How Much Do You Really Need for Retirement in Singapore?

Updated: 11 Dec 2025

However, determining precisely how much you need for retirement is a complex question with no one-size-fits-all answer. Your retirement needs will vary based on your income, lifestyle preferences, health, and life expectancy. In this guide, we'll explore the key factors to consider when planning for retirement in Singapore and provide practical steps to help you estimate your retirement savings needs.

Here’s how you can figure out how much money to save for retirement:

SingSaver Exclusive Offer

⚽ Make your move this World Cup season. Compare top brokerage deals on SingSaver, then apply to score exclusive upsized rewards this June. Make every play count. 📈🏆 T&Cs apply.

Make the most of every trade. 📊

Set up your account in under 5 minutes, explore your options with ease, and enjoy exclusive rewards as you grow your portfolio. 🪙🏆T&Cs apply.

What is the retirement age in Singapore?

The official retirement age in Singapore is 63. However, with increasing life expectancy and rising healthcare costs, many Singaporeans choose to work beyond this age. It's essential to factor in your anticipated retirement age when planning your finances.

1. How to estimate your retirement income needs in Singapore

Estimating your retirement income needs is a crucial first step in planning for your golden years. While there's no one-size-fits-all answer, a good starting point is to aim for replacing 70-80% of your pre-retirement income to maintain a comfortable lifestyle. However, this is a general guideline, and your specific needs may vary depending on your desired lifestyle, health, and personal circumstances.

To estimate your retirement income needs, begin by meticulously assessing your current spending habits and envisioning your desired retirement lifestyle. This involves two key aspects:

a) Evaluating current expenses

Create a detailed list of your monthly expenses, categorising them into those that will likely remain constant in retirement (e.g., housing, utilities, groceries), those that may decrease (e.g., commuting costs, work-related expenses, childcare), and those that may increase (e.g., healthcare, leisure activities, travel). Be sure to factor in Singapore-specific expenses like CPF Life payouts, healthcare costs (MediSave, Integrated Shield Plans), and housing costs, whether you rent or own your property.

>> Read more: Understanding needs vs. wants when budgeting.

b) Envisioning your retirement lifestyle

Imagine how you want to spend your retirement years. Do you dream of travelling the world, exploring exotic destinations and immersing yourself in different cultures? Or perhaps you envision pursuing hobbies and passions that you've put on hold during your working years, such as photography, painting, or learning a new language.

Each lifestyle choice comes with different financial implications. Travelling the world involves expenses like airfare, accommodation, meals, and activities. Pursuing hobbies may require investing in equipment, lessons, or materials. Spending time with family and friends may involve hosting gatherings, dining out, or gifting. Even a relaxed retirement lifestyle can incur costs for leisure activities, healthcare, and daily living expenses.

>> Read more: Best low-risk investments to store emergency funds.

Combining expenses and lifestyle

Combine your current expense analysis with your envisioned retirement lifestyle to create a comprehensive picture of your retirement income needs. For expenses that are likely to change, delve deeper into the factors driving those changes. For instance, if you anticipate increased travel in retirement, research potential destinations and travel styles to estimate costs accurately. If you plan to downsize your home, factor in the potential proceeds from selling your current property and the costs of purchasing a smaller one. The more granular your analysis, the more accurate your retirement income estimate will be.

Once you have a comprehensive understanding of your estimated monthly expenses in retirement, multiply that figure by 12 to arrive at your annual retirement income needs. Compare this figure to your current income to determine your replacement ratio – the percentage of your pre-retirement income you'll need to replace. This ratio helps you gauge whether your current savings and investment plans are on track to meet your retirement income goals.

>> Read more: 10 best budgeting apps to help you save.

SingSaver x Longbridge Exclusive Offer

Get S$160 Upsized Cash via PayNow, S$170 eCapitaVoucher, or a Stryv AirSleek (worth S$199) when you apply and get approved for a Longbridge SG account, fund a min. of S$2,000 and maintain the assets for 30 days from the day after meeting the deposit criteria. Offer is stackable with Longbridge welcome promo. Valid till 2 August 2026. T&Cs apply.

2. Retirement savings rules of thumb: How much should you set aside?

While personalised calculations are essential for accurate retirement planning, rules of thumb can provide a helpful starting point for estimating your savings needs. As mentioned earlier, the general guideline is to aim for replacing 70-80% of your pre-retirement income. However, this can be adjusted based on your individual circumstances, risk tolerance, and desired lifestyle.

In Singapore, CPF Life payouts provide a base level of retirement income, which can influence your overall savings target. While you'll no longer have to pay payroll taxes in retirement, you'll need to plan for healthcare expenses (MediSave, CareShield Life) and housing needs, especially if you plan to continue renting or have an outstanding mortgage.

