Learning how to pay your credit card bills is all a matter of paying attention to your amount due and payment due date. Here’s how the credit card billing cycle works, and what happens if you miss your payment.

Transitioning from a debit card to a credit card is often one of the first few indications of “adulting”. While owning a credit card is not a must for everyone, it’s an incredibly useful tool to game your finances.

But as the popular Spiderman adage goes, “with great power comes great responsibility”. It’s easy to charge all incoming transactions to your credit card blindly but when your card’s monthly bill rolls around, that’s when the panic sets in; because all of a sudden, your “invisible” expenses aren’t so invisible anymore.

Credit card bills can easily rack up in the hundreds, or even the thousands of dollars if you weren’t prudent in tracking your spending. Of course, if you can afford it, then by all means – but for many, it’s quite the opposite as they overspend beyond their means.

Remember, but it’s never too late to take charge of your finances. So if you’re struggling with managing your credit card expenditure and bills, keep reading!

Table of contents

- Understanding the credit card billing cycle

- When will you receive credit card bills?

- How to pay for credit card bills (by banks)?

- When to pay credit card bills?

- Tips to manage outstanding credit card bills

- Conclusion

Understanding the credit card billing cycle

The first thing to understand about your credit card bill is the billing cycle. There are three things to pay attention to here – the statement date, the interest-free period, and the payment due date.

The statement date is the date which your credit card bill is generated. It is fixed on the same date every month, unless there is a public holiday.

The payment due date is the date by which you have to pay your bill. The difference between the payment due date and the statement date is the interest-free period; typically, this is between 20 to 25 days.

So, for instance, if your bill’s statement date is 13 December, and your payment due date is 6 January, you have an interest-free period of 25 days.

What about transactions made on the statement date itself? Well, such transactions will be recorded in the next credit bill, which gives you up to an additional month’s time to pay your bill. For example, if you purchase a S$5,000 gaming computer package on 13 December, this transaction would be counted in the next credit card statement, issued on 13 Jan. You then have a further 25 days to make payment.

Of course, this also results in a larger credit card bill, as you’re paying two months' worth of transactions at once. This is where some people can get tripped up, as they may not have sufficient funds on hand to pay their bills in full.

When will you receive credit card bills?

In general, a billing period can either be charged by calendar month or statement month. A calendar month is more straightforward – commencing from the first day (1st) of a month to the last day (30th/31st) of the same month (e.g. 1st - 31st January).

Meanwhile, a statement month depends on your credit card’s approval date as reflected on your card’s (e-)statement. This statement month will normally appear on the top fold of your bill statement, indicating the exact date of when it commences and ends.

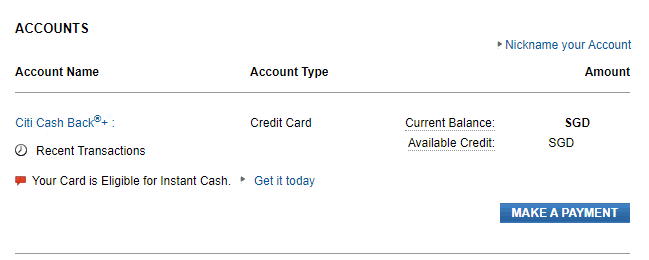

Here’s an example of a Citi credit card’s bill:

As you can see, the statement end date for this card ends on the 19th of every month, with a payment due date of around the 14th of every month. This suggests that the statement period for this Citi credit card ranges from the 20th of the previous month to the 19th of the current month (e.g. 20th September - 19th October).

Below is a rough overview of which credit cards follow the calendar and statement month formattings respectively.

|

Type of billing month

|

|

|

CALENDAR month

|

STATEMENT month

|

|

OCBC 365 Card

|

All CIMB credit cards

|

|

OCBC Frank Card

|

All Citi credit cards

|

|

OCBC Titanium Rewards Card

|

UOB Visa Signature Card

|

|

DBS Live Fresh Card

|

UOB One Card

|

|

DBS Altitude Card

|

UOB EVOL Card

|

|

DBS Woman’s Card

DBS Woman’s World Card

|

Standard Chartered Journey Card

|

|

POSB Everyday Card

|

Standard Chartered Rewards+ Credit Card

|

|

UOB Lady’s Card

UOB Lady’s Solitaire Card

|

|

|

UOB Preferred Platinum Visa Card

|

|

|

UOB PRVI Miles Card

|

|

|

KrisFlyer UOB Card

|

|

|

HSBC Advance Card

|

|

|

HSBC Revolution Card

|

|

|

Maybank Family & Friends Card

|

|

|

Maybank Horizon Visa Signature Card

|

|

|

Standard Chartered Smart Credit Card

|

|

|

AMEX Singapore Airlines KrisFlyer Credit Card

AMEX Singapore Airlines KrisFlyer Ascend Credit Card

|

|

|

OCBC 90°N Card

|

|

What if you don’t pay your credit card bill?

If you do not pay your credit card bill, in full, by the due date, several things can happen. These can range from additional charges, to a curtailment of your ability to access further credit facilities.

Let’s discuss each in detail.

You will incur a penalty charge

Once you fail to make payment before the due date, you will incur a Late Payment Fee. Typically, this amounts to a S$100 fee, levied each time you miss a payment.

As you can expect, this can cause problems for those who are finding it difficult to keep up with their credit card bills. When you’re trying to clear a S$1,000 balance, the last thing you want is to pay an extra S$100.

You will incur interest charges

You will be charged interest on the amount that is overdue, based on the prevailing interest rate determined by your card issuer. This can range from 25% to 29% per annum.

Note that overdue interest will compound daily until the outstanding amount is paid off in full, and there may be a minimum daily charge imposed. This – along with their Late Payment Fee – is why even a seemingly small credit card balance can quickly snowball into a substantial amount if you neglect to pay for a few months in a row.

