Best Ways to Invest Money in 2026

Updated: 13 Jul 2026

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

While investing offers a proven path to grow your wealth over time, the sheer variety of investment options available in Singapore can be overwhelming. From exchange-traded funds and high-yield accounts to bonds and more, navigating the investment landscape can be challenging, especially for those new to investing. Finding the right option that aligns with your financial goals and risk tolerance starts with careful consideration and research.

So, where should you begin?

The quick answer is: it depends. Regardless of your income, investment appetite, or age, you can access most types of investment options.

>> Compare cash management accounts and find the option that fits your investment needs.

16 best investment options this year

There are various types of investments available in Singapore, each catering to different financial goals and risk appetites. Consider these investment options this year, ranging from low-risk to high-risk alternatives:

1. High-yield savings accounts

While not technically an investment, high-yield savings accounts provide an accessible and low-risk way to grow your money in Singapore. Compared to regular savings accounts, high-yield accounts may yield higher interest rates. As such, they're generally an appealing option for those who don't want to take a significant risk yet want to earn a return on their cash.

Plus, high-yield savings accounts offer the added benefit of liquidity, allowing you to access your funds easily when needed. However, it's important to note that compared to other investment types, the returns on these accounts may be lower.

For those seeking potentially higher returns on uninvested cash, some brokerage firms offer accounts with rates comparable to high-yield savings accounts.

Best for: High-yield savings accounts are ideal for short-term savings goals or funds that you can access readily, such as an emergency fund or travel budget.

Where to open high-yield savings accounts: Banks such as OCBC, UOB, and DBS offer high-yield savings accounts. Compare rates on SingSaver to find the best deals.

