Certified Financial Planner (CFP): What Is It, and How to Become One

Updated: 10 Dec 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

The financial information provided here is solely for educational purposes. SingSaver does not offer financial advisory or brokerage services, and does not provide recommendations for specific investments.

Saver takeaways

-

Becoming a certified financial planner in Singapore requires proficiency in investment, insurance, tax and estate planning, all tailored to the local financial landscape.

-

CFPs in Singapore are held to a fiduciary standard, meaning they must act in their clients' best interests, ensuring ethical and client-focused advice.

-

On average, it takes significant time and resources to become a CFP in Singapore, reflecting the rigorous standards upheld by the FPAS.

SingSaver Exclusive Offer

⚽ Make your move this World Cup season. Compare top brokerage deals on SingSaver, then apply to score exclusive upsized rewards this June. Make every play count. 📈🏆 T&Cs apply.

Make the most of every trade. 📊

Set up your account in under 5 minutes, explore your options with ease, and enjoy exclusive rewards as you grow your portfolio. 🪙🏆T&Cs apply.

What exactly is a CFP?

In Singapore, a CFP, or certified financial planner, represents a financial advisor who has attained one of the most rigorous certifications in the field of financial planning. This designation signifies a professional's commitment to excellence and ethical practice, making them highly qualified to provide comprehensive financial advice. To earn the CFP certification in Singapore, candidates must meet stringent requirements set by the Financial Planning Association of Singapore (FPAS).

These requirements include several years of experience related to financial planning, passing a comprehensive CFP certification exam and adhering to a strict code of ethics. Notably, CFPs in Singapore are held to a fiduciary standard, meaning they are legally and ethically obligated to act in their clients' best interests at all times.

This fiduciary duty distinguishes CFPs from other financial advisors who may not have the same level of commitment to client-first principles, making them a trusted choice for individuals seeking reliable and unbiased financial guidance in Singapore.

>> Read: More than just savings — Five tips for proper wealth planning

What do certified financial planners do?

In Singapore, certified financial planners provide comprehensive financial planning services. They guide individuals and families towards achieving their financial goals by assessing financial situations and developing personalised plans. CFPs offer advice on investments, retirement, tax and estate planning, ensuring clients make informed decisions.

CFPs in Singapore also specialise in risk management, helping clients protect assets through insurance and mitigation strategies. They stay updated on financial regulations and market trends, providing timely advice.

Furthermore, they assist in navigating Singapore’s unique financial landscape, including CPF planning and property investments, tailoring strategies to local regulations and opportunities.

>> Read: A step-by-step guide to financial planning in Singapore

How can you gain CFP certification in Singapore?

Becoming a certified financial planner in Singapore involves a structured course that ensures professionals are well-equipped to provide comprehensive financial advice. It’s a commitment to upholding high standards in the financial planning industry.

This certification demonstrates a deep understanding of financial principles and a dedication to ethical practice, essential for building trust with clients in Singapore's competitive financial landscape.

Step 1: Educational requirements

Candidates must first meet the minimum academic qualifications, such as a diploma, A-Level certification or 3 years of working experience. They are then required to complete a Financial Planning Association of Singapore (FPAS)-approved CFP certification education programme, ensuring a solid foundation in financial planning principles and practices specific to the Singaporean context.

The full list of requirements include:

-

Examinations: Candidates must pass the CFP Certification Examination administered by the FPAS. This rigorous examination tests their knowledge and application of financial planning concepts, ensuring they are competent to provide expert advice to clients in Singapore.

-

Experience: To further validate their expertise, candidates need to accumulate a minimum of three years of relevant work experience in the financial services sector. This practical experience ensures they can apply their theoretical knowledge to real-world scenarios, enhancing their ability to serve clients effectively in Singapore.

-

Ethics: Finally, candidates must adhere to FPAS’ Code of Ethics and Professional Responsibility to maintain the integrity of their certification. This commitment to ethical conduct reinforces their dedication to acting in the best interests of their clients, building trust and credibility in Singapore’s financial community.

-

Continuing education: To maintain their certification and stay abreast of industry developments, CFPs in Singapore must fulfill a 30-hour continuing education requirement every two years. This ensures they remain updated on the latest financial regulations, market trends and best practices, providing clients with the most current and effective financial advice.

How much does it cost to engage a CFP?

While not everyone requires financial advisory services, a certified financial planner can be invaluable for those who need help organising their finances, navigating investments or setting clear financial priorities. A CFP’s expertise is particularly beneficial in Singapore's complex financial landscape, where strategic planning is crucial for achieving long-term financial security.

