Will Cancelling a Credit Card Hurt My Credit Score?

Updated: 11 Dec 2025

Thinking about cancelling a credit card? It might seem like a simple way to declutter your wallet, but hold on! Closing a credit card does actually affect your credit score. The impact depends on a few things, like how much of your credit limit you're using, your credit history, and your overall financial habits. Let's dive in and understand the effect of closing a credit card.

Whether you're looking to streamline your finances or simply want to get rid of an unused card, understanding the potential consequences is crucial for maintaining a healthy credit profile.

Find the right credit card for you in no time. 💳✨

Compare exclusive offers on SingSaver across cashback, miles, and rewards cards—plus enjoy stackable welcome gifts.

How will closing a credit card hurt your credit score

Your credit utilisation percentage can increase, lowering your credit score

When you cancel a credit card, you're essentially reducing your total available credit. This can push up your credit utilisation ratio – the percentage of available credit you're using. A higher credit utilisation ratio can negatively impact your credit score, making it appear as though you're heavily reliant on credit.

Older credit is better than new credit when it comes to credit score

The length of your credit history plays a significant role in determining your credit score. Cancelling an older credit card does shorten your credit history, potentially lowering your score. Lenders like to see a long and responsible track record of managing credit.

Other potential credit score impacts

Closing a credit card can have other effects on your credit score:

-

Reduced credit mix: If the cancelled card was your only credit card, your credit mix might take a hit. Lenders like to see that you can handle different types of credit, like loans and credit cards.

-

Impact on future credit approvals: A shorter credit history or higher credit utilisation due to closing a card could make it harder to get approved for loans or new credit cards in the future.

>> More: The 10 Commandments of Credit Cards You Should Always Follow

When it makes sense to close a credit card

The card has a high annual fee and you don’t use the rewards

If your credit card comes with a hefty annual fee but the rewards don't justify the cost, cancelling the card might be a smart move.

However, remember that even an unused card can benefit your credit score, especially if it has a high credit limit and was closed in good standing, with all balances paid off before closure.

Before cancelling, consider whether the card issuer offers any alternatives to help you retain your credit history and avoid the potential negative impact of closing the account. It's also worth checking if you can product switch to a different card with more relevant rewards that better suit your spending habits.

You struggle with overspending

If having access to a particular credit card consistently leads to overspending and financial mismanagement, cancelling it might be a good step towards improving your financial discipline. Sometimes, removing temptation is the best way to stay on track.

However, before you cancel, consider if there are other ways to manage your spending. Could you apply for a secured card? Or perhaps create a stricter budget and track your expenses more closely? If you're struggling with credit card debt, consider seeking professional help from a credit counsellor. Cancelling a card should be a last resort when other methods of managing your finances have failed.

>> Read next: 5 Ways to Get the Highest Credit Score in Singapore

You want to renew eligibility for sign-up bonuses

Some banks offer attractive sign-up bonuses to entice new credit card customers. These bonuses can include rewards points, cashback, or even air miles.

For example, if you've had a credit card with a particular bank for a while and are eyeing a juicy sign-up bonus for a new online shopping credit card they offer, cancelling your existing card might make you eligible for the bonus again.

However, weigh the potential benefits of the sign-up bonus against the potential impact on your credit score. If cancelling the card significantly increases your credit utilisation or shortens your credit history, it might not be worth it in the long run.

SingSaver x OCBC INFINITY Cashback Credit Card Exclusive Offer

Apply for an OCBC INFINITY Cashback Credit Card via SingSaver and choose from S$400 Cash, 25,000 MaxMiles by HeyMax (worth S$600 in travel value), Dyson Airstrait, Dyson V8 Cyclone cordless vacuum, or Samsung Galaxy Buds4 Pro + S$180 eCapitaVoucher Bundle. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$80 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

I don’t want to cancel my credit card: Other options

Downgrade to a no-annual-fee card

If the main reason you're considering cancelling a credit card is the annual fee, explore whether you can downgrade to a no-annual-fee version with the same issuer. This allows you to keep your credit history intact while eliminating the recurring cost.

Many credit card companies offer a variety of cards with different features and fee structures. By downgrading, you can essentially keep your account open but switch to a less expensive option. This can be a win-win situation, allowing you to save money while maintaining a positive credit history.

>> Read next: Best Credit Cards in Singapore for February 2025

Reduce credit limit

If you're worried about overspending and tempted to cancel your credit card altogether, consider requesting a credit limit reduction instead. This allows you to keep the card active and maintain your credit history, while limiting your spending capacity and reducing the risk of accumulating excessive debt.

Lowering your credit limit can be a useful strategy for managing your finances and building responsible credit habits. It can also be a good option if you're working to improve your credit utilisation ratio, as a lower credit limit can make it easier to keep your balance low relative to your available credit.

Keep the card active with occasional small purchases

If you're hesitant to cancel a credit card because of its potential impact on your credit score, consider keeping it active by making small, occasional purchases. This prevents the account from being closed due to inactivity, which can negatively affect your credit history.

By using the card for small expenses and paying off the balance in full each month, you can demonstrate responsible credit management and maintain a positive payment history. This can help strengthen your credit score over time and improve your chances of getting approved for future credit applications.

How to deactivate a credit card the right way

So, you've weighed the pros and cons and decided to close your credit card, but you’re now wondering, ‘How can I cancel my credit card without causing unnecessary damage to my credit score?’.

Here's a step-by-step guide to help you close your credit card the right way:

Pay off all outstanding balance

Before you close a credit card, it's crucial to pay off your entire outstanding debt, including any pending charges. This ensures that you don't leave any lingering debt that could accrue interest and potentially damage your credit score.