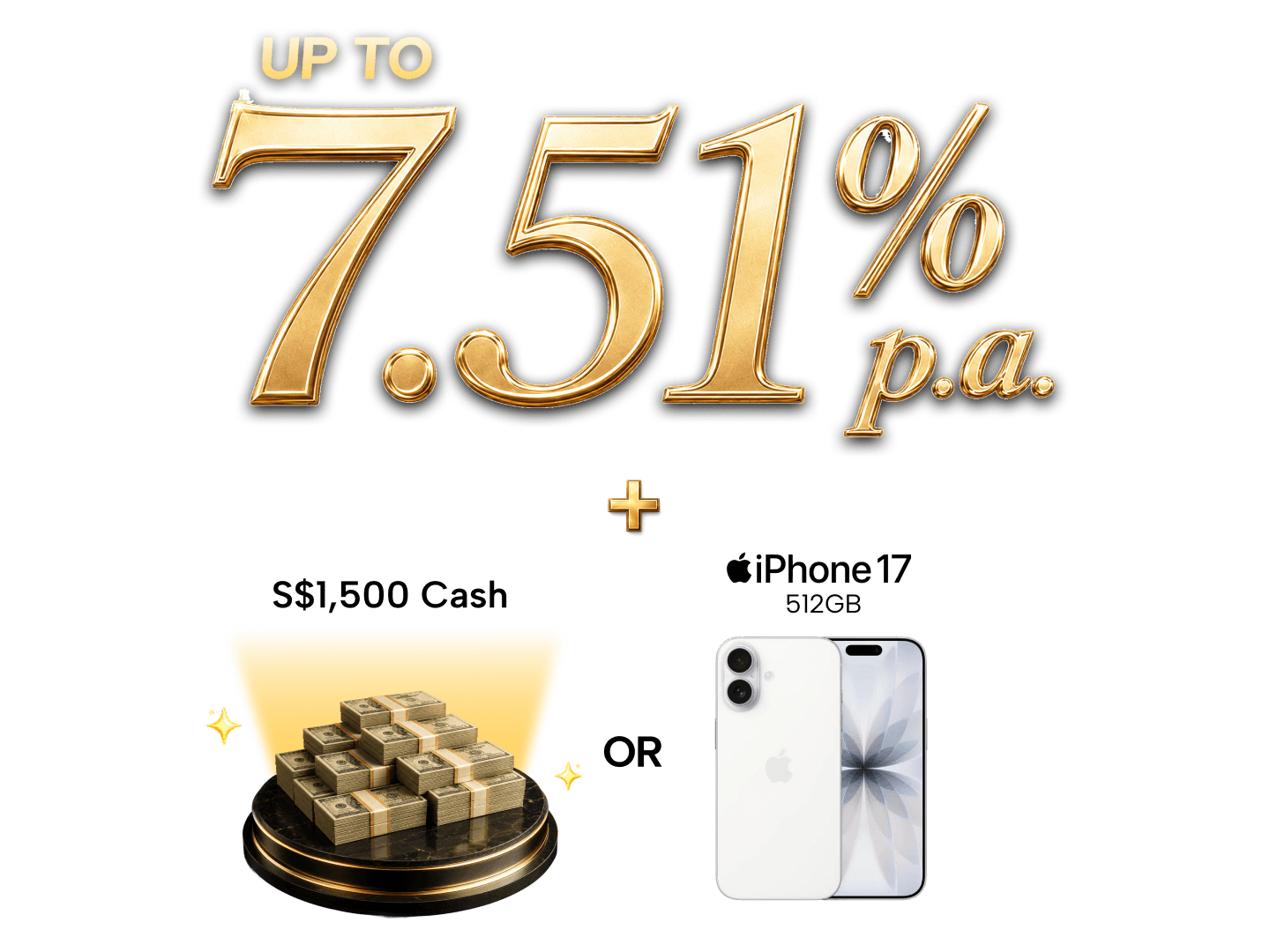

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 31 August 2026. T&Cs apply.

2. Fixed deposit accounts

Fixed deposit accounts, or FDs, can let you grow your savings with a guaranteed return. Similar to Certificates of Deposit (CDs) in other countries, this option involves depositing a fixed sum of money with a bank for a specified period, known as the lock-in period. In return, the bank offers a fixed interest rate that’s usually higher than regular savings accounts.

The interest rates on FDs vary depending on the deposit amount and the lock-in period. Generally, longer lock-in periods offer higher interest rates.

FDs provide a predictable return, making them suitable for investors seeking a safe and steady investment option with a fixed investment timeframe. However, it's important to note that early withdrawal from an FD may result in a penalty, so it's crucial to select a lock-in period that aligns with your investment needs.

Best for: Individuals with a low-risk tolerance seeking a safe and predictable investment option with a fixed investment timeframe, such as saving for a down payment on a house or a future vacation.

Where to open fixed deposit accounts: FDs are available at major banks in Singapore, including OCBC, UOB, and HSBC. However, you can compare rates and terms through SingSaver to find the best option for your needs.

3. Government bonds

Government bonds are one of the safest ways to grow your money in Singapore, making them especially appealing if you value capital preservation over chasing high returns. When you invest in a government bond, you’re essentially lending money to the Singapore Government, which is widely regarded as one of the most creditworthy governments in the world.

In Singapore, the two most common options for individual investors are Singapore Savings Bonds (SSBs) and Treasury bills (T-bills). While both are government-backed, they serve different needs depending on how long you can commit your money.

Singapore savings bonds (SSBs)

SSBs are designed for individuals looking for a low-risk, flexible investment that works well for long-term savings.

A key feature of SSBs is their step-up interest structure. Interest rates increase the longer you hold the bond, up to a maximum tenure of 10 years. If you hold the bond to maturity, you’ll receive the full long-term return. If you need your money earlier, you can redeem your investment after the first month without any penalty or loss of principal.

This makes SSBs suitable for goals that may change over time. For example, you might initially invest for retirement but later decide to redeem part of your holdings for a home renovation or your child’s education.

SSBs are also accessible to most Singaporeans, with a minimum investment of S$500.

Key features of SSBs

-

Fully backed by the Singapore Government

-

Can be held for up to 10 years

-

Flexible redemption with no capital loss

-

Suitable for long-term, low-risk savings

Treasury bills (T-bills)

T-bills are short-term government securities with maturities of six months or one year. They are typically used by investors who want to park their money safely for a fixed period while earning a return that may be higher than a regular savings account.

Unlike SSBs, T-bills do not pay interest periodically. Instead, they are sold at a discount to their face value. When the T-bill matures, you receive the full face value, and the difference represents your return.

For example, if you’re setting aside cash for upcoming expenses such as school fees or a planned holiday later in the year, a six-month T-bill allows your money to earn a return without being tied up for too long.

However, T-bills do not allow early redemption. While you may sell them on the secondary market, prices can fluctuate based on market conditions, which may affect your returns if you exit before maturity.

Key features of T-bills

-

Short investment horizon of six or twelve months

-

Lump-sum return paid at maturity

-

Minimum investment of S$1,000

-

No early redemption without market risk

How to choose between SSBs and T-bills

The right choice depends on how long you can commit your funds and whether you need flexibility.

