Citi Wealth First Account: High Rates, Best for Citigold Clients

Updated: 25 Jul 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

Looking to get more out of your savings while unlocking premium banking benefits? Citi’s Wealth First Account might just be the solution for high-net-worth individuals and Citigold clients.

If you’ve been searching for a savings account in Singapore that rewards you for growing your wealth — not just spending — the Citi Wealth First Account is worth serious consideration. Designed to complement Citigold and Citigold Private Client relationships, this account offers high interest rates, base interest with no cap, and a suite of lifestyle and investment perks. In this guide, we’ll break down how it works, who it’s best suited for, and how it compares with other high-yield accounts in the market.

Take your save and spend to the next level with premium banking options

Explore the best priority banking options from Standard Chartered, HSBC and Citigold and find what works for you

SingSaver feature: Citi Wealth First Account for high earners maximising interest earns

SingSaver’s take

The Citi Wealth First Account isn’t your typical savings account. It’s an account that helps you grow your wealth by rewarding you for your banking and wealth relationship. If you are a Citigold customer or join Citigold, you will be able to earn high interest rates on your savings. There is no minimum monthly income requirement, although to enjoy the bonus interest rates the minimum deposit is S$250,000 fresh funds.

Pros

Offers high interest of up to 7.51% p.a. and rewards you for your usual banking activities, and when you insure and invest

There is no cap on base interest earned

Decent attainable interest rate of 3% as long as you spend and save

Cons

Have to jump through some hoops to earn higher interest rate

There is a cap on how much bonus interest you can earn

Spending category is only applicable to Citibank Debit Mastercard

How does the Citi Wealth First Account work?

The Citi Wealth First Account rewards customers with tiered interest rates based on their total relationship with the bank. This includes your savings balance, investments, and insurance holdings with Citibank. Unlike typical accounts that only reward spending or salary crediting, Citi focuses on overall wealth engagement.

» MORE: A full guide to priority banking in Singapore

Interest is calculated in two parts — base interest and bonus interest. The base interest applies to all balances without a cap, which is a significant advantage over other savings accounts that limit interest to the first S$75,000 or S$100,000. To unlock bonus interest, you’ll need to hold Citigold status and meet investment or insurance milestones. For instance, Citigold clients can enjoy higher effective interest rates of up to 7.51% p.a. or more.

There is also a cap on the amount that earns interest in your account based on your banking relationship with Citi:

|

Balance tier |

Citigold |

Citigold Private Client |

|

Average daily balance; incremental balance |

First S$250,000 |

First S$500,000 |

|

Minimum Total Relationship Balance (TRB) maintained |

S$250,000 |

S$1,500,000 |

What are the benefits of a Citi Wealth First Account?

#1 It offers high interest rates

One of the biggest draws of the Citi Wealth First Account is its competitive interest rates, especially for Citigold clients. Depending on your relationship tier and engagement with Citi’s wealth management solutions, you could earn significantly more than traditional savings accounts or fixed deposits. It’s particularly attractive for those looking to grow large cash balances while benefiting from holistic banking services.

#2 There is no cap on base interest earned

Many high-interest savings accounts in Singapore cap the amount of funds eligible for bonus interest — often around S$100,000. The Citi Wealth First Account stands out by offering base interest with no cap. This makes it ideal for clients with higher liquidity, as you’ll continue to earn returns on the full balance instead of having excess funds idling with little to no yield.

#3 It offers other lifestyle and advisory benefits

Aside from interest, the account integrates well with Citi’s broader wealth ecosystem. As a Citigold or Citigold Private Client, you gain access to a Relationship Manager, tailored investment insights, travel perks, and exclusive event invitations. These lifestyle and advisory benefits add value beyond just the numbers, especially for clients who prioritise premium service and personalised financial planning.

What is an Accredited Investor?

In Singapore, an Accredited Investor (AI) is someone who meets specific income or asset thresholds as defined by the Monetary Authority of Singapore (MAS). These individuals are considered financially more sophisticated and capable of understanding the risks of complex investment products. To qualify as an AI, you must meet at least one of the following criteria:

-

Have an income of at least S$300,000 in the past 12 months; or

-

Own net personal assets exceeding S$2 million (with the first S$1 million of your primary residence excluded from the calculation); or

-

Hold net financial assets of more than S$1 million.

