + spend + insure/invest |

2% + 0.75% + 0.5% + 1.5% + 0.05% (base interest) = 4.8% |

|

Salary + save + spend + insure + invest |

2% + 0.75% + 0.5% + 1.5% + 1.5% + 0.05% (base interest) = 6.3% p.a. |

As seen above, the maximum possible EIR you can earn on your first S$100,000 is 6.3% p.a.

Before we can jump to calculating the rates, we have to address a few OCBC 360 Account basics.

Firstly, it’s important to note that regardless of your bank balance or action taken, all OCBC 360 Accounts start with a base interest rate of 0.05% p.a. This is a pretty standard base rate you’ll find across most savings accounts.

Salary crediting of at least S$1,800 monthly through GIRO/FAST/PayNow is one common denominator for the interest rates mentioned above. For most working young adults, this should be an easy target to reach, even after adjusting for take-home pay. Once you’ve hit the first S$100,000 on your bank balance, you’ll start enjoying an EIR of 3.2% p.a. If your balance is S$75,000 and below, you will receive interest rates of 1.6% p.a. The other common denominator is saving, which OCBC defines as increasing your average daily balance by at least S$500 per month.

Cash accounts to grow your money with

Find out how these alternatives to savings accounts work and whether you should park your money with them.

So, which tier of bonus interest should you aim for? Personally, we're on board with either the second or fourth one as they offer a good mix of returns and feasibility. Let us illustrate why below.

Salary Crediting + Save + Spend: Up to 3.3% p.a.

|

Account balance |

Interest (% p.a.) earned |

Maximum EIR |

|||

|

Base |

Salary |

Save |

Spend |

||

|

S$75,000 and under |

0.05% |

1.6% |

0.6% |

0.5% |

0.05% (Base) + 2% (Salary) + 0.75% (Save) + 0.5% (Spend) = |

|

S$100,000 and above |

3.2% |

1.2% |

0.5% |

||

|

EIR |

0.05% |

2% |

0.75% |

0.5% |

3.3% p.a. |

Young working adults will probably find it reasonably easy to fulfill all the criteria they need for the Salary + Spend + Save tier. Once they make their first S$100,000, they will earn an EIR of 3.3% p.a. After all, most young adults are already saving, spending and crediting their salary to a bank account each month. All you have to do to benefit from this is to consolidate your finances under the OCBC 360 Account!

Note that OCBC's minimum spend criterion of S$500 applies only when you charge the amount to select OCBC cards. Excluded transactions include fees and charges, balance transfers, cash advances, cash-on-instalment and PayLite.

