Citigold Review (2026): Is Citibank Singapore Priority Banking Tier Worth It?

Updated: 8 Apr 2026

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Looking to grow your wealth with expert guidance and global privileges? Citigold could be the priority banking experience you’ve been waiting for.

For affluent individuals who want more than just a bank account, Citigold offers a comprehensive suite of wealth management services, global banking access, and exclusive perks tailored to support your financial goals. Whether you're growing a portfolio, protecting generational wealth, or simply want better value from your cash, Citigold gives you access to a Relationship Manager, financial specialists, and a curated set of benefits both in Singapore and abroad. Let’s explore whether this premium programme is the right fit for you.

Celebrate your salary milestones with a premier banking experience

What’s the use of wealth if you don’t indulge? Explore priority banking with luxury perks, exclusive rewards and all the good things for the good life.

SingSaver feature: Citigold for a comprehensive suite of wealth management for the well-heeled

SingSaver Exclusive Rewards

- Get Upsized S$1,500 Cash or an Apple iPhone 17 512GB (worth S$1,599) when you make a deposit of S$500,000 and make a new qualified investment of minimum S$100,000 within 3 calendar months of account opening, including the month of account opening

- Get Upsized S$1,500 Cash or an Apple iPhone 17 512GB (worth S$1,599) when you make a deposit of S$500,000 and successfully sign up as an Accredited Investor (AI) within 3 calendar month of account opening, including the month of account opening

- Get Upsized S$1,200 Cash or an Apple iPhone 17 256GB (worth S$1,299) when you make a deposit of S$350,000 and successfully sign up as an Accredited Investor (AI) on an individual basis in the capacity as a primary accountholder within 3 calendar months of account opening, including the month of account opening.

- Alternatively, get Upsized S$900 Cash when you deposit S$350,000 within 3 calendar months of account opening, including the month of account opening.

- Enjoy additional S$200 Cash when you make a deposit of S$350,000 within the second month of account opening and maintain the funds until gift fulfilment.

Stackable Citi Rewards

- S$500 when you sign up as an Accredited Investor

- For every S$100k of Investment/Insurance purchase by MOB 3, customers enjoy S$1000 cash

- Enjoy Citigold Preferential Time Deposit Rates. (Up to 1.40% p.a. on 6-mth SGD Time Deposit; Up to 1.30% p.a. on 3-mth SGD Time Deposit) T&Cs apply.

- Terms and Conditions apply.

