7 Ways to Track Monthly Expenses in Singapore

Updated: 12 Dec 2025

Figuring out where your hard-earned money goes each month is the first step towards achieving your financial goals and gaining better control over your finances in Singapore.

Understanding where your money goes each month is a fundamental aspect of sound personal finance.

In Singapore, with its vibrant economy and diverse spending opportunities, keeping tabs on your monthly expenses can feel like a daunting task. However, by implementing effective strategies for tracking expenses, you can gain valuable insights into your spending habits, identify areas for potential savings, and ultimately work towards a more secure financial future.

This guide will walk you through practical methods to effectively monitor your monthly expenditure and take control of your financial well-being in Singapore.

SingSaver Personal Loan Cashback Offer

Enjoy one of the lowest interest rates from 0.90% p.a. (EIR from 1.75% p.a.) and up to S$6,500 in cashback when you apply for a personal loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

1. Review your account statements

The first critical step to understanding your financial flow is to thoroughly review your bank and credit card statements, along with any other financial transaction records. This detailed examination allows you to pinpoint exactly where your money is going each month.

By doing so, you can clearly distinguish between your fixed expenses — consistent monthly outlays like rent, utilities, insurance, and loan repayments — and your variable expenses, which fluctuate based on spending on items like groceries, transport, entertainment, and shopping. Recognising this difference can help identify areas where you have the most flexibility to adjust your spending habits and improve your expenditure tracking.

Compare credit cards to optimise your spending

Understanding your monthly expenses is the first step. The right credit card can help you earn rewards or cashback on your spending, effectively stretching your dollar further.

Find the right credit card for you in no time. 💳✨

Compare exclusive offers on SingSaver across cashback, miles, and rewards cards—plus enjoy stackable welcome gifts.

2. Group your spending categories

Simply knowing the amounts you've spent isn't enough; understanding what you're spending on is equally important. This is where categorising your expenses comes into play. By grouping similar expenses together, you can better understand where your money is going and identify areas where you might be overspending.

Many personal finance tools and even some credit card statements offer automatic categorisation features, tagging purchases under headings like "Dining," "Groceries," "Transport," or "Entertainment." Pay close attention to these categories, as they can reveal surprising insights into your spending habits.

For instance, you might discover that those frequent takeaway coffees or impulse buys are collectively taking a significant bite out of your monthly expenditure. Focusing on these high-impact areas, where you spend a considerable amount, can often lead to quicker and more noticeable improvements in your overall financial health.

>> Read more: Cost of living in Singapore

3. Develop a budget that aligns with your spending

After categorising your spending, the next essential step is to create a budget tailored to your financial life. Think of a budget as your personal guide for allocating your funds and making informed spending choices.

A common framework is the 50/30/20 rule: allocate around 50% of your income to essential needs, 30% to discretionary wants, and 20% to savings and debt repayment.

Beyond this, consider "Reverse Tracking" — planning your budget categories and amounts upfront and then monitoring your actual spending. This method helps control your monthly expenditure. The "Envelope System" is another tangible approach, allocating cash to specific categories like groceries or transport, providing a visual way to track monthly expenses and stick to your budget.

What are “needs”?

"Needs" are the expenses that are essential for your survival and daily functioning. These are typically non-negotiable and form the foundation of your monthly expenditure. According to the 50/30/20 framework, these should ideally account for around 50% of your net income. Common examples of needs include:

-

Housing: Rent or mortgage payments, property tax (if applicable and not included in mortgage), and essential home insurance.

-

Transportation: Costs associated with getting to work and other essential destinations, such as public transport fares (MRT, buses), car payments, petrol, vehicle insurance, and maintenance.

-

Healthcare: Health insurance premiums and out-of-pocket medical expenses.

-

Basic utilities: Electricity, water, gas, internet, and mobile phone bills.

-

Groceries and essential household items: Food, toiletries, and other necessary household supplies.

-

Childcare and education costs: If applicable, expenses related to raising children and their schooling.

-

Minimum debt payments: The minimum amounts required to service your loans and credit card balances.

What are “wants”?