SingSaver x OCBC Credit Cards Exclusive Promo

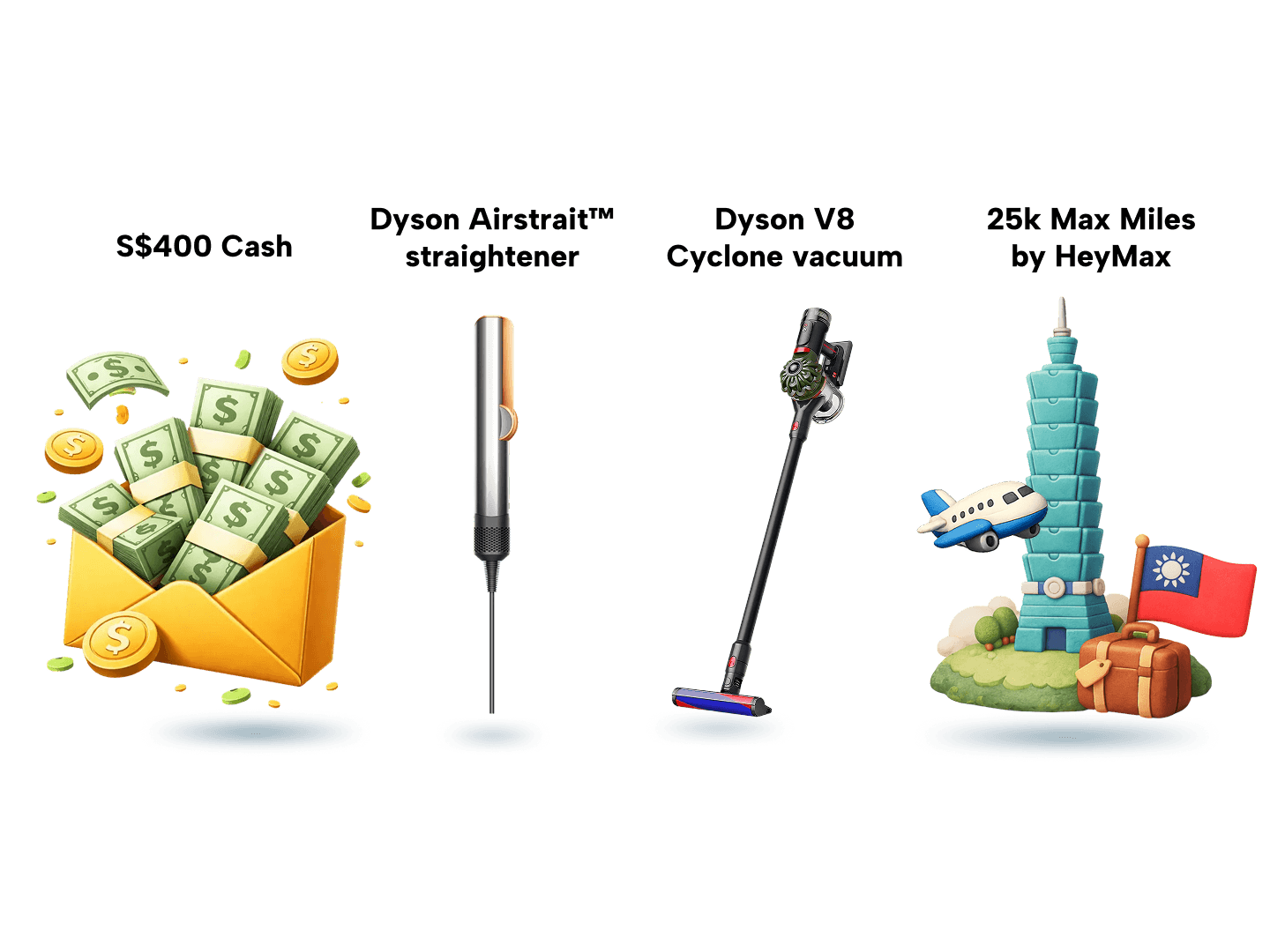

Apply for an OCBC Credit Card via SingSaver and choose from S$400 Cash, 25,000 MaxMiles by HeyMax (worth S$600 in travel value), 50,000 OCBC$ or 20,000 90°N Miles (each worth a round trip to Bali), or premium lifestyle rewards such as Dyson Airstrait, Dyson V8 Cyclone cordless vacuum, or Samsung Galaxy Buds4 Pro + S$180 eCapitaVoucher Bundle. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$80 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

OCBC credit cards eligible for Spend bonus

|

Credit card |

Benefits |

Requirements |

|

OCBC 365 Card |

5% cashback on dining worldwide and on food delivery 6% cashback on petrol 3% cashback on groceries worldwide, inclusive of online grocery orders 3% cashback on public transport and taxi + private hire rides worldwide |

Tier 1: Min. S$800 spend per month, capped at S$80 cashback Tier 2: Min. S$1,600 spend per month, capped at S$160 cashback |

|

OCBC 90°N Card |

7 miles per dollar spend on Agoda 1.3 miles per local spend 2.1 miles per overseas spend |

No min. spend required 90°N miles are not subject to any limits and never expire |

|

OCBC INFINITY Cashback Card |

1.6% unlimited cashback on all spend |

No min. spend required No cashback cap |

|

OCBC NXT Credit Card Apply Now |

Interest-free auto-instalments 1% cash rebates on monthly bills of S$1,000 or more |

Transactions between S$100-1,000 will be split across 3 months Transactions of S$1,000 or above will be split across 6 months Up to S$100 in monthly rebates |

|

OCBC Rewards Card |

15 OCBC$ (6 mpd) spend at Watsons and department stores 10 OCBC$ (4 mpd) spend in select retail categories, online and in stores Exchange OCBC$ for cash rebates, air miles, vouchers, products and more 2% bonus cash rebates for electronics purchased at Best Denki |

Earn a maximum of 15,000 bonus OCBC$ a month, up to 180,000 bonus OCBC$ a year. No cap on base OCBC$ earned. |

Salary Crediting + Save + Spend + Insure + Invest: Up to 6.3% p.a.

|

Account balance |

Interest (% p.a.) earned |

Maximum EIR |

|||||

|

Base |

Salary |

Save |

Spend |

Insure |

Invest |

||

|

S$75,000 and below |

0.05% |

1.6% |

0.6% |

0.5% |

1.2% |

0.05% (Base) + 2% (Salary) + 0.75% (Save) + 0.5% (Spend) + 1.5% (Insure) + 1.5% (Invest) |

|

|

S$100,000 and above |

3.2% |

1.2% |

2.4% |

||||

|

EIR |

0.05% |

2% |

0.75% |

0.5% |

1.5% |

6.3% p.a. |

|

Now, for those who are going all out, you only need to to perform 2 extra steps to get those sweet 6.3% p.a. interest rates. That means purchasing eligible insurance and investment products from OCBC.