If you are consistently late in paying, your card issuer may impose a higher interest rate on your outstanding balance. If that happens, you will have to keep up with your payments for a few consecutive months in order to have your interest rate lowered back down.

Your credit limit will be reduced

An immediate consequence of not paying your credit card bill in full will be that your credit limit will be reduced, and remain so until you pay off your balance, whether partially or in full.

Think of your credit card limit as a bottle of water. The water gets reduced as you spend on your card, and is only replenished as you pay your bill.

Your credit limit is predetermined by your card issuer, and different card issuers may grant you different credit limits. Usually, this is pegged at a multiple of your monthly salary, but you can also request for a specific credit limit.

For those new to credit cards, it’s a good idea to start with a lower limit – equal to a sum that you can definitely pay off within the next billing cycle. You may request for a higher credit limit as you learn how credit cards should be properly used.

Your credit score may be lowered

When choosing the credit limit to grant you, your card issuer may take your credit score into account. This is a measure of creditworthiness maintained by Credit Bureau Singapore, and can have far reaching impact on your financial destiny.

One of the main factors that impact your credit score is how you use unsecured credit facilities, such as credit cards and loans. Failure to pay your credit card bills on time signals that you are unable to use credit in a responsible manner.

This will lower your credit score, which can make it more difficult to apply for further credit facilities, such as other credit cards or personal loans. Being deemed a credit risk may also restrict you to higher interest rates, meaning you’ll have to pay a higher cost of borrowing.

Thankfully, bad credit scores are also relatively easy to repair. Pay your bills consistently on time, and your credit score will soon be restored – although your past misdeeds will still be recorded as part of your personal credit history.

Your credit card account may be suspended

If you are unable to pay off your bill in full, you may elect to pay the minimum sum. This is typically calculated at 3% of the outstanding total, or a minimum charge of S$50.

If you fail to pay even the minimum sum, further actions may be taken. This may range from increased interest charges, to even having your credit card account suspended.

Note that if your credit card balance reaches S$15,000, bankruptcy proceedings may be brought against you.

How do you pay credit card bills: DBS/POSB, UOB, OCBC, HSBC, Citibank, Maybank, CIMB, Standard Chartered

As far as technology goes, digital banking has streamlined credit card bill payments tremendously. More so, with the advent of ibanking apps, instances of phone or in-person banking have significantly decreased. All your bills (including utilities, education fees, etc.) can virtually (no pun intended) be settled via banking apps.

In general, your credit card bill can also be settled via other alternative banking methods:

- ATM

- InterBank GIRO

- Funds Transfer

- S.A.M. Machines

- AXS

- Paying directly in cash or cheque at your local branch

- Card payment from another bank’s website

- SMS payment (if applicable)

See also: Credit Card Annual Fee Waiver Guide By Banks – DBS, UOB, OCBC, & More

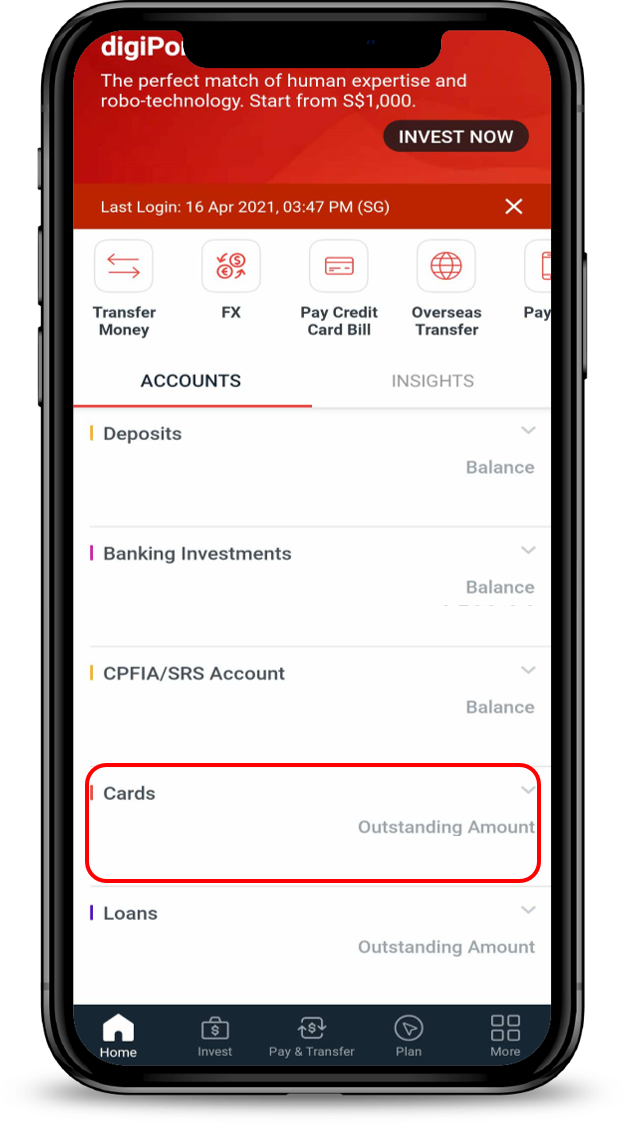

How to pay DBS/POSB credit card bills?