SSBs are better suited for long-term savings with the option to redeem anytime, while T-bills are more appropriate for short-term cash that you are confident you won’t need before maturity.

Many Singaporeans use both as part of their overall savings strategy, using SSBs for long-term financial security and T-bills to manage short-term cash more efficiently.

Best for: Government bonds are ideal for conservative investors, retirees, or anyone looking for a low-risk way to grow savings while preserving capital.

Where to buy government bonds: SSBs and T-bills can be purchased through DBS, OCBC, or UOB using a bank-linked investment account or CDP account.

4. Corporate bonds

A type of fixed-income security, corporate bonds are issued by companies to raise capital for business expansion, refinancing, or operational needs. In Singapore, corporate bonds can offer higher potential returns than government bonds, but that upside comes with additional risk.

When you invest in a corporate bond, you’re lending money to a company rather than the government. In return, the company pays you regular interest, known as a coupon, and repays your principal when the bond matures. Because companies vary widely in financial strength, corporate bonds span a broad risk and return spectrum.

One of the most important factors to assess is the issuer’s credit rating. Bonds issued by large, established companies with strong balance sheets tend to be more stable but offer lower yields. On the other hand, bonds from smaller or more leveraged companies usually pay higher interest to compensate investors for taking on greater default risk.

For example, a bond issued by a government-linked company or major local bank may feel relatively stable, while a bond from a property developer or overseas issuer may offer higher yields but be more sensitive to economic conditions and interest rate changes.

Liquidity is another consideration. Unlike SSBs, corporate bonds may not always be easy to sell before maturity, especially during periods of market stress. If you need to exit early, you may have to accept a lower price than expected.

Because of these risks, many investors use corporate bonds as part of a diversified portfolio rather than relying on them as a sole investment. Bond funds and ETFs can also provide exposure to multiple issuers, helping spread risk across sectors and companies.

Best for: Investors seeking higher fixed-income returns who are comfortable taking on additional risk and have a medium- to long-term investment horizon.

Where to buy corporate bonds: Corporate bonds can be purchased through investment banks such as OCBC, Citi, and Standard Chartered, or traded on the Singapore Exchange (SGX).

5. Money market funds

Money market funds are invested in short-term, low-risk debt securities like government bonds and treasury bills. They offer investors a relatively safe and liquid investment option with a stable return. Additionally, professional fund managers handle these funds by investing in a diversified portfolio of short-term yet high-quality debt instruments.

Best for: Money market funds are ideal for investors looking for short-term, low-risk investments with a stable return. They’re also suitable for those seeking to park their funds for a short period while earning a return.

Where to buy money market funds: You can purchase these funds directly from banks or through fund platforms like Moomoo, Syfe, and CMC Markets.

>> Discover the best low-risk investments to store your emergency funds

SingSaver x moomoo Exclusive Offer

Open a Moomoo account and fund a minimum of S$2,000 to get S$130 Cash, S$150 Grab Voucher, Apple AirPods 4 without ANC (worth S$199), or 9,000 Max Miles by HeyMax (worth S$162). Plus, receive up to S$800 Welcome Rewards fulfilled by Moomoo. Valid till 31 August 2026. T&Cs apply.

6. Mutual funds

Mutual funds are a popular investment option in Singapore, offering investors access to a diversified portfolio of assets such as stocks, bonds, or other securities. These funds pool money from multiple investors, allowing you to spread risk more efficiently than investing in individual securities on your own.

Most mutual funds are actively managed by professional fund managers. This means the manager makes decisions on which assets to buy or sell with the goal of outperforming the market. While this hands-on approach can potentially deliver higher returns, it also comes with higher costs. Management fees, operating expenses, and in some cases sales charges can reduce your overall returns over time.

Mutual funds are not traded on an exchange. Instead, they are bought and sold once a day at the fund’s net asset value (NAV), which is calculated after markets close. This makes them less flexible for short-term trading, but suitable for investors who are focused on long-term growth rather than daily price movements.

Best for: Those saving for retirement or have other long-term financial goals.

Where to buy mutual funds: Mutual funds can be bought through banks like DBS, OCBC, or Citibank. Alternatively, you can use online fund platforms like Fundsupermart (FSMOne).

7. Index funds

Index funds are passively managed funds that aim to replicate the performance of a specific market index, such as the Straits Times Index (STI) or the MSCI World Index. Instead of trying to beat the market, index funds are designed to match the index’s returns as closely as possible.

