CareShield Life helps you with long-term care costs related to disability. To increase your disability protection and payouts, you can upgrade your CareShield Life with supplements from these three private insurers: Great Eastern Life, Singlife and NTUC Income.

For the uninitiated, CareShield Life is a long-term care insurance scheme that provides financial support and monthly payouts for Singaporeans who are severely ill or disabled.

But more often than not, the financial support from CareShield Life is usually insufficient because of the high expenses you'll incur from long-term disabilities. As such, getting a CareShield Life supplement plan can help boost your payouts and lessen the financial burden on you and your loved ones.

Table of contents:

- CareShield Life vs ElderShield: what’s the difference?

- Why should you upgrade your CareShield Life plan?

- What are CareShield Life supplements?

- Best CareShield Life supplements plans: Great Eastern Life vs Singlife vs NTUC Income

- Great Eastern GREAT CareShield

- Singlife CareShield Standard

- Singlife CareShield Plus

- NTUC Income Care Secure

- Which CareShield Life supplement should I sign up for?

CareShield Life vs ElderShield: what’s the difference?

When misfortune strikes and you are faced with disability, the last thing you need is financial stress. CareShield Life, which replaces the former ElderShield, is a long-term care insurance scheme that seeks to alleviate the costs of personal and medical care should you become severely disabled.

Unlike ElderShield, which was optional, CareShield Life is compulsory. Singaporeans and Singapore Permanent Residents who are 30 years and above, or those born in 1980 or after are automatically enrolled. It’s optional for those born in 1979 and before.

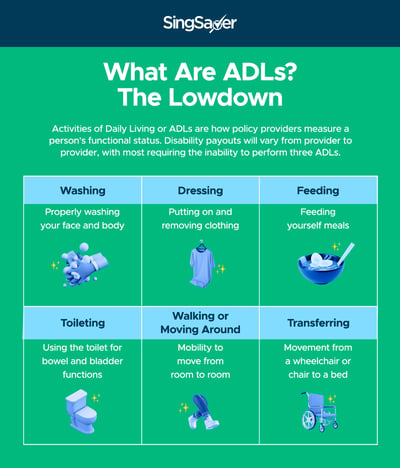

To qualify for CareShield Life, you must be considered severely disabled, in which you’re deemed unable to perform three out of the six Activities of Daily Living (ADLs): washing, dressing, feeding, toileting, walking or moving around, and transferring.

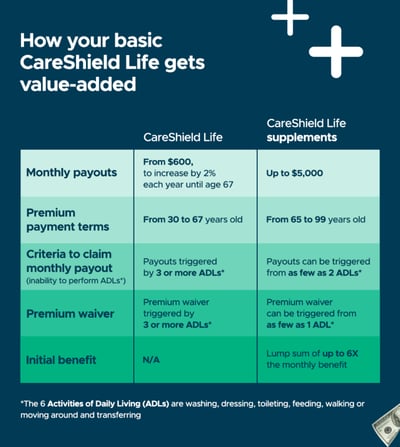

Those under CareShield Life are able to successfully claim lifetime cash payouts of S$600 a month as long as you’re severely disabled, and the monthly payouts will increase annually until you hit 67 years old, or when a successful claim is made, whichever is earlier.

From 2020 to 2025, the payouts will increase at 2% a year. After 2025, your payouts will increase and future adjustments will be decided by an independent council.

Once you’ve made your first successful CareShield Life claim, the monthly payout will stay fixed for the remainder of your disability. In other words, you will continue to receive the same payout even after the adjustments are made to payouts.

It’s also worth noting that if you’re 67 years or older when the scheme is available to you, your monthly payouts are fixed at S$612 per month.

Why should you upgrade your CareShield Life plan?

CareShield Life premiums can be paid via your MediSave account, and have relatively low maintenance. Additionally, your family members (spouse, children, parents, siblings, grandchildren) can also help you to pay with their MediSave accounts, or by topping up your MediSave with cash.

However, let’s face it: $600 per month is peanuts for disability-related treatments, especially if your condition is severe (remember that you can only claim from CareShield Life if you can’t perform at least three of the six ADLs).

What’s more, let’s not forget also that you will likely incur additional costs related to your disability, such as hiring a caregiver or domestic helper to help you with your daily tasks.

