HSBC Everyday Global Account

S$70000

Updated: 4 Jun 2026

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

The era of peak interest rates has officially transitioned into a more stable, normalized environment. With the U.S. Federal Reserve continuing its rate-cutting cycle and Singapore banks following suit, the strategy for finding the best savings account singapore has shifted. Gone are the days of effortless 7% yields; today, maximizing your returns requires a more tactical approach.

Whether you are looking for a high yield savings account singapore for your salary or a simple place to park your emergency fund, here is the updated analysis of where to find the high interest savings accounts singapore this year.

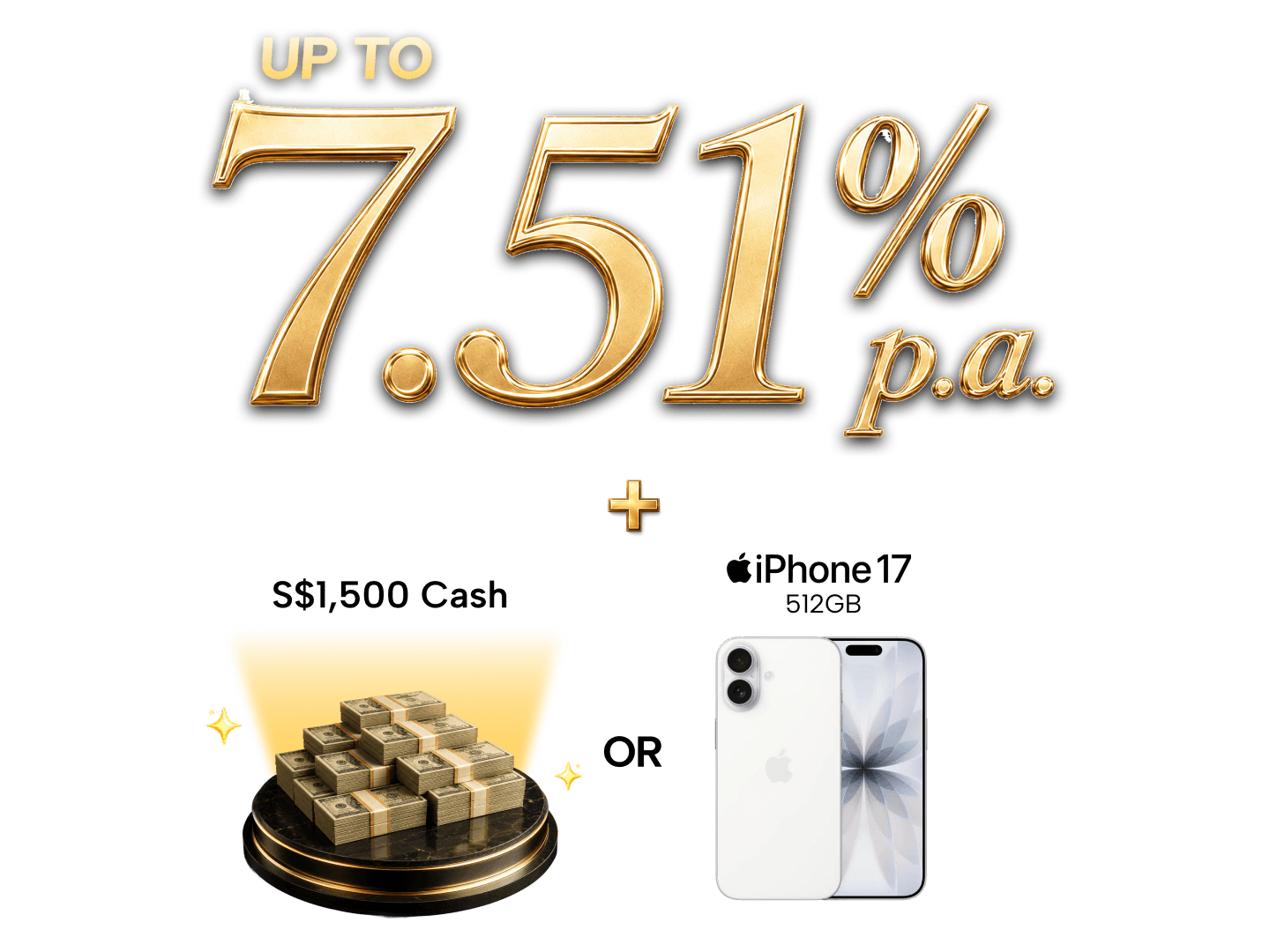

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

Grow your money with these low-free, high-interest accounts

The BOC SmartSaver account remains a competitive choice for high-spenders, now offering a maximum interest rate of up to 4.60% p.a. (revised from previous highs) for those who meet all criteria. By combining salary crediting of at least S$3,000, card spending, and bill payments, account holders can maximize returns. However, the most significant portion of interest (3.0%) is now tied to wealth products, making it less of a "pure" savings play for most.

The above information is provided by SingSaver.com.sg for information purposes only. In case of any discrepancy between the information provided by SingSaver.com.sg and relevant information provided by banks, card issuers or card providers (*partner institutions), the information provided by the partner institutions shall prevail. For more information, please refer to our Terms & Conditions and Privacy Policy page.

The HSBC Everyday Global Account is tailored for affluent customers, especially those eligible for HSBC Premier. With its multi-currency capabilities and attractive welcome offers, it's suitable for individuals with significant assets and international banking needs.

While some accounts advertise higher interest rates, the best savings account for you depends on whether you can consistently meet the conditions required to unlock those rates.

