What Should You Do If You Can’t Pay Your Credit Card Bill?

Updated: 11 Dec 2025

While it’s not ideal to leave unpaid balances on your credit card, here are some simple steps to help you minimise debt caused by accrued credit card interest.

Whether it’s because of a period of financial difficulty or due to a huge emergency expense, missing a credit card payment can happen to the best of us. When you can’t afford to pay off your credit card balance in full, the worst things you can do are to pay off only the interest or leave the bill unpaid entirely.

The longer you leave your credit card balance unpaid, the more you accumulate in late payment fees and interest. Averaging around 25% per annum, credit card interest rates can make it easy for debts to snowball into an amount you can’t manage.

Fortunately, there are ways for you to minimise the damage done by high credit card interest rates. Here are some simple steps you can take to save yourself from accruing even more debt due to unpaid credit card bills.

Find the right credit card for you in no time. 💳✨

Compare exclusive offers on SingSaver across cashback, miles, and rewards cards—plus enjoy stackable welcome gifts.

An Important Note on Making Full Repayments on Your Credit Cards

Credit cards are not designed for long-term loans. The interest rate is very high (around 25% p.a), so you should consider personal loans that have lower interest rates instead if you need to borrow a sum of money.

We recommend that you use credit cards as a mode of payment only. In other words, use your credit card to purchase things for rewards and discounts. However, pay off your monthly bills in full so there is no interest charged. Do not let late payment of your credit card bill become a bad habit.

Check if You Can at Least Pay Off the Minimum Repayment

Even if you do not want to pay in full, there is a minimum amount you must repay. Failing to do so not only costs you additional late fees, but also damages your credit rating. A bad credit score could affect your ability to apply for financial products in the future.

Most credit cards have a minimum repayment of S$50 or 3% of the outstanding amount, whichever is higher. If you can afford to pay this, do so promptly. Late or missed payments of the minimum repayment amount can result in additional late payment fees of up to S$100 per card per month!

If for some reason you cannot make the minimum repayment, call your bank and inform them in advance. You may be able to work out an alternative date on which to pay them.

Make a Balance Transfer as Soon as Possible

A balance transfer can help you pay off your credit card debt at a low or 0% interest rate.

For example, you owe S$5,000 on your credit card, but cannot afford to pay that amount in full. You also estimate that it will take you three to four months to pay off that S$5,000 (not counting interest).

Rather than let your credit card debt snowball, you could shift the debt onto a 0% interest balance transfer account. While you will still owe S$5,000 (plus a nominal processing fee), you now have extra time (normally 6 to 12 months) to slowly pay off the loan without accruing interest.

Note that while you are servicing your balance transfer, you should refrain from using your credit card to make new purchases. Focus on paying down your debt first before using any of your credit cards again.

SingSaver x OCBC 365 Credit Card Exclusive Offer

Apply for an OCBC 365 Credit Card via SingSaver and choose from S$400 Cash, 25,000 MaxMiles by HeyMax (worth S$600 in travel value), Dyson Airstrait, Dyson V8 Cyclone cordless vacuum, or Samsung Galaxy Buds4 Pro + S$180 eCapitaVoucher Bundle. Valid until 30 June 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$80 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 30 June 2026. T&Cs apply.

If You Cannot Make a Balance Transfer, Consider Using a Personal Instalment Loan

Most personal instalment loans have an interest rate of approximately 6% per annum. During promotional offers, you may also find personal loans with a 0% p.a. interest rate (usually for a limited time, such as the first three months).

If you are unable to utilise a balance transfer, you might want to consider taking a personal instalment loan to pay off your credit card debt. This works the same way as a balance transfer. However, the main difference is that you have to make fixed repayment for personal instalment loans, and you can extend your repayment over a longer tenure.

However, do note that if you try to repay the full loan amount before the tenure (e.g. you take a loan for one year but try to rush full payment after four months), you may be charged a prepayment penalty.

Get a Debt Consolidation Plan If You Owe More Than 12 Times Your Monthly Income

If you have maxed out multiple credit cards and owe at least 12 times your monthly income, you need to pay it off as soon as possible. The longer you wait, the more your debt will accumulate and the harder it will be to pay it off.

In this particular situation, a debt consolidation plan (DCP) can help you pay your outstanding balances from multiple credit cards. This is the process of using a single loan to pay off all your unsecured debts.

For example, you have a monthly salary of S$3,000 and owe S$500 on one credit card, S$7,000 on a second credit card, S$3,000 on a third credit card, and S$30,000 on a fourth card. That creates a total debt amount of S$40,500.

Most personal loans will only lend you up to 6 times your monthly income (S$18,000), which is not enough to pay off all your current debt. But when you get a DCP, the issuing bank gives you a single loan for S$40,500 for all your outstanding debts. You then repay the bank and manage a single loan instead of trying to juggle repaying all 4 credit cards at the same time.

Besides simplifying your debt management, a DCP also comes with a lower interest rate and a longer payment period. This saves you money on interest and makes monthly payments more affordable compared to trying to pay your debts without a DCP.

