Joint couple’s credit card: All you need to know

Updated: 22 May 2025

Making a shared credit card work may just be one of those new couple goals you would like to achieve. Here are the potential benefits and risks to know about before applying for a joint credit card.

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

What is a joint credit card for couples?

A joint credit card account is a credit card account held by two individuals, where both are authorised to make purchases and are equally responsible for the debt incurred. This means that both individuals' credit histories are linked to the account, and both are liable for repaying the entire balance (or debt), regardless of who made the charges.

However, it's important to note that joint credit cards for couples are not a standard product offered by most banks in Singapore.

Instead, couples here often manage shared expenses through supplementary cards (where one person is the primary cardholder, and the other is an additional or supplementary cardholder) or shared accounts (using a single credit card account, but with careful tracking and communication).

Sounds like your thing? Depending on how savvy you are when it comes to making credit cards work hard for you, a credit card for couples can accelerate your rewards journey by leaps and bounds.

But of course, there are tricks you can employ to make this happen. Read on to find out the pros and cons of sharing a credit card account and discover our curated selection of cards for couples (like the UOB One Card and Maybank Family & Friends Card) as well as tips on managing a shared credit card account!

What to know before sharing a credit card account

Combining your finances as a couple, whether through a formal joint credit card, supplementary card, or joint bank account, involves significant financial and interpersonal considerations. It's crucial to understand the implications before proceeding so that you can protect both your financial freedom and your relationship.

Looking for a new credit card?

Discover the top cashback, travel, miles, and rewards credit cards in Singapore on SingSaver. Find the perfect addition to your financial strategy.

Advantages of using a credit card for couples

While true joint credit cards are rare in Singapore, sharing a credit card account (or using supplementary cards) can offer some advantages, including:

-

Benefit from first-time sign-up bonuses: Most banks in Singapore offer rewards to entice new customers to sign up for their credit cards. To be eligible for the reward, though, you often have to hit a minimum spend within a specific period of time. Consolidating you and your partner’s spending on one card can help you reach the minimum spending requirement that much faster.

-

Earn rewards faster: The main reason for getting a credit card is to maximise the rewards you earn, whether that is in the form of cashback, miles, or vouchers. When you share a credit card with your partner, more qualifying transactions will naturally be made, leading to quicker earning and accumulation of rewards. This is especially helpful if your chosen credit card has a fairly high monthly minimum spend requirement.

-

Potentially pay less in annual fees: Given that the average annual fee for mainstream credit cards in Singapore is S$196.20, applying—and paying—for one joint primary credit card can be a financially savvy move that doesn’t compromise on the benefits you enjoy. For those who would like to skip annual fee payment altogether, be sure to check out our guide to asking for credit card annual fee waivers.

Disadvantages of using a credit card for couples

Despite the benefits you can reap, there are also potential pitfalls to weigh up before committing to sharing a card as a couple:

-

Liability for co-owner’s debt: Even with supplementary cards, the primary cardholder is liable for all debt incurred on the card, including spending by the supplementary cardholder. Racking up charges that you can’t pay back or missing bill payments could affect the primary cardholder’s credit score.

-

No increase in rewards due to caps: Depending on the credit card you hold, there may be rewards caps in place, making it impossible for you and your other half to chalk up more rewards despite a higher amount of eligible spending.

-

Can be inconvenient to track and split expenses: While earning and accumulating credit card rewards at an accelerated rate sounds nice in theory, tracking and splitting expenses to make sure you hit the minimum spend can get tedious.

-

Supplementary credit cards may come with annual fees: Not all supplementary credit cards are free for use – it all depends on the banks and the exact primary card you’re holding.

-

Affected by changes to your relationship: If your relationship ends (for whatever reason), you may have to cancel the credit card or open a new credit card as a replacement, which can negatively impact your credit scores.

Remember: sharing a credit card or account requires a higher level of trust and open communication between both parties to avoid financial misunderstandings and disputes.

» MORE: 4 questions couples should ask before opening a supplementary credit card

Why you might want a joint credit card account

All that said, a joint credit card account still holds its appeal for the following reasons:

-

Simplified financial management: A single card can streamline the tracking and payment of shared or recurring expenses, such as groceries, utilities, and dining out.

