Whether you’re a Luxe Shopper, Savvy Mom, or Culture Vulture, here are the best women's credit cards that give you the best bang for your buck.

When it comes to credit cards, Singaporean women are spoilt for choice. Whether your interests lie in designer fashion, theatre and musicals, fitness, dining or more practical activities like grocery shopping, there is a credit card that rewards you for it – which makes it all the more confusing to choose the right one.

We break down the best women's credit cards for the different types of Singaporean women.

Table of contents

- Best for deluxe shopping: UOB Lady's Card

- Best for savvy online shoppers: Citi Rewards Card

- Best for international shopaholics: DBS Woman's Card

- Best for culture vultures: OCBC Arts Platinum Card

Best Women's Credit Cards in Singapore 2024

|

|

|

|

|

| Best For | Luxe Shopper | Savvy Mom | International Shopaholic | Culture Vulture |

| Min. Annual Income | Singaporeans/PR: S$30,000 Foreigners: S$80,000 |

Singaporeans/PR: S$30,000 Foreigner: S$42,000 |

Singaporeans/PR: S$30,000 Foreigner: S$45,000 |

Singaporeans/PR: S$30,000 Foreigner: S$45,000 |

| Benefits | 15X UNI$ per S$5 spend (6 miles) on Beauty and wellness, Fashion, Dining, Family, Travel, Transport or Entertainment 1X UNI$ per S$5 spend (0.4 miles) on other purchases |

10X Rewards (4 miles) per S$1 spent on online and shopping purchases (including online groceries, online food delivery) 1X Reward (0.4 miles) on other purchases |

5X Rewards per S$5 spend (2 miles) online 1X Reward per S$5 (0.4 miles) spent on other purchases |

15 OCBC$ per S$5 spent on SISTIC purchases Priority show bookings |

| Annual Fee | S$196.20 (1st-year waiver) |

S$196.40 (1st-year waiver) |

S$163.50 (1st-year waiver) |

S$163.50 (Two-year waiver) |

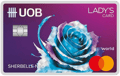

For the Luxe Shopper: UOB Lady’s Card

🆚SingSaver's Cashback vs Miles Campaign (Round 1) 🆚: Are you Team Cashback or Team AirMiles?

Receive rewards of up to S$370 Voucher or up to 34K Miles when you sign up for any participating Cashback or Miles Credit Card, respectively, within the promo period. The team with the most applications wins the rewards! Promo runs from 8 May, 5pm - 21 May 2024. T&Cs apply.

Plus, get up to 31x chances to win a Pair of RETURN Business Class Tickets to Switzerland, Zurich (worth 320K Max Miles) in the Grand Lucky Draw when you successfully apply for participating products. Promo runs from 8 May, 5pm - 21 May 2024. T&Cs apply.

UOB Lady's Card Welcome Gift: Enjoy the following rewards when you sign up for a UOB Lady's Card (Team AirMiles):

Get a chance to enjoy an exquisite dining experience for two at Michelin-starred restaurants (worth S$900) when you are one of the first 150 applicants every month during the promo period and make a min. spend of S$1,500 per month for 2 consecutive months from card approval date. Valid till 30 June 2024. T&Cs apply.

Men won’t get why women would need a credit card specifically for them, but UOB certainly does. The iconic UOB Lady’s Card is a comely addition to your wallet – this special edition design is by homegrown fashion designer Priscilla Shunmugam. The perks and rewards are a ladykiller.

Why you’ll love it:

Perhaps a more suitable question is: Why wouldn’t you? Earn 10X UNI$ per $S5 or 4 miles per S$1 (mpd) spent in one preferred category per quarter and 1X UNI$ per S$5 (0.4 mpd) on all other purchases.

How many times have you bought yourself an early birthday or Christmas present? While we advocate prudence with your finances, it’s ok to treat yourself on special occasions.

When you put a big-ticket shoe or bag purchase (over S$500) on UOB Lady’s 0% Interest LuxePay plan, it splits the cost over 6 or 12 months at no extra interest. Isn’t that great? And the best part – MasterCard e-Commerce Protection on all online purchases.

[Update!] And if you want to go the extra mile and bump your bonus miles earn rate up to 25X UNI$ per S$5 (10 mpd) spend? Simply open a UOB Lady's Savings Account, pair your card with it, and voila! That's an easy 10 mpd for every eligible preferred category transaction!

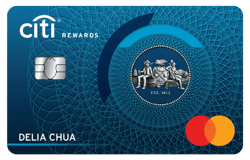

For the Savvy Mom: Citi Rewards Card

Whether you prefer to de-stress at the mall or online, the Citi Rewards Card helps you save money and earn flexible rewards points at the same time.