Because index funds follow a rules-based approach and do not involve active stock selection, they typically have lower fees than actively managed mutual funds. This makes them a cost-effective option for investors who want long-term exposure to the market while keeping expenses low.

Like mutual funds, index funds are usually priced and traded once a day after markets close, based on their net asset value. While this means they don’t offer intraday trading like ETFs, they are still a straightforward and efficient way to gain broad market exposure without frequent buying and selling.

Some of the well-known index funds available to Singapore investors include ABF Singapore Bond Index Fund, LionGlobal Infinity Global Stock Index Fund, and Phillip SING Income ETF.

>> Check out the best bond market index funds to buy

Best for: Investors with long-term savings goals who prefer a low-cost, passive investment strategy and are comfortable with market-linked returns.

Where to buy index funds: Index funds can be purchased through fund platforms, as well as banks like DBS and OCBC.

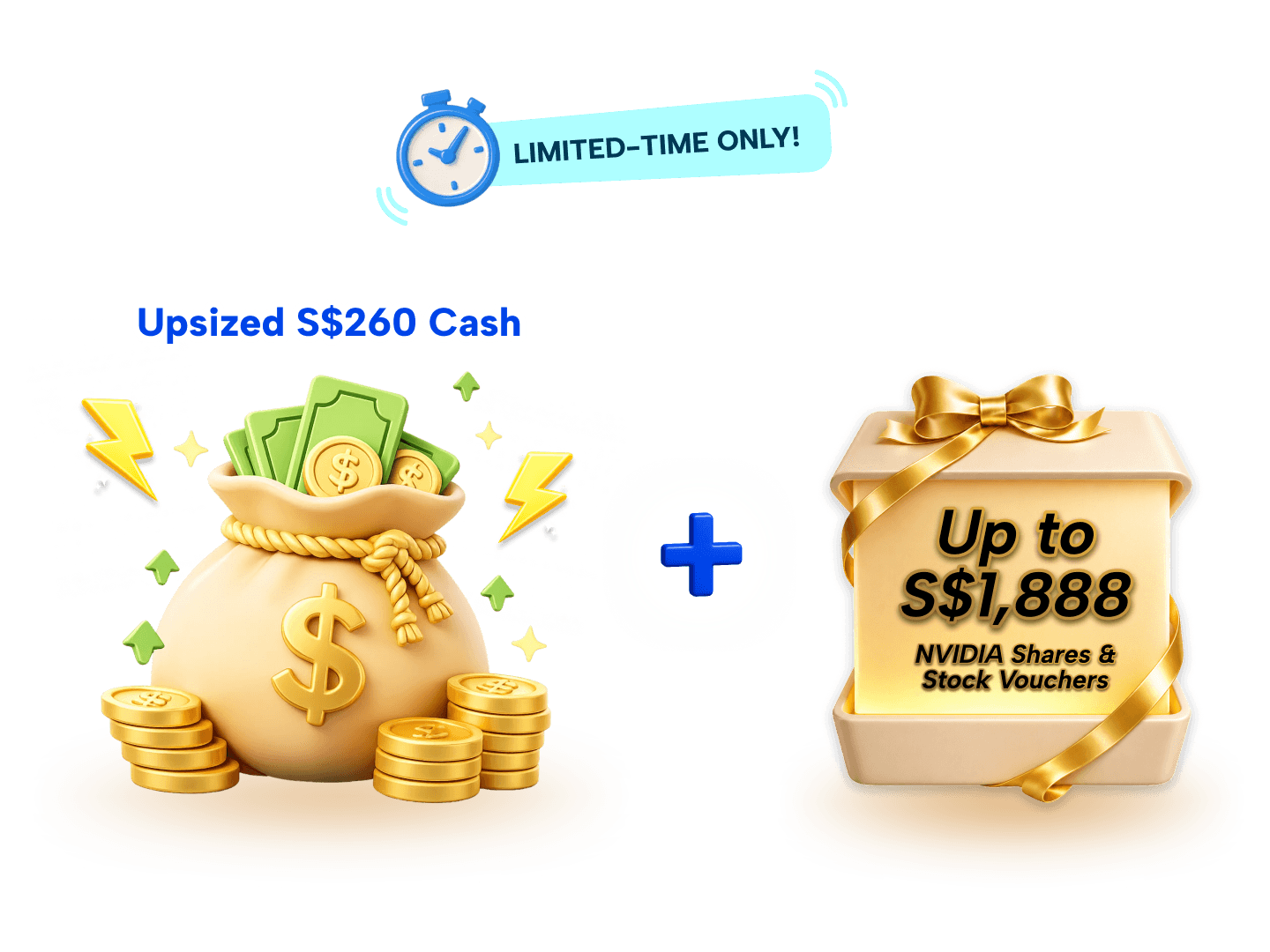

⚡ SingSaver x Webull Flash Deal ⚡

Open a Webull account and fund a minimum of SGD3,000 to receive S$110 Cash. Fund SGD10,000 to get upsized S$260 Cash, S$50 eCapitaVoucher + Samsung Galaxy Buds4 Pro (worth S$349) (total worth S$399), or 13k Max Miles by Heymax (worth S$234). Or, top up from as low as S$50 to get a Dyson Purifier Cool™ Gen 1. Valid till 4 August 2026. T&Cs apply.

8. Exchange-traded funds (ETFs)

Exchange-traded funds (ETFs) are a versatile investment option in Singapore that combine the diversification benefits of funds with the flexibility of stock trading. Like mutual funds, ETFs pool investors’ money to invest in a diversified basket of assets such as stocks, bonds, or commodities. However, unlike mutual funds, ETFs are traded on stock exchanges, allowing investors to buy and sell them throughout the trading day at market prices.

One of the biggest appeals of ETFs is diversification. With a single ETF, you can gain exposure to dozens or even hundreds of securities, reducing the risk of relying on the performance of any one stock. This is especially helpful given the sheer number of companies listed across global markets, where selecting individual stocks can be time-consuming and challenging.

ETFs are also generally cost-effective. Most ETFs are passively managed and track an index, which means they usually come with lower management fees compared to actively managed unit trusts. That said, investors should still factor in brokerage commissions when buying or selling ETFs, as these can affect overall costs if you trade frequently.

Another advantage is flexibility. Since ETFs are traded on the SGX like regular stocks, you can react to market movements in real time, whether you’re rebalancing your portfolio or taking advantage of market opportunities.

