UOB EVOL Card

S$0

Updated: 9 Jun 2026

Find out all the ways you are unconsciously racking up debt and how to pay them off.

Team

Student loans, mortgages and business loans — Everyone has fallen into debt at some point in their lives.

While the aforementioned debts are pretty obvious, there are some debts you may have incurred which are quietly eating away at your bank balance without you realising it.

Here are four ways you are racking up debt without knowing it, and the strategies that you can use to quickly and efficiently manage your debt in Singapore.

The folks at SingSaver love credit cards. We genuinely do. They're great because they are 1) convenient, 2) more secure than using cash/debit cards, and 3) you can earn rewards points, cashback, or miles at the same time. Besides that, credit cards are also amazing for building a healthy credit score so that you can secure a better bank loan in the future for big purchases such as an HDB flat or private property—if you pay your bills in full every month, that is.

However, should you only choose to pay the minimum sum of S$50 or 3% of your outstanding balance (whichever is higher) each month, you're on a downward spiral of high-interest credit card debt. Unfortunately, banks aren't generous enough to give you a free pass. Due to the shifting economic landscape and rising global interest benchmarks, major local and international retail banks in Singapore (such as DBS, OCBC, UOB, and Citi) have raised their standard interest rates. Most cards now charge a prevailing interest rate ranging from 27.8% to 27.9% per annum, which compounds daily on your unpaid statement balance.

Furthermore, if you miss that minimum payment deadline entirely, many financial institutions impose a penalty tier—bumping your interest rate up to 30.8% per annum until your account returns to good standing.

Oh, did we also mention that there's a late payment fee if you don't pay before the due date? Late payment fees across major Singapore issuers hover around S$100 per missed cycle. This is one of the absolute worst ways to spend your hard-earned money and can trigger rapid, unchecked debt accumulation, especially if you juggle multiple active credit cards.

Pay your credit card bill. In full. Every. Single. Month. Set up a GIRO automatic deduction linked to your primary savings account, place a recurring reminder on your phone, or get a close friend to hold you accountable. If you are already facing snowballing balances, learning how to manage debt effectively begins with halting new card expenditures immediately and tackling your highest-interest statements first. Credit card debt is an expensive burden, and you'll want to make sure you protect your financial health by avoiding it at all costs.

Buy Now Pay Later (BNPL) services like Grab PayLater and Atome—which divide consumer purchases into three or four interest-free instalments—are highly popular. They can be a strategic tool, but typically only for financially disciplined consumers who are tracking specific rewards or optimizing their credit card spending caps.

For folks who view BNPL services as a type of casual, friction-free "money lending" utility to purchase items they cannot otherwise afford, you have walked into one of the sneakiest debt traps to avoid. Should you miss a scheduled repayment, significant consequences await.

To safeguard consumers, the industry operates under the official BNPL Code of Conduct, which enforces strict consumer protection guidelines across all accredited providers in Singapore. If you miss a payment, your account is automatically and instantly frozen across the provider's network to prevent further spending. Furthermore, late payment fees are capped and regulated, but they still add up quickly. For instance, Atome charges an admin/late fee of S$15 the day after a payment is missed, and an additional S$15 if it remains unpaid after another seven days.

You will ultimately have to master self-control and establish a realistic personal budget. A golden rule to live by is: if you cannot afford to pay for the item in full with cash today, do not buy it. If you utilize BNPL services simply to smooth out monthly cash flow while keeping funds in high-yield savings accounts, treat those instalments as immediate debits. Map out the payment timelines on your digital calendar and ensure you maintain a sufficient cash buffer to meet the deductions automatically.

"When you're broke, you realize even the smallest luxuries cost you a pretty penny. Some of the very common money sinkers are subscription services such as Spotify and Netflix. It's important to go through your credit card statements to see what you're actually paying for, and if you're even still using the service. If not, cancel them."

— Nat Ho

Digital subscriptions represent a modern, hidden form of financial leakage. Because these payments are automated via digital tokens or card recurring billings, they easily slip under the radar, resulting in passive monthly expenses for platforms you rarely log into.

Keep close tabs on what you have subscribed to, and perform a monthly audit on your banking statements. Pay special attention to hidden ecosystem memberships that you might have signed up for via a "free trial" and forgot to cancel—such as ride-hailing premium tiers, grocery delivery passes, app store memberships, or car-sharing platform memberships.