%201.png?width=138&height=83&name=DBS-Bank-logo%20(2)%201.png)

DBS/POSB credit card bills can be paid via the DBS digibank app.

|

Step 1

Log into your DBS digibank account

|

|

|

Step 2

Tap either:

Select the credit card you wish to make payment for

|

|

|

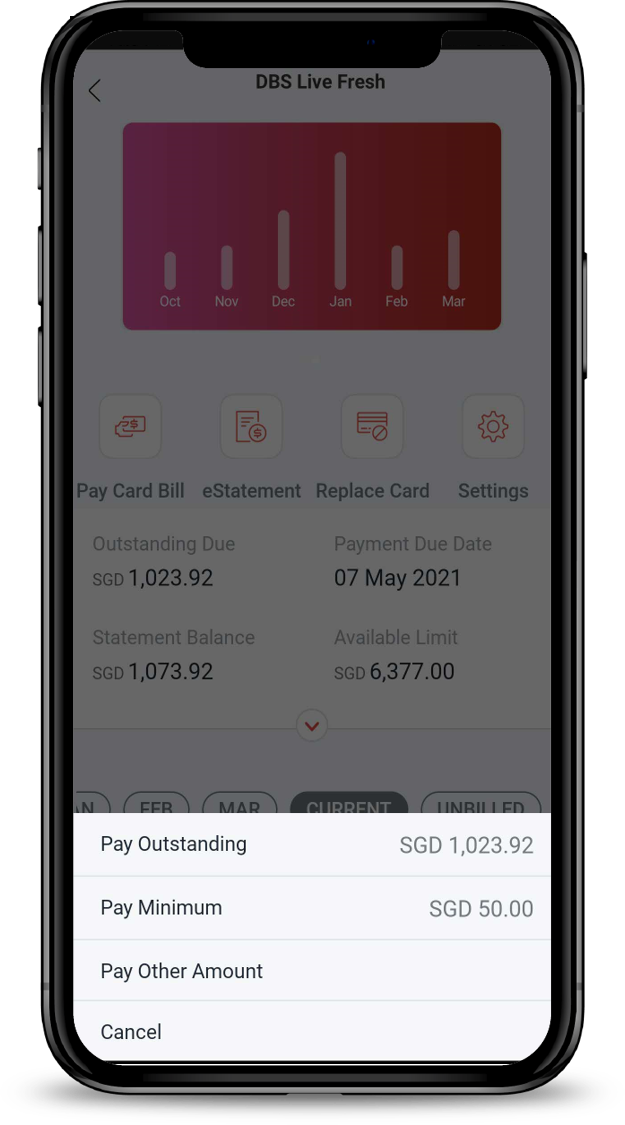

Step 3

Upon selecting “Pay Credit Card Bill”, choose either:

|

|

|

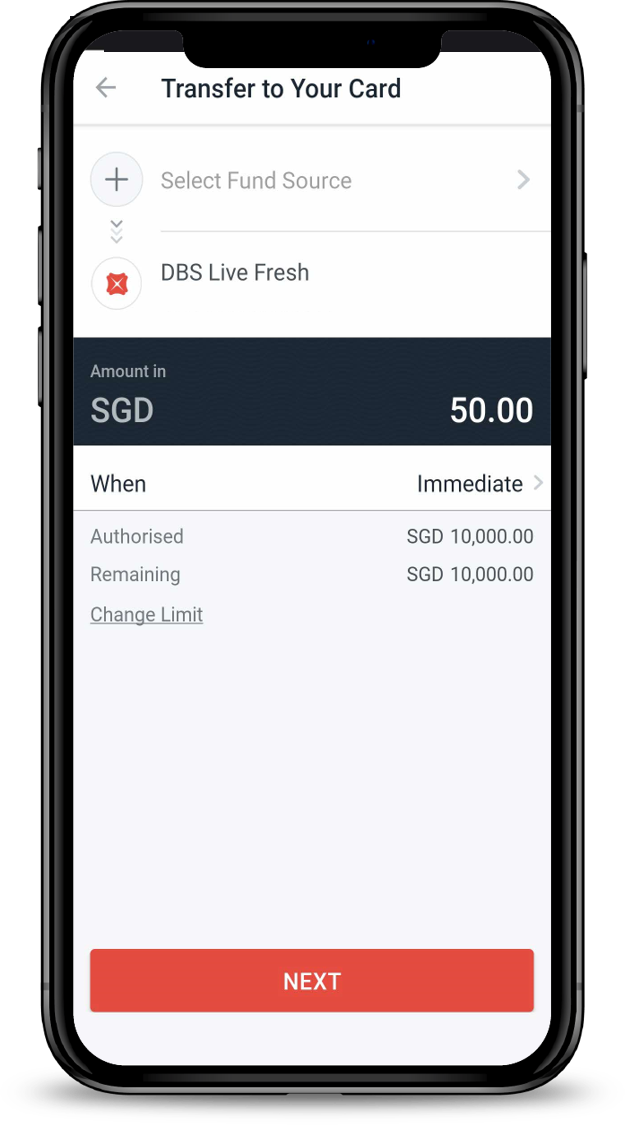

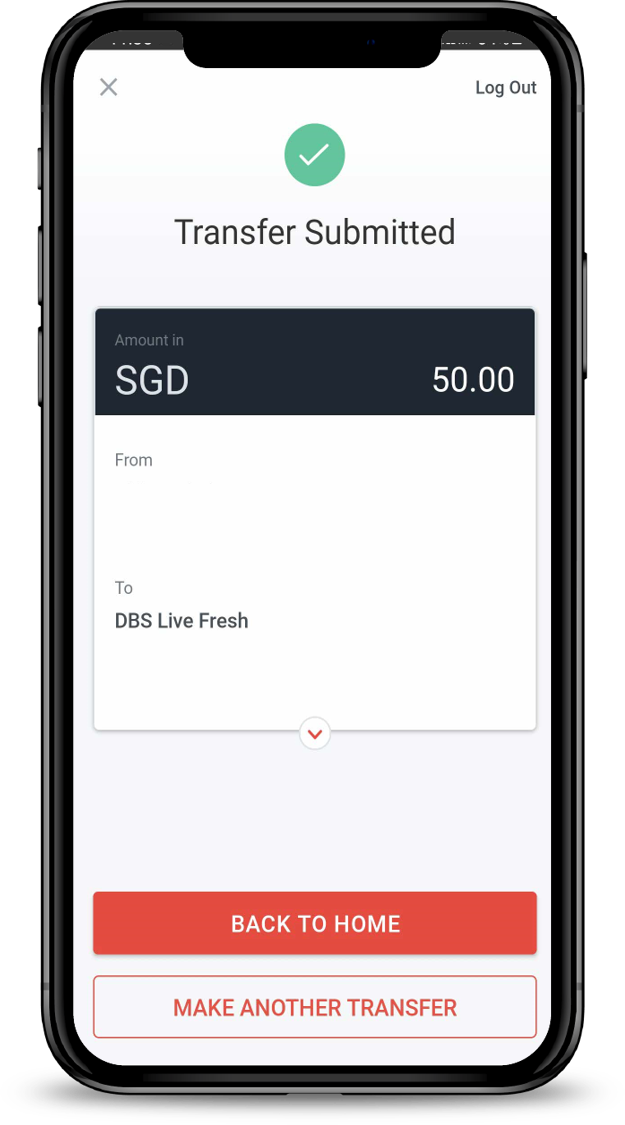

Step 4

Select “Fund Source” & enter intended “Amount” you wish to pay > Tap “Next” > Tap “Transfer Now”

|

|

|

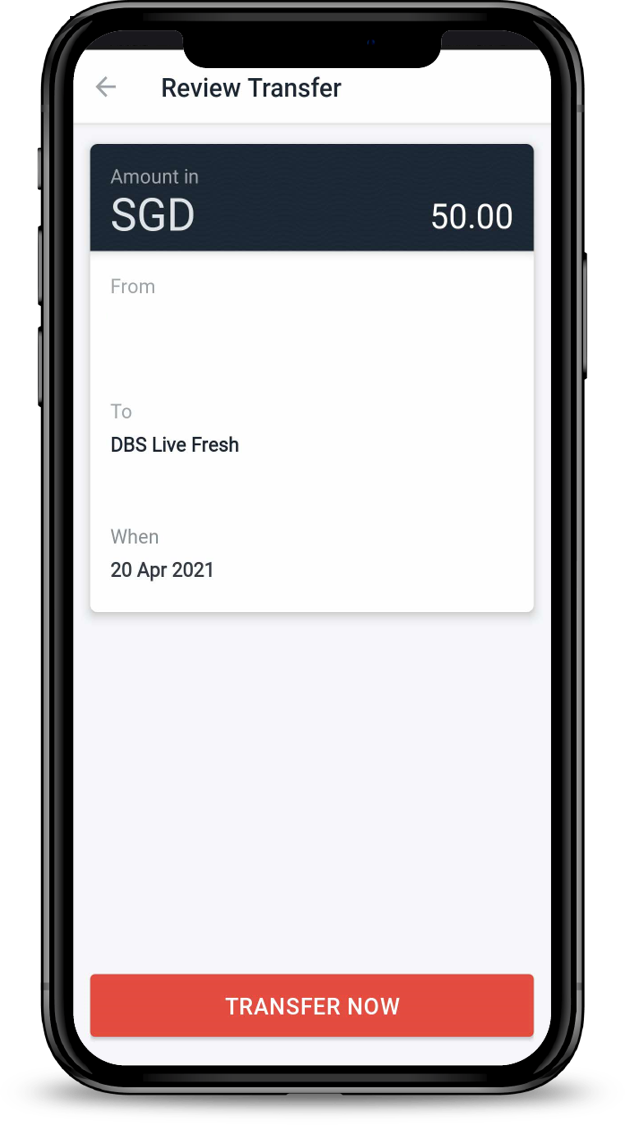

Step 5

Congrats, you’ve successfully paid your credit card bill! You should see a submission page like this.

|

|

Source: All images are adapted from DBS/POSB

How to pay UOB credit card bills?

UOB credit card bills can be paid via the UOB TMRW ibanking app.

|

Step 1

Log into your UOB TMRW ibanking account and select “Pay/Transfer”

|

|

|

Step 2

Select “My UOB Accounts/Cards” > Select the credit card you want to make payment for

|

|

|

Step 3

Enter the “Amount” you wish to pay or choose between “Minimum Payment”/”Full Payment”

Scheduling payment is also an option

|

|

|

Step 4

Review details of payment amount > Tap “Confirm” to complete payment

|

|

Source: All images are adapted from UOB

Other alternative methods to pay your UOB credit card bills include:

- Internet Banking / Phone Banking

- ATM

- InterBank GIRO

- S.A.M. Machines / AXS

- Cash

More information can be found on this UOB page.

How to pay OCBC credit card bills?

![]() OCBC credit card bills can be paid via the OCBC app.

OCBC credit card bills can be paid via the OCBC app.

|

Step 1

Log into your OCBC digital app account

|

|

|

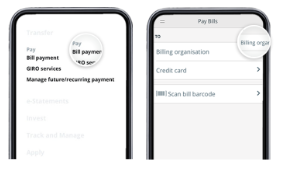

Step 2

Tap on “Bill Payment” > select “Billing Organisation”

|

|

|

Step 3

Select “Single Bill Payment” > Select relevant billing organisation > Fill in bill reference number > Slide to submit

|

|

|

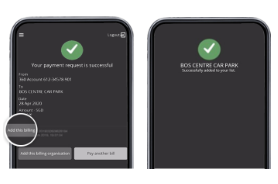

Step 4

Review payment details > Tap “Confirm” > Select “Add this billing organisation” to save details for future recurring payments

|

|

Source: All images are adapted from OCBC

For online banking instructions via desktop, refer to OCBC’s page for more details.

How to pay HSBC credit card bills?

%201.png?width=139&height=77&name=HSBC-Logo%20(1)%201.png) Note: From 25 Nov 2023 onwards, HSBC will no longer support the setting up of future-dated and recurring bill payments via HSBC Internet Banking. Recurring bill payments will have to be arranged via GIRO with your billing organisation instead.

Note: From 25 Nov 2023 onwards, HSBC will no longer support the setting up of future-dated and recurring bill payments via HSBC Internet Banking. Recurring bill payments will have to be arranged via GIRO with your billing organisation instead.