Evaluate your current savings rate and how it aligns with your retirement target. If you're saving significantly less than the recommended 10-15% of your income, explore ways to increase your savings, such as reducing discretionary spending, increasing your income through side hustles or investments, or adjusting your retirement timeline.

Remember that different lifestyles require different savings levels. If you envision a more lavish retirement lifestyle with frequent travel and leisure activities, you'll need to save more than someone who plans to live frugally. Conservative savers who prioritise financial security may even aim for a 90% income replacement to provide a buffer against unexpected expenses or financial shocks.

>> Read more: Is CPF Life sufficient for retirement?

3. Calculate your retirement needs with online tools

Retirement calculators can be valuable tools to estimate your future savings needs and required retirement income. Several online calculators are available, including the CPF Retirement Estimator, which helps you project your CPF Life payouts based on your current savings and contributions. Other calculators, such as those endorsed by the Monetary Authority of Singapore (MAS), can provide more comprehensive retirement projections, taking into account various factors like investment returns, inflation, and life expectancy.

When using retirement calculators, it's crucial to understand the underlying assumptions and adjust them based on your individual circumstances and investment strategy. Key assumptions to consider include:

-

Inflation rate: The rate at which the cost of goods and services is expected to rise over time. In Singapore, the average inflation rate is around 2-3%.

-

Expected investment returns: The average rate of return you expect to earn on your investments. A diversified portfolio of stocks and bonds may historically achieve returns of 6-7%, while a more conservative portfolio may yield lower returns.

-

Life expectancy: The average number of years you expect to live in retirement. Consider your family history, health conditions, and lifestyle factors when estimating your life expectancy.

By adjusting these assumptions to reflect your specific situation, you can obtain more accurate and personalised retirement projections.

>> Read more: Does the 4% withdrawal rule still make sense?

4. Review and adjust your retirement plan regularly

Retirement planning is not a one-time event; it's an ongoing process that requires regular reviews and adjustments. As your life circumstances change, so will your retirement needs. Job changes, salary increases, marriage, children, health conditions, and evolving lifestyle goals can all impact your retirement plan.

Key financial factors to consider when reviewing your retirement plan include:

-

Rising healthcare costs: Healthcare expenses tend to increase with age, so it's crucial to factor in potential medical costs and long-term care needs.

-

Changes in CPF policies: Stay informed about any changes in CPF policies or withdrawal ages that may affect your retirement planning.

-

Debt management: Aim to reduce or eliminate any outstanding debts before retirement to minimise financial burdens during your golden years.

Regularly check your financial readiness for retirement, adjusting your savings rate or investment allocations as needed. If you encounter significant life changes or financial challenges, revisit your retirement plan and make necessary adjustments to stay on track towards your goals.

If you find retirement planning overwhelming or need personalised guidance, consider seeking professional help. CPF offers retirement planning services, and there are various robo-advisors and MAS-certified financial planners that can provide an avenue of saving for retirement.

>> Looking to get started? Check out the best annuity plans for retirement in Singapore.

