How to Get a Personal Loan With Bad Credit in Singapore

Updated: 28 May 2026

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Life can throw unexpected financial challenges your way. Retrenchment could leave you without a steady income, while a sudden medical emergency or accident can prove catastrophic—especially if you do not have sufficient insurance coverage.

In times like these, you might look to apply for a personal loan with bad credit in Singapore to help bridge the financial gap. However, if your history with debt hasn't been ideal, you may find it difficult to get your application approved. Lenders are naturally risk-averse, meaning a personal loan with low credit score metrics can feel out of reach.

Fortunately, having poor credit doesn't automatically mean all doors are shut. By understanding how the ecosystem works, adjusting your borrowing strategy, and looking beyond traditional retail banks, you can still access the emergency funds you need.

Here is everything you need to know about navigating loans for poor credit score Singapore options safely and effectively.

» COMPARE: Best loans for bad credit in Singapore

How to check your credit rating in Singapore

Checking your credit score is crucial before applying for a loan, as lenders use it to assess your loan eligibility by checking if you meet their minimum requirement. You can obtain your credit report from credit bureaus like Credit Bureau Singapore (CBS) for a nominal fee.

Credit scores in Singapore range from 1000 (rated HH; highest probability of defaulting on repayment) to 2000 (rated AA; lowest probability of defaulting on repayment), with a higher score and rating being better. Credit scores of 1000 to 1812 (rated HH to EE) are generally seen as bad credit scores but individual lenders may have their own minimum credit score requirements as well.

When reviewing your credit report, pay attention to key factors like outstanding debts/overdue balances, repayment history, previous inquiries, and unauthorised inquiries. If you spot any discrepancies, address them by disputing errors directly with the credit bureau and focusing on improving your financial habits.

CBS occasionally offers free credit reports to help you keep track of your financial standing. Check their page for the latest updates.

Can I get a personal loan with bad credit in Singapore?

Yes, but your choices and the terms of your loan will vary significantly compared to someone with a pristine credit rating.

When you submit an application, financial institutions assess your risk profile by pulling your credit report from the Credit Bureau Singapore (CBS). If your report shows missed payments, defaults, or high credit utilisation, you may have a personal loan low CBS score Singapore issue. This signals to mainstream banks that you represent a high risk of default.

To bypass this hurdle or to steadily rebuild your rating, consider the following actionable steps:

Apply for a smaller loan amount

A bad credit score may prevent you from securing a major, multi-year personal loan from a traditional bank. Because an unsecured loan requires no collateral, your credit history acts as the primary guarantee that you will pay the money back.

If you are facing roadblocks, one of the best bad credit loan approval tips Singapore experts recommend is to scale down your expectations. Try applying for a significantly smaller loan amount. Lenders are far more willing to overlook a lower score if the total capital exposure is minimal.

Once granted a micro-loan, use it as a tool to rehabilitate your credit profile. Make absolutely sure you do not miss a single payment deadline. Consider setting up automatic calendar reminders or GIRO arrangements to avoid human error. Over time, borrowing small sums and paying them back promptly will show up as positive data on your report, demonstrating how to improve credit score for loan Singapore purposes so that banks will trust you with larger lines of credit in the future.

Restructure your outstanding debts

A low credit rating almost always stems from carrying too much active debt or mismanaging existing credit lines. If your monthly obligations are eating up a massive portion of your income, adding another personal loan will only worsen your financial health and deepen your debt spiral.

Instead of hunting for new credit lines, explore restructuring options to make your current payments manageable:

-

Debt Consolidation Plan (DCP): If you have accumulated unsecured debts across multiple banks that exceed 12 times your monthly income, a DCP lets you combine those liabilities into a single loan with a single bank at a much lower, fixed interest rate.

-

Balance Transfer: For smaller chunks of short-term debt, a balance transfer lets you move your balance to a new bank account that offers 0% interest for a promotional period (usually 6 to 12 months), allowing you to pay down the raw principal faster.