With a wide range of ETFs available in Singapore, investors can choose from products that track local indices, global equity markets, bonds, commodities, or even real estate investment trusts (REITs). This makes ETFs suitable for building a diversified portfolio across different asset classes and regions.

Some examples of ETFs available on the SGX include:

-

ETFs that track the Straits Times Index for exposure to Singapore’s largest listed companies

-

Bond ETFs that invest in government or investment-grade corporate bonds

-

REIT ETFs that provide diversified exposure to income-generating property assets

-

Commodity ETFs that track assets such as gold

To invest in ETFs in Singapore, you’ll need a brokerage account or access through a robo-advisor platform. When choosing an ETF, consider factors such as the underlying index, fees, liquidity, and whether the exposure fits your investment goals and risk tolerance.

Best for: Investors seeking low-cost, diversified investments with the flexibility to trade during market hours.

Where to buy: ETFs can be purchased through brokerage platforms such as OCBC Securities, UOB Kay Hian, and DBS Vickers.

SingSaver x Longbridge Exclusive Offer

Get S$388 Cash, S$420 Grab Vouchers, or an Apple Watch SE Gen 3 40mm (GPS) (worth S$349) + S$50 eCapitaVoucher Bundle (total worth S$399) when you apply and get approved for a Longbridge SG account, fund a min. of S$2,000, make at least 1 trade and maintain the assets for 30 days from the day after meeting the deposit criteria. Offer is stackable with Longbridge welcome promo. Valid till 31 August 2026. T&Cs apply.

9. Stocks

Stocks are one of the most well-known investment options, offering the potential for higher returns over the long term, but also coming with greater volatility. When you buy a stock, you’re purchasing a share of ownership in a company, which means your investment value rises or falls based on the company’s performance and broader market conditions.

In Singapore, many investors start with blue-chip stocks, which are typically large, well-established companies listed on the Straits Times Index (STI). These companies tend to have strong market positions, proven business models, and long operating histories, making them more resilient during economic downturns compared to smaller or less established firms.

That said, investing in stocks still requires research. It’s important to assess factors such as a company’s financial health, earnings growth, competitive advantages, and industry outlook. Diversifying across sectors, such as financial services, telecommunications, real estate, and consumer businesses, can also help reduce risk.

Stocks can deliver strong long-term growth, but prices can fluctuate significantly in the short term. This makes them more suitable for investors who are comfortable riding out market ups and downs and staying invested through different economic cycles.

