Savings by Age — How Much Should I Have in My 20s, 30s, 40s, 50s

Updated: 4 Jun 2026

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

When it comes to savings, many people ask the golden question — “How much should I have saved by a certain age?” The truth is, there is no universal answer. It depends largely on your financial commitments, life stage, and personal priorities. For example, if you are in your 30s and starting a family or buying a home, your focus may naturally shift towards building up your savings quickly for big-ticket expenses.

On the other hand, someone the same age but without immediate family plans may prefer to channel more funds into investments, prioritising long-term growth over short-term liquidity. Everyone’s lifestyle and financial goals are different, which is why the savings figures in this guide are meant as helpful benchmarks, not rigid targets. How you use them — whether as a goal to aim for or a milestone to celebrate — should ultimately align with your unique situation and habits.

How much are Singaporeans saving on average?

The 1x Annual Income Rule

A common rule of thumb is to have one time your annual salary saved by age 35.

As of early 2026, the median monthly income for a resident in the 35–39 age group is approximately S$7,350 (inclusive of employer CPF). This means a median earner should aim for a total wealth pot (Cash + CPF) of roughly S$88,200.

If you are a Professional, Manager, or Executive (PME), this benchmark may be higher. With core inflation projected by MAS to average 1.5%–2.5% this year, your "target" needs to be adjusted upward annually to maintain the same purchasing power.

Emergency Fund: 6 Months of Expenses

In 2026, the "standard" emergency fund needs a top-up.

Due to the cumulative effect of the 9% GST and recent increases in transport and utility costs, the monthly "burn rate" for a 35-year-old is higher than in previous years.

-

Recommendation: Calculate your average monthly outflow (including your mortgage) and multiply by six. If your monthly expenses are S$4,000, your baseline liquidity should be **S$24,000**. Keep this in high-yield accounts where rates for flagship accounts (like OCBC 360 or UOB One) currently hover between 4.0% and 4.5% p.a. for the first S$100,000.

CPF Savings: The 2026 Milestone

Find the bank account for your needs

Compare savings, current, and multi-currency accounts to make your money work smarter.

Recommended savings by age in Singapore

Income and financial obligations vary greatly depending on age. Young workers starting out in their careers typically earn less and may find saving a challenge, while mid-career individuals may be able to save more. In later years, expenses may stabilise or even decline, but retirement savings become a higher priority.

| Age group | Median monthly salary (2026 Est.)* | 20% savings per month (Recommended minimum) | 34.9% savings per month (2026 Average rate)** |

| 15 – 19 | $1,650 | $330 | $576 |

| 20 – 24 | $3,100 | $620 | $1,082 |

| 25 – 29 | $4,850 | $970 | $1,693 |

| 30 – 34 | $6,100 | $1,220 | $2,129 |

| 35 – 39 | $7,350 | $1,470 | $2,565 |

| 40 – 44 | $7,700 | $1,540 | $2,687 |

| 45 – 49 | $7,800 | $1,560 | $2,722 |

| 50 – 54 | $6,200 | $1,240 | $2,164 |

| 55 – 59 | $4,800 | $960 | $1,675 |

| 60 & over | $3,500 | $700 | $1,221 |

*Includes Employer CPF contributions. Figures are based on 2025 year-end data and 2026 wage projections.

**Based on the Dec 2025 seasonally adjusted Personal Saving Rate of 34.9% reported by the Department of Statistics (DOS).

Key Changes to Note for 2026:

-

Salary Growth: Nominal wages for the 35–49 age bracket have seen the strongest growth, crossing the S$7,000 mark as the labor market tightened in late 2025.

-

The S$8,000 CPF Ceiling: Effective January 1, 2026, the CPF OW ceiling is now S$8,000. For the 35–49 age groups, this means a higher percentage of their "Median Salary" is officially captured as savings (CPF), even if their liquid "take-home" cash feels tighter.

-

Average Savings Rate: The national personal saving rate has stabilized at approximately 34.9% in early 2026, slightly lower than the post-pandemic highs but significantly higher than the 20% "minimum" often cited.