The table below outlines our recommendations based on the maximum interest rate, against what you could realistically expect to save every month. Those who watch their bills or are certain of their salary can try maximising their savings, while others may wish to just park the money and forget about it, in which case using a more flexible account is more suitable.To find out which is the best savings account for salaried workers, let's say a typical salaried worker:

| Savings Account | Maximum Interest Rate (p.a.) | Realistic Interest Rate (p.a.) |

| OCBC 360 | 5.45% (Drops to 4.45% on May 1) | 1.95% – 2.45% (Salary + Save + Spend) |

| UOB One Account | 1.90% | 1.00% – 1.90% (Salary + Spend) |

| DBS Multiplier | 4.10% | 1.80% – 2.10% (Salary + 1-2 categories) |

| SC Bonus$aver | 7.05% | 2.05% (Salary + S$1k Card Spend) |

| BOC SmartSaver | 4.60% | 1.30% – 1.60% (Salary + Spend + Bills) |

| Trust Savings Account | 2.40% | 1.00% – 1.50% (Salary + 5 Card Spends) |

| HSBC Everyday Global | 2.80% | 1.65% – 1.80% (Fresh funds + Everyday+) |

| CIMB FastSaver | 2.30% | 1.50% – 1.90% (Tiered; no salary needed) |

| UOB Stash | 1.50% | 1.00% – 1.50% (Consistent balance growth) |

| Maybank Save Up | 4.00% | 1.25% – 2.50% (Depends on linked products) |

| SIF GoSavers | 1.30% | 1.30% (Flat rate on first S$100k) |

| GXS Savings Account | 1.22% | 1.22% (Boost Pocket 3-month rate) |

| Mari Savings Account | 0.88% | 0.88% (Flat rate; promo ended) |

| SC JumpStart | 2.00% | 2.00% (First S$50k; for ages 18–26) |

| RHB High Yield | 1.50% | 1.20% (On first S$50k) |

OCBC 360 vs. UOB One: OCBC currently holds the higher realistic rate for the "Salary + Save + Spend" crowd at 2.45%, but this will drop to 1.95% on May 1, 2026. UOB One has already settled at a maximum effective rate of 1.90%.

The "Digital Bank" Shift: Both GXS and MariBank have lowered their base rates significantly since 2024. GXS now relies on its Boost Pockets (lock-in) to reach 1.22%, while MariBank has reverted to a base rate of 0.88%.

Trust Bank: Remains the most competitive digital-first option, offering up to 2.40% if you can hit salary and investment targets, or a more realistic 1.50% for Union members with salary credit.