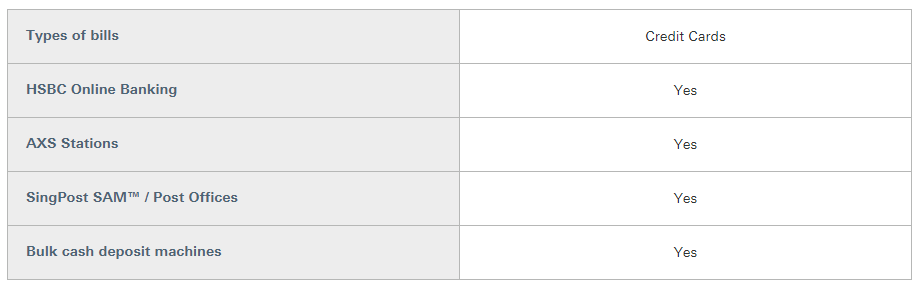

HSBC allows cardmembers to pay for credit card bills in a variety of ways.

Source: HSBC

But to pay for your bill via mobile banking, you need to set up your card’s bank as a “Billing Organisation” as a payee first via HSBC Online Banking. Thereafter, you can make recurring bill payments conveniently and securely through the HSBC app anytime, anywhere.

For ease of reference, we shall go through HSBC Online Banking mode of credit card bill payment as opposed to HSBC Mobile Banking here.

|

Step 1

Log into your HSBC Online Banking account

|

|

|

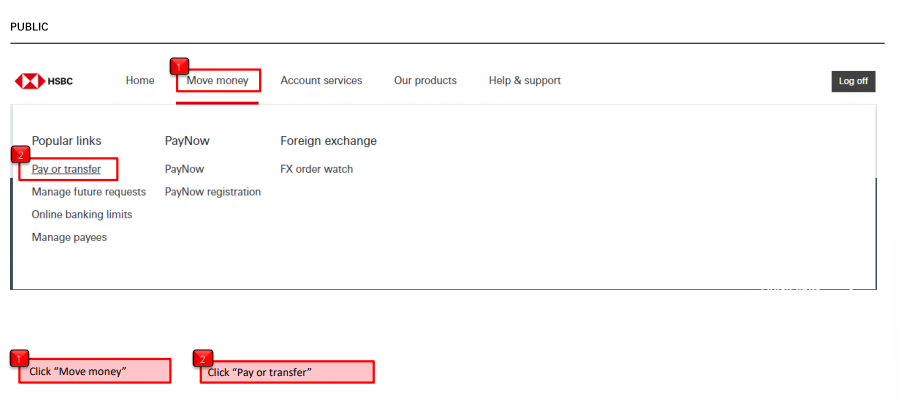

Step 2

Select “Move Money” from main tab > Select “Pay or transfer” option

|

|

|

Step 3

Select your preferred HSBC account to transfer money from > Select “New payment to a biller”

|

|

|

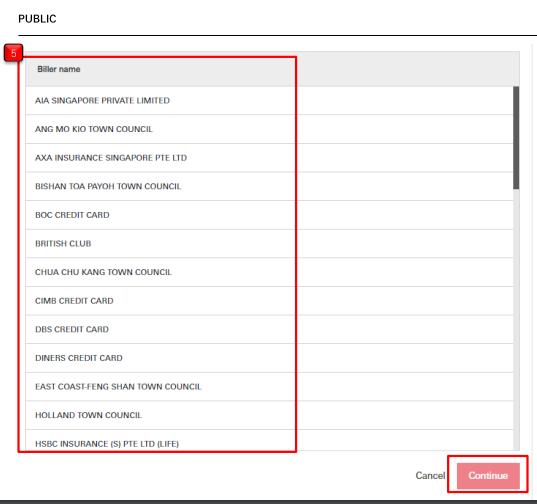

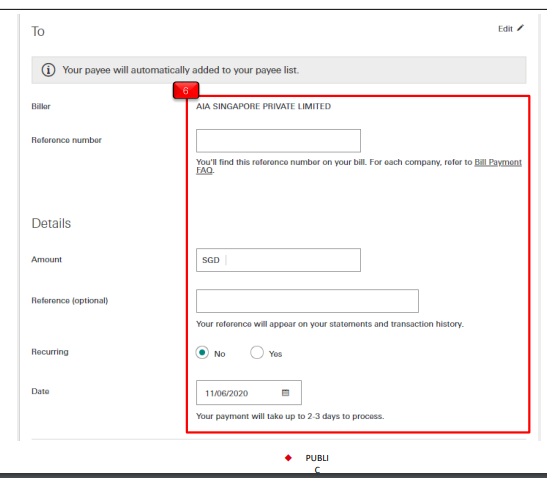

Step 4

Select correct payee biller > Tap “Continue”

Fill up required information (e.g. Reference number, amount, recurring option, date)

|

|

|

Step 5

Follow on-screen instructions to generate security code via the HSBC Singapore app > Complete transaction

|

|

Source: All images adapted from HSBC

SingSaver's Exclusive Offer: Enjoy the following rewards when you sign up for an HSBC credit card.

Receive a Dyson AM07 (worth S$459) or Apple Airpods (3rd Gen) With Magsafe Charging Case (worth S$274) or S$250 eCapitaVoucher or 15K Heymax Miles (worth a free flight to Tokyo, Japan) upon activating and spending min. S$500 by the end of the following calendar month from the card account opening date. Valid till 14 May 2024. T&Cs apply.

For HSBC TravelOne Card: Receive the above rewards when you activate and spend a min. S$500 plus pay an annual fee of S$196.20 by the end of the following calendar month from the card account opening date. Valid till 14 May 2024. T&Cs apply.

How to pay Citibank credit card bills?

.png?width=150&height=58&name=Citibank-Logo%201%20(2).png) Citibank allows cardmembers to pay for credit card bills in a variety of ways.

Citibank allows cardmembers to pay for credit card bills in a variety of ways.