Being classified as an AI is particularly relevant for those exploring Citigold or Citigold Private Client (CPC) status, as Citi may assess your eligibility and suitability for certain investment products using this framework. Once you're onboarded as a Citigold or CPC customer — and especially if you qualify as an AI — you gain access to a broader suite of exclusive investment opportunities. These can include structured products, private equity funds, sophisticated FX strategies, and other solutions that are not available to general retail investors.

» MORE: Citigold review 2025

When paired with the Citi Wealth First Account, AI status enhances your ability to take full advantage of Citi's wealth ecosystem. For example, higher investment volumes or more complex product types (available only to AIs) could help you meet the qualifying criteria to unlock higher bonus interest rates — sometimes up to 4.5% or more per annum. On top of that, Accredited Investors may receive more personalised advisory services and exclusive insights from Citi’s dedicated Relationship Managers or Investment Consultants.

In short, being an AI complements the Citi Wealth First Account by unlocking more investment options that contribute towards your total relationship balance and qualifying activities — both of which are key to earning enhanced interest and accessing premier banking privileges.

If you’re worth more, your banking should do more for you

It may be time to try out a priority banking account and enjoy competitive interest rates and personalised financial service

Who is the Citi Wealth First Account best for?

The Citi Wealth First Account is best suited for:

-

Affluent professionals — If you earn upwards of S$15,000 a month and are actively growing your wealth, this account can help you make the most of your cash holdings while giving you access to wealth planning tools.

-

Citigold clients — Already a Citigold customer? The Wealth First Account is designed to work in tandem with your existing relationship, maximising both interest earnings and value-added services like portfolio reviews and concierge support.

-

Business owners or retirees — Those with significant idle funds who want better returns than fixed deposits will find this account appealing, especially with the no-cap base interest and added flexibility.

» MORE: 3 signs it’s time to give priority banking a try

Not ideal for:

-

Young professionals — If you’re just starting your career with a modest income or savings, there are better entry-level accounts with fewer requirements and lower balance thresholds.

-

Everyday spenders — If you’re more focused on daily cashback or reward points, a savings account tied to card spend like the UOB One or OCBC 360 may be more rewarding.

-

Passive savers — If you don’t intend to engage with Citi’s investment or insurance offerings, you might not unlock the full interest potential of this account.

Are there any ongoing promotions?