-

Cost of Living Adjustment: While the 20% savings rule remains a benchmark, most financial advisors in 2026 suggest that due to core inflation, a 35-year-old should prioritize filling their Basic Healthcare Sum (S$79,000) and Full Retirement Sum (S$220,400) as their primary "savings" anchors.

>> MORE: Typical minimum balances to open savings accounts in Singapore

How much savings should I have in my 20s?

Your 20s in 2026 are the most critical years for navigating a high-cost environment while leveraging a revamped CPF system. While the immediate pressure of inflation is present, laying a financial foundation now is more impactful than ever due to the higher interest rate floors maintained through the mid-2020s.

In Singapore, the median monthly salary for those aged 20 to 24 has risen to approximately $3,100 in 2026, while those in the 25 to 29 bracket earn a median of $4,850. Following the 50/30/20 budgeting rule—where 20% of your income is earmarked for savings—you should aim to set aside between $620 and $970 per month. If you begin saving consistently at age 22, by the time you turn 25, you could realistically amass nearly $23,000. By age 30, with steady career progression and the higher CPF contribution ceilings now in effect, this total could exceed $65,000 in combined liquid cash and CPF Ordinary Account savings.

During this decade, your primary objective is to build a "resilience buffer." Your emergency fund remains the top priority. Given the increased cost of utilities, transport, and food in 2026, you should calculate your fund based on current living expenses, aiming for a six-month safety net. This fund should be parked in a high-yield savings account or Singapore Savings Bonds (SSB) to ensure liquidity while still hedging against inflation. Having this cushion prevents you from high-interest credit trap—a risk that has intensified as borrowing costs remain elevated compared to the early 2020s.

Beyond basic savings, 2026 is the year to master automated investing. With the statutory retirement age rising to 64 on July 1, 2026, your investment horizon is long, making compound interest your greatest ally. Even modest, recurring contributions into low-cost, diversified global index funds can grow exponentially.

At the same time, be wary of "digital lifestyle inflation." In an era of seamless social-commerce and subscription-heavy lifestyles, it is easy to let small, recurring expenses erode your margin. By living intentionally and keeping your fixed costs low even as your salary hits the new median benchmarks, you ensure that your 30s are spent building wealth rather than playing catch-up.

During this period, your financial goals should focus on establishing a firm foundation. An emergency fund is a top priority. Ideally, this should cover at least three to six months of essential expenses, acting as a safety net in case of unexpected job loss or medical emergencies. This fund offers peace of mind and protects you from dipping into your long-term savings or resorting to debt when challenges arise. For many young Singaporeans who may still be adjusting to working life, this step alone can provide greater financial security.

Beyond saving, investing should also be on your radar. Starting early allows you to take advantage of compound interest, where returns earned are reinvested to generate even more returns. Even small investments made in your 20s can grow exponentially over the decades. At the same time, it is important to avoid lifestyle inflation. As your income rises, it can be tempting to upgrade your spending on things like dining, gadgets, and travel. While there’s nothing wrong with treating yourself occasionally, living below your means and sticking to your savings targets will put you in a much stronger position later on.

>> MORE: Best credit cards for young adults in Singapore (2025)