Source: Citibank

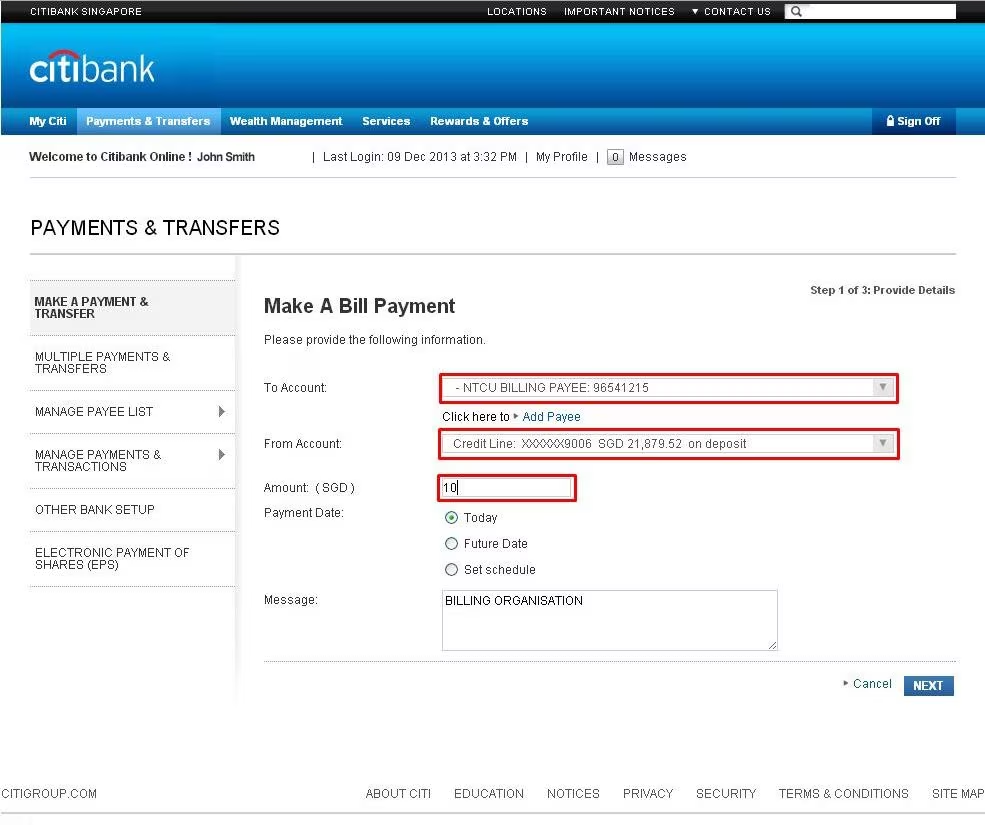

Here’s how you can pay your Citi credit card bill via Citibank Online.

|

Step 1

Log into your Citibank Online account

|

|

|

Step 2

Click “Make a Payment” under your Citi credit card account summary

Follow on-screen instructions of pop-up prompt:

|

|

|

Step 3

Tap “Add Payee” if you haven’t already added your billing organisation to your Citi account’s payee list

If you have already, fill up the following information:

*You can also make this bill payment a recurring payment by clicking “Set Schedule” and adjusting payment frequency from there

Once done, click “Next”

|

|

|

Step 4

Check payment details > Click “Make this transfer” > Done!

|

|

Source: Select images adapted from Citibank

⚡Flash Deal⚡: Be one of the first 500 applicants to get a PlayStation 5 Disc Version (worth S$799) or Dyson Airwrap (worth S$859) or S$500 ecapitaVoucher when you apply for a Citi Card and spend a minimum of S$500 within 30 days of card approval. Remaining applicants will enjoy existing rewards. Applicable to new-to-Citibank cardmembers only. Promo runs from 9 April, 9AM SGT - 2 May 2024. T&Cs apply.

SingSaver's Exclusive Offer: Receive the following rewards when you sign up for a Citi Credit Card:

Citi PremierMiles Card: Receive an Apple iPad 10th Gen Wifi 64GB (worth S$691.60) or Dyson Supersonic (worth S$699) or S$400 eCapitaVoucher or S$300 cash via PayNow upon activating and spending a minimum of S$500 within 30 days of card approval. Valid until 30 April 2024. T&Cs apply.

Other Citi Credit Cards: Receive a Dyson Supersonic (worth S$699) or Apple iPad 9th Gen 10.2 Wifi 64GB (worth S$508.30) or Dyson V8 Slim Fluffy (worth S$509) or S$400 eCapitaVoucher or S$300 cash via PayNow upon activating and spending a minimum of S$500 within 30 days of card approval. Valid until 30 April 2024. T&Cs apply.

How to pay Maybank credit card bills?

As of the time of writing, Maybank credit card bills can be paid via the following methods:

As of the time of writing, Maybank credit card bills can be paid via the following methods:

- Over-the-counter cash payments at Maybank branches

- Cheque payments made to “Maybank A/C No. XXXX XXXX XXXX XXXX”

- For more than 1 account payment, please address the cheque to “Maybank Cards” instead

- Interbank GIRO

- Maybank ATM

- Maybank Cash Deposit Machines

- Maybank Mobile Banking

- AXS Stations

- SingPost SAM

Note: Since 20 Oct 2023, payments made to Maybank and Other Banks’ credit cards have been suspended on classic Maybank Online Banking. The classic Online Banking portal is being discontinued and is being replaced by their new Maybank2u Online Banking portal instead.

How to pay CIMB credit card bills?