To prevent this from leading to financial strain, utilize free and fully legal local entertainment alternatives. For instance, you can access thousands of movies, e-books, and audiobooks for free via the National Library Board (NLB) mobile app, or stream local dramas and current events completely free on Mediacorp’s mewatch platform. Adopting a lifestyle rotation policy—where you subscribe to only one entertainment service at a time and cancel it before picking up another—is a practical strategy for anyone looking at how to get out of debt by trimming recurring overheads.

Apply for participating products, predict the next FIFA World Cup 2026 Champion, and win your share of up to S$30,000 cash. Applicable to the first 16 successful applicants at 2 PM and 8 PM daily only. Valid till 28 June 2026. T&Cs apply.

Or, apply and post creative World Cup content on Facebook or Instagram, tag SingSaver, and use #SingSaverWorldCup to win a Golden Ticket, giving you one chance to predict the winning team. Valid till 28 June 2026. T&Cs apply.

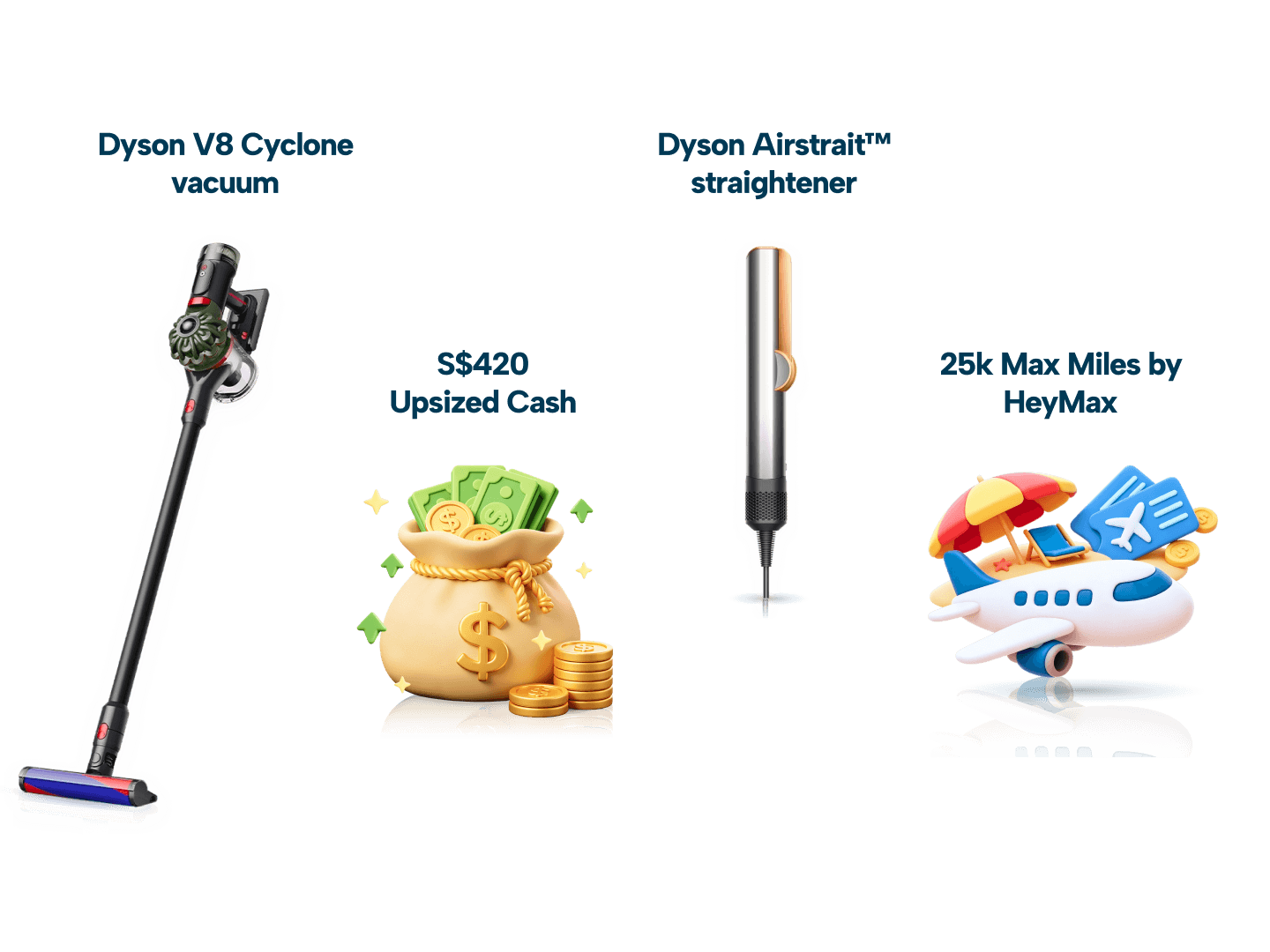

Score S$420 Upsized Cash, Dyson Airstait or V8 Cyclone cordless vacuum, 25,000 Max Miles by HeyMax (worth S$600 in travel value), or a Galaxy Buds4 Pro + S$160 eCapitaVoucher Bundle when you apply for an HSBC Credit Card via SingSaver and fulfil promo requirements. Valid until 30 June 2026. T&Cs apply.

When monthly expenses surpass earnings, it can be tempting to turn to fast cash facilities, such as credit card cash advances, overdraft lines, or short-term personal loans, to bridge the gap. Relying on additional borrowing to pay off existing consumer lines is a dangerous cycle that accelerates your overall indebtedness.

Unsecured personal lines of credit often carry effective interest rates (EIR) exceeding 20% p.a., while credit card cash advances frequently incur an immediate upfront transaction fee (typically 6% to 8% of the withdrawn amount or S$15, whichever is higher) alongside prevailing interest rates that run close to 28% p.a. from the exact day of withdrawal. Turning to these options without a structured repayment strategy is a primary driver of compounding financial distress.

If you find yourself using one loan to cover another, it is time to pivot toward a formal, structured relief framework rather than adding more liabilities. Singapore offers multiple regulatory and non-profit pathways designed to help citizens regain control of their finances.