-

Credit Counselling Singapore (CCS): If you are completely overwhelmed, contact CCS. This non-profit organisation assists distressed borrowers by creating a formal Debt Management Programme (DMP) and negotiating structured, affordable repayment schedules directly with your creditors.

By systematically paying down what you owe on time, you clear your financial record and allow your credit score to steadily recover.

Seek digital banks and non-bank financial institutions

If traditional retail banks reject your application due to rigid algorithmic risk assessments, you can broaden your horizons by looking at Singapore’s digital banking ecosystem and long-standing non-bank institutions.

Digital banks like GXS Bank (GXS FlexiLoan) and Trust Bank (Instant Loan) have introduced highly accessible, flexible borrowing structures into the local market. For example, the GXS FlexiLoan relies on customized, risk-based pricing with interest rates starting from 1.08% p.a. (EIR from 2.02% p.a.) and crucially charges zero annual fees or late fees. This structural flexibility makes digital banks highly appealing alternatives for individuals with irregular income streams or evolving credit histories.

Additionally, you can approach registered non-banking financial institutions, such as Hong Leong Finance or Singapura Finance. These established companies are fully regulated by the Monetary Authority of Singapore (MAS). While they still evaluate your CBS report and require a stable annual income, their internal underwriting criteria are sometimes more flexible than traditional commercial banks, giving you an alternative route to secure an unsecured facility.

Approach licensed moneylenders as a last resort

When emergency funds are required immediately and all bank avenues are exhausted, turning to a licensed moneylender bad credit Singapore option becomes a viable last resort.

Unlike commercial banks, licensed moneylenders operate under a distinct legal framework regulated strictly by the Ministry of Law (MinLaw) under the Moneylenders Act. Because they regularly service higher-risk borrowers, they are typically less concerned with a low CBS score, focusing instead on your immediate, verifiable monthly income.

However, because this space is high-risk for lenders, the cost of borrowing is higher. To ensure you are protected against predatory practices, you must verify that the firm is listed on the official Registry of Moneylenders and strictly adheres to the legal caps enforced by MinLaw:

-

Maximum Interest Rate: Licensed moneylenders are legally forbidden from charging more than 4% interest per month, regardless of whether the loan is secured or unsecured, and regardless of your personal income.

-

Capped Fees: Upfront administrative or processing fees cannot exceed 10% of the loan principal at the point of disbursement. If you miss a payment deadline, the late fee is legally capped at a maximum of S$60 per month, and late interest cannot exceed 4% per month for each month of delinquency.

-

Strict Borrowing Limits: For Singaporeans and Permanent Residents (PRs) earning under S$20,000 annually, the maximum legal amount you can borrow across *all* moneylenders combined is capped at S$3,000. For individuals earning S$20,000 or more per year, you can borrow up to 6 times your monthly income.

Warning: Always guard yourself against illegal online syndicates ("Ah Longs"). Legitimate licensed moneylenders are legally prohibited from advertising via unsolicited SMS, WhatsApp messages, or social media platforms. Furthermore, a licensed lender will never ask you to pay processing fees before the loan is approved or disburse funds without requiring you to pass a physical, face-to-face identity verification check at their registered business office.

» MORE: Compare personal loans in Singapore in 2025

Summary: Personal Loan Options for Different Credit Profiles in Singapore

To help you visualize how to get personal loan with low credit score parameters across different institution tiers, look at the baseline market comparison below:

| Lender Category | General Credit Requirement | Starting Interest Rates (Advertised) | Typical Effective Interest Rate (EIR) | Key Considerations |

| Traditional Retail Banks (e.g., UOB, SCB, CIMB) | Low Risk / Excellent to Good Score (High CBS Grades) | From 0.90% to 1.48% p.a. | From 1.75% to 3.22% p.a. | Hardest approval criteria; usually requires a minimum annual income of S$30,000. Offers competitive promotions and cashback. |

