Can You Pay a Mortgage With a Credit Card in Singapore?

Updated: 11 Dec 2025

The answer is yes, but it may not be straightforward or always the most financially sound choice. Our guide will cover the potential costs and drawbacks to consider before taking your next steps.

Saver-savvy tips

-

Direct mortgage payments with a credit card are generally not accepted by banks and financial institutions in Singapore. Some banks or card issuing companies may also have restrictions against paying for mortgage on their cards.

-

Third-party services offer a workaround, but typically come with associated fees.

-

Whether it's a financially prudent option depends on carefully weighing the rewards against the costs.

Is paying your mortgage by credit card even an option in Singapore?

It's a common assumption that you should be able to pay your mortgage with a credit card, similar to other large expenses such as weddings or home renovations, so that you can accumulate rewards or gain some short-term financial breathing room.

However, the reality in Singapore is different.

Direct credit card payments are not a standard option for home loan payments. Moreover, banks and financial institutions in Singapore typically do not allow homeowners to directly use a credit card to pay their mortgage installments.

One key reason is due to regulations by the Monetary Authority of Singapore (MAS). MAS has regulations in place that discourage banks from actively promoting or facilitating residential property payments via credit cards. This is partly to prevent the accumulation of unsecured debt for such substantial sums.

However, while direct payments are restricted, third-party platforms like CardUp and ipaymy offer workarounds on a technicality. The downside is that these options are typically not free and eligibility is not guaranteed. Even when you register for an account on these platforms, eligibility for using a specific credit card to pay your mortgage depends on the terms and conditions set by your credit card issuer, your mortgage lender, and the card network (Visa, Mastercard, Amex).

Therefore, while there are ways to indirectly pay your mortgage with a credit card, it's crucial to understand the limitations and potential costs involved before proceeding. This will help you ensure you’re making the right decision for your financial health and financial future.

Saver-savvy tip

Still have questions about mortgage and home ownership in Singapore? Our useful articles might be able to help:

How to use a credit card for mortgage payments in Singapore

It's important to reiterate that your mortgage lender (e.g., HDB or a bank) in Singapore will not directly accept credit cards as a payment method for your home loan.

You need to use indirect methods and third-party services like CardUp or ipaymy as an intermediary instead.

How it works is that you authorise the platform to charge your credit card for the mortgage amount, and then the platform transfers the funds to your mortgage lender via a method the lender accepts (typically a bank transfer). You can usually set up recurring payments or make one-time mortgage payments with the linked credit card.

Notably, these platforms typically charge a processing fee for their service. For CardUp, this is 2.6% for Singapore-issued cards and 3.3% for internationally-issued cards. This may vary with promotions and offers.

However, be aware that not all credit cards will earn rewards (e.g., miles or cashback) when used to pay your mortgage. Always check your credit card terms and conditions carefully to ensure you’re not missing out on lost rewards. There might be restrictions on what transactions qualify for rewards.

If you choose to use a credit card to pay your mortgage this way, it's also absolutely crucial to pay off your credit card bill in full and on time each month. This will help avoid incurring high interest charges, which can quickly negate any potential benefits.

Saver-savvy tip

Just because you can use a credit card for a big payment doesn’t mean you should. Find out the pros and cons of making big payments with credit cards to make the best decision for your bank account.

On the hunt for a new credit card?

Browse and compare the best credit cards in Singapore in 2025 with in-depth card reviews.

What to consider before using a credit card for your mortgage payments in Singapore

Before deciding to pay off your mortgage in Singapore with a credit card, you should carefully evaluate whether it's a financially sound strategy for you. Here are key factors to consider:

Are the rewards worth the fees?

It's tempting to earn credit card rewards (like miles or cashback) on a large monthly expense like your home loan. However, the processing fees charged by platforms like CardUp can easily outweigh the value of those rewards.

For instance, if your monthly mortgage payment is S$3,000 and the processing fee is 2.6%, you'll pay an extra S$78 per transaction. This amount may seem small but it adds up quickly over time!

The only scenario where racking up these additional charges might make sense is if you're trying to meet a minimum spending requirement to qualify for a substantial credit card sign-up bonus and the value of that bonus significantly exceeds the processing fees, or if your credit card has an exceptionally high (and rare) earn rate.

However, even then, it's crucial to check your credit card's terms and conditions, as some issuers in Singapore may exclude payments made through third-party billers from earning rewards.

Don’t overlook interest charges

A major risk of using a credit card for mortgage payments is the potential for incurring high interest charges. Credit card interest rates in Singapore are typically quite high, often ranging from 26% to 28% per annum.

If you don't pay your credit card bill in full and on time each month, the interest charges will quickly erode any potential benefits from rewards and can lead to significant debt accumulation.

This risk is especially concerning with recurring monthly payments like your mortgage, as the interest can compound over time.

How it affects your credit score

In Singapore, your credit score is calculated by credit bureaus such as Credit Bureau Singapore (CBS). While credit scores aren’t as widely-considered here compared to countries like the United States, for example, they can still impact services and products like bank loan applications.