>> See the best SG stocks investment brokerage accounts

Best for: Stocks are ideal for long-term investors with a higher risk tolerance and are comfortable with market volatility.

Where to buy: Stocks can be bought through the SGX or brokerage platforms like OCBC Securities and DBS Vickers.

SingSaver x CMC Markets Exclusive Offer

Open a CMC Markets account and get 2,500 Max Miles by HeyMax (worth S$45), an upsized S$20 cash via PayNow or S$40 Grab Voucher. Valid till 2 August 2026. T&Cs apply.

10. Dividend stocks

Dividend stocks are a popular choice among Singapore investors who want regular income in addition to potential long-term growth. These stocks pay out a portion of a company’s profits to shareholders, usually on a quarterly or semi-annual basis.

In Singapore, dividend stocks are often associated with blue-chip companies, particularly banks, telecommunications firms, and REITs. Many of these companies have established track records of paying consistent dividends, making them appealing to income-focused investors.

Beyond providing regular payouts, dividend stocks can also offer capital appreciation if the underlying company grows over time. Reinvesting dividends allows investors to benefit from compounding, which can significantly boost long-term returns, especially for those investing over many years.

However, dividend payouts are not guaranteed. Companies may reduce or suspend dividends during challenging economic periods, so it’s still important to assess a company’s financial strength, payout ratio, and long-term sustainability before investing.

>> Learn more about high-dividend stocks and how to invest in them

Best for: Income-focused investors seeking regular payouts, retirees looking for cash flow, or long-term investors who plan to reinvest dividends for compounded growth.

Where to buy: Dividend stocks can be purchased on the SGX or through brokerage platforms like OCBC Securities, UOB Kay Hian, or DBS Vickers. You can also invest in dividend-focused funds through unit trust platforms.

Eager to explore the investment options above? Invest through the best brokerage accounts or speak with a finance expert to determine the ideal investment plan for your individual needs and circumstances. Remember, diversification and understanding your risk tolerance are key factors in achieving your investment goals.

SingSaver x IG Markets Exclusive Offer

Get S$50 Cash, S$70 eCapitaVoucher, or 4,000 Max Miles by HeyMax (worth S$72) when you open an IG Markets account and make a min. deposit of S$1,000 and make at least 1 trade within 30 days of opening your account. Valid till 31 August 2026. T&Cs apply.

11. CPF Investment Scheme (CPFIS)

The CPF Investment Scheme (CPFIS) lets you invest a portion of your CPF savings to potentially earn higher returns than CPF’s base interest rates. CPFIS is split into two accounts, each with different rules and risk profiles.

CPFIS-OA (Ordinary Account):

After setting aside the first S$20,000 in your Ordinary Account, you can invest the remaining balance in products such as unit trusts, ETFs, bonds, and shares. This option is commonly used by CPF members who want their OA savings to work harder over the long term.

CPFIS-SA (Special Account):

The Special Account is more conservative by design and is intended for retirement savings. Investments are limited to lower-risk instruments such as Singapore Government Bonds and selected unit trusts, provided you maintain at least S$40,000 in your SA.

Important note for members aged 55 and above:

From age 55 onwards, CPF rules change. Your Special Account is closed, and SA savings are transferred to your Retirement Account (RA), up to the Full Retirement Sum (FRS). As a result, CPFIS-SA investing, including strategies commonly referred to as “SA shielding”, is no longer applicable for members aged 55 and above. Any remaining CPF savings beyond the RA are held in the Ordinary Account and are subject to CPFIS-OA rules instead.

While CPFIS can enhance long-term growth potential, investments still carry market risk and product fees. It works best as part of a long-term retirement strategy rather than a short-term return play.

Best for: CPF members below age 55 with a long runway to retirement who are comfortable taking measured investment risk to potentially improve long-term outcomes.

Where to start: CPFIS investments are accessed through CPF-approved agent banks (DBS, OCBC, UOB) and CPFIS-approved products offered by brokers and fund platforms.

12. Supplementary Retirement Scheme (SRS)

The Supplementary Retirement Scheme (SRS) is a voluntary programme designed to help you save for retirement while potentially lowering your taxable income. Contributions qualify for tax relief, and withdrawals are only partially taxable if spread over 10 years from the statutory retirement age.

SRS money can be invested in a wide range of products, including stocks, bonds, SGS, SSBs, fixed deposits, unit trusts, ETFs, and insurance products. That flexibility makes SRS useful if you want to build a diversified, retirement-focused portfolio beyond CPF.