Based on Singlife’s long-term care study, long-term care costs alone could rack up to S$2,324 per month on average if you factor in caregiver expenses, medication and therapy. This could cause significant financial strain due to the loss of income if you’re unable to continue working in the event of your disability.

A Ministry of Health study also showed that one in two healthy Singaporeans could become severely disabled in their lifetime and that an estimated three in 10 could be severely disabled for 10 years or more. Causes range from strokes to chronic conditions like diabetes, dementia and even road accidents.

What are CareShield Life supplements?

This is where supplements from private insurers may come in handy to safeguard you from skyrocketing medical and caregiving costs. CareShield Life supplements provide more coverage for both moderate and severe disability, coupled with higher long-term care payouts to minimise any out-of-pocket expenses.

Better yet, CareShield Life supplements’ premiums are eligible for MediSave deduction, capped at S$600 a year. In fact, you can even increase your monthly CareShield Life supplement payouts to up to S$5,000 a year, depending on the plan and premium.

Currently, there are three private insurers that provide CareShield supplements: Singlife, Great Eastern Life, and NTUC Income.

Best CareShield Life supplements plans: Great Eastern Life vs Singlife vs NTUC Income

| CareShield Life Supplement | Sample Premium* | Sample Monthly Payout at Age 30 | Claim Eligibility |

| Great Eastern GREAT CareShieldmonthly b | S$343.12 - Up to age 67 (after 20% discount) | S$300 (excludes CareShield Life payout) | Any 1 out of 6 ADLs |

| S$600 | Any 2 out of 6 ADLs | ||

| Singlife CareShield Standard | S$384.91 - Up to age 69 | S$600 (excludes CareShield Life payout) | At least 3 out of 6 ADLs |

| Singlife CareShield Plus | S$461.38 - Up to age 69 | S$600 (excludes CareShield Life payout) | At least 2 out of 6 ADLs |

| NTUC Income Care Secure | S$220.44 - up to age 67 | $1,200 (includes CareShield Life payout) | At least 2 out of 6 ADLs |

* Sample premium for a 30-year-old male

As mentioned, there are three private insurers that you can pick from. To get you up to speed, we’ve handpicked the best CareShield Life supplements in the market to see which of these plans offer more bang for your buck.

| GREAT CareShield | Singlife CareShield Standard | Singlife CareShield Plus | NTUC Care Secure | |

| Policy term | Lifetime | Lifetime | Lifetime | Lifetime |

| Premium term | The premium term for entry age 30 to 47 is up to 67 or 95 (ALB). The premium term for entry age 48 to 64 is up to 95 (ALB1) or 20 years |

Premium term options of 69 and 99 | Premium term options of 69 and 99 | Premium term options of 67 and 84 years |

| Premium waiver | When unable to perform at least 1 ADL2 | When unable to perform at least 1 ADL2 | When unable to perform at least 1 ADL2 | When unable to perform at least 2 ADL2 |

| Max monthly payout | S$5,000 | S$5,000 | S$5,000 | S$5,000 |

| Criteria to claim monthly payout (inability to perform ADLs) | 1 out of 6 ADLs to claim 50% of monthly payout3 2 out of 6 ADLs to claim 100% of monthly payout3 |

3 out of 6 ADS to claim 100% of monthly payout3 | 2 out of 6 ADS to claim 100% of monthly payout3 | 2 out of 6 ADS to claim 100% of monthly payout3 |

| Initial benefit upon successful claim | One lump sum of 3 times the monthly payout (if unable to perform 1 out of 6 ADLs)4 | One lump sum of 3 times the monthly payout (if unable to perform 3 out of 6 ADLs)4 | One lump sum of 3 times the monthly payout (if unable to perform 2 out of 6 ADLs)4 | One lump sum of 3 times the monthly payout (if unable to perform 2 out of 6 ADLs)4 One lump sum of 6 times the monthly payout (if unable to perform 3 out of 6 ADLs)4 |

| Rehabilitation benefit | NA | 50% of your last monthly payout (2 ADLs) | 50% of your last monthly payout (2 ADLs) | NA |

| Caregiver relief | Additional 60% of your monthly payout payable (up to 12 months5 | Additional 60% of the monthly payout (up to 12 months)5 | Additional 60% of the monthly payout (up to 12 months)5 | NA |

| Dependent care | 30% of monthly payout payable upon inability to perform at least 2 ADLs for up to 48 months6 | Additional 20% of the month benefit up to 36 months if you have a child aged 21 and below6 | Additional 20% of the month benefit up to 36 months if you have a child aged 21 and below6 | Additional 25% of the month benefit up to 36 months if you have a spouse, child, parents/parents-in-law6 |

| Death benefit | NA | 300% of the last paid disability benefit or rehabilitation benefit | 300% of the disability benefit | 300% of the disability benefit |

1Age Next Birthday (ANB) and Age Last Birthday (ALB)

2Subject to Deferment Period, and for as long as he continues to suffer from the disability.