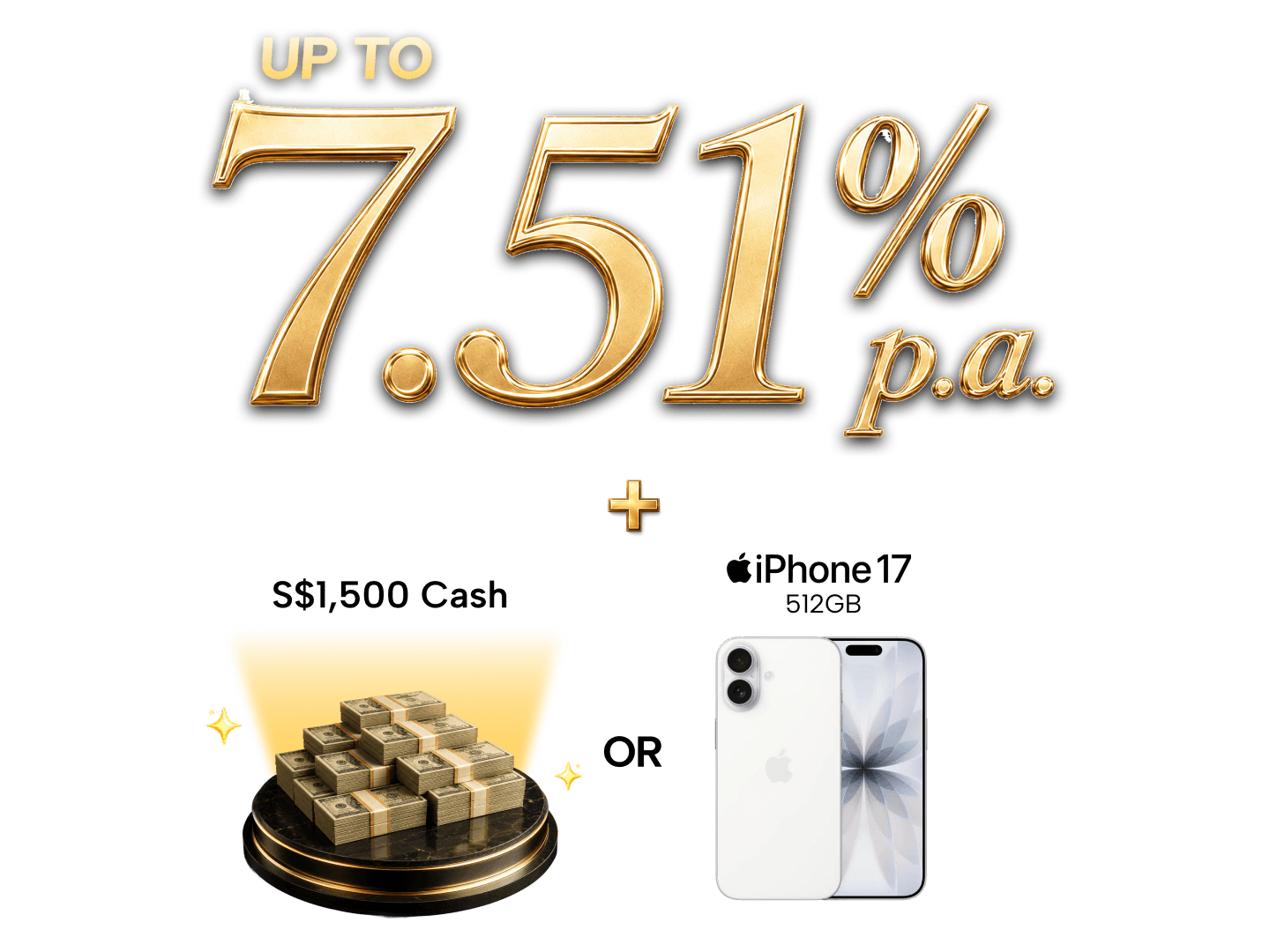

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

Click here for more information.

Do note that promotion terms and reward amounts may vary depending on ongoing campaigns. Be sure to check Citibank’s official website or SingSaver’s banking deals page for the most current offers.

Comparison to other savings accounts

Every account suits different needs. Citi’s offering shines when you have a large deposit and prefer growing your wealth through investment-linked benefits, rather than focusing solely on spending or transactional behaviour.

Here’s how the Citi Wealth First Account stacks up against other premium savings accounts in Singapore:

|

Account Name |

Max Effective Interest |

Minimum Balance |

Cap on Bonus Interest |

Wealth Client Requirement |

|

Citi Wealth First Account |

Up to 7.51% p.a. (with Citigold) |

S$250,000 |

No cap on base interest |

Yes (Citigold) |

|

Around 3.0% p.a. |

S$200,000 |

Capped at S$200,000 |

Yes (Premier Banking) |

|

|

Up to 3.88% p.a. |

S$200,000 |

Capped at S$100,000 |

Yes (Priority Banking) |

|

|

Up to 4.0% p.a. |

S$100,000 |

Capped at S$100,000 |

Yes (Lady’s Privilege Programme) |

The Citi Wealth First Account is best suited for high-net-worth individuals who already hold — or are ready to commit to — a Citigold relationship. If you are already investing through Citi or open to doing so, the interest upside and additional perks are unmatched. However, if you prefer a simpler, more passive way to earn without actively managing your bank relationship, OCBC Premier Dividend+ offers a steady alternative. For those who prefer a more transactional mix of spending and investing, Standard Chartered’s Priority Bonus$aver provides a balanced middle ground.