Contribution caps (annual): S$15,300 for Singaporeans and PRs, and S$35,700 for foreigners.

Best for: Taxable-income earners who want tax relief while investing for retirement.

Where to start: Open an SRS account with the operator banks (DBS, OCBC, UOB), then invest through approved platforms/products.

13. Cash management accounts

Cash management accounts are investment-style accounts that typically place your cash into low-risk instruments such as money market funds and short-term bonds. They’re designed to offer better yield potential than a regular savings account, while keeping your funds relatively accessible.

Common reasons investors use cash management accounts include:

-

Higher yield potential than standard savings (though not guaranteed)

-

High liquidity (typically easy deposits/withdrawals)

-

Useful for short-term parking of funds (e.g., emergency funds or “waiting to invest” cash)

Some platforms may also allow SRS funds, depending on the provider and product structure.

Best for: Investors who want to park cash more efficiently than a regular savings account while keeping access relatively flexible.

Where to start: Offered by brokerages and investment platforms (availability and structure vary by provider).

SingSaver x Chocolate FInance Exclusive Offer

Get up to S$120 Cash via PayNow or up to S$130 Grab Vouchers when you apply for a Chocolate Finance account via SingSaver, fund a min. of S$1,000 in your first deposit and maintain the amount for 60 days from date of account opening. Valid till 2 August 2026. T&Cs apply.

14. Robo-advisors

Robo-advisors are digital platforms that use algorithms to build and manage investment portfolios based on your goals, timeline, and risk tolerance. Most robo-advisors invest using diversified ETFs, and they handle rebalancing automatically.

Key benefits include:

-

Lower fees than traditional advisory (varies by platform)

-

Built-in diversification through ETF portfolios

-

Convenience and automation (goal-setting, recurring deposits, auto-rebalancing)

As with any market-based investment, returns are not guaranteed, and portfolios can decline during market downturns.

Best for: Hands-off investors who want a diversified portfolio with automated management and are investing for medium- to long-term goals.

Where to start: Robo-advisors are available via their apps/platforms; compare fees, portfolio options, and minimums before choosing.

15. Real estate investment trusts (REITs)

REITs let you invest in a portfolio of income-generating real estate assets without buying property directly. In Singapore, S-REITs are listed on the SGX and cover sectors like retail, office, industrial/logistics, and hospitality.

Why investors consider REITs:

-

Diversification across multiple properties (and sometimes regions)

-

Income potential through distributions (REITs typically pay out most of their taxable income)

-

Liquidity (listed and tradable like stocks)

-

Useful as an income-oriented portion of a broader portfolio

However, REIT prices and distributions can be affected by interest rates, financing costs, occupancy/rent trends, and property sector cycles.

Best for: Investors seeking income potential and portfolio diversification who can tolerate market fluctuations.

Where to start: Buy S-REITs via SGX brokerage accounts, or consider REIT ETFs for diversified exposure.

16. Cryptocurrencies

Cryptocurrencies are digital assets secured by cryptography and commonly built on blockchain technology. They can be highly volatile, and prices may swing sharply based on market sentiment, regulation, macro conditions, and project-specific risks.

Common ways people gain exposure include:

-

Cryptocurrency exchanges (buy/sell/trade crypto assets)

-

Digital wallets (storage; some allow in-app purchases)

-

DeFi platforms (higher complexity and risk; smart contract and platform risks)

-

Crypto index funds/ETFs (where available, typically via regulated products)

-

Investing in blockchain/crypto-related companies (indirect exposure via equities)

Because risk is significantly higher than most traditional asset classes, crypto exposure is usually kept as a small slice of a diversified portfolio (if used at all).

Best for: Investors with a high risk tolerance who understand the volatility and are comfortable with the possibility of substantial losses.

Where to start: Use reputable, regulated providers where possible, and prioritise security practices (e.g., strong authentication, withdrawal controls).

Best brokerage accounts for online stock trading

| Products | Min. Commission Fee (SG Stocks) | Min. Deposit | Min. Commission Fee (US Stocks) | Min. Trading Fee | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

S$0 | S$1500 | US$0 | 0 % | |||||||||

S$0 * | S$3000 | US$0 * | 0 % | |||||||||

S$0 | S$2000 | US$0 | 0.03 % | |||||||||

| S$0 | S$2000 | S$0 | S$0.99 /order | ||||||||

US$1 | S$1000 | US$1 * | N/A | |||||||||

S$50 | S$0 | N/A | 0 % | |||||||||

S$0 | S$500 | N/A | 0 % | |||||||||

How to shape an investment strategy that fits you

After reviewing the investment options available in Singapore, the next step is to figure out how they fit together to suit your personal situation. A good investment strategy isn’t just about returns; it’s about choosing an approach you can stay comfortable with over time.