High-Water Mark: Standard Chartered Bonus$aver still lists 7.05%, but this requires massive insurance/investment premiums. For a typical salaried worker, the rate is much closer to 2.05%.

Strategic Tip: If your bank's realistic rate is now below 2.50%, consider moving excess cash to the CPF Ordinary Account (guaranteed 2.5%) or 6-month T-Bills, which are still yielding roughly 3.4% – 3.7% as of mid-April 2026.

To maximize the latest high-interest accounts, our typical worker now:

Has S$20,000 in savings (The "Emergency Fund" baseline);

Credits a salary of at least S$2,000 (Meeting the basic threshold for OCBC and UOB);

Spends at least S$500 on a credit/debit card (The standard "Spend" requirement);

Performs 3 GIRO or PayNow transactions (Replacing the old "Bill Payment" category).

From these updated criteria, here is the annual interest you’ll earn across the top accounts as of April 16, 2026:

| Savings Account | Interest Rate (p.a.) | Annual Interest Earned (S$) |

| OCBC 360 Account | 2.05% | S$410.00 |

| DBS Multiplier | 1.80% | S$360.00 |

| HSBC Everyday Global | 1.65% | S$330.00 |

| CIMB FastSaver | 1.50% | S$300.00 |

| UOB One Account | 1.00% | S$200.00 |

| Trust Savings Account | 1.00% | S$200.00 |

| GXS Savings Account | 1.22% | S$244.00 |

| Mari Savings Account | 0.88% | S$176.00 |

| BOC SmartSaver | 0.60% | S$120.00 |

Take note that these are estimates only, and it is best to consult the bank or financial organisation itself for further details.

UOB One's Balance Trap: In previous years, UOB One was highly competitive. However, in 2026, the bank has heavily "back-loaded" its interest. If you only have S$20,000, you are stuck in the lowest tier (1.00%). You only unlock the higher effective rates once your balance crosses S$100,000.

The "Bill Payment" Shift: Banks like OCBC and UOB no longer give bonus interest just for paying bills. You now get rewarded for the "Save" category (increasing your balance by S$500 monthly) or GIRO/PayNow debits.

OCBC 360 Stability: OCBC remains the strongest for this specific profile (Salary + Spend) because their bonus interest applies to the first dollar of your balance, unlike tiered accounts that penalize smaller balances.

Digital Bank Cooling: Since the 2024–2025 "hype" phase, MariBank and GXS have lowered their base rates. GXS now requires you to lock money into a 3-month Boost Pocket to even reach 1.22%.

Which one should you choose?

If you have exactly S$20,000, the OCBC 360 is your best bet for pure yield. If you value a "no-hoops" experience, CIMB FastSaver is the superior choice as it doesn't require the salary or spend categories to hit its 1.50% mark.

If you're drawing a monthly salary, many banks offer bonus interest rates when you credit your salary into your savings account. These accounts are designed to reward everyday banking behaviours such as paying bills, spending on credit cards, and even investing or insuring with the same bank. The more you do with one bank, the more interest you earn.

Effective May 1, 2026, OCBC has revised its flagship 360 account. While the headline rate has dipped from the highs of 2024, it remains a dominant bank with highest interest rate singapore for salaried professionals who can consolidate their financial life.

Maximum Rate: Up to 4.45% p.a. (on the first S$100,000).

Realistic Rate: Approx. 2.05% - 2.45% p.a. (Salary + Save + Spend).

Key Change: The "Save" bonus has been streamlined to 0.40%–0.80% based on tiered balances, and the "Spend" bonus now sits at 0.25% p.a.

| Category | Bonus Interest (p.a.) | Your Qualification |

| Salary | 1.20% | YES (S$2,000 credited) |

| Spend | 0.40% | YES (S$500 spent) |

| Save | 0.40% | Optional (If you add S$500/month) |

| Base Rate | 0.05% | YES (Standard) |

| Total Rate | 2.05% | For your profile |

1. Lower Barriers to Entry

Unlike the BOC SmartSaver, which now requires a S$3,000 salary to unlock its bonus, or the UOB One, which only pays meaningful interest on balances above S$75,000, OCBC 360 allows a mid-income earner with a modest nest egg to actually see significant returns.