OCBC Premier Dividend+

Compared to OCBC’s Premier Dividend+ Account, the Citi Wealth First Account offers significantly higher potential interest — up to 7.51% p.a. (with conditions) versus OCBC’s approximate 3.0% p.a. While both accounts target affluent customers with minimum balances of S$200,000 or more, Citi stands out with its no-cap base interest and dynamic bonus interest structure tied to Citigold status and wealth engagement. In contrast, OCBC’s dividend-style interest is more passive and based primarily on account tenure and balance size, making it a better fit for savers who prefer a set-and-forget approach. Citi, however, rewards those who are actively investing or insuring through its platform, providing more upside for high-net-worth individuals seeking both returns and premium banking experiences.

Standard Chartered Priority Bonus$aver

When compared to Standard Chartered’s Priority Bonus$aver, the Citi Wealth First Account delivers stronger returns with less dependence on everyday banking behaviours. Bonus$aver requires a combination of salary crediting, card spend, bill payments, and eligible product purchases to hit the top rate of 3.88% p.a., which is capped at the first S$100,000 of deposits. Citi, on the other hand, offers up to 7.51% p.a. with no cap on base interest and focuses on deeper wealth relationships via Citigold.

While SC’s account may appeal to those with active transaction patterns, Citi is better suited for clients who prefer to grow wealth through larger investments and enjoy access to a full suite of Citigold lifestyle, travel, and advisory benefits.

Got priority banking? It’s time for a premium credit card

Pair your banking with an appropriate credit card from our top-of-the-line range

Eligibility

To open a Citi Wealth First Account, you must be:

- At least 18 years old

- A Singaporean, PR, or foreigner with valid documentation

- A Citigold or Citigold Private Client (min. S$250,000 in investible assets)

The account is best paired with a Citigold relationship, which includes a dedicated Relationship Manager and access to wealth management tools.

How do I apply for a Citi Wealth First Account?

Applying for the Citi Wealth First Account is relatively straightforward — but keep in mind, this account is best suited for individuals who meet the Citigold eligibility criteria. You’ll need a minimum of S$250,000 in total relationship balance (which can include savings, investments, and insurance with Citi) to qualify as a Citigold client.

To apply, you can visit the Citibank website or head down to any Citibank branch for a consultation. If you prefer convenience, you can initiate the process online using MyInfo via Singpass, which auto-fills your personal information for a quicker application. Expect to provide supporting documents like your NRIC or passport, income proof (e.g. payslips or IRAS notice of assessment), and asset declarations if you’re aiming for Accredited Investor status. If you're new to Citibank, you’ll likely be guided through both account opening and Citigold onboarding in a single process.

Reviews of best priority banking accounts in Singapore

Read reviews of the various priority banking accounts in Singapore and what each account has to offer to find the best product for your needs:

Frequently asked questions about the Citi Wealth First Account

Citigold is Citi’s premium banking relationship — available to customers who maintain at least S$250,000 in total assets with the bank. It includes wealth advisory, lifestyle privileges, and a dedicated Relationship Manager. Citi Wealth First is a high-interest savings account designed for Citigold clients. While you can open the account without Citigold status, you’ll only unlock its best interest rates and perks if you’re a Citigold member actively investing or insuring through Citi.

To maximise your returns with Citi Wealth First, you’ll need to qualify for Citigold, which requires a minimum total relationship balance of S$250,000. There’s no hard minimum to open the account itself, but without Citigold status and wealth engagement, you’ll only earn the base interest of 0.01% p.a.

Yes, but you won’t benefit from the enhanced interest rates unless you qualify as a Citigold or Citigold Private Client. The account is technically open to all individuals, but its features are clearly designed to reward clients with deeper relationships with the bank.

Interest is made up of two components — base and bonus. All account holders earn a base interest of 0.01% p.a. with no cap on balance. Bonus interest is tiered and applies when you meet Citigold requirements and participate in eligible investment or insurance activities.

It can be. While fixed deposits typically offer fixed rates for a set period, Citi Wealth First allows more liquidity and the potential to earn up to 7.51% p.a. on your balance. The key is meeting Citigold criteria and actively engaging with Citi’s wealth platform.

You’ll need to meet one of the following MAS criteria: an annual income of at least S$300,000, net personal assets above S$2 million, or net financial assets exceeding S$1 million. Accredited Investors may get access to more complex investment products through Citi, which can help unlock higher bonus interest tiers when paired with Citi Wealth First.

Relevant articles

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.