Your preferences around involvement, risk, and time horizon all influence what a sensible portfolio looks like for you.

Hands-on or hands-off: finding your investing approach

One of the first things to consider is how actively you want to manage your investments.

Some investors prefer to be closely involved, researching markets, tracking news, and making frequent portfolio adjustments. This approach offers greater control but also requires time, discipline, and the ability to make decisions during volatile periods.

Others prefer a more automated experience. By using diversified funds, professionally managed portfolios, or digital platforms, these investors aim to grow their money without needing to monitor markets constantly. This approach can be more practical for those with limited time or less interest in day-to-day decision-making.

Neither style is inherently better — what matters is choosing one that aligns with your lifestyle and level of confidence.

Selecting investments based on involvement level

The way you prefer to invest often determines the products you gravitate towards.

Investors who favour a lower-maintenance approach may choose broad-based funds that follow market indices or diversified portfolios designed for long-term growth. These options tend to focus on consistency and cost efficiency rather than trying to outperform the market.

Those who enjoy a more active role may build portfolios around individual stocks or actively managed funds that pursue specific themes or strategies. While this can increase return potential, it also introduces greater variability and requires closer monitoring.

Many investors blend both approaches, using diversified funds as a foundation, while selectively adding higher-conviction investments on top.

Considering full-service investment solutions

For some investors, managing investments independently isn’t the priority. Full-service options such as relationship-managed banking or advisory platforms offer portfolio construction, monitoring, and access to a wider range of investment opportunities.

These services can be useful if you value professional guidance and convenience, but they often come with higher fees. It’s worth weighing whether the additional support justifies the cost relative to your needs and portfolio size.

Understanding how much risk you’re comfortable taking

Risk tolerance isn’t just about numbers — it’s also about how you react emotionally to market swings. Knowing where you stand can help prevent panic-driven decisions during periods of volatility.

Higher-risk investing styles

Investors with a higher tolerance for risk often prioritise growth and are willing to accept larger fluctuations in portfolio value. This may involve allocating more capital to equities, emerging markets, or alternative assets.

While this approach can deliver strong long-term gains, it also requires the ability to stay invested during sharp market declines without making reactive decisions.

Lower-risk investing styles

More cautious investors tend to focus on protecting capital and maintaining stability. Their portfolios may include a greater proportion of bonds, income-generating assets, or lower-volatility investments.

Although growth may be slower, this approach can provide peace of mind and more predictable outcomes, especially for those approaching major financial milestones.

Building a balanced risk profile

Many investors fall somewhere in between. By combining growth-oriented and defensive assets, it’s possible to pursue long-term returns while managing downside risk. The exact balance should reflect both your financial goals and your comfort with uncertainty.

Matching investments to your time horizon

How long you plan to stay invested plays a major role in determining suitable investment choices.

Investing with a longer runway

If your goal is many years away, short-term market movements tend to matter less. A longer horizon gives investments more time to recover from downturns, which can make growth-focused assets more appropriate despite their volatility.

Investing for nearer-term goals

When your timeline is shorter, flexibility and capital preservation become more important. Investors saving for near-term expenses often prioritise stability over growth to reduce the risk of needing funds during a market dip.

Deciding how to deploy your money

Beyond what you invest in, how you invest can also affect outcomes.

Investing a lump sum gives your money maximum exposure to the market from the start, which can be beneficial over long uptrend periods but increases the risk of poor timing.

Spreading investments over time through regular contributions can help smooth out entry points and reduce emotional stress. While this may limit upside in rising markets, it can make investing more manageable for many people.

Why diversification still matters

Diversification helps reduce reliance on any single investment, sector, or market. By spreading your portfolio across different asset types and regions, you lower the impact of individual setbacks.

While diversification doesn’t remove risk entirely, it can help create more consistent performance over time and reduce the likelihood of major losses tied to a single exposure.

Ultimately, the goal is to build a portfolio that supports your financial objectives — and one you’re comfortable sticking with through both calm and turbulent markets.

Relevant articles

8 Best ETFs for February 2025 and How to Invest

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.