Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

If you’re planning for a wedding, you’ll know that expenses can run sky high. Read on to find out how wedding loans could help defray your out-of-pocket payments.

Few life milestones are as stressful and expensive as a wedding. From the banquet to the honeymoon, there's so much to plan and pay for. Many couples don’t mind splurging for the wedding of their dreams, even if it strains their finances. After all, they’ll have to shoulder other major costs such as home renovations and flat downpayments too.

This is when wedding or marriage loans can prove indispensable. Also known as personal loans, these funds can tide you over during this period when your cash outflow is high.

Here’s a guide to the best wedding loans and how they could help you turn your vision of your big day into reality.

⚡SingSaver x Trust Personal Loan Flash Deal⚡

Enjoy low interest rates from 1.00% p.a. (EIR 2.28% p.a.) plus up to S$1,750 in cashback and rewards when you sign up for Trust Bank Personal Loan via SingSaver. Plus, receive a S$10 FairPrice E-Vouchers from Trust when you sign up with the referral code SINGSAVE. Valid till 2 August 2026. T&Cs apply.

What is a wedding loan and how does it work?

A wedding loan is a type of unsecured credit facility that provides a lump sum of cash you can use to pay for any wedding expenses. Such loans are available without the need for collateral backing.

Wedding loans are fixed instalment loans, which means you will repay your loan via monthly repayments. Repayment includes the interest charged on the loan; once you finish up paying all your monthly instalments, your entire loan would be paid off.

Wedding loan tenures range from one to seven years, although most banks have an upper limit of five years. This makes wedding loans one of the most flexible and affordable ways to pay for the high costs involved.

So, how much can you loan for your wedding expenses? That depends on your income. Typically, you can borrow up to 4-6x your monthly salary. If you're earning S$120,000 or more per year, you might even be able to borrow up to 10x your salary.

Say “I do” to offsetting wedding expenses

From cashback cards to customisable rewards cards, we roundup the best credit cards for managing your wedding expenses.

How to apply for a wedding loan in Singapore?

Wedding loans are readily available in Singapore, since personal loans are offered by all major banks and financial institutions. Qualifying applicants will need to meet age and income requirements, the latter often being significantly higher for foreigners.

You'll need to provide a copy of your NRIC, IRAS Notice of Assessment, CPF statement, recent pay slips, and documents reflecting your billing address.

Applications can be done online for most banks; some also allow you to apply through their mobile apps. For financial institutions, you can apply online or visit one of their branches.

Difference between a personal loan and a wedding loan

If you're thinking that a wedding loan sounds a lot like a personal loan, that's because they are both one and the same.

Wedding loans are just personal loans that you use for your marriage expenses. However, there is actually no restriction on what you can use your loan for. Once the cash has been disbursed to your account, you are free to use the funds at your own discretion.

For this reason, some couples may take out personal loans that exceed the cost of their wedding, so they can use the leftover funds for other expenses, such as renovation costs.

How can a wedding loan help you?

Wedding loans allow you to borrow 4 to 10 times your monthly salary, making them a quick and easy way to cover wedding costs. Here are some of the estimated expenses you can tap on a wedding loan to cover:

-

Wedding banquet (15 tables of 10): S$5,800–47,300

-

Wedding photography: S$2,000–4,000

-

Wedding videography: S$2,000–4,000

-

Pre-wedding photoshoot: S$350–800

-

Wedding hair and make-up: S$250–1,000

-

Wedding car rental: S$300–900

-

Wedding gown and suit: S$500–5,000

-

Wedding rings: S$500–2,000

You can expect wedding loans to cover amounts between S$10,000–70,000, depending on how lavish you want your big day to be. Some of these expenses could possibly be offset by the flurry of red packets you’d receive at your wedding.

Since nobody can predict how much you'll be receiving from your guests, you'd want to ensure you have enough cashflow to cover your overheads and then some. Erring on the side of caution with a larger wedding loan is recommended.

How to pick the best wedding loan

-

Go for the lowest interest rate. As wedding loans can be large, lower interest rates can help you save on repayment, especially if you have a longer tenure. Be sure to check the Effective Interest Rate (EIR) for a more accurate comparison when reviewing loans.