![]() CIMB credit card bills can be paid via several methods:

CIMB credit card bills can be paid via several methods:

- CIMB Clicks Internet Banking

- Auto-Debit / Interbank GIRO

- Internet banking from other banks

- AXS

- CIMB branches

- Cheques

Out of these options, the easiest payment method would probably be CIMB Clicks Internet Banking option. Simply follow the steps below:

- Log in to your CIMB Clicks Internet Banking account via this portal

- On the left menu: Select “Clicks Settings” > Select “Link my CIMB Credit Card” (You may skip this step if you already linked your card)

- On the left menu: Select “Bill Payment” > Select “Pay to CIMB Credit Cards” (Choose the credit card you wish to settle payment for)

- Key in transfer amount > Finalise transaction

Alternatively, if you wish to set up a recurring payment channel via GIRO for your CIMB credit card, please refer to the instructions here.

SingSaver Exclusive Offer: Receive S$280 cash via PayNow upon activating your CIMB credit card and spending min. $988 for 60-day periods following card approval. Valid until 2 May 2024. T&Cs apply.

How to pay Standard Chartered credit card bills?

%201.png?width=150&height=58&name=Standard_Chartered_(2021)%201.png) Standard Chartered (SCB) credit card bills can be paid via three methods:

Standard Chartered (SCB) credit card bills can be paid via three methods:

- Funds transfer from SCB current or savings account either via online or mobile banking

- Funds transfer from other bank's accounts using Fast and Secure Transfers (FAST)

- Payment via SCB's Cash Deposit Machines (CDM)

To use SCB's online or mobile banking function, follow these instructions:

- Log in to your Standard Chartered Online Banking or Mobile Banking Account

- For online banking: Select "Transfers & Payments" > "Pay SC Credit Cards"

- For mobile banking: Select "Pay & Transfer" > "Pay Credit Card"

- Select the credit card you intend to make payment for

- Follow on-screen instructions to complete the transaction process

- You're done!

For more details on the other credit card bill payment methods, refer to this SC page.

SingSaver's Exclusive Offer: Enjoy the following rewards when you sign up for a Standard Chartered credit card. Eligible for new Standard Chartered cardholders only.

.png?width=800&height=250&name=SCB_LIGHTNING_BLOGARTICLE_KV1_800x250%20(2).png)

⚡Flash Deal⚡: Get a PlayStation 5 Disc Version (worth S$799) or Dyson Airwrap (worth S$859) or S$500 e-capita Vouchers as one of the first 500 to apply for an SCB Simply Cash Card with a min. spend of S$500 upon card approval. Remaining applicants will enjoy existing rewards. Valid till 12 May 2024. T&Cs apply.

.png?width=800&height=250&name=SCB_SIMPLY_BLOGARTICLE_800x250%20(2).png)

Plus, get an additional S$20 e-Capitaland Voucher when you split the payment for your purchases with SCB Easy Pay, pay your bills with SCB Easybill or put any of your purchases on instalment in SCB Savings Account or Current Account within 60 days of approval. Valid till 12 May 2024. T&C applies.

.png?width=800&height=250&name=SCB_Smart_BLOGARTICLE_800x250%20(2).png)

Standard Chartered Smart Card and Rewards+ Card: Receive an Apple iPad 9th Gen 10.2 Wifi 64GB (worth S$508.30) or Apple AirPods Pro 2nd Generation (worth $365.70) or Nintendo Switch Gen 2 (worth S$399) or up to S$300 cash upon activating and spending min. S$250 spend within 30 days of card approval. Also, get an additional S$20 e-Capitaland voucher when you make a min. spending of S$1,000 in your 2nd month. Valid till 12 May 2024. T&Cs apply.

Plus, get an additional S$20 e-Capitaland Voucher when you split the payment for your purchases with SCB Easy Pay, pay your bills with SCB Easybill or put any of your purchases on instalment in SCB Savings Account or Current Account within 60 days of approval. Valid till 12 May 2024. T&C applies.

Standard Chartered Journey Credit Card Only: Receive a Dyson AM07 (worth S$459) or Apple AirPods (3rd Gen) With Magsafe Charging Case (worth S$274) or up to S$120 cash upon activating your card within 30 days and no minimum spend required. Also, get an additional S$20 e-Capitaland voucher when you make a min. spending of $1,000 in your 2nd month. Valid till 12 May 2024. T&Cs apply.

Get an additional S$20 e-Capitaland Voucher when you split the payment for your purchases with SCB Easy Pay, pay your bills with SCB Easybill or put any of your purchases on instalment in SCB Savings Account or Current Account within 60 days of approval. Valid till 12May 2024. T&C applies.

Plus, receive up to 45,000 miles when you apply with annual fee payment (S$196.20 incl. GST) and make a min. spend of S$3,000 within 2 months of card approval. Valid till 30 June 2024. T&Cs apply.

When to pay for your credit card bill?

When it comes to credit card bills, common sense would dictate to pay either early or on time; and it goes without saying that late payments will incur penalty fees. However, which is more ideal: Paying early or on time?

Which is better: Paying credit card bills early vs on time?

Theoretically, there is no fundamental drawback to paying your credit card bill early; if anything, it’s a good practice to do so. This is because bank transactions – regardless of mobile or internet banking – can take up to a few days to be fully processed.

Suppose your credit card bill’s due date is 31 October 2023, theoretically, you shouldn’t be penalised because you’re fulfilling the payment by the stipulated deadline. However, because the bank transaction might require some time to successfully go through, your credit card’s bank might only receive the payment a few days later.

As a result, your card’s bank might deem your credit card bill payment late in such situations and potentially impose late fees. To rectify this issue, you’d need to contact your card’s bank to explain and reverse any fees imposed. But, you should advisably only do so once the payment amount has successfully been transacted over from your bank account to your card’s account.

If you abide by these steps, your credit card bill should be properly paid for and any imposed late fees should be reversed or nullified.

The only downside to paying your credit card bill too prematurely might be a lack of funds in your bank account to fully pay the amount. But that’s just a minor downside.

What if you don’t pay your credit card bill?

If you do not pay your credit card bill, in full, by the due date, several things can happen. These can range from additional charges, to a curtailment of your ability to access further credit facilities.

Let’s discuss each in detail.