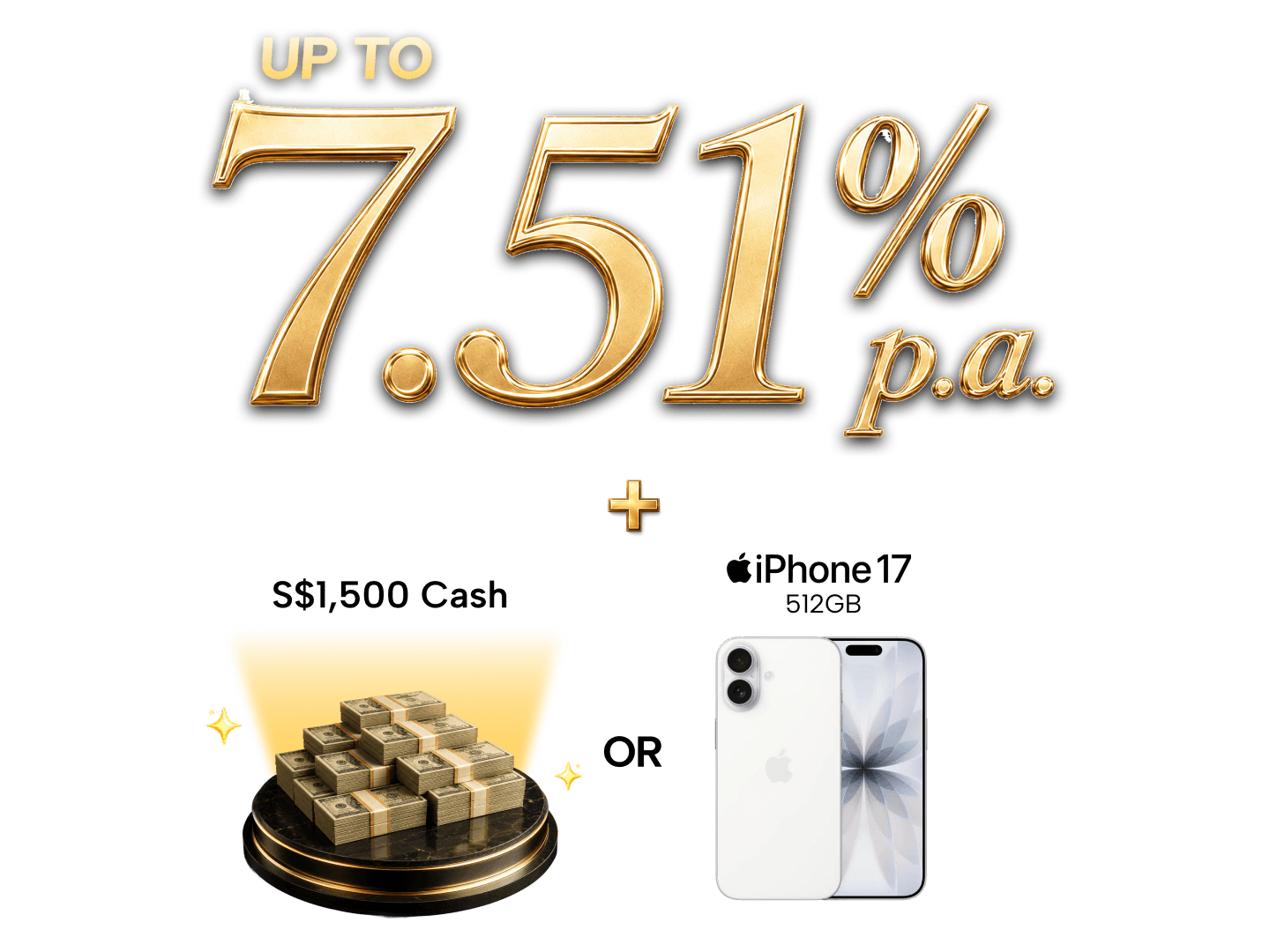

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

4 Tips on Boosting Your CPF Life Savings

Your CPF savings are a cornerstone of your retirement planning in Singapore. Maximising these savings can significantly enhance your financial security and provide a solid foundation for your golden years. Here are four practical strategies to help you boost your CPF Life savings and achieve your retirement goals:

1. Make cash top-ups to your CPF Special Account (SA)

Take advantage of the attractive interest rates offered by your CPF Special Account (SA) to accelerate the growth of your retirement nest egg. By making cash top-ups to your SA, you not only earn higher interest than you would in a regular savings account, but you also enjoy tax relief of up to $7,000 per year. This tax advantage can further enhance your savings and help you reach your retirement goals faster.

2. Transfer Ordinary Account (OA) balance to SA

If you have excess funds in your Ordinary Account (OA) that you no longer need for housing, consider transferring them to your SA to earn higher interest. While your OA funds are primarily meant for housing expenses, any excess funds can be transferred to your SA to benefit from the higher interest rates. However, carefully consider your future housing needs before making this transfer, as you won't be able to use those funds for housing purposes once they're in your SA.

3. Choose not to withdraw at 55

When you reach age 55, you have the option to withdraw a portion of your CPF savings. However, if you don't need the funds immediately, consider leaving them in your CPF account to continue earning interest and compounding over time. The power of compound interest can significantly boost your savings over the long term, especially if you start early and maintain a disciplined approach.

4. Defer your payouts up to age 70

While you can start receiving your CPF Life payouts at age 65, delaying your payouts can significantly increase your monthly income in retirement. For each year you defer, your payouts can grow by up to 7%, resulting in a substantial increase in your retirement income. If you can afford to delay your payouts and don't need the funds immediately, deferring them can be a smart strategy to enhance your financial security in your later years.

By implementing these strategies and consistently contributing to your CPF savings, you can build a robust retirement foundation and enjoy greater financial peace of mind in your golden years.

SingSaver x moomoo Exclusive Offer

Open a Moomoo account and fund a minimum of S$2,000 to get upsized S$150 Cash, S$150 Grab Voucher, Apple AirPods 4 or 9,000 Max Miles by HeyMax (worth S$162). Plus, receive up to S$800 Welcome Rewards fulfilled by Moomoo. Valid till 2 August 2026. T&Cs apply.