-

Choose a suitable loan tenure. The longer your loan tenure, the lower your monthly payment will be. This gives you financial flexibility at the cost of potentially paying more over time. For example, if you take out a personal loan of S$50,000 over 3 years from UOB, you'll be paying S$1,508.89 a month which will amount to S$54,320.00 at the end of your tenure. The same loan with UOB over a period of 1 year has a significantly lower repayment total sum of just S$51,440.

>> More: Personal loans vs. credit cards: Which is better for financing your wedding?

Best wedding loans in Singapore

So you’ve decided that taking a loan would help you to breathe a little easier as your big day approaches. Let’s take a look at some of the best options in the market.

HSBC Personal Loan

Product details

-

Get approval in principle within 1 minute.

-

Get up to S$200,000 in loans, subject to your salary. You get 4x your monthly salary if your annual income is between S$30,000-199,999. An annual income of S$120,000 and above is needed to qualify for loans 8x your monthly salary.

-

Pay interest on only the sum you utilise and enjoy flexible monthly repayment terms.

-

Access your funds through internet banking, mobile banking or with your debit card.

-

Enjoy instant card disbursements with a HSBC account.

-

Your available credit limit is reinstated upon monthly repayment.

-

Score up to S$3,600 cashback by providing marketing consent and taking out a new loan with a tenure between 3-7 years.

SingSaver's take

With the longest tenure available in the market, this is the perfect loan for people who are feeling the strain of multiple recurring payments. A S$40,000 loan over 7 years, for example, would work out to be just S$547 a month, whereas you’ll need to repay S$1,181 a month with a 3-year tenure.

