18 Top Passive Income Ideas for 2026 and Their Earning Potential

Updated: 22 Apr 2026

Passive income isn’t just about earning money with minimal effort — it’s about creating sustainable revenue streams that align with your financial goals and lifestyle. Whether through investments, rental properties, or digital ventures, diversifying your income sources can help you build long-term wealth and financial security, all while letting your money work for you.

In an era of stabilizing interest rates and a focus on high-quality growth, finding the best ways to make passive income is essential for financial freedom. Whether you are looking to hedge against inflation or build a retirement nest egg, having a suite of income generating assets is a proven strategy.

Here are the top passive income ideas to help you generate additional income in Singapore for 2026.

SingSaver Exclusive Offer

⚽ Make your move this World Cup season. Compare top brokerage deals on SingSaver, then apply to score exclusive upsized rewards this June. Make every play count. 📈🏆 T&Cs apply.

Make the most of every trade. 📊

Set up your account in under 5 minutes, explore your options with ease, and enjoy exclusive rewards as you grow your portfolio. 🪙🏆T&Cs apply.

What is passive income?

Passive income refers to earnings that require little to no active involvement once set up. Unlike active income — where you trade time for money through a salary or hourly wage — passive income allows your assets, investments, or prior efforts to generate earnings on their own.

Examples include rental income, dividend-paying stocks, and interest from high-yield savings accounts. While most passive income streams require an initial investment of time, money, or both, they can continue to provide financial returns with minimal upkeep, helping you build long-term wealth.

>> Looking for quick cash? Find out how you can build a side income in five steps

18 ways to generate passive income

Investment-based ways

Investing in assets that generate returns can be an effective way to build a passive income stream. These are often cited as the best passive income investments due to their potential for both capital growth and regular payouts.

1. Dividend stocks

Investing in dividend-paying stocks allows you to earn a share of a company’s profits on a recurring basis. In 2026, "dividend aristocrats" in the Singapore market, such as local banks and stable industrial firms, remain popular income generating assets.

-

How much can you earn? Dividend yields for Singapore blue chips currently range between 4.0% and 5.5%. If you invest S$10,000 in a stock with a 5% yield, you could earn S$500 annually.

⚡ SingSaver x Webull Flash Deal ⚡

Open a Webull account and fund a minimum of SGD3,000 to receive S$110 Cash. Fund SGD10,000 to get upsized S$230 Cash, S$50 eCapitaVoucher + Samsung Galaxy Buds 4 Pro (worth S$349) (total worth S$399), or 13k Max Miles by Heymax (worth S$234). Or, top up as low as S$50 to get a Dyson Purifier Cool™ TP10. Valid till 2 August 2026. T&Cs apply.

2. Dividend index funds and exchange-traded funds (ETFs)

If you prefer a hands-off approach, dividend ETFs are among the best ways to make passive income without picking individual stocks.

-

How much can you earn? In 2026, high-yield dividend ETFs in Singapore (like the STI ETF or REIT ETFs) yield between 3.5% and 5.2%. A S$10,000 investment at a 4.5% yield generates S$450 a year.

SingSaver x Plus500 Exclusive Offer

Get S$300 Cash, Samsung Galaxy Buds4 Pro (worth $349), or 20,000 Max Miles by HeyMax when you open a Plus500 account through SingSaver, make a min. deposit of S$1,500, and execute at least 3 trades in Commodities or Indices or Options within 14 days. Valid till 2 August 2026. T&Cs apply.

💎 Exclusive Deposit Bonuses from Plus500

Get S$13,000 plus 8,000 Trader Points when you deposit min. S$75,000 with bonus code DIAMOND, S$688 plus 408 Trader Points with min. S$1,000 using SingSaver688, or S$288 plus 128 Trader Points with min. S$500 using SingSaver500. Valid till 2 August 2026. T&Cs apply.

3. Bonds and bond index funds

Bonds are essential for portfolio stability. While yields have moderated in 2026, they remain a "safe haven" for those looking to generate additional income with low risk.

-

How much can you earn? 10-year Singapore Government Securities (SGS) are currently yielding around 2.2% to 2.5%. Corporate bonds may offer 3.5% to 5% depending on credit ratings.

Saver takeaways

Passive income is a powerful way to build wealth, but don’t forget about the tax implications — it can make all the difference between maximising your earnings and facing an unexpected bill. Many new investors and side hustlers overlook tax planning, only to realise later that a portion of their income goes towards tax obligations.

At the same time, there are ways to make your money work smarter. Depending on your income source, you may qualify for deductions or reliefs that help you retain more of your earnings. Whether you’re earning through investments, rental income, or side gigs, understanding your tax responsibilities early ensures you’re making the most of your passive income streams.