One of the factors that influences your credit score is your credit utilisation ratio: the amount of credit you're currently using compared to your total credit limit.

Using your credit card to pay a mortgage will likely consume a large portion of your available credit, increasing your credit utilisation ratio. If your credit utilisation ratio exceeds 30%, it can negatively impact your credit score. This is especially true if you already carry other balances on your credit card.

For example, if you have a credit limit of S$10,000 and your mortgage payment is S$3,000, using your credit card for this payment would immediately increase your utilisation ratio to at least 30%.

If you choose to use a credit card to pay your mortgage, consider requesting a credit limit increase from your card issuer to help manage your credit utilisation ratio and minimise any potential negative impact on your credit score.

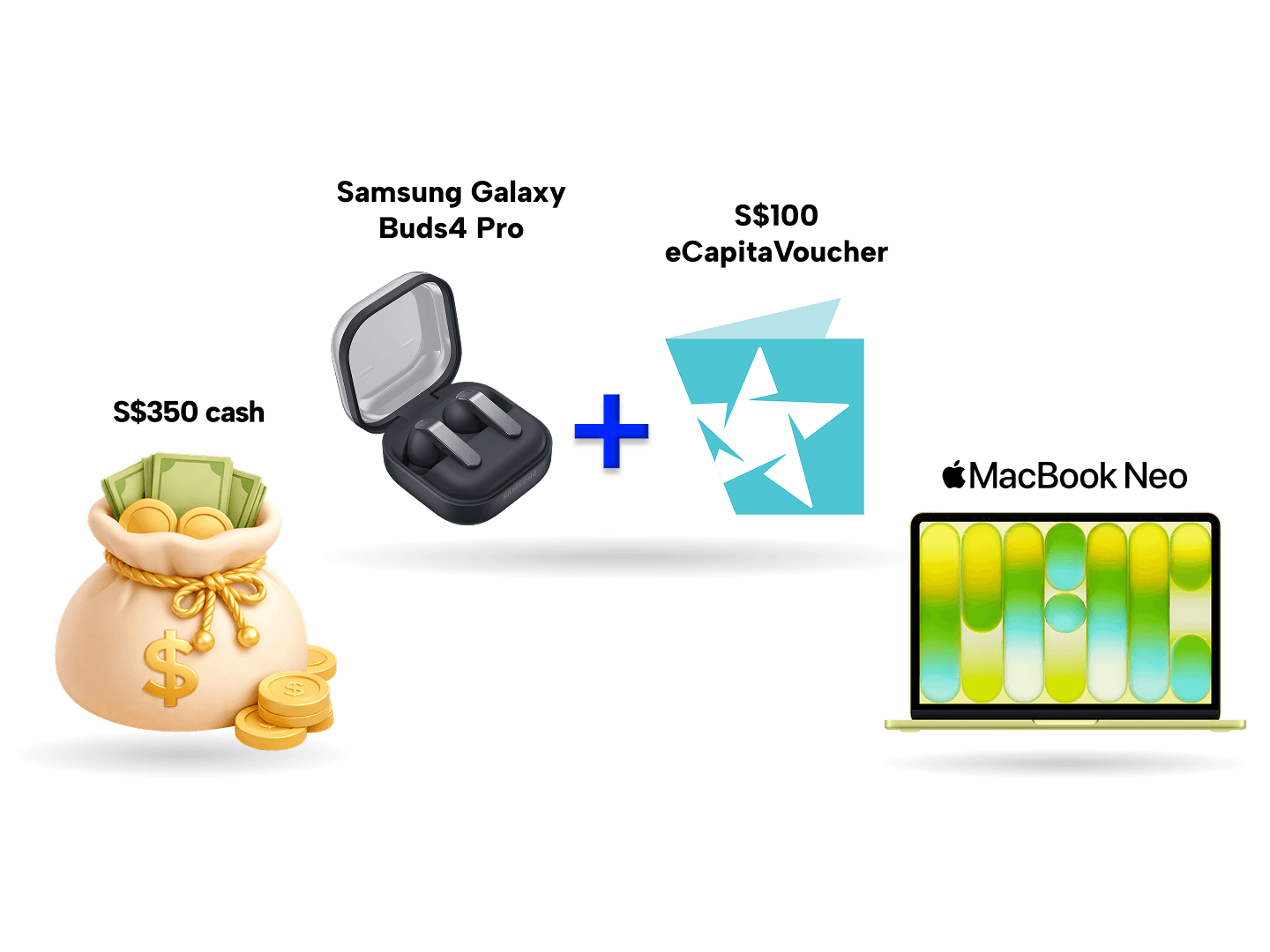

SingSaver x SCB Simply Cash Card Exclusive Offer

Get a Samsung Galaxy Buds4 Pro + 100 eCap bundle (worth S$449) or up to S$370 when you apply for a Standard Chartered Simply Cash Credit Card via SingSaver, spend a minimum of S$800 within 30 days of card approval, and apply for one of these products: EasyPay, Bonus$aver Account, CashOne, or CCFT. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

So, is it ever worth paying an extra fee to use a credit card for mortgage payments?