SingSaver x HSBC Personal Loan Exclusive Offer

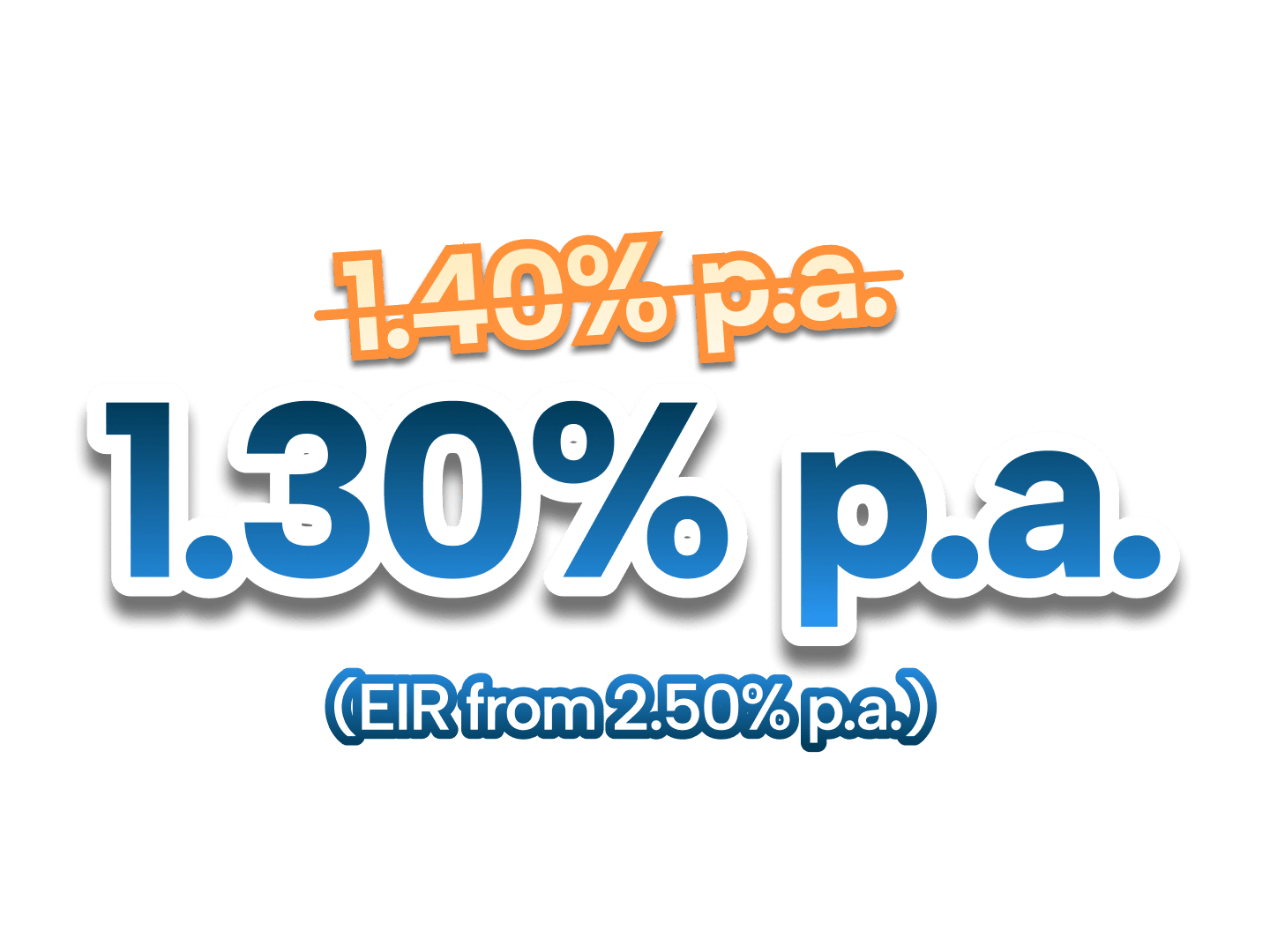

Enjoy attractive interest rates from 1.30% p.a. (EIR from 2.50% p.a.) when you apply for HSBC Personal Loan via SingSaver. Available to new and existing customers! Valid till 2 August 2026. T&Cs apply.

Trust Bank Instant Loan

Product details

-

Turn a portion of your Trust credit card's available credit balance into cash.

-

No processing or hidden fees.

-

Already have a Trust savings account? Get your loan deposited into your savings account in seconds.

-

Choose a tenure between 3 to 60 months.

SingSaver's take

Low interest rates, zero processing fees and a no-fuss process makes the Trust Bank Personal Loan a winner. The Trust Bank Personal Loan is a good choice for people seeking hassle-free, fast approval loans

UOB Personal Loan

Product details

-

Instant approval for UOB customers when you apply online between 8am-8pm.

-

Up to 2% cash rebates for loans S$15,000 and above with a tenure of at least 36 months. (Only for direct applications through the UOB Personal Loans page.)

-

Monthly repayments of as low as $20 per month, get approvals for loans as little as S$1,000.

SingSaver's take

Ideal for existing UOB customers, since they can get instant approval easily by applying online during business hours. Another big benefit is UOB's cashback mechanism, a perk for anybody looking to get a short to medium term loan between 3 to 5 years.