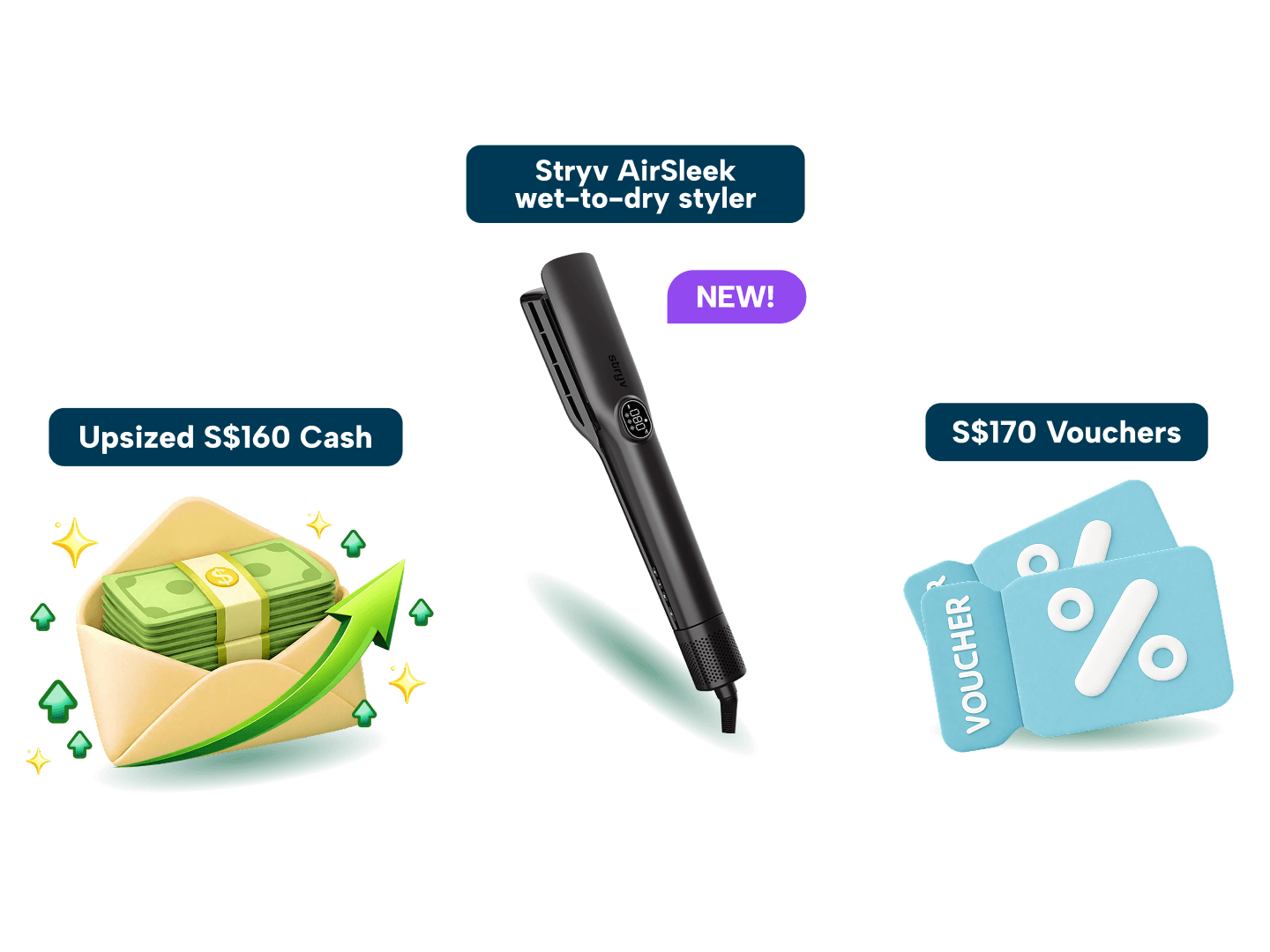

SingSaver x Longbridge Exclusive Offer

Get S$160 Upsized Cash via PayNow, S$170 eCapitaVoucher, or a Stryv AirSleek (worth S$199) when you apply and get approved for a Longbridge SG account, fund a min. of S$2,000 and maintain the assets for 30 days from the day after meeting the deposit criteria. Offer is stackable with Longbridge welcome promo. Valid till 2 August 2026. T&Cs apply.

4. Real estate investment trusts (REITs)

REITs are a favorite for Singaporeans. In 2026, with borrowing costs stabilizing, REITs have recovered. Sector-specific REITs (Data Centres and Logistics) are currently some of the best passive income investments.