| Digital Banks & Alternative Financial Providers (e.g., GXS Bank, Trust Bank, Lendela) | Medium Risk / Thin Credit History accepted | From 1.00% to 1.56% p.a. | From 2.02% to 3.00% p.a. | Highly flexible; instant digital application via Singpass Myinfo. Great for gig workers or rebuilding scores. |

| Licensed Moneylenders (e.g., EZ Loan, Credit Culture) | High Risk / Bad Credit accepted | Up to 1.0% per month (Fintech Pilots) or capped at 4% per month | Varies based on loan tenure and risk profile | High cost of borrowing. Regulated caps of 10% administrative fees and S$60 late fees apply. Income verification required. |

What credit score do I need for a personal loan Singapore?

While there is no single universal cutoff number used by every institution, traditional retail banks favor applicants holding an AA or BB risk grade from CBS (scores closest to 2,000). If your score falls into the high-risk categories (closer to 1,000), major banks will likely decline your unsecured applications. However, if you possess a lower score but still maintain a stable, verifiable annual income above S$20,000, digital banks and legal alternative lenders offer real paths to approval.

If you are unsure of where you stand, you can pull your official credit report directly from the Credit Bureau Singapore website for a processing fee of S$6.42 (inclusive of GST). Alternatively, you can claim a copy for free if you have applied for a new credit facility with any CBS-member bank or institution within the last 30 days.

Need the funds to embark on your next step in life?

Explore the top personal loans in Singapore with personalised loan rate estimates from licensed lenders.

Expected interest rates for a loan with bad credit in Singapore

Personal loan interest rates and terms in Singapore depend on factors such as your credit score, lender policies, and other financial factors.

Borrowers holding a personal loan low CBS score Singapore profile typically face the following structural challenges:

-

Higher interest rates: Lenders often charge higher interest rates/EIR to borrowers with bad credit to compensate for the increased risk of payment delinquency.

-

Lower loan amounts: Lenders may approve smaller loan amounts for borrowers with bad credit due to concerns about their overall repayment capacity.

-

Shorter repayment periods: Lenders may offer shorter repayment periods to borrowers with bad credit, which lowers the lender's exposure time but results in higher monthly installments.

If you are wondering what credit score do I need for a personal loan Singapore banks will accept, the Credit Bureau Singapore (CBS) scores individuals on a scale from 1,000 to 2,000 across specific risk grades. Here is an estimated comparison of personal loan interest rates in Singapore based on these credit score categories:

| Credit Score Category | Score Range | Typical Effective Interest Rate (EIR) | Risk Perception by Lenders |

| HH | 1000 - 1723 | Highest (Often rejected by traditional banks; referred to alternative lenders) | Very High Risk |

| GG | 1724 - 1754 | High (Premium pricing or digital bank risk-based pricing applies) | High Risk |

| FF | 1755 - 1781 | High to Moderate (Requires stable income to secure standard rates) | Moderate-High Risk |

| EE | 1782 - 1812 | Moderate (Standard bank promotional pricing with less leeway) | Moderate Risk |

| DD | 1813 - 1824 | Moderate to Favourable (Standard market rates apply) | Low-Moderate Risk |

| CC to AA | 1825 - 2000 | Lowest (Eligible for premium bank rates and immediate automated approval) | Low Risk |

How to improve your loan approval chances with bad credit in Singapore

Borrowers with low credit scores in Singapore can still optimize their application profile. Utilize these proven bad credit loan approval tips Singapore strategies to improve your chances of securing a personal loan:

-

Add a guarantor or joint applicant: Some lenders allow a guarantor (co-signer) or joint borrower with better credit to improve approval chances. This is especially useful if you’re looking to apply for a personal loan with bad credit in Singapore or without standard corporate income proof. A guarantor typically has no access to the loan amount but legally commits to repaying the loan if the principal borrower is unable to. A joint borrower shares active access to the loan amount and shares joint responsibility with the principal borrower. This individual should be a trusted friend or family member with a clean CBS history.