⚡SingSaver x UOB Personal Loan Flash Deal⚡

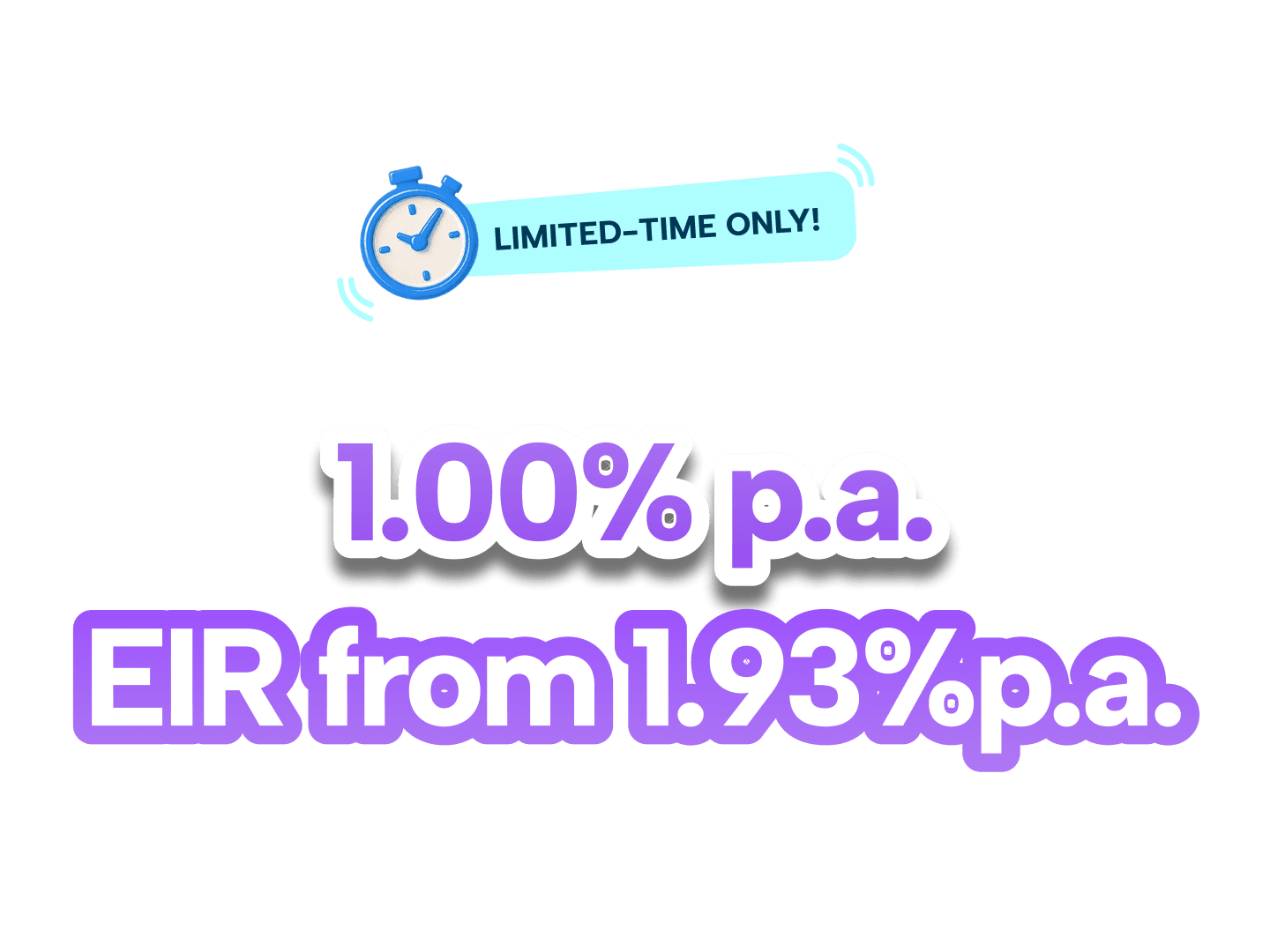

Get one of the lowest interest rates from 1.00% p.a. (EIR from 1.93% p.a.) plus up to S$1,900 in cashback and rewards when you apply for a UOB Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

Citi Quick Cash Loan

Product details

-

Convert your Citi Credit Card or Ready Credit into cash and repay your loan together with your monthly payment.

-

Choose between 1 to 5 years for your tenure.

-

Loan up to 4x your monthly income, or 8x of your monthly salary with an annual income of S$120,000 or above

-

Existing Citi customers can apply for their loans through the Citi Mobile® App or Citibank Online.

SingSaver's take

A great pick for existing Citi customers, since they will be able to get their disbursements instantly. Also a good option for those who don't mind using their credit limit for a loan, as opposed to a more traditional loan application.

Standard Chartered CashOne Personal Loan

Product details

-

Receive your funds instantly with an existing Standard Chartered Current or Cheque & Save account. Up to 15 minutes' waiting time is needed for disbursement to non-Standard Chartered bank accounts.

-

Choose between a loan tenure of 1 to 5 years.

-

Borrow up to 2x your monthly salary with an annual income under S$30,000. People with an annual income of S$30,000 or more can borrow 4x their monthly salary.

-

Repay as low as S$50 per month without late charges, if you have paid your full monthly instalment amount for 6 consecutive months.

-

Customers who may miss their minimum amount due repayments more than twice in a 6-month period may have their loan tenures extended. They may also get an additional 4% p.a. added to their EIR effective from their next statement date.

-

An early redemption fee of S$150 or 3% of your outstanding principal applies, whichever is higher.

SingSaver's take

Financially disciplined and ready to commit to a new loan? You might want to consider Standard Chartered Bank's CashOne Personal Loan, since you'll benefit from their competitive rates and late penalty fee waiver, thanks to your rigorous observance of the repayment schedule.