-

Clearer picture of combined spending: A single statement provides a consolidated view of joint spending, facilitating more effective budgeting.

-

Reduced need for frequent fund transfers: A joint credit card can minimise the need for constant transfers between individual accounts to cover shared costs.

-

Ease of paying recurring shared bills: If applicable, a joint credit card can simplify the payment of recurring shared bills.

Best credit cards for couples in Singapore (2025)

For couples who prioritise cashback

Product details

-

Up to 10% Cashback (20% for new cardholders until June 30, 2025) on eligible merchants

-

Up to 4.33% Cashback on Singapore Power (SP) utilities bills.

-

Base Cashback: 3.33% on all eligible retail spend (excluding mobile wallet top-ups, insurance, school fees, etc.) when meeting minimum spend.

-

Fuel Savings: Up to 24% at Shell and SPC petrol stations.

-

Earn up to 8.33% cashback quarterly with a minimum spending of $500 per month

-

Earn up to 10% cashback quarterly with a minimum spending of $2,000 per month

-

3.33% base cashback rate with a minimum spending of S$500 per month, for transactions not with selected partners

-

Up to 24% savings on fuel at Shell

-

Up to 22.66% off petrol purchases at SPC

-

Automatic fee waiver in first year

-

First supplementary card is free

-

Complimentary travel insurance – public conveyance accident coverage up to S$500,000 and COVID-19 emergency assistance, evacuation and repatriation up to S$50,000

SingSaver’s take

This credit card is a great choice if you intend to share the card or get a supplementary card for your significant other. UOB One’s cashback is tiered: you’ll earn 3.33% base cashback if you spend at least S$500, S$1,000, or S$2,000 per statement month for each qualifying quarter (i.e. S$50, S$100, S$200 cashback per quarter).

There's also an additional cashback of 5% if you spend S$500 or S$1,000 per month in a quarter, and 6.67% cashback if you spend S$2,000 per statement month for each qualifying quarter.

For couples who spend consistently in chosen categories

Product details

-

Earn up to 8% globally on 5 categories, choose from: beauty & wellness, data communication & online streaming, dining & food delivery, entertainment, groceries, online shopping, pharmacy, retail & pets, sports & sport apparel, transport

-

Minimum spend of S$800 monthly to earn bonus cashback rate

-

Base cashback rate of 0.3% on monthly spending below S$800

-

Monthly cap of S$125 bonus cashback (S$25 per category)

-

Earn additional bonus cashback for spending in MYR and IDR

-

Enjoy exclusive cardholder privileges such as dining deals

SingSaver’s take

Maybank Family & Friends Card is another strong contender if you’re looking to share your credit card account with your partner. Simply decide on the five categories you spend most on and start racking up bonus cashback with a minimum monthly spending of S$800 – that works out to an average of just S$400 per person.

For couples who travel frequently

Product details

-

Earn 3 mpd on Singapore Airlines, Scoot, Kris+ and KrisShop purchases

-

Earn up to 3 mpd on dining, food delivery and online shopping with a minimum annual spend of S$800 on Singapore Airlines, Scoot and KrisShop

-

Earn 1.2 mpd on all other spend

-

Fast tracked way to KrisFlyer Elite Silver status

-

Enjoy exclusive cardholder privileges, including complimentary welcome miles, KrisShop rebates, complimentary KrisShop tier upgrades, and more

SingSaver’s take

If you and your partner are gunning for Singapore Airlines award tickets, consider the KrisFlyer UOB Credit Card that lets you earn unlimited 3 KrisFlyer miles per S$1 spent on dining, food delivery, online shopping, travel, transport and SIA-related purchases, unlimited 1.2 KrisFlyer miles per S$1 on all other spends.

The one thing you need to be aware of for this credit card is its bonus miles crediting cycle: all bonus miles earned will only be awarded within two months after your card membership year. The odd crediting policy may or may not be a deal breaker for you, depending on how you look at it.