-

Consider a secured loan: Utilizing collateral (such as fixed deposits or property equity) can drastically swing odds in your favor. Opting for a secured loan bad credit Singapore arrangement reduces the lender's risk profile to near zero, as opposed to an unsecured loan. However, note that if you fail to repay a secured loan, your collateral may be seized and your credit score will still be negatively impacted.

-

Declare all income sources: Non-salary income such as legal rental income from properties, continuous CPF contributions, or official alimony can strengthen loan applications. Be as transparent about your comprehensive cash flow as possible to get the optimal loan terms and prove how to improve credit score for loan Singapore eligibility.

-

Request a smaller loan amount: Applying for a loan well within affordable, realistic repayment limits increases instant approval chances because it keeps your Total Debt Servicing Ratio (TDSR) balanced.

Where to get a personal loan with bad credit in Singapore

Banks

Some retail and digital banks in Singapore may offer personal loans to borrowers with lower credit scores under customized risk-based pricing. However, approval remains heavily dependent on structural parameters such as stable ongoing employment status and recent repayment history.

Licensed moneylenders

A licensed moneylender bad credit Singapore option, regulated under the strict oversight of the Ministry of Law, may be more willing to approve loans for poor credit within an expedited timeline—including immediate digital disbursement. This category also includes registered credit unions, although securing a loan through them typically requires active membership with the organization first. Note that legal interest rates here are strictly capped at 4% per month, leading to a higher overall EIR.

Fintech platforms

Fintech comparison platforms and loan matchmakers like Lendela or MoneyIQ help borrowers automatically compare customized loan offers from various legal lenders simultaneously. These include institutional peer-to-peer funders or specialized platforms like Funding Societies, which may be more open to evaluating holistic data metrics when lending to individuals with bad credit.

SingSaver Tip:

When you apply for personal loan bad credit products, be aware that some lenders may charge an upfront origination or administrative fee. This fee is typically a fixed percentage of the loan amount and is legally deducted from the loan cash principal before it is disbursed to your account, or added directly to your Equated Monthly Installments (EMI). Always factor in any and all hidden administrative fees when calculating the total cost of your loan to get the most accurate EMI and EIR numbers.

Singer-savvy tip

When applying for a loan, be aware that some lenders may charge an origination fee. This fee is typically a fixed percentage of the loan amount and can be deducted from the loan before it's disbursed or added to your Equated Monthly Installments (EMI). Always factor in any and all fees when calculating the total cost of your loan to get the most accurate EMI and EIR numbers.