CFPs in Singapore typically command higher fees than non-certified advisors, reflecting their rigorous certification, fiduciary duty and specialised expertise in navigating the local financial landscape. Clients can expect to pay for services through various structures, including fixed fees for comprehensive financial plans, hourly consultation rates or retainer-based fees for ongoing financial guidance. Singaporean investors should evaluate the value of a CFP’s expertise in relation to their financial needs and goals, considering the comprehensive and ethical guidance provided.

Alternatively, online fiduciary financial advisors, some providing access to CFPs, often charge a percentage of assets under management (AUM), sometimes between 0.3% to 1% annually. Singaporean investors should evaluate fees based on the complexity of their financial needs, considering the value and expertise a CFP brings to achieving their financial goals.

>> Read: Money confessions: Secrets your financial advisor won’t tell you

How can I find a certified financial planner in Singapore?

The FPAS offers an official directory where you can verify and locate CFP-certified professionals. Additionally, the Monetary Authority of Singapore (MAS) maintains a financial advisor registry, allowing you to check licensing and disciplinary records, ensuring your advisor is both qualified and compliant.

Verifying a CFP’s credentials through FPAS or their official website is essential. It's important to check for any past disciplinary actions or complaints before engaging an advisor, ensuring they have a clean record and adhere to ethical standards.

For those seeking convenience and potentially lower costs, digital platforms in Singapore offer virtual access to CFPs. Many financial advisory firms and robo-advisors in Singapore also connect clients with certified financial planners, providing a range of options to suit different needs and preferences.

What are the differences between a CFP and a CFA in Singapore?

In Singapore's financial sector, professionals often hold various certifications, each signifying specialised expertise. Understanding these distinctions is crucial for choosing the right advisor. While both CFPs and CFAs are highly regarded, they cater to different aspects of financial services:

Chartered financial analyst (CFA) vs. certified financial planner: In Singapore, the CFA and CFP designations represent distinct areas of financial expertise. CFAs specialise in investment analysis, portfolio management and corporate finance, typically serving corporations and institutional investors. In contrast, CFPs focus on personal financial planning, including retirement, tax, estate and insurance planning, primarily working with individuals and families.

Certified public accountants (CPA) in financial advisory: CPAs primarily specialise in tax planning and accounting, providing essential services for both individuals and businesses. Some financial advisors in Singapore also hold CPA certifications, enabling them to offer clients more tax-efficient strategies. This dual expertise allows them to navigate Singapore's complex tax regulations and provide comprehensive financial advice.

Chartered financial consultant (ChFC): ChFCs offer financial planning services similar to CFPs, but with additional training in behavioral finance, estate planning and modern financial planning topics. While less common than CFPs in Singapore, ChFCs provide holistic financial advice. Their broader training equips them to address diverse client needs, including the psychological aspects of financial decision-making.