For couples who shop online frequently

Product details

-

Earn up to 10X Rewards points for online spending

-

Earn 1X Reward point for all other spending

-

No minimum spend required to earn base Rewards points

-

Rewards points are credited to your account and can be converted to miles at various airlines

-

Rewards points can be used to offset spending and split purchases into monthly instalments

-

Enhanced 4 mpd rate for online and contactless spend is subject to a monthly cap

-

Supported by various payment platforms

SingSaver’s take

If you and your partner mostly spend on online and/or contactless purchases, you should definitely consider the HSBC Revolution Credit Card. This rewards credit card has a straightforwardGet rewards system— it lets you earn 10X rewards points (4 air miles or 2.5% cashback per S$1) on online purchases and contactless payments. All other spending will be eligible for 1X reward point for every S$1 spent.

The best part? No minimum spend is necessary to start chalking up 10X rewards points on the first S$1,000 spent on such transactions per calendar month! Plus, there’s no annual fee you need to deal with for as long as you have this card in your arsenal.

The free ENTERTAINER with HSBC access is the cherry on top that deserves some spotlight for it lets you enjoy a plethora of 1-for-1 dining, lifestyle and hotel deals at no extra cost.

Predict the Champion. Share S$30,000 in Cash! ⚽

Apply for participating products, predict the next FIFA World Cup 2026 Champion, and win your share of up to S$30,000 cash. Applicable to the first 16 successful applicants at 2 PM and 8 PM daily only. Valid till 28 June 2026. T&Cs apply.

Or, apply and post creative World Cup content on Facebook or Instagram, tag SingSaver, and use #SingSaverWorldCup to win a Golden Ticket, giving you one chance to predict the winning team. Valid till 28 June 2026. T&Cs apply.