SingSaver x Citigold Exclusive Offer

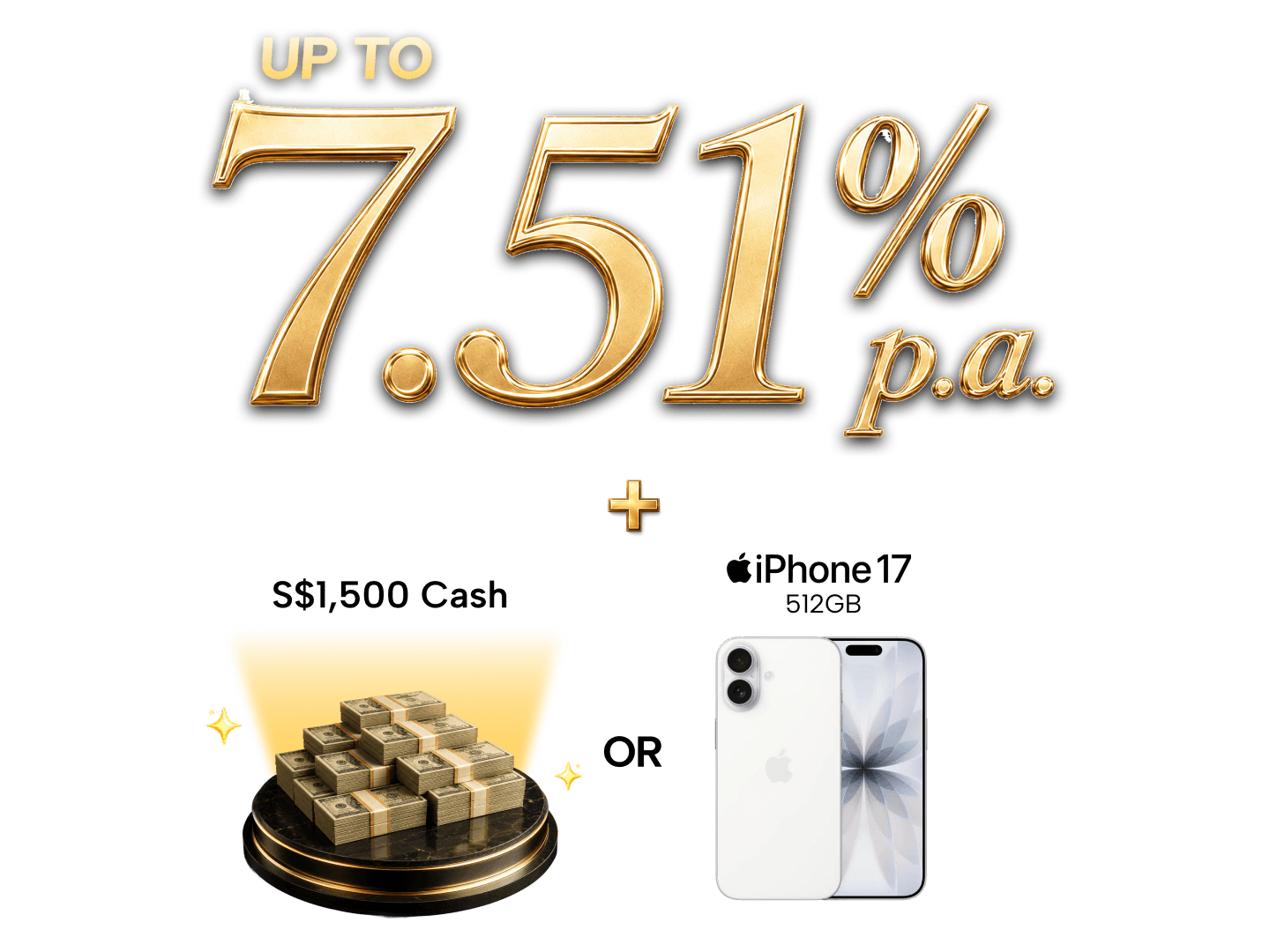

Get up to S$1,500 upsized Cash via PayNow or an Apple iPhone 17 512GB when you successfully apply for a Citigold account and make a minimum S$350,000 deposit within 3 months of account opening. Valid till 2 August 2026. T&Cs apply.

Elevate how you grow your wealth 💎

Enjoy up to 7.51% p.a. interest when you join Citigold and open a Wealth First account. Plus, unlock up to 3.01% p.a. on your savings—more returns and even more value back to you. Plus, enjoy a dedicated relationship manager and tailored wealth solutions. Valid till 2 August 2026. T&Cs apply.

How much savings should I have in my 30s?

In 2026, median salaries rise sharply as professionals move into managerial roles. For those aged 30 to 34, the median monthly salary is approximately $6,100, while for those aged 35 to 39, it reaches $7,350 (inclusive of employer CPF). Using the 20% savings rule, you should be aiming to set aside $1,220 to $1,470 per month.

By age 35, a disciplined saver who started in their 20s should ideally have a total net worth (Cash + Investments + CPF) of at least $100,000 to $150,000. By the time you reach 40, this figure should realistically cross the $250,000 mark, fueled by the higher $8,000 CPF Ordinary Wage ceiling and compound growth.

