5 steps to create a budget that works for you

Updated: 10 Jun 2026

Allocate your income wisely across essential expenses, discretionary spending, savings, and debt repayment.

Written byAfina Najib

Senior Content Editor - Singapore

Managing your finances can sometimes feel like trying to solve a complex puzzle, but it doesn't have to be. Whether you are aiming to clear a lingering debt, mapping out a downpayment for your first BTO flat, or working hard to secure a comfortable retirement, everything begins with clear financial planning.

Learning the exact steps to create a budget will transform your relationship with money. Let's walk through how to build a resilient, modern framework to manage your hard-earned cash in Singapore.

How to create a budget

A good budget ensures you’re covering essentials, saving for the future, and still having enough for life’s little joys. Follow these five steps to establish a budget that works for you.

Step 1: Calculate your net income (take-home pay)

The absolute baseline of any budget is knowing exactly how much liquid cash flows into your bank account each month. Many people make the critical mistake of budgeting using their gross monthly salary, which leads to accidental overspending.

In Singapore, you must calculate your take-home pay by subtracting your employee Central Provident Fund (CPF) contributions from your gross salary.

Important Compliance Note: Be sure to account for current CPF statutory limits. The Ordinary Wage (OW) ceiling is capped at S$8,000 per month. If you are a salaried employee under the age of 55, your mandatory employee CPF deduction is 20% of your salary up to this S$8,000 cap (amounting to a maximum employee deduction of S$1,600). Don't forget to also subtract minor monthly community deductions like CDAC, SINDA, Eurasian Association, or MENDAKI funds.

Step 2: Pick a budgeting strategy that suits you

Fixed expenses are your non-negotiables. These are the recurring costs that stay relatively predictable month after month, and failing to pay them carries direct consequences.

-

Housing: Monthly home loan payments (HDB or bank loan) or rent.

-

Insurance: Premiums for Integrated Shields, life insurance, critical illness plans, and CareShield Life.

-

Utilities & Bills: Standard SP Group electricity bills, broadband internet, and mobile phone plans.

-

Debt Paydowns: Fixed monthly payments toward education loans, car loans, or personal loans.

Predict the Champion. Share S$30,000 in Cash! ⚽

Apply for participating products, predict the next FIFA World Cup 2026 Champion, and win your share of up to S$30,000 cash. Applicable to the first 16 successful applicants at 2 PM and 8 PM daily only. Valid till 28 June 2026. T&Cs apply.

Or, apply and post creative World Cup content on Facebook or Instagram, tag SingSaver, and use #SingSaverWorldCup to win a Golden Ticket, giving you one chance to predict the winning team. Valid till 28 June 2026. T&Cs apply.

SingSaver Exclusive Offer

⚽ Make your move this World Cup season. Compare top brokerage deals on SingSaver, then apply to score exclusive upsized rewards this June. Make every play count. 📈🏆 T&Cs apply.

Make the most of every trade. 📊

Set up your account in under 5 minutes, explore your options with ease, and enjoy exclusive rewards as you grow your portfolio. 🪙🏆T&Cs apply.

Plan for what truly matters

Want to take charge of your financial future? Learn how to set clear, achievable goals that align with your life priorities.

Step 3: Keep track of your spending

Variable expenses change based on your daily lifestyle choices. Because these costs fluctuate wildly, they are usually the primary reason a budget goes off track.

-

Food: Groceries, daily food court meals, and weekend café visits or restaurant dining.

-

Transport: Daily public transit via SimplyGo (MRT/buses) or ride-hailing services like Grab, Gojek, and Tada.

-

Lifestyle & Entertainment: Streaming platform subscriptions (Netflix, Spotify), shopping, hobbies, and social gatherings.

To make tracking simple, use tools that seamlessly sync your financial data. While dedicated spreadsheets work beautifully, modern bank systems like DBS NAV Planner or OCBC Financial Masterpiece leverage SGFinDex (Singapore Financial Data Exchange) to automatically pull and categorize your actual spending across multiple financial institutions, making tracking virtually effortless.

Step 4: Set up automatic savings

The most effective way to protect your money from your own spending urges is to automate your savings. The moment your salary hits your primary bank account, an automated standing instruction should immediately route a percentage of your income to a separate account.