SingSaver x HSBC Credit Cards Exclusive Offers

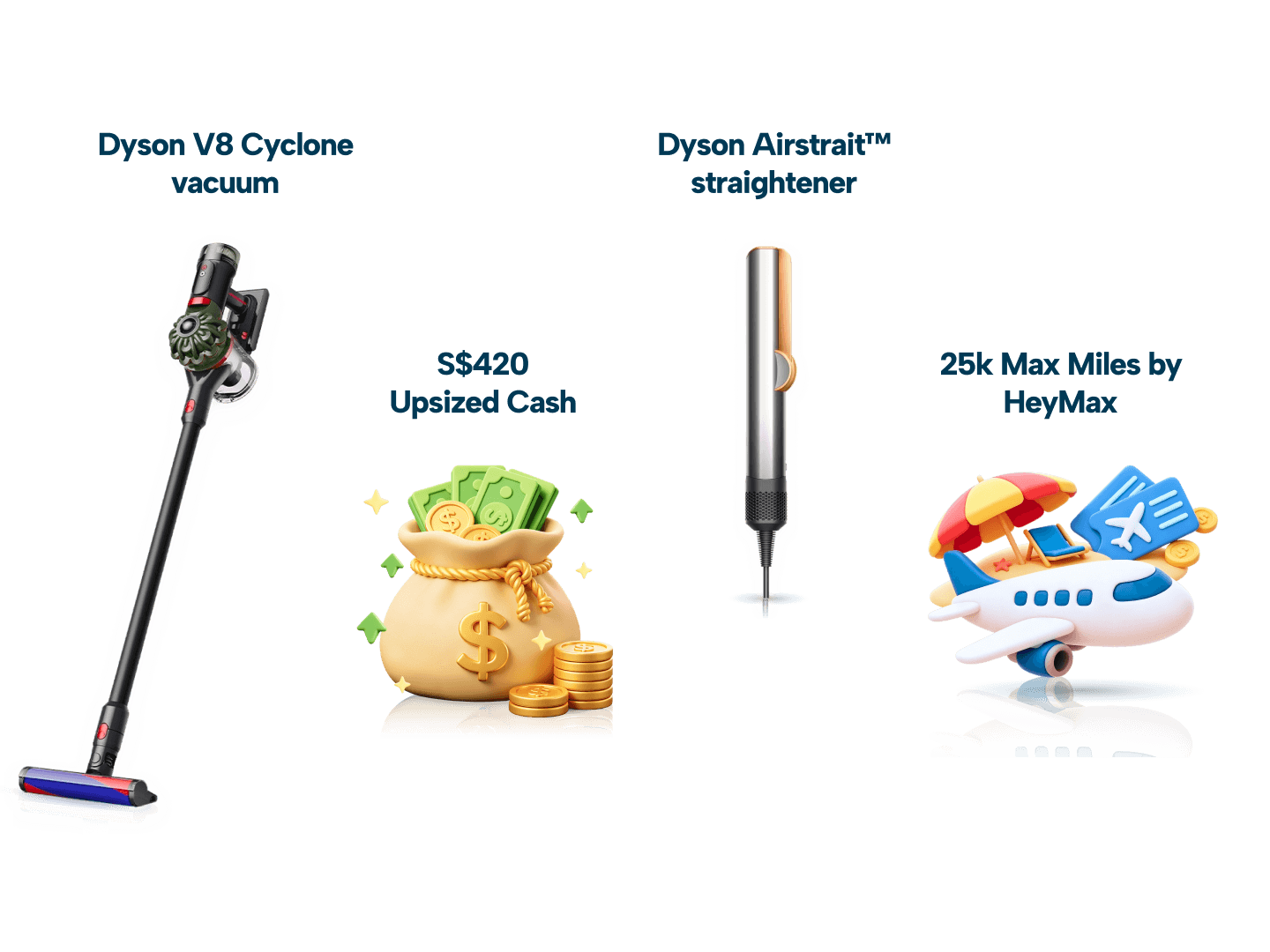

Score S$420 Upsized Cash, Dyson Airstait or V8 Cyclone cordless vacuum, 25,000 Max Miles by HeyMax (worth S$600 in travel value), or a Galaxy Buds4 Pro + S$160 eCapitaVoucher Bundle when you apply for an HSBC Credit Card via SingSaver and fulfil promo requirements. Valid until 30 June 2026. T&Cs apply.

Tips on how to manage a credit card for couples

Whether you're sharing a single card or making use of supplementary cards, here are some tips for effective financial management:

-

Don’t go overboard: Keep things simple by limiting yourself to a handful of shared credit cards. For instance, one credit card (or supplementary card) could be a do-it-all card that you reach for when you’re unsure which one to use. The other shared credit card could be one that rewards you for all online purchases.

-

Agree on repayment responsibilities: Decide how the credit card bill will be paid, whether one person is responsible or if you'll split the cost.

-

Establish clear spending rules: Discuss and agree on how the card will be used, setting spending limits for different categories if needed.

-

Track expenses diligently: Utilise online banking tools or budgeting apps to track monthly spending by both individuals. Even a spreadsheet on Microsoft Excel or Google Sheets can help.

-

Review statements together: Periodically review credit card statements as a couple to identify any discrepancies or areas for improvement.

-

Communicate openly about finances: Have regular discussions about credit card usage and any concerns.

Alternatives to joint credit card accounts

Couples in Singapore may find these alternatives more suitable than traditional joint credit cards:

-

Supplementary credit cards: This is the most common approach, where the primary cardholder can issue additional cards to their partner, children, and other family members. While convenient, remember that the primary cardholder remains liable for all charges, including those made by an authorised user.

-

Joint bank account with debit cards: Opening a joint bank account for shared expenses can be a straightforward way to manage shared finances. However, this option may not be as attractive because debit cards don't offer the credit-building benefits of credit cards.

-

Secured credit cards: These cards require a cash deposit that acts as your credit limit, lessening the risk of incurring an unmanageable debt. This makes it easier for individuals with poor credit or a smaller income to acquire a credit card too. Explore the best secured credit cards in Singapore.

» MORE: Best credit cards for low-income earners in Singapore

Frequently asked questions about joint credit cards

Yes, it is possible to open a joint credit card account in Singapore. However, this is becoming an increasingly rare offering amongst banks and financial institutions. Your other options are to open a joint savings account together or apply for a supplementary credit card for your partner.

You can add someone to your credit card account as an authorised user. This allows them to get their own card and make purchases on the account; however, they are considered a supplementary cardholder instead of a joint account holder. As the primary cardholder, you remain responsible for the entire account.

Instead of a joint credit card account, you may consider having one partner apply for a credit card as the primary holder, and issuing a supplementary card to the other partner. While this offers many similar features to a joint credit card account, only the primary cardholder will be building credit, and he/she is solely responsible for any charges incurred.

Relevant articles

Understanding Additional Cardholders & Supplementary Cards in Singapore

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.