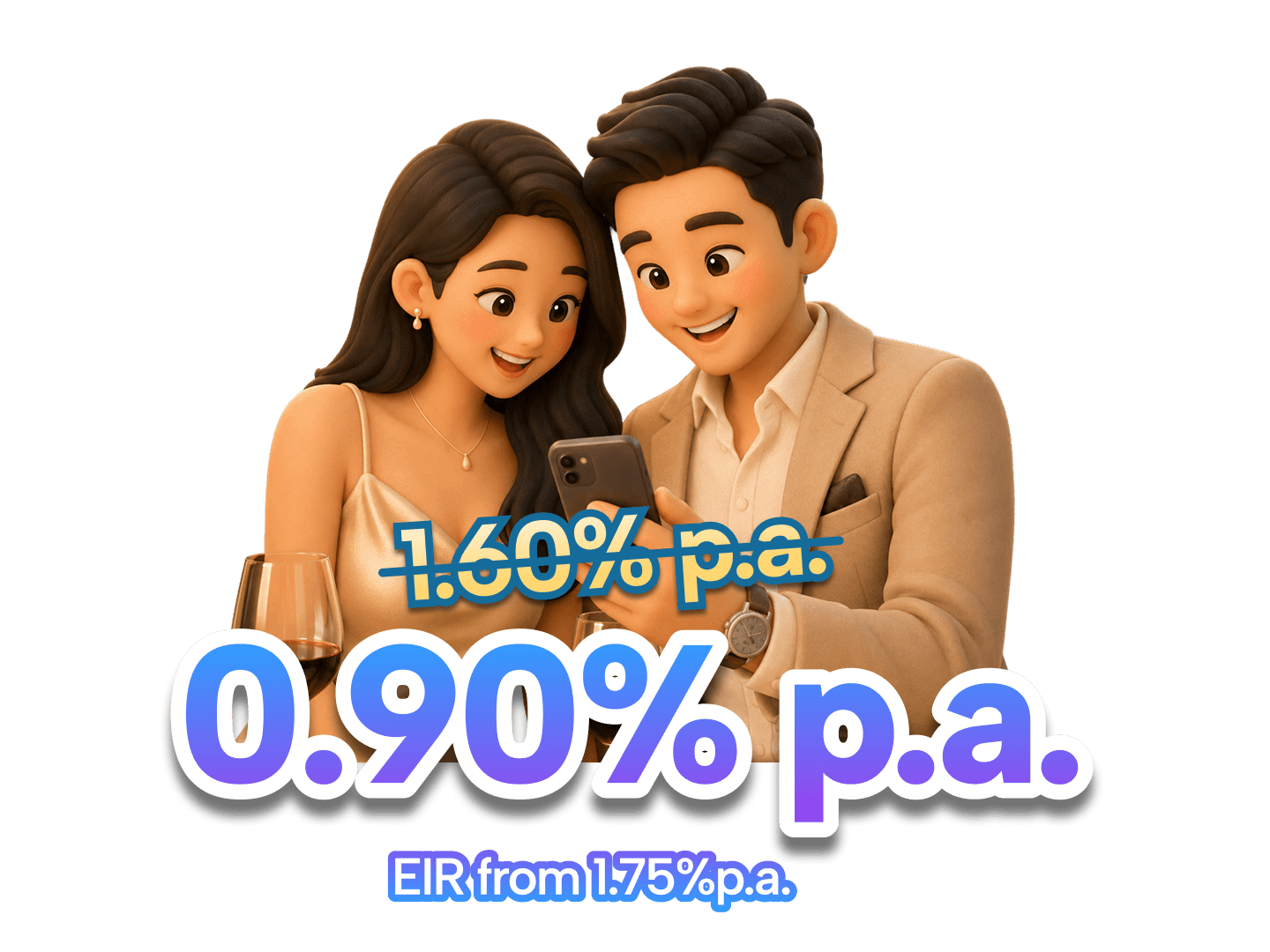

⚡SingSaver x SCB CashOne Personal Loan Flash Deal⚡

Enjoy one of the market's lowest interest rates starting from 0.90% p.a. (EIR from 1.75%) plus up to S$1,800 in Cashback when you apply for Standard Chartered CashOne Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Bad credit loans to avoid in Singapore

While tough financial circumstances may sometimes compel us to seek emergency funding, executing due diligence is critical. Relying on the wrong lender tier can trap you in predatory debt loops, permanently damaging your financial standing.

Unlicensed moneylenders ("Ah Longs")

Avoid borrowing from illegal loan sharks, also known as "Ah Longs," under any circumstances. These predatory lenders often charge exorbitant, illegal interest rates and regularly resort to extreme digital harassment, doxxing, or physical intimidation tactics to enforce repayment. Always check the Ministry of Law's official online list of licensed moneylenders before engaging with any firm.