2. The "Salary + Spend" Sweet Spot

Most banks have complicated their "Bill Payment" or "GIRO" categories in 2026. OCBC keeps it simple: as long as your salary comes in and you use an OCBC credit card (like the 365 Card for 5% dining cashback), you hit the 2% mark.

3. Safety in the OCBC Ecosystem

With the "normalization" of interest rates, many digital banks (MariBank/GXS) have dropped their rates to 0.88% – 1.22%. By staying with a major local bank like OCBC, you get the security of a Tier-1 bank while still outperforming digital-only competitors by nearly double the interest.

One Final Tip: If you are willing to lock away some of that S$20,000, consider the OCBC Money Lock feature. In 2026, many banks offer an additional 0.05% to 0.10% "security bonus" for locking your funds, which protects you from digital scams while slightly boosting your yield.

Not everyone receives a monthly salary in Singapore — and in 2026, that’s no longer a barrier to earning competitive interest. Whether you’re self-employed, a gig worker, or retired, these accounts let you earn steady returns without salary crediting or mandatory credit card spend.

These accounts are ideal for those who value flexibility. For instance, the UOB Stash Account remains a top-tier choice for consistent savers, now offering up to 2.00% p.a. for those who grow their balance month-on-month. Meanwhile, digital leaders like MariBank and GXS have standardized their rates at 0.88% to 1.30% p.a., providing a baseline for everyday liquid cash.

| Savings Account | Realistic Interest Rate (p.a.) | Requirement Highlights |

| UOB Stash | 1.40% – 2.00% | Maintain or increase Monthly Average Balance (MAB) |

| CIMB FastSaver | 1.50% – 1.90% | Tiered rates on balance; extra 0.30% for fresh funds |

| GXS Savings Account | 1.08% – 1.30% | 1.08% on "Saving Pockets"; up to 1.30% on "Boost Pockets" |

| SIF GoSavers | 1.30% | Flat rate on first S$100,000; no hoops |

| RHB High Yield Savings | 1.00% – 1.50% | Tiered rates; best for balances above S$100,000 |

| Mari Savings Account | 0.88% | Simple flat rate on all balances (up to S$100k) |

| Standard Chartered Bonus$aver | 1.00% | Base rate for non-salary/non-spenders |

For Larger Balances (S$50k – S$100k): The UOB Stash is the winner here. As long as your balance this month is S$1 higher than last month, you earn a bonus that brings your total interest up to **2.00%** on the "Next S$30,000" tier (effectively 1.50% EIR on S$100k).

For Digital Convenience: GXS Bank outperforms MariBank in 2026 by offering 1.08% on its Saving Pockets and the ability to lock in 1.30% via "Boost Pockets" for tenures as short as 1 to 3 months. MariBank remains the simplest with a flat 0.88%, but is currently less competitive on yield.

For Stability & Fresh Funds: CIMB FastSaver is excellent if you are moving money from another bank. They currently offer a 0.30% p.a. fresh funds bonus (valid through April 30, 2026), which can push your yield toward 1.90% for certain tiers without any salary or spend requirements.

For Absolute Simplicity: SIF GoSavers is a "park and forget" account. It offers a flat 1.30% on the first S$100,000 with zero conditions, making it the most predictable option for retirees.

| Savings Account | Minimum Balance (ADB) | Fall Below Fee (Monthly) |

| OCBC 360 | S$3,000 | S$2 (Waived for first year) |

| DBS Multiplier | S$3,000 | S$5 (Waived if age ≤ 29) |

| HSBC Everyday Global | S$2,000 | S$5 |

| UOB One Account | S$1,000 | S$5 |

| UOB Stash | S$1,000 | S$2 |

| BOC SmartSaver | S$3,000* | S$7.50 |

| SC Bonus$aver | S$3,000 | S$5 |

| CIMB FastSaver | None | None |

| Maybank Save Up | S$1,000 | S$2 |

| RHB High Yield | S$500 | S$2 |

| SIF GoSavers | None | None |

| Trust Savings Account | None | None |

| GXS Savings Account | None | None |

| Mari Savings Account | None | None |

| SC JumpStart | None | None (Age 18–26) |

With banks "normalizing" interest rates downwards this year, finding the best account now depends more on your liquidity needs and digital habits than just the headline rate.

