Retirement Planning Guide: When Can You Retire in Singapore?

Updated: 11 Dec 2025

Here's a step-by-step approach to retirement planning in Singapore, ensuring a financially secure and fulfilling future.

Planning for a financially secure retirement in Singapore starts now. You don't want to work indefinitely, and relying solely on your CPF might not provide the lifestyle you envision. Traditional retirement strategies, like the 4% withdrawal rule, may also be insufficient in today's economic climate, especially with rising living costs and inflation. So, taking proactive steps in financial planning today and exploring diverse investment options can pave the way for a comfortable and fulfilling retirement.

SingSaver Exclusive Offer

⚽ Make your move this World Cup season. Compare top brokerage deals on SingSaver, then apply to score exclusive upsized rewards this June. Make every play count. 📈🏆 T&Cs apply.

Make the most of every trade. 📊

Set up your account in under 5 minutes, explore your options with ease, and enjoy exclusive rewards as you grow your portfolio. 🪙🏆T&Cs apply.

When can you retire in Singapore?

In Singapore, your retirement timeline is determined by your desired retirement age and achieving financial independence to replace your employment income. The earliest you can tap into your CPF savings is age 55, but it's crucial to understand how this impacts your retirement income.

For example, if you're a Singapore Citizen or Permanent Resident born in 1958 or after, you'll be automatically included in CPF LIFE when you turn 65, provided you have at least S$60,000 in your retirement savings. CPF LIFE offers different plans — Basic, Standard, and Escalating — each with varying monthly payout amounts. Understanding these plans and their impact on your monthly income is crucial for optimising your retirement funds.

While you can make withdrawals from your CPF savings from age 55, starting early may reduce your eventual CPF LIFE payouts. Delaying withdrawals and investing strategically can significantly boost your retirement income. It's also important to consider the rising cost of living and inflation, which can erode your retirement savings over time. Factoring these into your retirement planning ensures your funds last throughout your golden years.

Ultimately, the timing of your retirement is a personal decision. Some retire early (by choice or necessity), while others retire later. But many find it best to transition gradually rather than retire abruptly.

5 steps for retirement planning

Retirement planning involves a series of steps designed to help you achieve financial independence and enjoy your golden years to the fullest. By taking a proactive approach and following these steps, you can build a secure financial foundation for your retirement.

1. When to start retirement planning in Singapore

When should Singaporeans start saving for retirement? The sooner, the better. Time is your greatest asset, allowing you to harness the power of compounding, where your savings and investments grow exponentially. Even small, regular contributions made early in your career can significantly accumulate over time, giving your retirement funds a substantial boost. Remember, CPF contributions begin with your first job, so you're already starting your retirement journey!

However, it's crucial to debunk some common retirement misconceptions. Firstly, relying solely on your CPF might not be enough to support your desired lifestyle in retirement. Supplementing your CPF savings with personal investments and savings is essential. Secondly, the 4% withdrawal rule, a popular guideline for retirement withdrawals, needs to be adjusted based on individual circumstances and economic conditions in Singapore. Don't assume it applies universally — assess your own needs and adjust accordingly.

2. Determine your retirement funding needs

Estimating your retirement expenses in Singapore requires a thoughtful assessment of your current lifestyle and how you envision your retirement years. Consider your desired living standards, including housing, leisure activities, and potential healthcare costs. Will you be travelling extensively? Downsizing your home? Pursuing new hobbies? These factors significantly influence your retirement budget. Don't forget to account for inflation, which can erode your savings over time.

In Singapore, your retirement income typically comes from a combination of CPF LIFE payouts and personal savings or investments. Understanding the different CPF LIFE plans and their estimated monthly payouts is crucial for determining how much you'll need to supplement from other sources. A common guideline is to aim for 70% to 90% of your annual pre-retirement income, but remember that this is just a starting point. Your individual needs and aspirations will eventually determine your retirement funding goals.

3. Balancing short-term needs and long-term retirement goals

Retirement planning is crucial to your overall financial strategy, but it's likely not your only financial goal. Many Singaporeans have other pressing financial priorities, such as paying off housing loans, managing credit card debt, or building an emergency fund. It's essential to balance these immediate needs with your long-term retirement goals.