In this decade, your strategy must evolve beyond a simple savings rate. You are likely facing the "Triple Threat" of 2026: higher mortgage servicing costs, childcare/education inflation, and the "Sandwich Generation" responsibility of supporting aging parents.

-

Maximize the CPF Shield: With the Basic Healthcare Sum (BHS) at $79,000 for 2026, your first priority should be capping this. Once capped, your mandatory MediSave contributions will overflow into your Special Account, earning a stable 4% p.a. risk-free—a vital tool as market volatility remains a theme in 2026.

-

Invest with Intention: At 35, you have nearly 30 years until retirement. Diversifying into global equities or REITs is essential to beat the 2.5% inflation rate. If you have hit your 6-month emergency fund milestone, consider the "Invest the Rest" approach.

-

Audit Your "Life Milestones": 2026 is a year of moderation. With Category A and B COEs consistently high, many 30-somethings are opting for private-hire or public transport to funnel that "car money" (approx. $2,500/month) into their mortgage or kids' education funds.

Ultimately, your 30s are about velocity. While 20% is the minimum, those aiming for financial independence in the current 2026 climate should strive for a 30% to 35% savings rate—utilizing tax-efficient vehicles like the Supplementary Retirement Scheme (SRS) to keep more of their hard-earned salary.

How much savings should I have in my 40s?

By your 40s, you are likely entering your peak earning years in a more complex economy. As of April 2026, median salaries for Singaporeans in this age group have shifted upward to reflect a tightening labor market. Those aged 40 to 44 now earn a median of approximately $7,700 monthly, while those aged 45 to 49 earn around $7,800 (inclusive of employer CPF).

Applying the 20% savings rule, you should be setting aside roughly $1,540 to $1,560 each month. Over a five-year stretch, this adds another $93,000 to your nest egg. If you have been disciplined throughout your 20s and 30s, it is now realistic—and necessary—to target a total net worth (Cash, Investments, and CPF) of $350,000 to $450,000 by your late 40s to keep pace with the 2026 cost of living.

Go exclusive with priority banking

Take your wealth management to the next level with a priority banking account

How much savings should I have in my 50s?

As you enter your 50s in 2026, the finish line for retirement planning is in sight. However, the goalposts have moved: on July 1, 2026, the statutory retirement age officially rises to 64, and the re-employment age to 69. This gives you a slightly longer runway to accumulate wealth, but it also necessitates a larger nest egg to combat the higher cost of living.

Median salaries in 2026 have remained resilient for this demographic. Those aged 50 to 54 earn a median of approximately $6,200, while those aged 55 to 59 earn around $4,800 (inclusive of employer CPF). Saving 20% of this income translates to $960 to $1,240 monthly. By this stage, assuming steady contributions since your 30s, your cumulative savings target (Cash + Investments + CPF) should ideally be between $500,000 and $650,000 to maintain a comfortable middle-class lifestyle in 2026.

Healthcare and Legacy Planning are no longer optional in your 50s. With the 2026 updates to CareShield Life, which saw increased premiums and higher payouts, you should ensure your long-term care insurance is adequate. Reviewing your MediShield Life coverage against current private hospital costs is also vital.

Finally, 2026 is the year to solidify your estate plan. Ensure your CPF Nominations are up to date and your Lasting Power of Attorney (LPA) is settled. Preserving your capital becomes the priority; while you shouldn't exit the market entirely, reducing exposure to volatile "growth" stocks in favor of capital preservation will safeguard the decades of hard work you've put in.

>> MORE: Retirement planning guide

How much should I save for retirement at 60

Reaching your 60s is a major financial milestone, but in 2026, it is also a time of transition. With the statutory retirement age rising to 64 and the re-employment age to 69 on July 1, 2026, many 60-year-olds are choosing—or are now legally empowered—to extend their peak earning years. This extra window is a golden opportunity to bridge any remaining gaps in your nest egg.

By now, you should have a precise estimate of your monthly requirements. Recent 2026 data indicates that a "Basic" retirement lifestyle for a single senior in Singapore now costs approximately $2,700 per month, accounting for the cumulative effects of inflation on food and utilities over the last few years. If you envision a "Comfortable" lifestyle including semi-regular travel and dining, you should budget for closer to $3,400 to $4,500 per month.