"Wants" are the discretionary expenses that enhance your lifestyle but are not strictly essential for survival. These can be more challenging to manage as they often involve impulsive purchases and entertainment. The 50/30/20 rule suggests allocating around 30% of your net income to these categories. Examples of wants include:

-

Dining out and ordering takeaways.

-

Entertainment activities like movies, concerts, and social events.

-

Shopping for non-essential items such as new clothes, gadgets, and home decor.

-

Subscription services for streaming platforms or other non-essential services.

-

Travel and holidays.

-

Hobbies and recreational activities.

Understanding savings and debt repayment

The final category in the 50/30/20 budget is "Savings and Debt Repayment," which ideally accounts for 20% of your net income. This portion of your funds should be directed towards building your financial security and reducing your liabilities. This includes:

-

Building an emergency fund to cover unexpected expenses.

-

Contributing to savings accounts for future goals (e.g., down payment on a house, retirement).

-

Investing in financial instruments to grow your wealth over time.

-

Making extra payments on high-interest debts like credit cards and personal loans, beyond the minimum required.

Setting clear financial goals can provide strong motivation for prioritising savings and debt repayment. Whether it's saving for a dream vacation or planning for retirement, having specific targets in mind can make it easier to stay disciplined with your monthly expenses and allocate funds effectively towards your future.

SingSaver x CIMB Personal Loan Exclusive Offer

Enjoy attractive interest rates from 1.28% p.a. (EIR from 2.46% p.a.) when you get approved for a loan with a minimum tenure of 3 years. Available to new customers only. Valid till 2 August 2026. T&Cs apply.

4. Leverage budgeting and expense-tracking apps

In today's digital age, numerous budgeting and expense-tracking applications are available to simplify your financial management. These apps often sync with your Singaporean bank accounts and credit cards, providing a real-time overview of your transactions, saving you the effort of manual logging.

Many also offer features like automatic spending categorisation, customisable budget creation, goal setting, and insightful reports on your spending patterns.

Popular options in Singapore include Planner Bee, DBS NAV Planner, and YNAB. These tools allow you to set spending limits for various categories and receive alerts as you approach them, enhancing your ability to track monthly expenses efficiently and make informed financial decisions.

5. Explore alternative methods for monitoring expenditure

Beyond popular apps, consider these other effective ways to monitor your spending in Singapore:

Reverse tracking: Plan your budget in detail before the month begins, then carefully track your actual spending against these planned amounts. This helps you pinpoint where your spending habits deviate from your intentions, allowing for adjustments in future months. Identifying where you frequently exceed your budget provides valuable insights into your spending weaknesses.

Targeted tracking: Instead of tracking every single expense, concentrate on one or two specific spending categories you want to manage more closely. For instance, if you're looking to reduce your dining expenses in Singapore, focus solely on tracking every dollar spent on meals outside your home for a month. This financial planning approach can provide a clearer understanding of your spending in those key areas, making it easier to find potential savings.

Envelope system: This is a tangible, cash-based budgeting method. Allocate a specific amount of physical cash to different spending categories relevant to your lifestyle (e.g., groceries at local markets, transport via MRT/buses, entertainment). Place this cash in separate envelopes. Once an envelope is empty, you've reached your spending limit for that category for the month. This visual method can be particularly effective for controlling discretionary spending and provides a clear, physical representation of your budget.

6. Identify opportunities to reduce your expenses

As you consistently track monthly expenses, you'll inevitably identify areas where you can potentially cut back on your spending. This could involve both your fixed and discretionary expenses.

For significant fixed expenses like housing and transportation, explore options such as refinancing your mortgage (if applicable), considering a more fuel-efficient vehicle, or evaluating your current utility providers for better rates. For variable expenses, look for smaller, more frequent savings opportunities, such as reducing the frequency of dining out, finding more affordable entertainment options, or cutting down on impulse purchases. Even small reductions in multiple spending categories can add up to big savings over time, freeing up more funds for your financial goals.

7. Explore ways to increase your income

If you've diligently explored all avenues for lowering your expenses and still struggle to meet your financial goals, consider exploring ways to increase your income. In Singapore, various opportunities exist to supplement your primary income. This could involve taking on a part-time job or a side hustle that aligns with your skills and interests.