-

How much can you earn? Average S-REIT yields in May 2026 range from 5.0% to 6.8%. A S$10,000 portfolio could net you S$500 to S$680 annually.

>> Read more: A complete guide to REITs

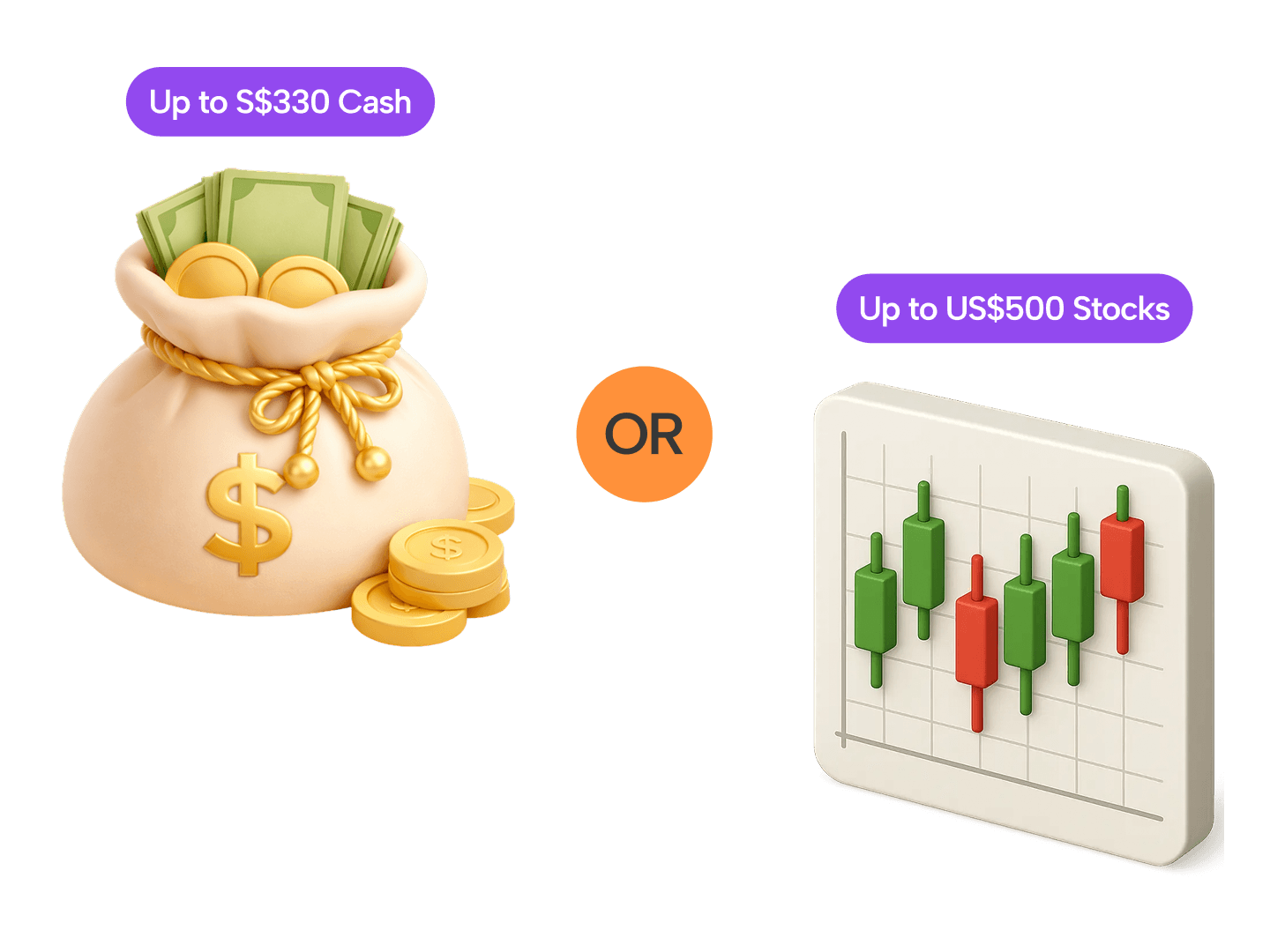

SingSaver x eToro Exclusive Offer

Get S$330 cash via PayNow or up to USD 500 in stocks (fulfilled by eToro) when you open an eToro account and fund a minimum of S$1,000, maintain the fund for 30 days, and make at least 1 trade. Valid till 2 August 2026. T&Cs apply.

5. Money market funds

For those seeking liquidity, money market funds are excellent income generating assets that park cash in short-term debt.