- Citigold Exclusive Benefits and Privileges

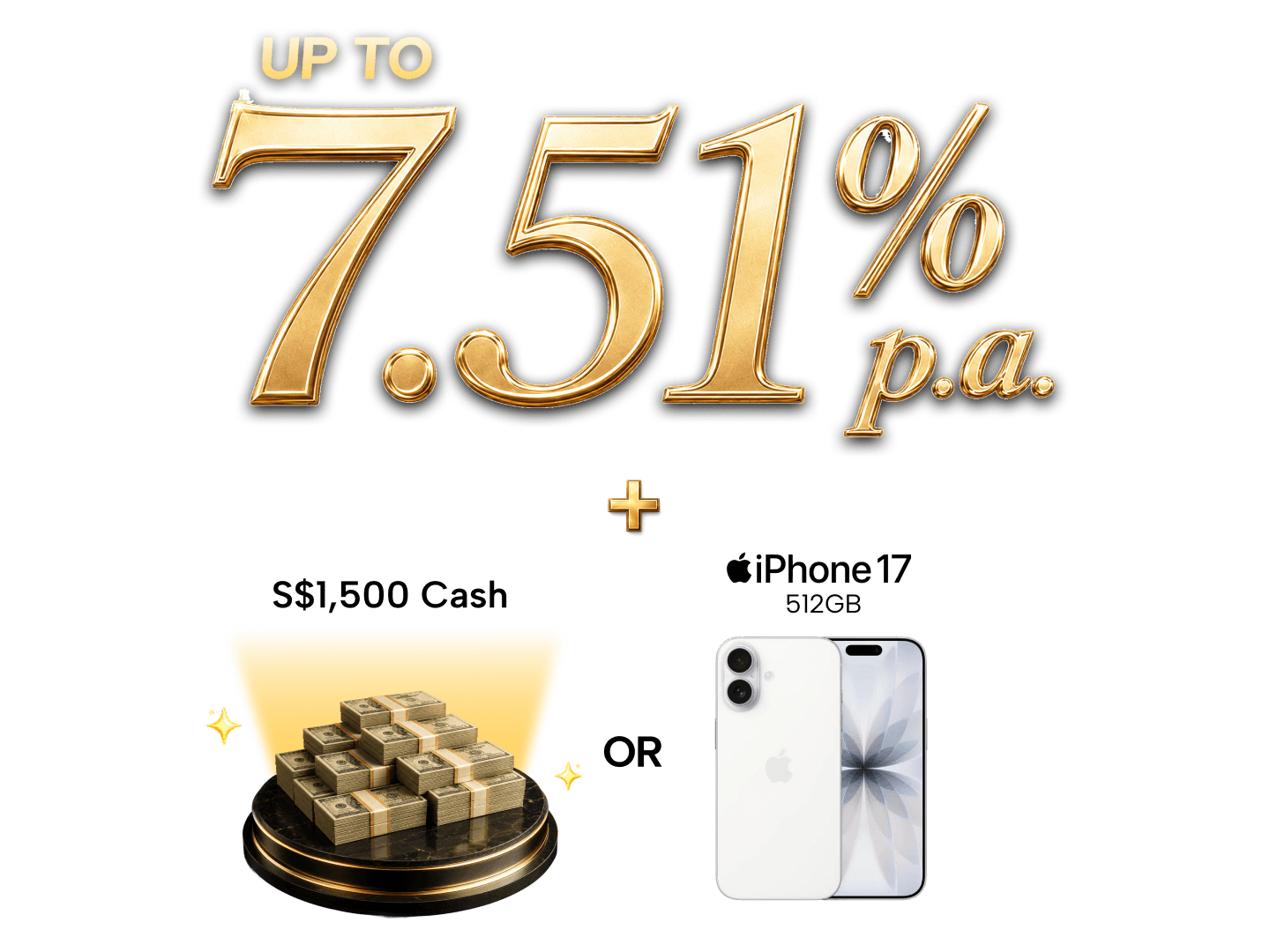

- Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. T&Cs apply.

- Enjoy zero foreign transaction or currency conversion fees in over 15 currencies with Citibank Global wallet when you pay with your Citigold Debit Mastercard.

- Enjoy 0%* commission buy trades online for U.S. & Hong Kong markets for 6 months when you open a new Citibank Brokerage account.

- Get wealth management advice and solutions from a dedicated Relationship Manager and team of wealth specialists

- Receive in-depth global market insights and research knowledge from a team of over 350+ research analysts.

- Enjoy fully personalised wealth management solutions with Citigold's Total Wealth Advisor.

- Citigold status is maintained at Citibank branches overseas.

- Read our full review of Citigold

- What is an Accredited Investor?

- An Accredited Investor is someone who meets the requirements set out by the Monetary Authority of Singapore (MAS) and has opted in to be treated as an Accredited Investor by the bank. Accredited Investors generally have access to a wider range of investment products than non-Accredited Investors, and at the same time require less regulatory protection.

- How to be an Accredited Investor

- Start your wealth journey with Citigold and speak to your relationship manager.

- Advantages of an Accredited Investor

- Diversified wealth opportunities

- Access to a more comprehensive range of financial products and services available only to Accredited Investors

- Access to a team of wealth experts

- Connect with an experienced Relationship Manager and a team of wealth experts who will partner you to achieve your wealth goals

- Wide range of investments

- Trade in Bonds, Structured Notes and restricted Investment Funds without the minimum S$200k per transaction requirement

- Eligibility for Accredited Investor

- Net personal assets exceeding S$2 million in value (or its equivalent in a foreign currency); or

- Financial assets (net of any related liabilities) exceeding S$1 million in value (or its equivalent in a foreign currency); or

- An income in the preceding 12 months of not less than S$300,000 (or its equivalent in a foreign currency)

SingSaver’s take

As Singapore’s banking landscape evolves, the gap between digital-first savings accounts and relationship-based wealth management continues to widen. Priority banking programmes now compete not only on interest rates, but also advisory access, global banking features, and investment ecosystems.