To make your savings work harder, look for high-yield savings accounts that reward you for everyday behavior. Popular options include:

-

UOB One Account: Offers strong baseline interest when you hit a minimum monthly card spend combined with salary credit or GIRO bills.

-

OCBC 360 Account: Rewards you with staggered bonus interest rates as you save, spend, and insure or invest through them.

-

DBS Multiplier: Ideal for multi-category banking structures, calculating bonus tiers based on your collective monthly financial interactions.

Note: High-interest bank account promotional rates shift over time based on macroeconomic environments, so remember to periodically verify current tiers on official bank portals.

Creating a personal budget

When you are actively creating a personal budget, staring at a blank screen can feel incredibly overwhelming. Utilizing a structured, visual dashboard allows you to clearly map out your fixed vs. variable spending alongside your long-term wealth goals.

A robust personal budget template serves as a vital financial mirror. It allows you to enter your projected targets alongside your actual cash outcomes, keeping you completely honest about your real-world spending habits.

How to prepare a budget plan

To successfully prepare a budget plan that actually sticks long-term, you need an intuitive, globally proven allocation system. One of the best starting frameworks for Singaporeans is the widely popular 50 30 20 rule.

[ Your Take-Home Pay ]

│

├──► 50% Needs (Rent/Mortgage, Utilities, Groceries, Insurance)

├──► 30% Wants (Dining out, Café runs, Shopping, Streaming)

└──► 20% Financial Goals (Emergency savings, Investments)

Here is exactly how to break down your net income using this structural approach:

-

50% for Needs: Half of your net income is explicitly reserved for essential living expenses. This covers your housing obligations, transport, basic groceries, health insurance, and standard utility bills.

-

30% for Wants: This is your guilt-free spending allowance. It funds your lifestyle choices, social dinners, movie tickets, travel savings, and non-essential shopping.

-

20% for Financial Goals: This portion is set aside for your future self. It should be aggressively channeled into building your 6-month emergency cash cushion, contributing to long-term investment portfolios, or making voluntary top-ups to your CPF accounts.

Step 5: Review and adjust your budget regularly

Life changes — so should your budget. Whether you're getting married, buying a home, having a child, or switching jobs, your financial priorities will shift. Adjust your savings, spending, and investment allocations accordingly.

Avoid lifestyle inflation by resisting the urge to increase expenses just because your income rises. Instead, direct extra funds into savings or investments to build long-term financial security. Review your budget every three to six months and refine it as needed to ensure it aligns with your current financial situation.

Set clear priorities for your budget

Before tackling debt or investments, set aside some cash for unexpected expenses. Financial experts often suggest having several months’ worth of essential expenses saved. However, starting with at least $500 to $1,000 can provide a safety net for minor emergencies, such as urgent repairs or medical costs.

If saving this amount upfront isn’t feasible, set aside a small portion of each paycheck — even $50 a month can make a difference. Without this cushion, you may end up relying on credit cards or loans, which can lead to costly debt cycles.

While it might feel disheartening to see a portion of your salary deducted for CPF, these contributions are a crucial part of your long-term financial security. In Singapore, employers are required to contribute 17% of your salary to CPF, on top of the 20% you contribute yourself.

Unlike voluntary retirement plans in other countries, CPF is compulsory, ensuring you build savings for housing, healthcare, and retirement. Since these contributions grow over time through government-guaranteed interest rates, they play a key role in wealth accumulation.

Rather than viewing CPF deductions as a loss, think of them as a forced savings plan that secures your future — so make sure you’re maximizing the benefits available to you.

High-interest debt — like credit cards, personal loans, or payday loans — can drain your finances quickly. These debts accumulate interest fast, meaning you could end up paying double or even triple the original amount borrowed.

If you’re struggling to keep up with payments, consider:

-

Debt consolidation to combine multiple loans into one with a lower interest rate.

-

Repayment plans to negotiate lower monthly payments.

-

Seeking professional advice if your total unsecured debt equals 50% or more of your gross income.

-

Once your high-interest debts are under control, focus on long-term financial security. Aim to save 10–15% of your income for retirement through CPF or investment accounts like a Supplementary Retirement Scheme (SRS) account.