Your desired retirement lifestyle is the primary driver of your savings target. While a basic plan covers essentials like housing, transport, and subsidized healthcare, an "Aspirational" retirement in 2026 can exceed $6,100 per month. Projecting these costs is vital: even with inflation stabilizing at 1.5%–2.5%, medical cost inflation is projected to be much higher, meaning today’s estimates must include a significant healthcare buffer to remain realistic over a 25-year retirement.

In terms of income, CPF LIFE payouts will form the backbone of your strategy. As of 2026, the Enhanced Retirement Sum (ERS) has been raised to $440,800.

Let your money work for you while you rest with a good robo-advisor

Compare automated investment options and find the one that suits your retirement needs.

Savings principles for Singaporeans of all ages

Start saving early

Regardless of whether you are just starting your career or counting down the years to retirement, one principle holds true — the earlier you begin saving, the more options and security you will have later on. Time is one of your biggest allies when it comes to building wealth. Thanks to the power of compounding, every dollar you save and invest has the potential to generate returns, which can in turn be reinvested to create even greater gains. Starting early means you can contribute smaller amounts consistently and still reach meaningful goals without needing to play catch-up later in life.

Adapt savings strategy to changing life stages and circumstances

As you move through life’s stages, your priorities and financial needs will change — and your savings approach should evolve accordingly. In your 20s, the focus may be on building an emergency fund and starting small investments. As you enter your 30s and 40s, attention naturally shifts towards growing your wealth, preparing for family commitments, and planning for long-term goals like home ownership and children’s education. By your 50s and 60s, preserving wealth, maximising retirement income, and estate planning take centre stage. Adapting your strategy to meet these changing demands ensures your financial plan stays relevant and achievable.

Don't give in to lifestyle inflation

As your income increases, it's tempting to elevate your spending. Avoid falling into the common trap of lifestyle inflation. As salaries rise, it can be tempting to upgrade your home, car, and holidays in step with your income. While it is normal to enjoy the fruits of your labour, consistently increasing your spending can erode your ability to save and invest for the future. Practising mindful spending, automating savings, and regularly reviewing your financial goals can help you stay disciplined. Ultimately, successful saving is not about depriving yourself — it is about ensuring that you are prepared for whatever life brings, while still having the freedom to enjoy today.

Focus on personal financial goals for a secure financial future

While benchmarks provide guidance, personalising your savings strategy to fit your unique circumstances is paramount. Regularly review your financial plan, stay informed, and make adjustments as needed to ensure long-term financial security.

Frequently asked questions about how much savings you should have by age

As a general rule, aim to save at least 20% of your take-home pay each month. However, if your expenses are lower or your salary is higher, saving more — ideally closer to Singapore’s average personal savings rate of 31.5% — can help you reach your financial goals faster.

Not at all. While starting early gives you a head start, it is never too late to begin saving. In your 30s and 40s, focus on increasing your savings rate, cutting unnecessary expenses, and investing wisely to catch up. Every dollar saved still makes a difference, especially when combined with consistent effort and good financial habits.

There is no one-size-fits-all answer, as your savings target depends on the lifestyle you wish to maintain. Based on the 2023 Household Expenditure Survey, a retiree household spends around $2,349 monthly on average. Assuming no other income, this would require roughly $30,000 annually or $600,000 to fund 20 years of retirement. However, CPF LIFE payouts, investments, and other income sources will likely reduce the amount of cash savings you need.

Yes, CPF balances should be included in your overall savings plan, especially your Special Account and Retirement Account balances, which are specifically designed to fund your retirement needs. However, keep in mind CPF funds are typically locked until eligible withdrawal ages, so it is important to have liquid savings as well.

Both saving and investing play important roles throughout your life. In your younger years, you may want to focus more on growing your investments to take advantage of compound interest. As you approach your 50s and 60s, preserving your capital becomes a priority. This means gradually shifting towards lower-risk investments while maintaining adequate cash savings for flexibility and emergencies.

Park your money in a savings account and watch it grow

Explore interest rates, features, and fees to find the right savings account for your goals.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.