-

How much can you earn? Yields in 2026 are competitive, often hovering around 3.4% to 3.8% p.a., making them superior to standard savings accounts.

>> Read more: The best low risk investments to store your emergency funds

SingSaver x moomoo Exclusive Offer

Open a Moomoo account and fund a minimum of S$2,000 to get upsized S$150 Cash, S$150 Grab Voucher, Apple AirPods 4 or 9,000 Max Miles by HeyMax (worth S$162). Plus, receive up to S$800 Welcome Rewards fulfilled by Moomoo. Valid till 2 August 2026. T&Cs apply.

Interest-based opportunities

These income-generating options carry lower risk compared to traditional investments, as their returns are influenced by benchmark interest rates rather than market fluctuations. Unlike stocks or funds, your principal remains intact, making these options a more stable way to earn passive income.

High-yield savings accounts

A high-yield savings account is a simple yet effective way to earn passive income while keeping your funds easily accessible. In 2026, major banks like OCBC and UOB continue to offer competitive rates for those who credit their salary and meet spending requirements. For instance, the OCBC 360 Account now allows users to earn up to 4.45% p.a. on their first S$100,000, making it a powerful tool for growing your liquid cash.

Saver-savvy tip

Savings account interest rates remain competitive. Make the most of your idle cash by choosing a high-yield savings account that offers attractive returns while keeping your funds easily accessible. Check out our top picks for the best high-interest savings accounts.

7. Fixed deposits (FDs)

A fixed deposit (FD) is a secure savings option where you place your money in a bank for a predetermined period in exchange for a fixed interest rate. As of April 2026, promotional rates for 6 to 12-month tenures are averaging around 1.5% to 2.1% p.a., providing a predictable return for those who do not require immediate access to their capital. While rates have normalized from previous highs, they remain a "risk-free" anchor for a diversified income portfolio.

Real estate passive income opportunities

Earning passive income through property ownership can be a lucrative option, whether by investing in rental properties or leveraging unused space. While buying a property may require significant capital, those with existing assets can generate consistent cash flow through rental income.

8. Buy a rental property

Investing in a rental property is a sustainable way to generate additional income, offering a consistent flow of earnings from tenants. In the current 2026 market, strategic investments in the Outside Central Region (OCR) near upcoming MRT hubs are delivering healthy gross yields of 3.5% to 4.5%. While prime district yields are slightly lower at 2.5% to 3.5%, they continue to attract investors focused on long-term capital preservation.

9. Rent out your home while you're away

If you aren’t ready to invest in a separate rental property, you can still earn passive income by renting out your home when you're away for extended periods. Under 2026 regulations, private residential properties require a minimum stay of three consecutive months, making this ideal for homeowners on long work assignments or sabbaticals. While platforms like Airbnb exist, you must ensure your tenancy agreements comply with Singapore’s strict minimum stay laws to avoid legal complications.

10. Rent out a spare room

Leasing out a spare room is a stable way to earn rental income without giving up your entire living space and is a common practice for offsetting mortgage payments. In 2026, a common room in a central HDB estate can fetch between S$700 and S$1,100, while master rooms in condos can command over S$1,800. This method provides a steady monthly check with significantly lower management overhead than maintaining an entire second property.

11. Start a vending machine business

Vending machines offer a unique way to earn passive income by providing snacks, drinks, or even hot meals in high-traffic locations like MRT stations and office lobbies. Once the initial setup is complete, modern 2026 machines utilize AI for inventory tracking and contactless payments, requiring only a few hours of restocking per week. Choosing a prime location is the most critical factor, as it determines your ability to quickly recover your initial machine investment.

Alternative investment passive income opportunities

Alternative investments can provide lucrative passive income streams, but they often come with higher risks compared to traditional stocks and bonds. Before investing, it's crucial to understand the potential rewards, risks, and terms associated with these options. Conduct thorough research and assess your risk tolerance before committing.

>> Discover more about alternative investment options

12. Peer-to-peer lending

P2P lending platforms connect you directly with local SMEs in need of growth capital, allowing you to act as the "bank." In 2026, these platforms are seeing average annual returns of 9% to 13%, though you must be prepared for the risk of borrower defaults. By diversifying your capital across dozens of small loans, you can mitigate individual risks while maintaining a high overall yield.

13. Private equity investments

Private equity involves investing in non-public companies, often through venture capital or private debt funds available to accredited investors. In the Q2 2026 outlook, small and mid-market buyouts are particularly attractive, with some funds targeting annualized returns of 8% to 12%. These are long-term income generating assets that typically require you to lock up your capital for several years in exchange for higher potential rewards.