The "Clean & Clear" Winner: CIMB FastSaver Account If you want to avoid the "complexity trap," CIMB remains the strongest traditional choice. It offers up to 1.50% p.a. without requiring salary credit or card spend—making it the ideal "set and forget" account for those who don't want to track monthly criteria.

Best for Salaried Workers: OCBC 360 or DBS Multiplier Despite the May 1, 2026 rate revisions, the OCBC 360 is still our top pick for salaried workers. It yields a realistic 2.05% p.a. for a simple "Salary + Spend" combo. If you're under 29, the DBS Multiplier is a strong runner-up because its fall-below fees are waived, and its entry tiers are very accessible.

Best for Large, Quiet Balances: UOB Stash Account The UOB Stash rewards those who simply let their money sit and grow. With realistic returns reaching 2.00% p.a. for larger balance increments, it’s a safer, more predictable alternative to fluctuating digital bank rates.

Best for Digital Agility: GXS Bank While MariBank has cooled off, GXS remains competitive via its "Boost Pockets." If you’re willing to lock your funds for just 1 to 3 months, you can earn up to 1.30% p.a.—significantly higher than a standard base savings rate, with a seamless, fee-free mobile experience.

Bottom Line: In 2026, the best account is the one that doesn't eat your interest in fees. If you can't maintain a S$3,000 balance, stick to the digital banks or CIMB to ensure you aren't paying S$5 a month just to keep your account open.

Read reviews of the various savings accounts in Singapore and what each account has to offer to find the best product for your needs:

It’s advisable to keep three to six months’ worth of expenses in your savings account for emergencies. This ensures quick access to cash when needed without tapping into investments.

Depending on the account, you could earn between $5 to $60 a year on $1,000, assuming interest rates range from 0.5% to 6% p.a. Choose a high-interest account to maximise your earnings.

You can split your savings. Keep a portion in a high-interest savings account for liquidity, and consider investing the rest in low-risk instruments like fixed deposits, T-bills, or robo-advisors for better returns.

Yes, through compound interest. While it won’t make you rich, parking your money in a high-yield account can generate passive income over time, especially when paired with consistent saving habits.

Compare interest rates, minimum balance requirements, fees, and bonus criteria. Choose one that aligns with your income type, banking habits, and whether you prefer fuss-free or reward-based accounts.

Compare interest rates, minimum balance requirements, fees, and bonus criteria. Choose one that aligns with your income type, banking habits, and whether you prefer fuss-free or reward-based accounts.

It typically takes 15 minutes to open an online savings account using MyInfo via Singpass. Some banks may require additional verification or document uploads.

It refers to the interest earned only on the portion of your balance that falls within a certain tier. For example, 0.5% on the first $10,000, and 2% on the next $20,000 — not a flat rate across your full balance.

A savings account earns interest and is used to store money, while a current account is typically used for transactions, with features like cheque books and linked overdraft facilities, but usually no interest.

Students should go for no-fee, easy-access accounts that don’t need salary crediting. Good options include:

Parents can open child or joint accounts with no minimum balance and simple saving tools. Popular picks include:

OCBC Mighty Savers®: Bonus interest for regular deposits; no fall-below fee for kids under 16.

POSB My Account: No minimum deposit, grows with your child through youth to adulthood.

UOB Junior Savers: Easy transfers from a parent’s UOB account; encourages early saving habits.

Stay up to date with the latest insights on saving smarter, comparing high-interest accounts, and finding ways to grow your money faster — all designed to help Singaporeans make confident, well-informed financial decisions.

Simply complete this short form and stand to score the Apple iPhone 17 Pro worth S$1,749!

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.