Citigold, Citibank Singapore’s entry-level wealth management tier, remains one of the most visible options for clients.

But in an environment of stabilising interest rates and low-cost brokerages, does Citigold still justify the capital commitment?

Here is a fact-checked 2026 review based on Citibank Singapore disclosures and reputable Singapore financial sources.

Pros

Massive Welcome Rewards: Receive up to S$60,676 in cash (stackable) when joining as a New-to-Bank client, including a S$200 Digital Bonus for online applications.

High-Yield "Wealth First" Account: Earn up to 7.51% p.a. interest by bundling banking with simple wealth actions (Spend, Invest, Insure, Borrow, and Save).

Global Citigold Status: Enjoy priority banking privileges across 30+ countries, fee-free global transfers, and emergency cash withdrawals of up to US$10,000 worldwide.

Dedicated Wealth Team: Access a Relationship Manager and a specialized team of 350+ analysts for personalized portfolio reviews via the Citigold Total Wealth Advisor.

International Lifestyle Perks: Exclusive access to Citi Wealth Hubs (Orchard and Malacca Street), 0% commission on US/HK stock trades for 6 months, and zero FX fees via the Citibank Global Wallet.

Cons

Higher AUM for Welcome Gifts

Complex Interest Tiers: Achieving the headline 7.51% p.a. requires significant product engagement (e.g., S$50k investment or insurance), which may not suit "pure" savers.

Advisory Value varies for DIYers: Investors who prefer low-cost, self-directed platforms (like Moomoo or IBKR) may find the standard bank brokerage fees less competitive despite the RM service.

Accredited Investor (AI) Bias: The most lucrative rewards and "bonus" interest rates are increasingly gated behind AI status, which requires specific net-worth or income thresholds.

Welcome Promotions (New-to-Bank Customers)

Citibank Singapore periodically runs acquisition campaigns for new Citigold clients involving cash rewards and investment incentives.

Typical promotion structures may include:

- Cash rewards for depositing fresh funds

- Bonuses tied to investment activity

- Additional incentives for Accredited Investors

⚠️ Note: Promotional rewards vary by campaign period and are subject to Citibank Singapore’s prevailing terms and conditions. Readers should verify current offers directly with the bank.

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

1. Eligibility

Eligible assets may include:

- Savings and current account balances

- Fixed deposits

- Investment holdings (unit trusts, bonds, equities)

- Eligible insurance products distributed by Citibank Singapore

If balances fall below the required threshold:

- A S$15 monthly service fee may apply.

- Citigold status may be reviewed if balances remain below requirements for an extended period.

Unlike digital banks, priority banking tiers evaluate clients based on overall wealth relationships rather than standalone accounts.

2. Interest Rates: Citi Wealth First Account (2026)

A major component of the Citigold ecosystem is the Citi Wealth First Account, a hybrid savings account designed to reward broader wealth activity.

Interest Structure (April 2026)

- Base interest: 0.01% p.a.

- Maximum potential rate: Up to 7.51% p.a. (bonus interest)

Higher interest tiers are unlocked through qualifying “wealth actions,” such as:

| Wealth Action | Example Requirement |

|---|---|

| Invest | ≥ S$50,000 in eligible investments |

| Insure | ≥ S$50,000 single-premium insurance purchase |

| Spend | ≥ S$250 monthly debit card spend |

| Save | Increase balance by S$3,000 monthly |

| Borrow | Eligible mortgage relationship |

Important context for readers:

👉 The headline rate applies only when multiple conditions are met simultaneously and typically on capped balances.

This structure mirrors Singapore’s broader trend toward activity-based savings accounts rather than flat high-interest deposits.

Travel with peace of mind, backed by these international accounts

These banks boast lower foreign transaction fees and comparable ATM rates, so you can go overseas with ease

4. Key Benefits

A. Dedicated Relationship Manager

A defining feature of Citigold is access to a dedicated Relationship Manager (RM) supported by specialists across:

- Investments

- Insurance planning

- Mortgage advisory

- Wealth structuring

For clients transitioning from self-directed banking, this human advisory layer is often the primary differentiator versus digital banks.