3All payouts here are subject to the Deferment Period. Payouts are payable for as long as the life assured suffers from the applicable number of disabilities, up to the life assured’s lifetime.

4The Initial Benefit is a lump sum payment equivalent to 3 times of the Monthly Payout. In the event the Life Assured fully recovers from the disability, the Initial Benefit may be paid again for subsequent episodes of inability to perform at least 1 ADL. However, it is not payable if such subsequent disabilities arise from or are related to the cause of disability(ies) for which there was a previous claim for Initial Benefit.5Subject to Deferment Period and payable for up to a maximum of 12 months (whether consecutive or not) per Policy Term.6Applicable if the Life Assured has a Child who is below 22 years old (age last birthday) as at the Claim Date; subject to Deferment Period and payable for up to a maximum of 48 months (whether consecutive or not) per Policy Term.

Great Eastern GREAT CareShield

Promotion: Enjoy 20% perpetual discount on your premiums (discount applies throughout your coverage) when you sign up.

Great Eastern’s GREAT CareShield stands out from the rest of the pack as the only MediSave-approved CareShield supplement plan that provides monthly payouts from the inability to perform any ADL.

Depending on your plan, you can receive S$300 to S$5,000 in monthly payouts, on top of your existing CareShield Life payouts.

Mild disability mayoften puts someone at a disadvantage as their quality of life is affected but not severe enough to receive insurance payouts.

When this happens, the financial burden from a lower income, coupled with an increase in medical expenses, is very stressful. This is where Great Eastern’s GREAT CareShield can come in to give you a peace of mind.

With GREAT CareShield, you start receiving monthly payouts1 and a lump sum Initial Benefit2 of up to $15K if you’re unable to perform any one ADL. Additionally, you will receive monthly Caregiver Benefit3 and Dependant Care Benefit4 if you’re unable to perform two or more ADLs.

GREAT CareShield is available to you as long as you have an ElderShield or CareShield Life policy.

1Subject to Deferment Period. 50% of the selected Monthly Payout will be payable upon the inability to perform one ADL and 100% of the selected Monthly Payout will be payable upon the inability to perform at least two ADLs. Payouts of Monthly Payout are payable for as long as the Life Assured suffers from the applicable number of disabilities, up to a lifetime.

2Subject to Deferment Period. The Initial Benefit is a lump sum payment equivalent to 3 times of the Monthly Payout. In the event the Life Assured fully recovers from the disability, the Initial Benefit may be paid again for subsequent episodes of inability to perform at least one ADL. However, it is not payable if such subsequent disabilities arise from or are related to the cause of disability(ies) for which there was a previous claim for Initial Benefit.

3Subject to Deferment Period and payable for up to a maximum of 12 months (whether consecutive or not) per Policy Term.

4Applicable if the Life Assured has a Child who is below 22 years old (age last birthday) as at the Claim Date; subject to Deferment Period and payable for up to a maximum of 48 months (whether consecutive or not) per Policy Term

Singlife CareShield Standard

Promotion: Enhance your CareShield Life or ElderShield coverage with Singlife CareShield Standard or Plus to enjoy 20% lifetime premium discount!

When you look at the sheer number of good stuff packed into a single plan, Singlife CareShield Standard plan is indeed a strong contender.

The benefits include rehabilitation benefit, dependent care benefit, caregiver relief benefit and death benefit. What’s more, you can choose between fixed payouts or increasing payouts at 2% or 3% p.a. until the end of the premium term, or when a claim is made, whichever is earlier.

To qualify for the rehabilitation benefit monthly payout, you must be unable to perform two ADLs (moderate disability). Depending on your plan, you’re eligible to receive an additional S$200 to S$5,000 ON TOP of the payouts from your CareShield Life plan.

Furthermore, you can choose whether you want fixed or increasing payouts to make budgeting easier. You also don’t have to continue making premium payments once you’re unable to perform one ADL.