>> Find out more about brokerage fees and commissions

14. Crypto staking

Crypto staking allows investors to earn passive income by participating in the validation of blockchain transactions. By staking your cryptocurrency, you contribute to the security and efficiency of the network and, in return, receive rewards in the form of additional tokens. Most investors delegate their holdings to a validator, who performs the technical work of verifying transactions.

While staking can generate attractive yields, it comes with risks. Some cryptocurrencies require you to lock up your holdings for a fixed period, limiting liquidity. Additionally, if the validator you stake with is penalised, your staked assets may also be affected. Staking opportunities are typically available for proof-of-stake (PoS) cryptocurrencies such as Ethereum (ETH), Cardano (ADA), and Solana (SOL), but not for Bitcoin.

How much can you earn?

Staking rewards vary depending on the cryptocurrency and platform used. Some exchanges offer annual percentage yields (APY) ranging from 2% to 12%, though rates fluctuate based on network conditions. For instance, staking Ethereum might yield around 2% APY, meaning a S$10,000 stake could earn approximately S$200 per year, excluding platform fees or potential price changes in the underlying asset.

Creating products for passive income

Turning your skills and knowledge into a digital product can be a rewarding way to generate passive income. Whether it's launching an online course, writing an e-book, or building a blog, these assets can continue earning money long after the initial effort is put in. The key is to create something valuable that people will want to purchase or engage with over time. If done right, product creation can become a scalable income stream that works for you even while you sleep.

15. Monetising written content for passive income

Creating a niche blog or digital publication allows you to earn through display ads, sponsored content, or affiliate marketing. By 2026, successful local content creators are leveraging AI to maintain high output, earning anywhere from S$500 to several thousand dollars a month in commissions. While it takes time to build an audience, it eventually becomes a self-sustaining asset that attracts traffic and revenue 24/7.

>> Discover more: Profitable side hustles for Singaporeans

16. Creating an online course

If you have expertise in a particular skill — whether it's coding, digital marketing, or even personal finance — you can turn your knowledge into a digital course. Platforms like Udemy allow creators to sell courses to a global audience. While creating a course requires significant upfront effort, such as structuring lessons, recording videos, and designing supplementary materials, a well-made course can continue generating income with minimal ongoing work.

How much can you earn?

Earnings from digital courses vary widely based on pricing, demand, and platform visibility. While some instructors earn a few hundred dollars per month, top course creators generate full-time incomes. On platforms like Udemy, the average instructor makes around S$4,400 per year, with high-performing instructors earning significantly more. Success depends on marketing, course quality, and engagement levels.

Earning passive income with your car

Owning a car or a parking space presents opportunities to generate passive income with minimal effort. Whether it's renting out your unused parking spot or leveraging your vehicle for advertising, these methods can help offset car-related expenses while putting your assets to work.

17. Add ads to your vehicle

Wrapping your car with brand advertisements allows you to earn a fixed monthly fee simply by driving your usual routes. In 2026, many advertising firms offer "passive" payouts of S$50 to S$150 per month depending on your car's model and the areas you frequent. This is a low-effort way to offset your monthly road tax or insurance premiums without changing your daily schedule.

18. Part-time carpooling services

Using regulated carpooling apps like GrabShare or Ryde allows you to pick up passengers heading in your same direction during your daily commute. While it won't replace a full-time salary, it is an easy way to generate additional income that can cover your monthly petrol and ERP costs. Under Singapore's 2026 carpooling rules, you can perform up to two trips a day, making it a flexible and social way to lower your vehicle's total cost of ownership.

Simple ways to cut expenses

While these methods may not generate passive income, reducing unnecessary expenses can help you save more money in the long run. The easiest way to grow your wealth is to avoid spending where you don’t need to. Here are a few simple ways to save money without any upfront investment:

Use public transport more often. Opting for buses and MRT instead of taxis or private hire cars can significantly cut monthly transport costs, especially with Singapore’s well-connected public transport system.

Lower your electricity bill. Beyond switching off lights, small changes like using energy-efficient appliances, installing water-saving showerheads, and switching to smart power strips can help reduce your monthly utility costs.

Audit your subscriptions. Many people unknowingly spend money on services they no longer use. Take time to review your digital subscriptions, streaming services, and memberships to eliminate unnecessary expenses.

>> Explore more ways to save money

SingSaver Exclusive Offer

⚽ Make your move this World Cup season. Compare top brokerage deals on SingSaver, then apply to score exclusive upsized rewards this June. Make every play count. 📈🏆 T&Cs apply.

Make the most of every trade. 📊

Set up your account in under 5 minutes, explore your options with ease, and enjoy exclusive rewards as you grow your portfolio. 🪙🏆T&Cs apply.