You will incur a penalty charge

Once you fail to make payment before the due date, you will incur a Late Payment Fee. Typically, this amounts to a S$100 fee, levied each time you miss a payment.

As you can expect, this can cause problems for those who are finding it difficult to keep up with their credit card bills. When you’re trying to clear a S$1,000 balance, the last thing you want is to pay an extra S$100.

You will incur interest charges

You will be charged interest on the amount that is overdue, based on the prevailing interest rate determined by your card issuer. This can range from 25% to 29% per annum.

Note that overdue interest will compound daily until the outstanding amount is paid off in full, and there may be a minimum daily charge imposed. This – along with their Late Payment Fee – is why even a seemingly small credit card balance can quickly snowball into a substantial amount if you neglect to pay for a few months in a row.

If you are consistently late in paying, your card issuer may impose a higher interest rate on your outstanding balance. If that happens, you will have to keep up with your payments for a few consecutive months in order to have your interest rate lowered back down.

Your credit limit will be reduced

An immediate consequence of not paying your credit card bill in full will be that your credit limit will be reduced, and remain so until you pay off your balance, whether partially or in full.

Think of your credit card limit as a bottle of water. The water gets reduced as you spend on your card, and is only replenished as you pay your bill.

Your credit limit is predetermined by your card issuer, and different card issuers may grant you different credit limits. Usually, this is pegged at a multiple of your monthly salary, but you can also request for a specific credit limit.

For those new to credit cards, it’s a good idea to start with a lower limit – equal to a sum that you can definitely pay off within the next billing cycle. You may request for a higher credit limit as you learn how credit cards should be properly used.

Your credit score may be lowered

When choosing the credit limit to grant you, your card issuer may take your credit score into account. This is a measure of creditworthiness maintained by Credit Bureau Singapore, and can have far reaching impact on your financial destiny.

One of the main factors that impact your credit score is how you use unsecured credit facilities, such as credit cards and loans. Failure to pay your credit card bills on time signals that you are unable to use credit in a responsible manner.

This will lower your credit score, which can make it more difficult to apply for further credit facilities, such as other credit cards or personal loans. Being deemed a credit risk may also restrict you to higher interest rates, meaning you’ll have to pay a higher cost of borrowing.

Thankfully, bad credit scores are also relatively easy to repair. Pay your bills consistently on time, and your credit score will soon be restored – although your past misdeeds will still be recorded as part of your personal credit history.

Your credit card account may be suspended

If you are unable to pay off your bill in full, you may elect to pay the minimum sum. This is typically calculated at 3% of the outstanding total, or a minimum charge of S$50.

If you fail to pay even the minimum sum, further actions may be taken. This may range from increased interest charges, to even having your credit card account suspended.

Note that if your credit card balance reaches S$15,000, bankruptcy proceedings may be brought against you.

Read more:

Will a Debt Consolidation Plan Affect My Credit Score?

Two Strategies to Consider When Clearing Debt in Singapore

Not Ju$t You: Swimming in Debt in Singapore

What to do if you owe an outstanding credit card balance?

This brings us to our next question: What if you paid your credit card’s minimum amount already? What’s the next best course of action to take?

Once you’ve paid the minimum balance, you should formulate a plan to clear off the outstanding owed amount as soon as possible. Unless you can somehow spontaneously manifest money out of thin air, you’re better off opening a balance transfer account.

What is a balance transfer?

In short, a balance transfer is an account that lets you move your debt from one account to this new one with low or 0% interest rate. While the owed principal debt amount remains the same, you’re at least able to stave off any interest from incurring – allowing you to both pay off your debt faster and manage your credit score.

For instance, imagine you owe S$1,500 on your credit card bill and require at least one month to fully pay off the remainder (not counting interest). By transferring your outstanding debt into a balance transfer amount, you’re now granted an interest-free grace period of about six to 12 months. This allows you to consistently pay off your debt without incurring additional interest.

Needless to say, you should avoid making any new purchases with your credit card (or other credit cards for that matter).

Read more:

How Do Balance Transfers Work and Should You Get One?

Unpaid Credit Card Bills? Here's How a Balance Transfer Can Help

💡 Pro-tip #1: If you’re already struggling with credit card bills, do not attempt to apply for a new credit card or use another existing credit card to pay off your outstanding debt. That would just be an unwise and irresponsible decision at that point.

💡 Pro-tip #2: Alternatively, you can consider opting for a personal instalment loan to pay off your credit card debt. These loans tend to charge a lower interest rate of about 6% p.a. But we recommend looking out for those with promotional offers of 0% p.a. interest on the first three months, for example.

Read more:

Standard Chartered CashOne Personal Loan Review

Citibank Quick Cash Loan Review

Best DBS Personal Loan Promotions in Singapore

Best Short-Term Personal Loans in Singapore

Conclusion

At the end of the day, the biggest takeaways for managing your credit card bills are: to pay your bills early (the earlier the better) or on time, and pay the minimum amount at least if you’re unable to afford the full amount by the due date.

Remember, responsible credit card management not only helps you avoid late fees and high-interest charges but also paves the way for better financial stability and a stronger credit score, opening doors for more financial freedom and opportunities in the future. 🙂

💡 Pro-tip: We recommend tracking your credit card bills on your calendar – whether physical or digital, we leave it up to your preference. Personally, I prefer using the Google Calendar because it’s already synced up to all my Google accounts (personal, work) and other important existing data.

Besides that, it can also be added to your phone’s and desktop’s homepage as a widget for easy and convenient reference. Thank you technology!

Read these next:

4 Ways to Pay Off Credit Card Debt in Singapore

10 Commandments of Credit Cards You Should Follow

Should I Use My Credit Card to Pay For Everything?

Citi PayAll vs SC EasyBill vs CardUp: Bill and Tax Payment

Unpaid Credit Card Bills? Here's How a Balance Transfer Can Help

Back to Blog

Back to Blog