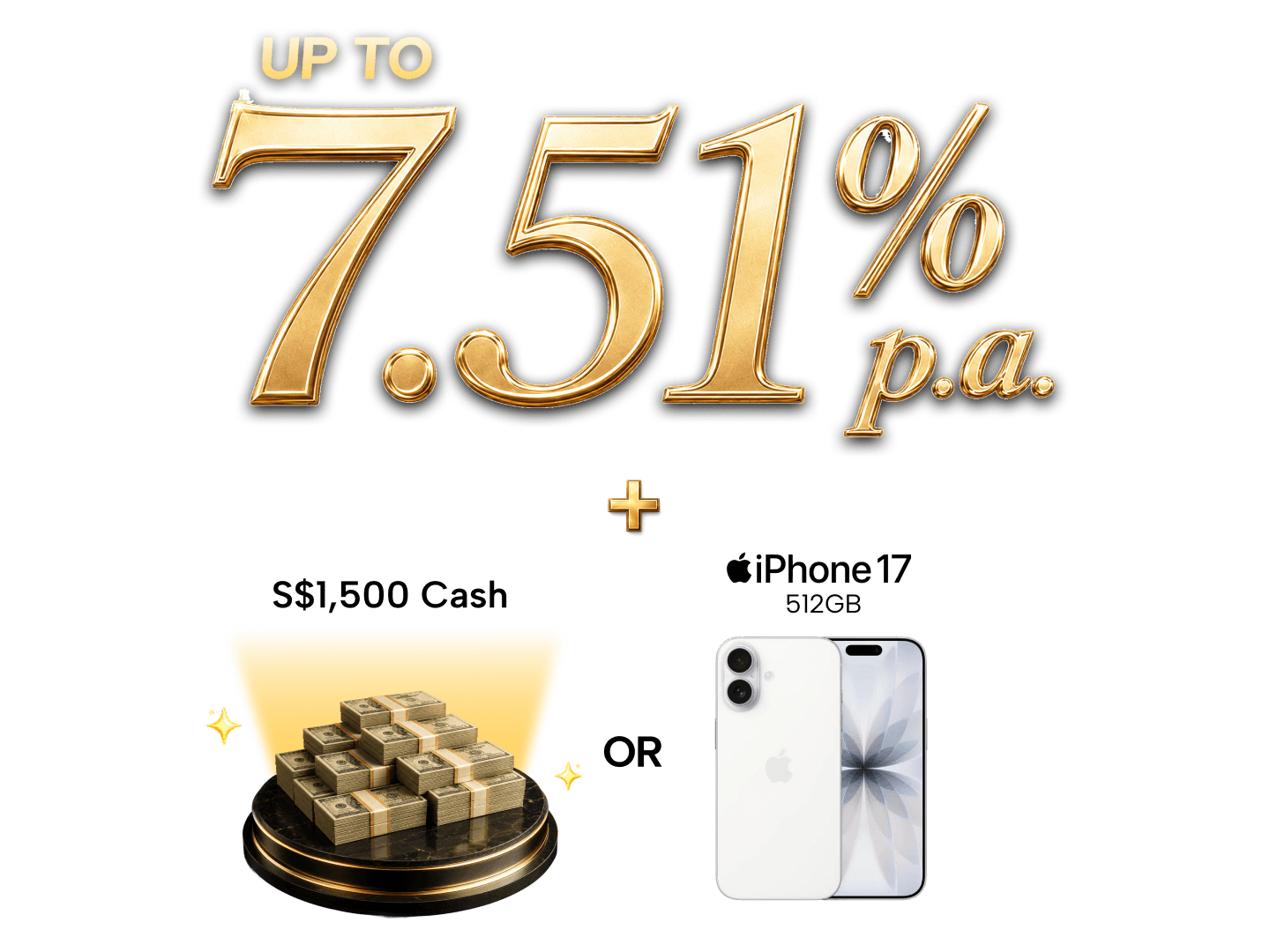

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

What are the differences between a CFP and a financial advisor in Singapore?

In Singapore, the distinction between a CFP and a general financial advisor lies in the level of certification and ethical obligations. A CFP holds a specific, rigorous certification, ensuring years of experience, fiduciary responsibility and comprehensive training in financial planning.

In contrast, "financial advisor" is a broad term encompassing professionals offering various financial services like planning, investment and insurance, but it does not necessarily indicate a specific credential or adherence to a strict ethical code.

Singaporeans can verify a CFP’s status through the FPAS website, ensuring their advisor is genuinely certified. It is crucial to check credentials and disciplinary records before engaging any advisor, ensuring transparency and trust.

Meanwhile, understanding how financial advisors are paid is also crucial. Fee-only advisors charge clients directly, ensuring no commission-based conflicts, while fee-based advisors may earn commissions on products they recommend. Singaporean investors should always ask about their advisor's fee structure to ensure transparency and align interests.

Fee-only or fee-based financial advisors: What’s the difference?

In Singapore, fee-only financial advisors are compensated directly by their clients, ensuring no commissions from product sales. This model minimises conflicts of interest, as advisors have no incentive to push specific financial products. Fee-based advisors, on the other hand, earn both client fees and commissions, which may become potential conflicts as they may favour promoting commission-based products.

While CFPs in Singapore are held to a fiduciary standard, requiring them to act in clients’ best interests regardless of payment, understanding the fee structure is vital. Clients should always inquire about how their advisor is compensated. This ensures transparency and aligns the advisor’s interests with the client’s financial goals in Singapore's competitive financial landscape.

Steps when choosing a CFP in Singapore

Selecting the right CFP in Singapore is crucial for achieving your financial goals. It's about finding a professional who not only has the expertise but also aligns with your values and needs.

Here’s a step-by-step guide to help you make an informed decision:

-

Step 1: Verify credentials — Ensure the planner holds a valid CFP certification recognised by the FPAS.

-

Step 2: Assess experience — Consider the planner's experience in areas relevant to your specific financial needs, such as retirement planning, investment management or estate planning.

-

Step 3: Understand fee structures — Clarify how the planner charges for their services—whether they are fee-only, commission-based or a combination of both.

-

Step 4: Check for disciplinary actions — Review any past disciplinary issues through the FPAS or relevant regulatory bodies like the Monetary Authority of Singapore (MAS).

Additional resources

5 Best Wealth Management Services in Singapore

Priority Banking In Singapore: How Does It Help To Grow Your Wealth?

Relevant articles

A Step-by-Step Guide to Financial Planning in Singapore

Creating a solid financial plan is like mapping out your route to financial success. It's about understanding where you are now, where you want to be, and how you'll get there. This guide provides a step-by-step approach to financial planning, with a focus on strategies and resources relevant to Singaporeans.

Is It Time to Fire Your Financial Advisor? These 5 Signs Say Yes

Stay ahead in everything finance

Subscribe to our newsletter and receive insightful articles, exclusive tips, and the latest financial news, delivered straight to your inbox.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.