Why you’ll love it:

As its name suggests, this card offers you rewards galore when you shop for you and your family's new-season clothes, bags and shoes at department stores or online. Think 10X Rewards Points (4 mpd) that help you chalk up points quicker than a blink of an eye!

Citi Rewards Card is also great for all other online purchases — you can expect to snag 4 mpd when you order groceries and food deliveries online or book rides with Grab, Gojek and more.

Also, you can get exclusive discounts with your Citi Rewards Card and are entitled to enjoy other Citi privileges ranging from travel, petrol to gourmet deals.

🆚SingSaver's Cashback vs Miles Campaign (Round 1) 🆚: Are you Team Cashback or Team AirMiles?

Receive rewards of up to S$370 Voucher or up to 34K Miles when you sign up for any participating Cashback or Miles Credit Card, respectively, within the promo period. The team with the most applications wins the rewards! Promo runs from 8 May, 5pm - 21 May 2024. T&Cs apply.

Plus, get up to 31x chances to win a Pair of RETURN Business Class Tickets to Switzerland, Zurich (worth 320K Max Miles) in the Grand Lucky Draw when you successfully apply for participating products. Promo runs from 8 May, 5pm - 21 May 2024. T&Cs apply.

SingSaver's Exclusive Offer: Receive the following rewards when you sign up for a Citi Rewards Card (Team AirMiles):

Get a Dyson Supersonic (worth S$699) or Apple iPad 9th Gen 10.2 Wifi 64GB (worth S$508.30) or Dyson V8 Slim Fluffy (worth S$509) or S$400 eCapitaVoucher or S$300 cash via PayNow upon activating and spending a minimum of S$500 within 30 days of card approval. Valid until 15 May 2024. T&Cs apply.

Plus, upgrade your rewards when you top up S$999 for an Apple MacBook Air 13” (M3 chip) 256GB (worth S$1,599) or an Apple iPhone 15 Pro 128GB (worth S$1,664.25). Alternatively, top up S$1,488 for a Samsung Galaxy S24 Ultra Titanium Gray 12+512GB 5G (worth S$2,128). Valid till 2 June 2024. T&Cs apply.

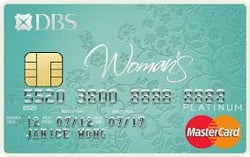

For the Online Shopaholic: DBS Woman’s Card

If you can't resist your shopaholic tendencies, then the DBS Woman’s Card will be your shopping best friend.

Why you’ll love it:

For starters, this card rewards you with 10X DBS Points per S$5 (or 4 mpd) spent on online shopping – and they even offer MasterCard e-Commerce Protection for non-delivery and damaged items!

Meanwhile, for eligible overseas purchases, that's up to 3X DBS Points per S$5 (or 1.2 mpd). If you're savvy with miles cards, you'd know that this overseas miles earn rate is comparable to that of most travel credit cards.

This card comes with a My Preferred Payment Plan, which combines and converts your major retail purchases up to a 24-month interest-free instalment plan with a low processing fee. And we’ve already mentioned the e-Commerce Protection!

And whenever you need a little retail therapy, it rewards you with DBS rewards points for your online purchases. With a spread of deals ranging from beauty and wellness, fashion, travel, dining and entertainment, the DBS Woman’s Card is hard to beat as an all-in-one card.

For the Culture Vulture: OCBC Arts Platinum Card

If you’re the girl in your friend group who’s always dragging people to theatre shows, art galleries, and performances, the OCBC Arts Platinum Card is for you.

Why you’ll love it:

Enjoy priority access to shows by Singapore Dance Theatre, Singapore Lyric Opera, and T.H.E Dance Company.

Also, you'll get to redeem tickets and invites to exclusive events, exhibitions and shows, and earn 15 OCBC$ per S$5 spent on SISTIC purchases.

Similar articles

The Best Credit Cards for Large Purchases in Singapore

Best Credit Cards for Online Food Delivery (GrabFood, Foodpanda, Deliveroo)

Best Rewards Credit Cards In Singapore: 2024 Comparison

Best UOB Credit Cards In Singapore

7 Reasons Why Men Should Sign Up for Women’s Credit Cards

Best Cashback Credit Cards In Singapore (2024)

How To Plan Your Credit Card Strategy For The Year Ahead, According to MileLion

Amazon Prime Day Happening on 11 & 12 July 2023, Offering Up to S$20 Discounts

Back to Blog

Back to Blog