In most cases, it's best to avoid paying extra fees for transactions. However, there might be specific situations where it could be worth considering in Singapore.

For example, if you're trying to reach a minimum spending requirement to earn a valuable credit card sign-up bonus, using a platform like CardUp to temporarily pay your mortgage with a credit card might be worthwhile. The value of the bonus should significantly outweigh the processing fees and you can change back to a different payment method like GIRO deposits or bank transfers once you’ve earned your bonus.

In very limited circumstances, if you're facing a temporary cash flow issue and need a short-term delay in paying your mortgage, this method could provide a brief window. However, this is NOT a long-term solution and should be avoided if possible.

In most other scenarios, the processing fees will likely negate any potential benefits, making it financially unwise to pay mortgage payments with a credit card.

Challenges of paying your mortgage with a credit card in Singapore

Even when using third-party services, several challenges and potential pitfalls exist when attempting to pay your mortgage with a credit card in Singapore.

This is mostly due to the difficulty in aligning expectations between three different entities: card networks, card issuers, and mortgage lenders.

Card networks like Visa, Mastercard, and Amex each have their own rules regarding what types of transactions are allowed.

A card issuer like your bank or credit union may have specific restrictions on using your card for certain types of payments. Some credit card issuers in Singapore may even explicitly exclude mortgage payments or loan repayments from earning rewards or may disallow such transactions through third-party platforms. For example, some banks might not allow you to earn miles or cashback on CardUp transactions.

Additionally, mortgage lenders (be it HDB or a bank) do not tend to directly accept credit card payments.

Successfully using your credit card to pay your mortgage requires all three entities’ policies and agreements to align, which can be extremely difficult. If any of the involved parties (card network, card issuer, mortgage lender) rejects the transaction, your mortgage payment may fail. This can lead to late fees, penalties from your lender, and potentially a negative impact on your credit score or credit card debt even before you notice something’s gone wrong.

Therefore, it's essential to thoroughly investigate the eligibility and terms and conditions with all three parties before attempting to pay your mortgage with a credit card.

Is it a good idea to pay your mortgage with a credit card?

While it's technically possible to pay your mortgage with a credit card in Singapore through platforms like CardUp, it's generally not recommended as a regular practice. It's only worth considering in very specific situations and with careful, deliberate financial planning.

Here's a summary of the key considerations:

Only consider if you pay off your credit card in full every month: This is crucial to avoid high interest charges that will negate any potential rewards.

Rewards must outweigh fees: The value of any rewards earned must be significantly higher than the processing fees charged by the third-party platform.

Avoid if you're already using a significant portion of your credit limit: Increasing your credit utilisation ratio can negatively impact your credit score and overall financial health.

Before you commit to paying your mortgage with a credit card, carefully assess your budget and cash flow to ensure you can comfortably repay your credit card bill in full each month. If you're already struggling to manage your credit card balance, using it for mortgage payments is likely to worsen your financial situation.

Other risks include overspending and accumulating credit card debt due to the ease of using a credit card, damage to your credit score due to high credit utilisation or missed credit card repayments, and the likelihood that reward points will not compensate for the processing fees.

Overall, using a credit card for mortgage payments in Singapore might be suitable for financially disciplined individuals seeking to maximise a specific rewards goal (e.g., a sign-up bonus) but is generally not a recommended long-term strategy, especially for those who have difficulty managing their credit card balance.

Frequently asked questions about paying your mortgage with a credit card

While it's technically possible to pay your mortgage with a credit card in Singapore, it's not a direct, easy, or convenient process. You'll need to use a third-party service that charges your card and then transfers the funds to your mortgage lender.

-

Find a reputable third-party payment service in Singapore that accepts credit cards for mortgage payments (e.g., CardUp, ipaymy).

-

Verify with your credit card issuer that they allow this type of transaction and whether you'll earn rewards.

-

Set up your mortgage payment through the chosen service, carefully noting the associated processing fees.

-

Ensure you have a plan to pay your credit card bill in full and on time to avoid interest charges or credit card debt.

-

You might earn credit card rewards (if the transactions are considered eligible by your card issuer), but the processing fees will likely outweigh the value of those rewards. Always calculate the potential earnings against the fees to determine if it's worthwhile.

Deciding on your next credit card?

Explore the best travel, cashback, rewards, and everyday spend credit cards (and more) in Singapore!

Airport Lounge Access, Bonus Air Miles!

- 12 complimentary lounge passes per statement year at over 1,400 airport lounges worldwide, for you and a guest.

- Earn 2.4 air miles per S$1 spent in foreign currency, and 1.4 air miles per S$1 spent locally.

- Waiver of miles conversion fees.

- Travel with peace of mind with up to S$1,000,000 Travel Personal Accident Insurance coverage.

- 24/7 UOB Visa Infinite Concierge for your banking and lifestyle needs.

- Airport lounge

- Bonus air miles

- Overseas rebate

- Non-waivable annual fee.

- High S$120,000 min. annual income requirement.

- Annual Fee required