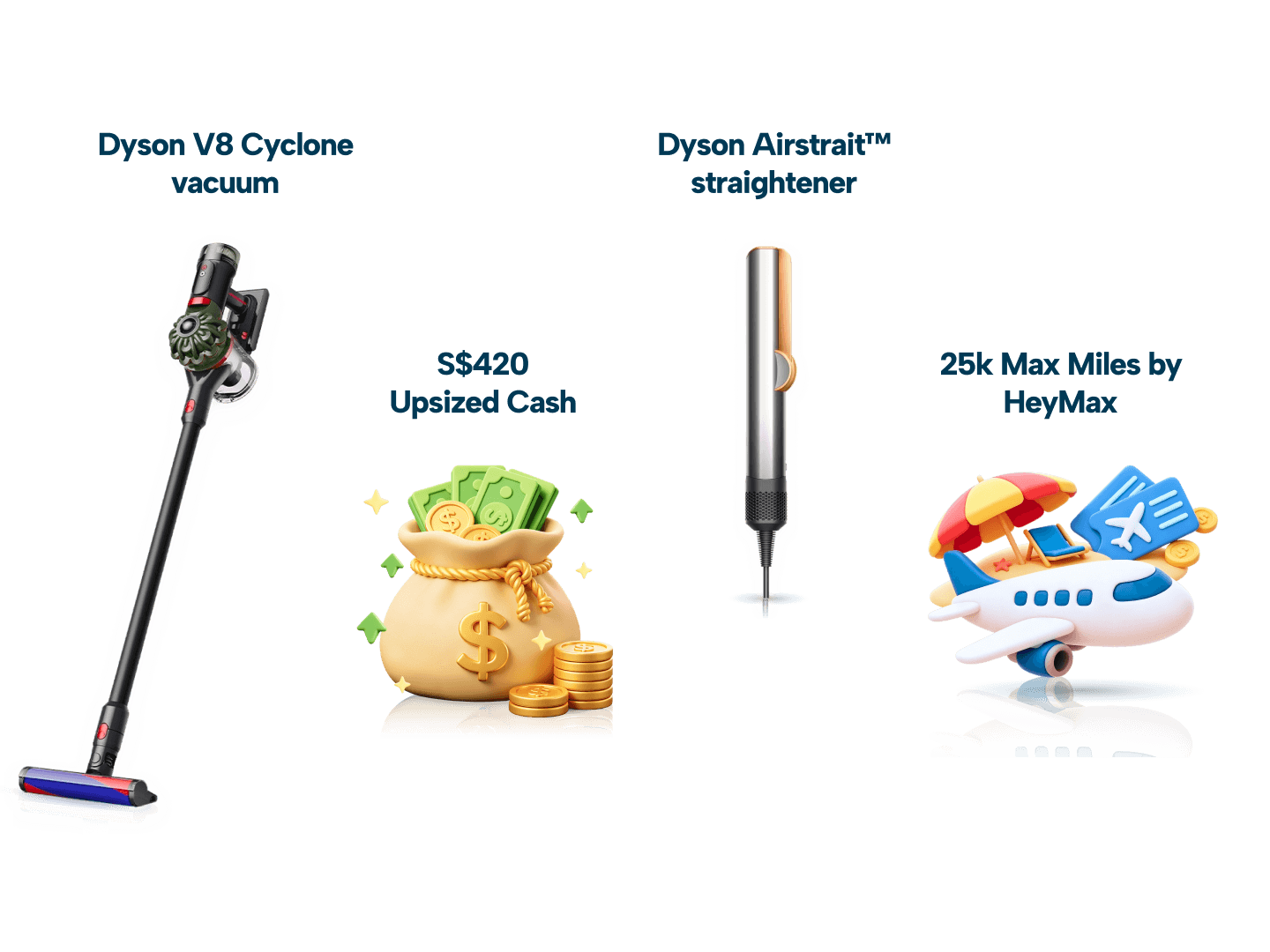

SingSaver x HSBC Live+ Credit Card Exclusive Offer

Score S$420 Upsized Cash, Dyson Airstait or V8 Cyclone cordless vacuum, 25,000 Max Miles by HeyMax (worth S$600 in travel value), or a Galaxy Buds4 Pro + S$160 eCapitaVoucher Bundle when you apply for an HSBC Live+ Credit Card via SingSaver and fulfil promo requirements. Valid until 30 June 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$50 to upgrade to the latest Dyson, Sony, and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 1 June 2026. T&Cs apply.

Avoid Using Any New Credit Until Your Debt is Fully Paid

The solutions we’ve outlined above should help you clear your outstanding balances as soon as possible. However, in order for any of these methods to work, you need to avoid adding to your debt.

Therefore, keep your credit card locked in a drawer or frozen in a block of ice until your balance has been fully paid off. (In case you choose to apply for a DCP, all your existing credit facilities will be automatically closed until all outstanding debt is less than 8 times your monthly salary.)

Managing credit card debt is a matter of forming a plan and having the discipline to execute it. By tackling your high-interest debts with any of these above methods, your progress grows with each cleared debt, which gives you more funds to save for a rainy day or to reach other financial goals.