Other supports include:

- You can get a lump-sum benefit up to 3X your monthly payout if you’re severely disabled

- Continue to receive 50% of your last monthly payout during rehabilitation if you’re still unable to perform two ADLs (for CareShield Standard only)

- Receive 20% more of your monthly/rehabilitation benefit for up to 36 months if you have a child under 22 years old

- Receive 60% more of your monthly/rehabilitation benefit for up to 12 months to help with caregiver costs

- Receive a payout 3X your monthly/rehabilitation benefit if you pass away

- Increase your monthly payout at key life milestones such as buying a property or becoming a parent

Singlife CareShield Plus

The main difference between Singlife CareShield Standard and CareShield Plus is the severe disability definition: you’re eligible for CareShield Standard claims if you can’t perform at least three ADLs, while for CareShield Plus, it’s just two.

CareShield Plus also provides a 20% perpetual premium discount as well as additional goodies such as dependent care, caregiver relief and death benefit.

Granted, while there’s a lack of rehabilitation benefit under this plan, it’s important to note that 100% of the monthly payout will be activated in the event of moderate disability (inability to perform two out of six ADLs).

NTUC Income Care Secure

![]()

NTUC Income’s Care Secure offers decent coverage with a support benefit (initial payout) of up to 600% of the disability benefit, a dependent benefit of 25% of the disability benefit every month for up to 36 months and death benefit of 300% of the disability benefit.

Moreover, NTUC policyholders are also privy to exclusive offers that range from shopping discounts to luxury staycations deals.

But one significant stumbling block is that its monthly payout is inclusive of CareShield Life’s payout. To compare, GREAT CareShield Advantage and Singlife CareShield Standard both offer monthly payout in addition to the basic payout, which simply means you’re able to get more at the end of the day.

Which CareShield Life supplement should I sign up for?

There’s definitely no hard and fast rule to this. When deciding on the supplement that’s right for you, you’ll need to consider your own medical needs and priorities.

If you want your loved ones taken care of if anything should happen to you, we suggest that you opt for plans that include dependent benefits as they’ll be able to receive a payout if you become disabled. Remember that the payout you’re eligible for is also dependent on the premium that you are paying.

In this regard, Singlife’s CareShield Standard provides the most well-rounded benefits along with a higher payout. However, do take note that if you opt for the increasing payout plan, you’d need to fork out increasing premiums at 2% or 3% p.a.

Meanwhile, NTUC Income’s lump-sum payout is quite generous: you will receive 3X your first monthly payout if you can’t perform at least two ADLs and 6X of your first monthly payout with the inability to perform at least three ADL. However, the monthly payout you receive if you can’t perform at least three ADLs is inclusive of the basic payout you receive from CareShield.

Lastly, as mentioned above, Great Eastern’s GREAT CareShield is the only plan that offers you a monthly payout when you can’t perform at least one ADL. You’ll also receive the full monthly payout if you can’t perform at least two ADLs. The flip side is there’s no death benefit.

Protected up to specified limits by SDIC.

Note: This is only product information provided. You may wish to seek advice from a qualified adviser before buying the product. If you choose not to seek advice from a qualified adviser, you should consider whether the product is suitable for you. Buying an insurance product that are not suitable for you may impact your ability to finance your future healthcare needs.

If you decide that the policy is not suitable after purchasing the policy, you may terminate the policy in accordance with the free-look provision, if any, and the insurer may recover from you any expense incurred by the insurer in underwriting the policy.

Read these next:

CareShield Life And MediSave Care: Everything You Need To Know

5 Best Personal Accident Insurance Plans In Singapore (2023)

What’s The Difference Between MediSave And MediShield Life: A 2-minute Explainer

5 Best Term Insurance Plans in Singapore (2023)

5 Best Cancer Insurance Plans In Singapore

Similar articles

5 Tips for Caring for a Parent With Dementia

5 Misconceptions Singaporeans Have About Disability Insurance

Does Every Singaporean Need Disability Income Insurance?

Best Annuity Plans For Your Retirement In Singapore

Caring for a Loved One? Remember To Protect Yourself with Singlife CareShield

What Happens If: My Mum Doesn’t Have Life Insurance?

Insurance Savings Plans: Singlife Account vs GIGANTIQ vs SingTel Dash PET

CareShield Life And MediSave Care: Everything You Need To Know

Back to Blog

Back to Blog