One approach is to integrate your CPF savings, private savings, and investments into a holistic retirement plan. This involves strategically allocating funds to different priorities, ensuring you're adequately prepared for both short-term needs and long-term financial security. For instance, while consistently contributing to your CPF and building your retirement nest egg, allocate a portion of your income towards an emergency fund and debt repayment. This balanced approach ensures you're not neglecting any critical financial aspects, especially the importance of minimising debt before retirement to maximise your financial stability during your golden years.

4. Select the right retirement plan in Singapore

Building a robust retirement plan involves more than just saving; it's about selecting the right combination of savings and investment vehicles to suit your needs and risk tolerance.

Beyond your CPF contributions, which form the foundation of your retirement savings, consider exploring other options to enhance your retirement income. Topping up your CPF Retirement Sum to the Basic Retirement Sum (BRS), Full Retirement Sum (FRS), or Enhanced Retirement Sum (ERS) levels can provide a stable stream of income during retirement. As of 2025, the ERS level has been adjusted to 4x the BRS level, offering even greater potential for accumulating retirement funds.

Additionally, explore diversifying your investments to supplement your CPF payouts. Fixed deposits offer a low-risk option for preserving capital, while Supplementary Retirement Scheme (SRS) accounts provide tax benefits on contributions and investment returns. For those comfortable with higher risks, consider investing in stocks, ETFs, and REITs for potentially higher long-term growth. Remember, there's no one-size-fits-all solution — the best retirement plan is the one tailored to your specific circumstances and financial goals.

If you want to boost your retirement savings beyond your CPF contributions, consider exploring Supplementary Retirement Scheme (SRS) accounts. These accounts offer tax benefits on your contributions and investment earnings, making them a smart choice for growing your retirement nest egg.

>> Learn more: What is the Supplementary Retirement Scheme (SRS)?

Here are several retirement savings and investment options available in Singapore:

>> Read more: How to increase your CPF LIFE plan payouts for retirement

5. Building your retirement investment portfolio

Constructing a well-diversified investment portfolio is a cornerstone of retirement planning in Singapore. Your investment choices should align with your risk tolerance and the length of your investment horizon.

Generally, a younger investor with a longer time frame can afford to take on more risk for potentially higher returns. As you approach retirement, it's advisable to gradually shift towards a more conservative approach, prioritising capital preservation over aggressive growth. This means diversifying your portfolio across different asset classes, such as:

-

Stocks: Offer potential for high growth but come with higher volatility.

-

Bonds: Generally less volatile than stocks, offering a fixed income stream.

-

Mutual Funds and ETFs: Provide instant diversification and professional management.

-

Real Estate: Can offer stable returns and potential for appreciation.

Regularly review and rebalance your portfolio to ensure it remains aligned with your risk tolerance and retirement goals. Consider seeking advice from a financial advisor for personalised guidance on investment strategies.