If you don’t have access to CPF, consider alternatives like:

-

Robo-advisors (e.g., StashAway, Syfe) to automate your investments.

-

Exchange-traded funds (ETFs) or index funds for long-term growth.

Starting early allows you to take advantage of compounding interest, which can significantly grow your savings over time.

-

After addressing immediate financial concerns, continue building your emergency fund. Ideally, you should save three to six months’ worth of essential expenses, such as rent, utilities, and groceries. This ensures financial stability in case of job loss, medical emergencies, or other unexpected events.

It’s normal for this fund to fluctuate, as emergencies will arise. The key is to replenish it regularly to maintain financial security.

Once your most urgent debts are cleared, focus on other outstanding balances like student loans, auto loans, or mortgages. These debts typically have lower interest rates and may even offer tax benefits.

To make faster progress, allocate any extra funds from discretionary spending or small savings from daily expenses — without sacrificing retirement contributions or emergency savings.

If you’ve built financial stability, congratulations! Now, you have more flexibility to plan for personal goals such as:

-

Buying a home: Set aside funds for a down payment to reduce future loan amounts.

-

Investing in passive income: Consider stocks, ETFs, or real estate for long-term wealth growth.

-

Saving for lifestyle goals: Whether it’s a dream vacation, further education, or starting a business, having dedicated savings for personal goals helps you stay on track without dipping into emergency funds.

Some banks and budgeting apps even allow automatic savings “buckets” where you can allocate money for different purposes. The more you plan, the faster you’ll reach financial freedom.