⚡SingSaver x SCB CashOne Personal Loan Flash Deal⚡

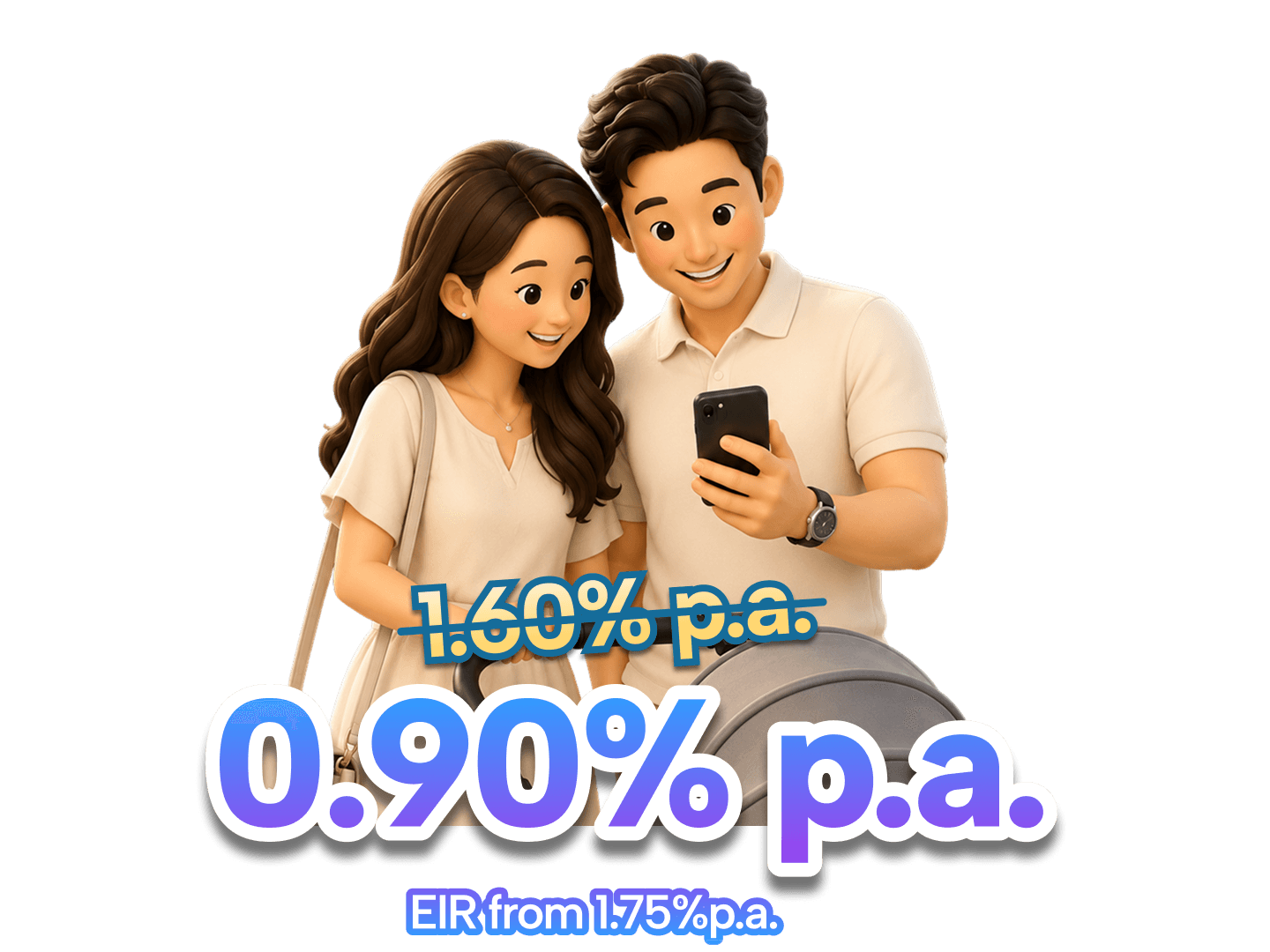

Enjoy one of the market's lowest interest rates starting from 0.90% p.a. (EIR from 1.75%) plus up to S$1,800 in Cashback when you apply for Standard Chartered CashOne Personal Loan via SingSaver. Valid till 2 August 2026. T&Cs apply.