>> Read more: Investment strategies for new investors

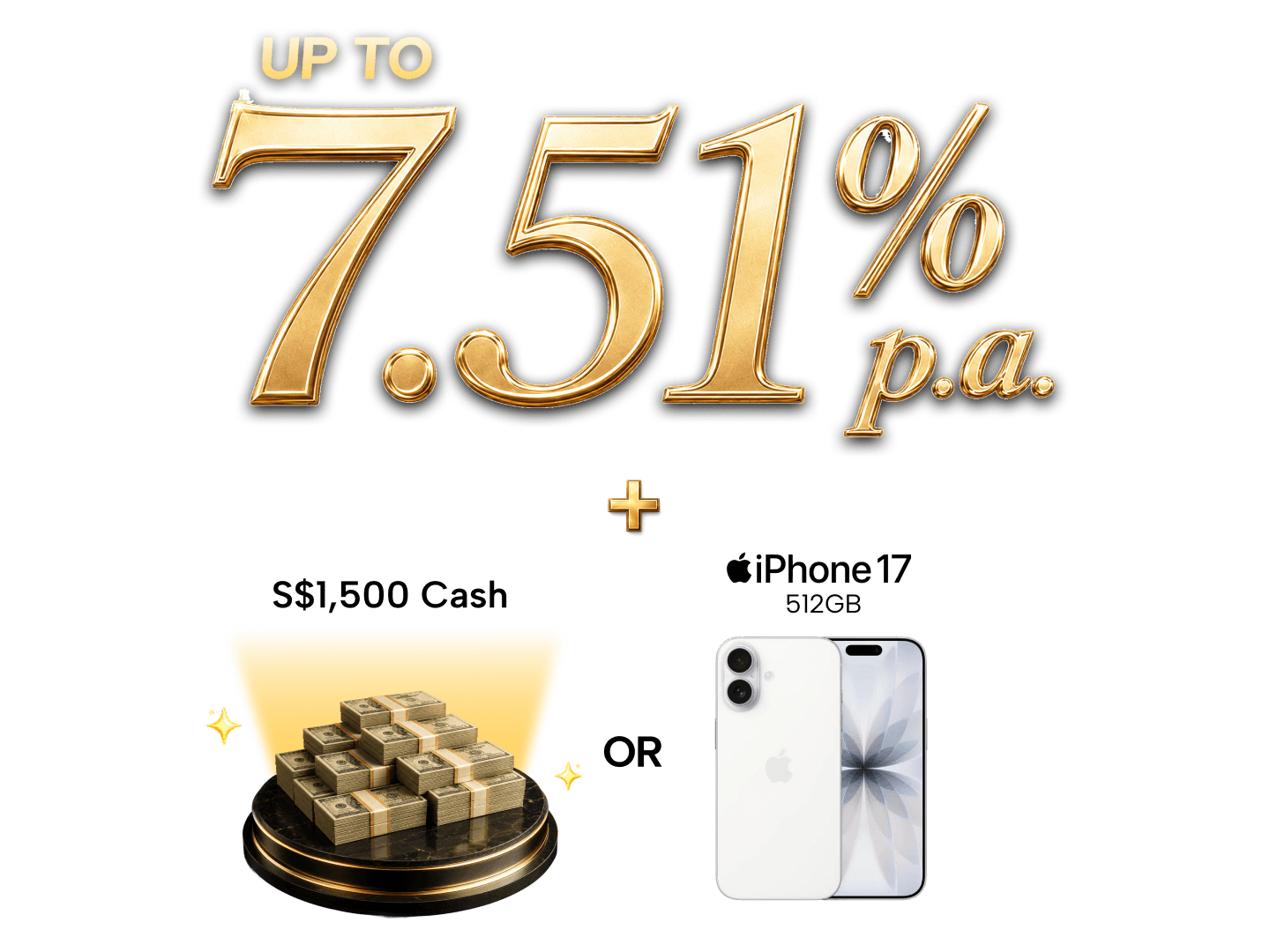

SingSaver x Citigold Exclusive Offer

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

What’s next

Congratulations on taking these necessary steps towards securing your retirement in Singapore! But retirement planning isn't a "set it and forget it" task. Your financial goals and circumstances may change, so it's essential to review and adjust your retirement plan regularly. This includes revisiting your investment strategy, assessing your risk tolerance, and maximising tax relief options available for your CPF contributions and other savings schemes.

Need help navigating your options or figuring out what to do in retirement? SingSaver offers resources and tools to help. Explore our guides, use our calculators, or connect with a financial advisor. Start planning today and embrace the exciting opportunities that await you in your golden years!

Frequently asked questions about retirement planning in Singapore

To estimate your retirement expenses in Singapore, consider factors like housing costs, healthcare needs, lifestyle preferences, and inflation. Use online calculators and budgeting tools to create a realistic estimate.

The best investment options for retirement in Singapore include diversifying your portfolio with a mix of CPF top-ups, fixed deposits, SRS accounts, stocks, ETFs, and REITs. Consider your risk tolerance and investment timeline when making investment decisions.

The optimal timing for withdrawing your CPF LIFE payouts depends on your financial needs and health. Explore different CPF LIFE payout schemes and choose the one that aligns with your retirement goals.