OCBC offers a wide range of insurance products, such as Protection, Endowment and Investment-Linked plans. There is also no shortage of options for savvy investors. Think Unit Trusts, Equities & Treasury, Precious Metals and more. Best of all, you can invest at your convenience through the OCBC app.

Once you purchase an eligible insurance or investment OCBC product, they will net you interest rates of 1.2% p.a. each, adding up to a total of 2.4% p.a on your first S$75,000. Once your account balance is sitting at S$100,000 or above, this interest doubles to 2.4% p.a. each, which becomes 4.8% p.a. when combined. These bonus interest rates are effective for 12 months after the date of purchase.

The EIR of each investment and insurance product is 1.5% p.a.—which means you will gain an additional EIR of 3% if you purchase one of each. This is how we end up at the figure of 6.3% p.a.

Who is the OCBC 360 Account for?

Fresh grads and those new to the workforce

According to The Straits Times, the median monthly pay for fresh grads has risen from $4,317 in 2023 to S$4,500 in 2024. In other words, most fresh grads can expect to earn an entry-level salary of at least S$3,000. This easily exceeds the salary crediting requirement of S$1,800 per month which nets you interest rates of 1.6% p.a. on your first S$75,000.

Moreover, spending S$500 and above per month as a young adult in Singapore is only too easy, especially if one frequently dines out, splurges on meals or gym memberships. But of course, this largely depends on one’s budgeting and spending preferences. Assuming you also portion off a minimum of S$500 to save per month, both spending and saving will add extra interest rates of 1.10% p.a.

>> LEARN: Typical savings account minimum balances in Singapore

Professionals, Managers, Executives and Technicians (PMETs)

PMETs who have been working steadily for a number of years have in all likelihood have a decent amount of savings. They can probably afford to dabble in investments and enjoy more comprehensive insurance coverage. PMETs who hit that coveted 6.3% p.a. will reap all the benefits OCBC has to offer with the 360 Account, especially if they still have plenty left in the bank—which will naturally translate to greater returns.

Those who have amassed plenty in savings

But hey, whoever said the OCBC 360 Account is only for younger people? Those looking to retire are also likely to have accumulated a good deal of savings. They can use this to their advantage to meet the OCBC 360 Account’s Grow bonus—an EIR of 2.2% p.a. on balances of S$250,000 and above.

Frequently asked questions about the OCBC 360 Account

You need to increase your average daily balance by at least S$500 from the month before. Average daily balance is computed based on the total amount of daily balances divided by the total number of days in the month. For example, if your bank account balance in June is at S$25,000 and goes up to S$25,500 in July, you’ll be eligible for an additional Save bonus with an EIR of 0.75% p.a. You will not be eligible for this bonus if your balance stays at S$25,000, dips below that, or if you only managed to increase your balance by less than S$500.

While there is no minimum annual income requirement, you’ll need to credit at least S$1,800 per month via eligible means to earn the Salary bonus interest. Do note that salary credit via cheques, cash deposit and fund transfer do not qualify for this bonus interest. Only salary credited under GIRO/PayNow via GIRO with transaction description “GIRO-SALARY” and FAST/PayNow transactions via FAST with the code "SAL" or description “SALARY/SALA/SAL" qualify for the Salary bonus.

The OCBC 360 Account’s interest rates were adjusted as of 1 May 2025. This coincides with the UOB updating the One Account’s interest rates in the same month. Before the adjustment, OCBC 360 Account members were able to earn an EIR of 4.05% via salary credit and saving. Maximum EIR also dropped from a high of 7.65% to the current EIR of 6.3%. OCBC has also raised the average daily balance for their Grow bonus from S$200,000 to S$250,000—this used to get you an extra 2.4% p.a. but this has since been lowered to 2.2% p.a.

Is it time to break up with your Savings Account?

Sometimes, things just aren’t meant to be. Learn the telltale signs that your Savings Account is past its expiry date.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.