Look into a formal debt management plan or check your eligibility for a Debt Consolidation Plan (DCP) through participating retail banks if your total outstanding unsecured debt across all financial institutions exceeds 12 times your monthly income. Alternatively, you can reach out to Credit Counselling Singapore (CCS), a registered social service agency that provides targeted financial counseling, public educational workshops, and subsidized repayment programs to help individuals systematically settle their liabilities and achieve long-term financial freedom.

| Financial Product / Activity | Common Debt Risks & Pitfalls | Smart Financial Habits for Today | Source / Authority |

| Credit Cards | Paying only the minimum sum; incurring interest rates of 27.8% to 30.8% p.a. compounding daily. | Always pay statement balances in full via automated GIRO deductions to build a strong credit history. | DBS, UOB, OCBC Card Terms; Credit Bureau Singapore |

| Buy Now Pay Later (BNPL) | Missing payments; incurring structured late fees (e.g., Atome's S$15 fee); instant account suspension. | Treat BNPL as a cash expense. Strict account freezing is mandated under the official BNPL Code of Conduct. | Monetary Authority of Singapore (MAS); Singapore FinTech Association |

| Streaming & Subscriptions | Unused auto-renewals; trial periods that roll over silently into premium charges. | Audit card statements monthly. Utilize free, fully legal local options like the NLB app or Mediacorp's mewatch. | National Library Board; IMDA Guidelines |

| Emergency Funding & Debt Relief | Taking high-interest cash advances (charging ~28% p.a. + transactional fees) to clear older debts. | Avoid multi-borrowing. Speak to Credit Counselling Singapore (CCS) or explore a Debt Consolidation Plan (DCP) if debt exceeds 12x monthly income. | Association of Banks in Singapore (ABS); Credit Counselling Singapore |

Accumulating debt in Singapore often happens quietly through small, overlooked habits rather than massive, one-time splurges. By relying on credit card minimum payments (which can skyrocket interest rates up to 30.8% p.a.), treating Buy Now Pay Later (BNPL) instalments as free money, letting unused digital subscriptions auto-renew, or juggling high-interest lines of credit, you can easily fall into a compounding financial cycle. Breaking these habits requires a shift toward automated full repayments, disciplined budgeting under the official BNPL Code of Conduct, and utilizing free community resources like Credit Counselling Singapore (CCS).

Don't let hidden leaks derail your savings goals. If you are struggling with mounting balances, the most critical step you can take today is to establish a structured roadmap to financial freedom. Discover actionable strategies, compare structured repayment options, and learn exactly how to manage debt effectively by checking out our Comprehensive Guide to Debt Consolidation Plans in Singapore.

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.