CIMB Personal Loan

Product details

-

Malaysians with a minimum annual income of S$30,000 can also apply for this loan.

-

Instant approvals even without a CIMB bank account or credit card.

-

Loan up to 2-8x your income, up to a maximum of S$200,000.

-

Zero early repayment and processing fees.

-

Choose a tenure between 1 to 5 years.

SingSaver's take

CIMB has one of the most transparent loan pages, which includes all associated fees and rates. CIMB boasts no early repayment fees, which can be a big plus, especially if your financial situation were to change. It also has one of the lowest qualifying minimum annual incomes at S$20,000, making it extremely accessible for anybody in need of quick cash.

SingSaver x CIMB Personal Loan Exclusive Offer

Enjoy attractive interest rates from 1.28% p.a. (EIR from 2.46% p.a.) when you get approved for a loan with a minimum tenure of 3 years. Available to new customers only. Valid till 2 August 2026. T&Cs apply.

OCBC ExtraCash Personal Loan

Product details

-

Instant approval and disbursement of funds when you apply with SingPass and have your financial and personal data ready on MyInfo.

-

Choose a loan tenure between 1 to 5 years.

-

Get up to 6x your monthly income, if your minimum annual income is S$120,000 or above.

-

A late fee of S$80 applies.

-

A restructuring fee of 3% of your outstanding loan amount applies.

-

Want to make early partial or full repayment? A minimum of 3% of the amount to be repaid or S$1,000 applies for early partial repayment. 1 month's interest in lieu will be charged for early full repayment.

SingSaver's take

OCBC's interest rates are on the high end, which means full repayment of a relatively small loan of S$10,000 over a year will cost you up to S$10,554.36. Meanwhile, a loan of S$50,000 over 3 years can cost you up to S$68,742.72 in total!

Licensed moneylenders

Another non-bank option you can consider, especially if you have a low credit score or insufficient credit history, is licensed moneylenders. While this is an entirely viable option as licensed moneylenders have to abide by the Moneylenders Act, such as not charging more than 4% interest per month, borrowing from licensed moneylenders can still come with its risks. Always check to see if your prospective lender appears on the Ministry of Law's list of licensed moneylenders and ensure that you can afford the repayments on time before agreeing to take out any loans.

>> More: Wedding banquet price list for 2025.

Conclusion

A wedding loan can help soothe financial headaches so you can be your best self on your special day. They can give you a much needed budgetary boost, and give you some breathing room as you work on making your repayments.

Want to snap up the best deals and exclusive offers? Apply for your loan of choice through SingSaver’s comprehensive comparison tool now.

Frequently asked questions about wedding loans

Must the wedding ceremony of your dreams always result in debt? Well, that depends on how well you manage your finances. An average wedding in Singapore costs S$30,000-50,000 but extravagant celebrations can cost upwards of S$80,000. A typical personal or wedding loan will allow you to borrow between 4-6x your monthly salary over 1-5 years. Assuming you take out a S$40,000 loan with an EIR of 4.43% p.a. over 3 years—this works out to a total repayment of S$42,788! While working couples may be able to easily make repayment of S$1,177.44 a month by pooling their finances, this can become tricky when other costs start adding up over the length of your tenure.

Most people use personal loans for wedding expenses, but few banks openly market them as wedding loans. Trust Bank is one exception, as they offer instant wedding loans from 2.22% p.a. (EIR 4.22% p.a.). CIMB and Standard Chartered bank also market their personal loans as a way for people to offload hefty wedding expenses. Many online lenders and even Singapore's oldest credit co-operative, TCC, on the other hand, do provide dedicated wedding loans.

A glowing credit report shouldn't be a prerequisite for a perfect wedding. If your credit history has seen better days, you might have to look beyond banks for wedding loans. Licensed moneylenders are one option, provided they are aboveboard and on the Ministry of Law's list of licensed moneylenders. Your other option is credit co-operatives, who are not-for-profit financial institutions operated by members of the same industry. Look to see if you might be eligible for membership for any credit co-operatives listed on the Ministry of Culture, Community & Youth's Co-ops Sector page.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.