High-Interest Short-Term Loans

While some licensed moneylenders offer legitimate fast cash or payday loans, these can still be incredibly costly due to the legally maximum allowable interest rates (up to 4% per month). Be highly wary of independent lenders who promise "no-credit-check" loans online or via text messages, as these are often unregulated predatory operations or scams with hidden processing traps. Repeatedly refinancing short-term credit facilities results in compounding EIR, leading you to pay far more in interest than the original loan principal.

Alternatives to personal loans for bad credit in Singapore

If you do not currently qualify for traditional unsecured products due to a weak credit rating, consider these regulated alternatives to avoid high-interest payday traps:

-

Government financial assistance programmes: Singapore offers several institutional, government-backed financial aid frameworks designed to support individuals facing temporary or prolonged financial distress. This includes ComCare Assistance, which provides direct cash assistance and social support for low-income individuals and families; the Silver Support Scheme, which offers quarterly cash supplements to eligible retired seniors; and MOE Tuition Fee Loan & Study Loan Schemes to support students enrolled in MOE-subsidized post-secondary educational tracks.

-

Negotiating with creditors: If you are struggling to maintain your monthly obligations, proactively approach your existing creditors, such as retail banks, credit card issuers, or landlords. Many are willing to offer restructured, elongated payment plans or temporary relief options like loan deferments. If you are dealing specifically with overwhelming medical bills, institutional safety nets like MediFund or customized public hospital payment plans offer immediate interest-free payment relief.

-

Family or employer loans: Borrowing directly from family members, trusted friends, or your company's HR emergency advancement program can provide an interest-free or low-cost alternative to market loans. However, to preserve personal relationships, it is highly advisable to write a formal legal agreement detailing a clear repayment schedule to protect both parties.

-

Buy Now, Pay Later (BNPL) services: For managing smaller, essential everyday purchases without taking on traditional high-interest debt, consider utilizing Singapore-compliant BNPL services like Atome or Grab PayLater. These platforms break up retail transactions into interest-free installments and do not require traditional hard credit bureau checks, though strict internal transactional spending limits apply to ensure consumer protection. (Note: Legacy platforms like ShopBack PayLater have been fully discontinued in the Singapore market).

SingSaver x Credible.sg Exclusive Offer

Experience fast, convenient loans with Credible.sg and earn cashback rewards on top—making your financial moves smarter and more rewarding! Valid till 30 June 2026. T&Cs apply.

Frequently asked questions about how to get personal loans for bad credit

In Singapore, "bad credit" typically refers to a low credit score rated HH up to EE. While there's no single definition of ‘bad’ credit and lenders have their own respective minimum rating requirements, a score below a certain threshold can make it more challenging to secure credit.

Bad credit can make lenders hesitant to approve a loan application as they indicate a higher risk of defaulting on payments to lenders. If the personal loan is approved, borrowers with bad credit may face higher EIR, lower loan amounts, and shorter repayment periods.

Secured loans, co-signed loans, and joint loans may be easier to obtain with bad credit. Secured loans use collateral, while co-signed and joint loans involve another person with better credit. In the event that payments can’t be made, the collateral will be seized or the guarantor or joint applicant will be responsible for repayment.

Factors that can disqualify you from getting a personal loan include a crest score that’s too low, insufficient income, excessive outstanding debts, or a short or non-existent credit history. If you check your personal loan application and see a rejection you can contact the lender to ask why before seeking out a different lender or improving your loan application.

The loan amount you can borrow with bad credit varies depending on the lender and your financial situation. Generally, lenders may offer smaller loan amounts to borrowers with bad credit.

Want to improve your credit rating to improve your chances of loan approval?

Learn top tips for building your credit score and securing your financial future.

Relevant articles

How to Get a Personal Loan In Singapore With a Bad Credit Score

Best Loans to Help Improve Bad Credit Score in Singapore (2020)

Stay ahead in everything finance

Subscribe to our newsletter and receive insightful articles, exclusive tips, and the latest financial news, delivered straight to your inbox.

Compare personal loan lenders in Singapore

Find the best personal loan lenders for you

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.