-

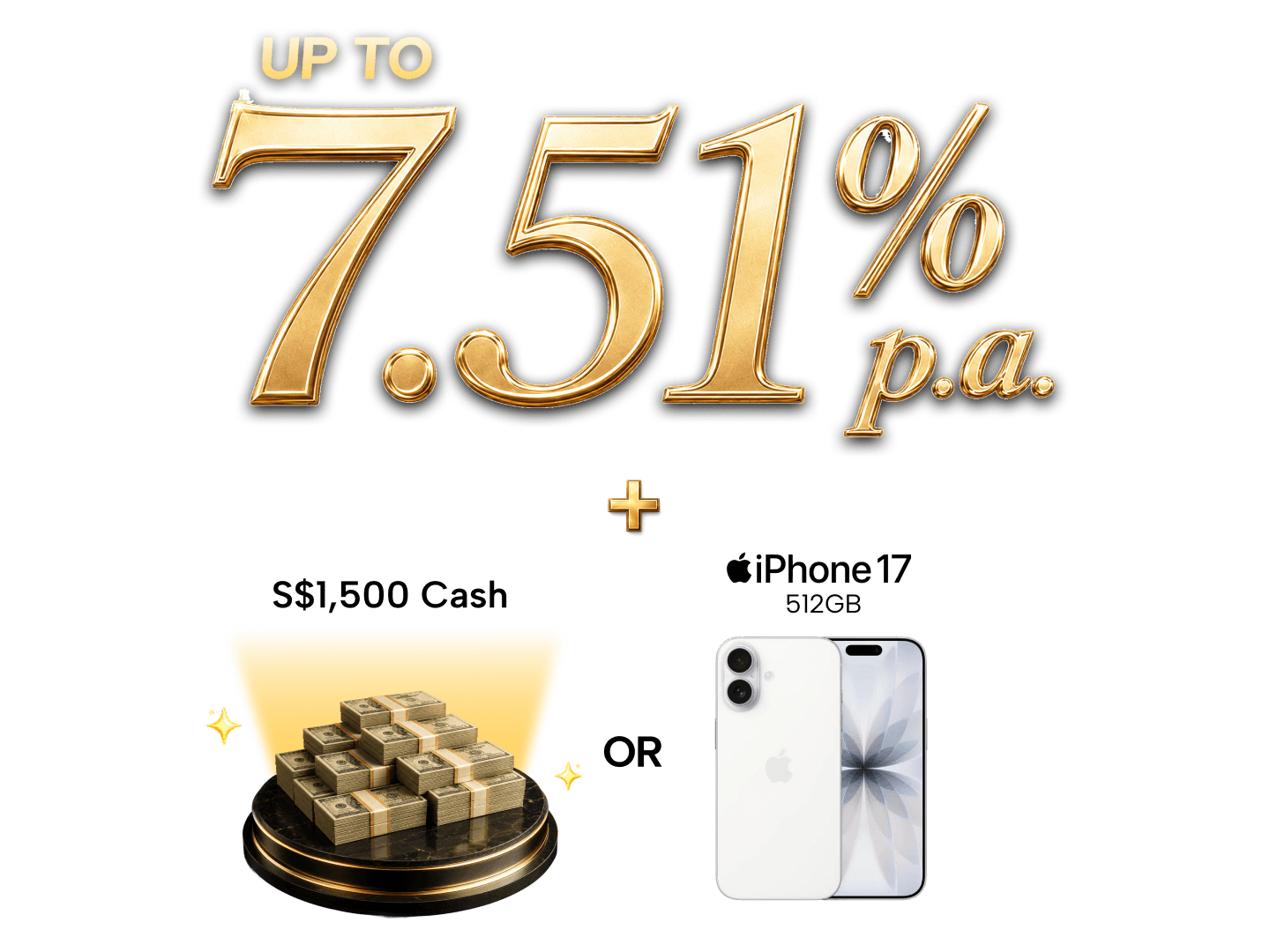

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 30 June 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 30 June 2026. T&Cs apply.

Top budgeting tips

-

Build an emergency cushion first: Before allocating a single dollar toward higher-risk investments, ensure you have saved three to six months' worth of essential living expenses inside a highly liquid, safe bank account.

-

Pay yourself first: Treat your savings goal exactly like a bill that must be paid. Do not wait to see what cash is "leftover" at the end of the month to save. Save first, then freely spend the remainder.

-

Review subscription drift: Go into your bank statements once every quarter and aggressively cancel unused digital memberships or streaming services that automatically bill you in the background.

Maximise your CPF contributions

For Singaporeans and Permanent Residents, optimizing your CPF structure is a foundational pillar of smart wealth management. Because CPF balances earn compounding, risk-free interest rates backed by the Singapore government, it serves as a powerful retirement engine.

-

Voluntary Top-ups (RSTU Scheme): You can perform cash top-ups to your Ordinary Account (OA) or Special Account (SA) / Retirement Account (RA) to capture higher interest rates and claim attractive tax reliefs up to prevailing statutory limits.

-

Know Your Retirement Sums: The key reference metrics for your long-term retirement planning scale predictably over time.

-

The Age 55 Structural Reset: It is crucial to understand that when you turn 55, your Special Account (SA) is closed. Your SA savings, along with your OA savings up to your Full Retirement Sum, are automatically consolidated into a brand-new Retirement Account (RA) to fund your lifelong CPF LIFE payouts. Remaining balances sleep safely in your OA, where you can still choose to manually transfer them into your RA up to the enhanced limits to lock in optimal interest yields.

CPF Retirement Sums Reference

| Metric | Purpose | 2026 Financial Thresholds |

| Basic Retirement Sum (BRS) | The foundational minimum baseline required for your retirement account if you own a property with a sufficient lease charge. | S$110,200 |

| Full Retirement Sum (FRS) | The standard retirement target, equivalent to two times the BRS. | S$220,400 |

| Enhanced Retirement Sum (ERS) | The absolute maximum cap allowed for RA top-ups, allowing you to maximize lifelong monthly CPF LIFE payouts. | S$440,800 |

Summary: Your financial road map

A budget shouldn't feel like a financial straightjacket; it is a tool that grants you absolute freedom over your lifestyle choices. By executing these strategic steps—calculating true take-home pay, mapping expenses via the 50 30 20 rule, and utilizing a visual template—you lay a permanent path toward true financial peace of mind.

Relevant articles

A Step-by-Step Guide to Financial Planning in Singapore

Creating a solid financial plan is like mapping out your route to financial success. It's about understanding where you are now, where you want to be, and how you'll get there. This guide provides a step-by-step approach to financial planning, with a focus on strategies and resources relevant to Singaporeans.

About the author

Afina Najib

Spending most of her young writer's phase working as a freelancer, Afina's written for various industries ranging from e-commerce, travel to health and finance. Her expertise lies in her ability to make complex subjects like finance easy to consume for everyday readers.