B. Global Banking Connectivity

Citigold is positioned strongly for internationally mobile clients.

Key global features include:

- Multi-currency spending via Citi Global Wallet

- Transfers between Citibank accounts worldwide

- Overseas assistance services for card loss or emergencies

These features may appeal to:

- Frequent travellers

- Expatriates

- Parents funding overseas education

C. Wealth Advisory Spaces

Citibank Singapore has increasingly shifted toward wealth advisory hubs rather than traditional transactional branches, focusing on investment consultations and financial planning discussions.

5. Fees and Costs to Consider

While Citigold provides advisory access, costs remain an important consideration.

Potential fees include:

- S$15 monthly service fee if balance requirements are unmet

- Investment platform and fund management fees

- Brokerage charges after promotional periods

Compared with DIY brokerages commonly used in Singapore — such as low-cost online trading platforms — advisory-led banking solutions may involve higher overall costs.

Launch your business with a business loan in Singapore 2025

Need some capital for that great idea to take off? We recommend business loans with flexible terms and no-collateral required

6. Citigold vs Other Priority Banking Tiers (Singapore, 2026)

Each programme reflects a different strategic focus rather than a strictly superior offering.

7. Who Citigold Is Best For

Consider Citigold if you:

✅ Want personalised financial advice

✅ Maintain significant cross-border banking needs

✅ Prefer guided investing over DIY platforms

✅ Qualify as an Accredited Investor seeking broader product access

It may not suit you if you:

❌ Prefer ultra-low investment costs

❌ Only want a high savings rate without conditions

❌ Primarily use robo-advisors or self-directed trading platforms

Final Verdict: Is Citigold Worth It in 2026?

Citigold is no longer simply a premium savings account — it functions as a relationship-based wealth platform combining banking, advisory, and investment access.

However, value depends heavily on whether clients actively use advisory services and wealth features. Pure savers or cost-focused investors may find simpler digital alternatives more efficient.

Frequently asked questions about Citigold

The current welcome offer is:

SingSaver Exclusive Rewards

-

Get an upsized reward of S$1,000 or an Apple iPhone 16 128GB (worth S$1,299) or a Nintendo Switch 2 + Mario Kart World Bundle + S$350 eCapitaVouchers when you make a deposit of S$300,000 and opt in as an Accredited Investor.

-

Alternatively, get S$500 when you deposit S$300,000.

-

Enjoy an additional S$200 Grab Voucher when you make a deposit of S$300,000 within the first 30 days from the date of account opening and maintain the funds until gift fulfilment.

-

Enjoy additional S$200 Grab Voucher when you invest S$30,000 within 3 months from the date of account opening.

Stackable Citi Rewards

-

Enjoy $300 rewards when you become an accredited investor. T&Cs apply.

-

Complete Investment Risk Profile and Fact Find Report and get S$100 cash. T&Cs apply.

-

Multiply your rewards and enjoy S$250 cash for every S$50,000 investment and/or insurance purchase. T&Cs apply.

-

Hold a valid primary/main Citi Credit Card and get a S$100 bonus cash reward. T&Cs apply.

-

Take up a Citi Home Loan and get a S$500 bonus cash reward. T&Cs apply.

-

Enjoy Citigold Preferential Time Deposit Rates of up to 2.70%* p.a. on a 3-month SGD Time Deposit. T&Cs apply.

Check the latest terms on SingSaver.

-

No, you’re not required to lock in your funds, but you must maintain a total AUM of at least S$250,000 across deposits, investments, and insurance.

Yes, joint Citigold accounts are allowed, and the AUM can be shared between both account holders.

Citigold does not directly manage CPF monies, but your Relationship Manager can advise on how to use your CPF OA and SA for investing through the CPF Investment Scheme (CPFIS).

Citi Wealth First is a high-interest savings account, while Citigold is a full-fledged wealth management relationship. You can pair both to optimise cash yield and advisory benefits.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.