Closing a credit card with an outstanding balance can be seen as a red flag by lenders, suggesting financial instability. It's always best to settle your dues in full before closing an account to maintain a positive credit history and avoid any negative repercussions.

Redeem any unused rewards

Don't let those hard-earned rewards go to waste! Before you close your credit card account, make sure to redeem any unused rewards points, cashback, or air miles. Some cards may automatically forfeit your rewards balance upon cancellation, so it's best to use them up or transfer them to another account if possible.

Check your card's rewards program for redemption options and deadlines. You might be able to convert your points into cash rebates, vouchers, or merchandise. Redeeming your rewards is a smart way to maximise the value of your credit card before closing it.

Contact your bank and request account closure

Once you've paid off your balance and redeemed your rewards, it's time to officially close your credit card account. Contact your bank's customer service department and request account closure. They may ask you to confirm your identity and provide some information about your account.

Some banks may require you to submit a written request or complete a cancellation form. Be sure to follow their instructions carefully to ensure the account is closed properly. It's also a good idea to request written confirmation that the account has been closed to prevent any future issues or disputes.

Monitor your credit report post-cancellation

After cancelling your credit card, it's a good practice to monitor your credit report to ensure the account closure is accurately reflected. You can obtain a copy of your credit report from the Credit Bureau Singapore (CBS). Check for any errors or discrepancies and make sure the account status is updated correctly.

>> Read next: 3 Reasons To Cancel Your Credit Card (And How To Do Just That)

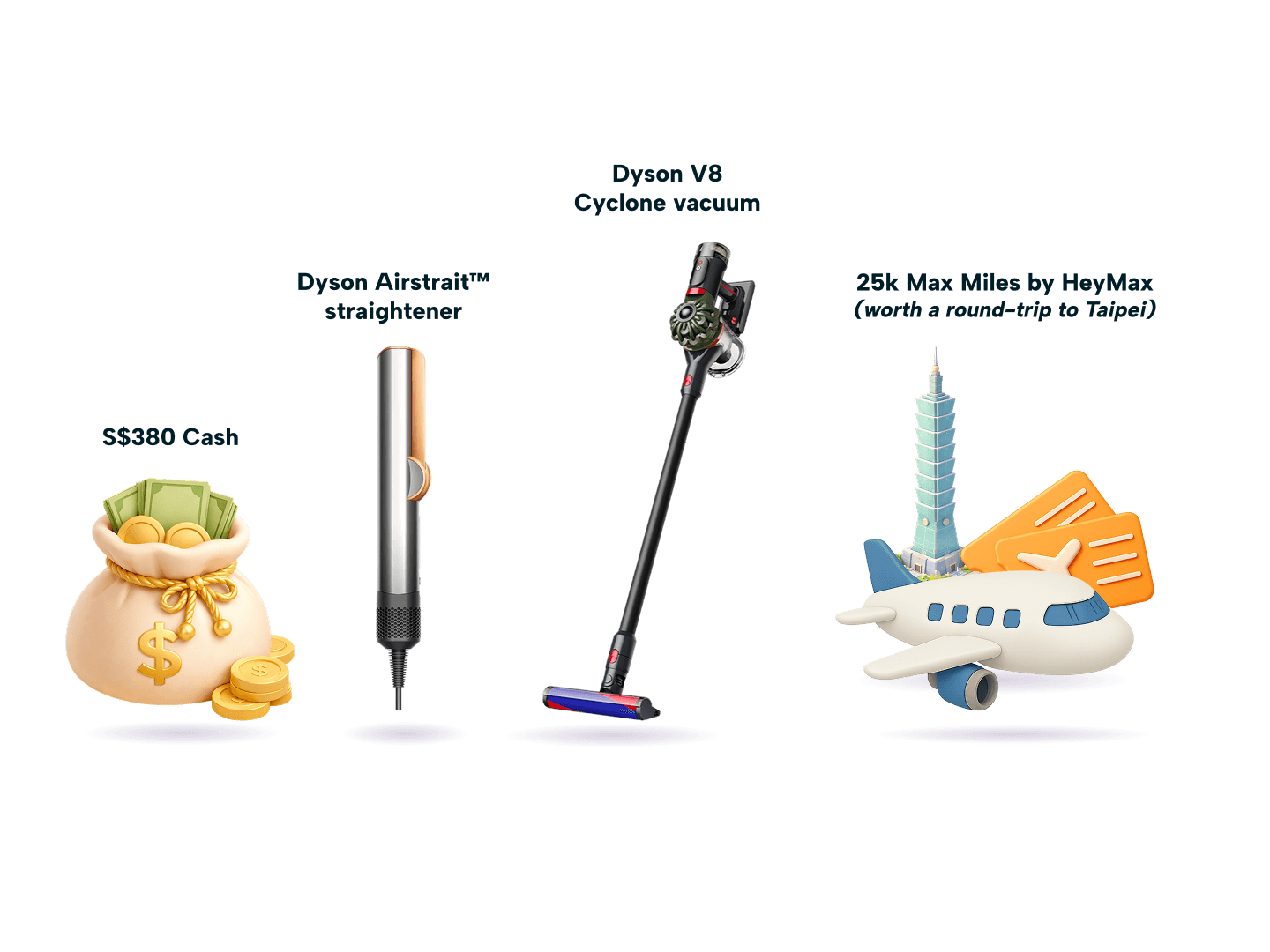

SingSaver Exclusive Offer

Apply for a Citi Cashback+ Credit Card via SingSaver and score S$380 Cash, 25,000 Max Miles by HeyMax (worth S$600 in travel value), Dyson Airstrait or V8 Cyclone cordless vacuum, or Sony WF-1000XM6 (Earbuds) + S$50 eCap bundle upon activating and spending a minimum of S$500 within 30 days of card approval. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.