You could also consider selling items you no longer need online through various platforms available in Singapore. Freelancing or offering your expertise on a project basis can also be a viable option. Exploring these avenues to earn more money can provide additional financial flexibility and accelerate your progress towards your financial objectives. Remember to factor in any tax implications of additional income earned in Singapore.

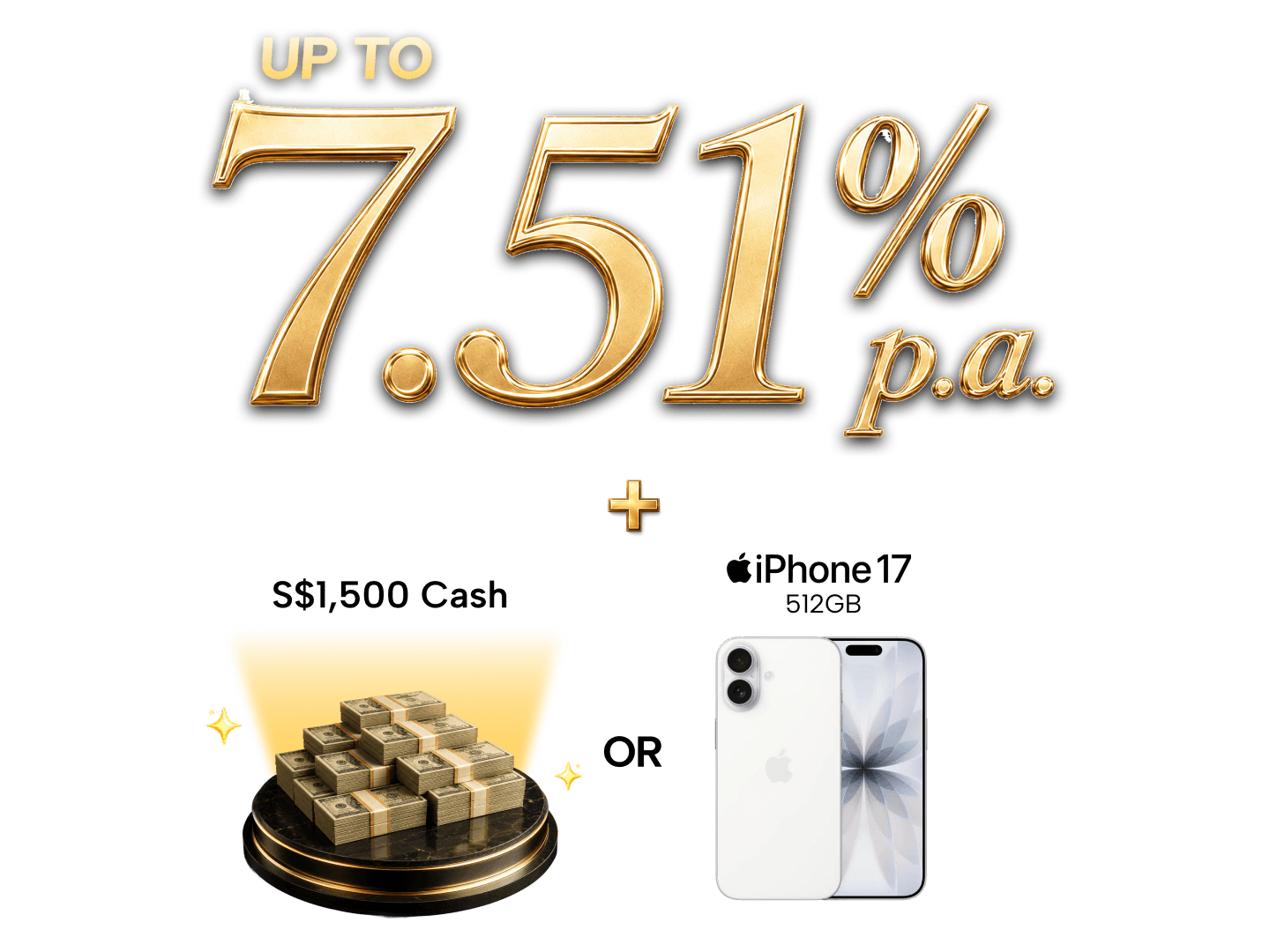

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.